Gold & Precious Metals

Gordon G. Chang

Beijing is planning to avoid U.S. financial sanctions on Iran by paying for oil with gold. China’s imports of the metal are already large, and you can guess what additional purchases are going to do to prices.

On the last day of 2011, President Obama signed the National Defense Authorization Act for Fiscal Year 2012. The NDAA, as it is called, attempts to reduce Iran’s revenue from the sale of petroleum by imposing sanctions on foreign financial institutions conducting transactions with Iranian financial institutions in connection with those sales. This provision, which essentially cuts off sanctioned institutions from the U.S. financial system, takes effect on June 28.

The NDAA gives the president the power to waive the sanctions depending on the availability and price of supplies from non-Iranian sources. He can also exempt financial institutions from countries that have significantly cut back purchases of Iranian petroleum. Last month, the State Department announced waivers for Japan and ten European countries. China, which has received American waivers in the past under other Iran legislation, is now Tehran’s largest oil customer and investor as well as its largest trading partner. Given the new mood in Washington, Beijing cannot count on getting more exceptions in the future.

As the Wall Street Journal noted in early January, the sanctions are “an attempt to force other countries to choose between buying oil from Iran or being blocked from any dealings with the U.S. economy.” The strict measures put Chinese officials in a bind. They apparently believe their geopolitical interests align with those of Tehran, but their economy is becoming increasingly reliant on America’s.

To Read More CLICK HERE

Brian Sylvester of The Gold Report

Last year, Africa was the region that witnessed the strongest growth in gold-mining operations. In an exclusive interview with The Gold Report, Nana Sangmuah, managing director of research with Toronto-based Clarus Securities, expects that trend to continue and suggests some immediate smart investments in Ghana, Mali, Liberia and the Democratic Republic of the Congo.

The Gold Report: Gold consultancy GFMS, which is now owned by Thomson Reuters, recently published its 2012 Gold Survey. GFMS predicts that before the end of 2012, the yellow metal will likely reach above its all-time nominal high of $1,920/ounce (oz) in September 2011. The catalysts include inflation concerns and sovereign debt problems in Europe, especially Spain. What are your thoughts on these predictions and conclusions?

Nana Sangmuah: I agree with those predictions and the drivers. One thing that has been missing from the gold rally is inflation hedge demand. With the significant monetary easing that has occurred to drive a global recovery, inflation is definitely going to be an issue at some point. We haven’t seen inflation trade come into gold throughout these 10+ years. That’s the strong headwind that is going to move gold to another level.

TGR: The survey reported that mine production hit a record high in 2011, rising 2.8% year over year to reach 2,818 metric tons (mt). That marks the second straight year that gold production reached a new all-time high. Does that mean the theory of peak gold is dead?

NS: Not exactly. If you peel back the data over the past two years, the greater part of this growth has come from mines digging into their stockpiles and people revisiting old resources that previously were thought not to be economic but at these price levels look economic. There have been very few discoveries despite the fact that there’s been quite a lot of money spent on the exploration front. That rate of increase is not sustainable going forward. And the bigger picture still looks grim because the last big discovery of 5+ million ounces (Moz) is the Aurelian discovery—the Fruta del Norte deposit in Ecuador, which now belongs to Kinross Gold Corp. (K:TSX; KGC:NYSE)—from early in the 2000s. It takes on average at least five years to move from discovery into production, so we’re looking at a situation where the supply is not going to grow that much. If the investment demand is sustainable going forward, basically there won’t be enough ounces to feed that demand.

TGR: The GFMS survey also reported that new gold-mining operations contributed 47 mt of new gold supply, while Africa was the region that witnessed the strongest growth, increasing production by 51 tons (t) despite a 5 t drop in output from South Africa. Do you believe Africa will continue to lead the way in worldwide gold production?

To Read More CLICK HERE

Dear Reader,

Vedran Vuk here, filling in for David Galland. Today, I’ll discuss the scenario of a European recovery. Would one mean that we’re finally out of the woods? I have a couple of other interesting pieces along with the Friday Funnies, so let’s get started.

What If Europe Does Recover?

By Vedran Vuk, Senior Analyst

Let’s play along with the economic scenario many market participants are predicting: a calmer Europe. If the continent does recover, is it time to put on the party hats and celebrate? Well, not quite. Sure, the pressure on equities would ease up, causing a brief rise in the market. But what then? Are we really out of the woods?

If Europe escapes this mess without a major crisis, those countries won’t come back at a screaming pace. Instead, the path to economic recovery will still be a slow crawl. Furthermore, China continues to have problems of its own. What started as talk of a Chinese slowdown is turning into real numbers. Sure, China isn’t doing horribly, but it’s hardly the hot market of a few years ago. The promise of never-ending growth with minimal risk just isn’t materializing. There are also other major players with mixed performances. With commodity prices cooling a bit, Brazil’s GDP growth is projected at 3.2% in 2012, a slight improvement from last year’s 2.7% growth. However, only a few years ago, predicting double-digit growth rates would have drawn no laughter, based on Brazil’s impressive 7.5% growth rate in 2010.

And then there’s the US story. The job market is improving at a snail’s pace… much like the rest of the world. If the euro crisis ends, it won’t mean a burst of growth for the US – but it could mean some additional headwinds. US Treasuries will no longer be shielded by buyers protecting themselves from the worst-case scenario. As soon as the coast is clear, Treasury investors will leave in droves, either flooding back into equity markets or higher-yielding euro countries.

To Read More CLICK HERE

»» Strong U.S. earnings continued to prop up a number of equity markets. U.S. stocks outperformed for the week, but Asian indices lagged.

»» China has become a bigger swing factor for earnings results of multinational companies.

»» First-quarter U.S. GDP growth of 2.2% indicates the economy remains locked in a sub-par zone, making dividend investing and stock selection that much more important. (page 2)

»» Global Roundup: Updates from the U.S., Canada, Europe, and Asia. (pages 3-4)

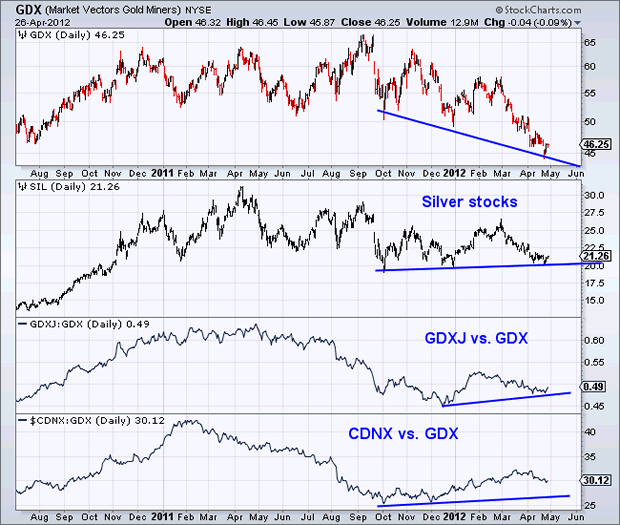

Jordan Roy-Byrne

While the precious metals sector has consolidated and struggled to find a bottom, an important development has taken place. First, lets harken back to 2007-2008. Large cap mining stocks peaked in March 2008, yet the speculative sides of the sector “gave out” far earlier. The juniors and silver stocks actually peaked in April 2007. That was about a full year ahead of the large gold stocks. As the 2007-2008 crisis unfolded, juniors and silver stocks led the way down and displayed extreme relative weakness even as metals prices were firm.

Today, we have an entirely different and bullish development. As you can see in the chart below, the speculative areas of the sector have been outperforming the large gold producers (GDX). If this were really an end to the bull market or another collapse, the juniors and silver stocks would not be showing this kind of relative strength. In fact, the silver stocks have actually managed to hold near their 2010-2011 lows even as gold stocks have broken to new lows. We also see that the CDNX has been outperforming GDX since October while GDXJ has been outperforming since December.

GDX (Market Vectors Gold Miners) NYSE

Given the recovery of the past few days, we are likely witnessing the start of the next cyclical bull market for the gold and silver stocks which have essentially been in a cyclical bear or correction since December 2010. The above analysis implies that the more speculative areas of the sector, the juniors and silver stocks will be the leaders.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair