Marc Faber : Well, I mean, you know, I’ve learned that what I know I obviously learned from someone. I didn’t invent it. So I worked at White Weld with Gary Schilling and he’s a friend of mine; I see him occasionally at the conferences and so forth. And I disagree with him about that we have deflation. He lives in New Jersey. I went to New York airport the other and day and then I drove to New York City and the Lincoln Tunnel fee has just increased from $8 to $14. Well, I’m sorry, that is a 50 percent increase. And so there is no deflation in the system today. But if you say there is deflation in the housing market, yeah, there has been deflation in the housing market and if you ask me will there be one day a deflationary collapse, yes, one day there will be a deflationary collapse, but you understand, as an investor it’s nice to say there will be a deflationary collapse, but it could happen from Dow Jones 100,000 or gold price 20,000 or from home prices that are much higher than today and from a dollar that has depreciated much more than is the case today. So the difficulty for the investor is actually to navigate between today and the time of collapse that I think is inevitable. But how do you protect your wealth in the meantime and in the time of collapse? Investors, and I think they have to begin to think about this already today and say, okay, what does it mean if there is a global kind of deflationary collapse. In a deflationary collapse, everything essentially goes down in value, but obviously, like in an inflationary boom, in an inflationary boom you have different assets that go up at different times with different intensity. So let’s say if you look at 2000 to today, you were better off in gold and commodities than in equities. Now, in a deflationary collapse, the key is to say, okay, I’m only going to lose 50 percent when everybody else will lose 90 percent. So relatively speaking, I will be much better off. And that is the strategy that investors should consider: How to position themselves to lose less in the deflationary collapse in the final crisis than the majority of people. Then relatively to other people, their position will improve.- 06 Apr 2012

Stocks & Equities

Perspective

The stock market is included in the orthodox calculation of Leading Indicators. Problem is that at the end of a great financial bubble, such as in 1929 and 1873, the recession started virtually with the collapse of speculation, which was also the case in 2007. This is one of the features of a bubble and its collapse. Stocks peaked in October 2007 and the recession started in that fateful December.

Essentially, both the stock market and the economy recovered when the panic ended in March 2009. We have thought that the relation would continue such that the first business expansion out of the crash would end with the end of the first bull market. It should be admitted that we had thought that the US expansion would end with the commodity-high of last April. Usually we leave the discussion about recoveries and recessions to the cult of economics, but sometimes it’s worth a try. After all, the NBER typically determines the start of the recession – one year after the actual start.

Naturally, we can’t help but wonder if the life that recently came into the economic numbers will turn down with the stock market – with little delay. Taking out 1340 on the S&P would set the downtrend. What would set the downtrend in GDP?

A couple of weeks ago central bankers were comfortable that stimulus and fixes had – well – fixed things. No more easing was required. Then, this week’s hit to the markets seems to have dislocated policymaker confidence such that Bernanke had to state that he would not raise administered rates. Our view has been that it has been market forces that have lowered such rates. In troubled times conservative funds go to the most liquid items and they are short-dated instruments in the senior currency and gold. This drives the former down in yield and the latter up in price.

The swing in Fed opinion reminds of Tokyo at its extraordinary peak at the end of 1989. Speculation was radical and policymakers were trying to talk the action down – which is always impossible because such speculation will run to collapse. With the initial break in the Nikkei, policymakers became nervous and talked about lowering margin requirements. Shortly after the top of a bubble??? Japan’s subsequent contraction has been one for the history books.

Our “new financial era” recorded a number of cyclical speculative thrusts and cyclical bear markets until a classical bubble was accomplished in 2007. Despite easing that exceeds the determined efforts by the Fed at the start of the post-1929 contraction,

financial history remains on the typical post-bubble path. One could even say that central bankers have been extremely belligerent in attacking the normal forces of contraction.

However, sovereign debt markets are saying that it is not working well. An updated chart on the “Spanish Fandango” follows.

CREDIT MARKETS

With the break in overall confidence, the long bond jumped almost 5 points in three trading days. Junk, high-yield bonds, and sovereign debt sold off. The sub-prime which had rallied from 38 in October to 52.5 in February has slumped to 47.4. The chart has broken down and the target is the 38 of last October. Municipals are close to ending their test of the highs in February.

This year’s seasonal reversal to widening in May could lead to very unsettled credit markets later in the year.

The long bond was oversold and the bounce has corrected this condition and the price is likely to drift down to test the low.

Action in lower-grade stuff has not been healthy, and an economist at an orthodox place (IMF) has discovered that there is not enough collateral behind all of the debt. In Victorian times this was called “over trading” and today its “leveraging”. No matter what the term, it is always followed by liquidation or in today’s terms “de-leveraging”. The next stage could inspire articles that it is impossible for the world’s economy to generate enough income to service the debt burden.

There will be plenty of opportunity for a “new” wave of young economists to point out the glaring blunders of the ancient and “barbarous relic” of interventionist economics.

Commodities

Base metals and crude oil declined enough to prompt a rebound with the Fed turning on the speculation switch again. Neither were oversold enough to set an intermediate bottom. Natural gas got headlines in declining below $2.00, but it is not as oversold as at the 2.23 low in January. Also, late April often sets a seasonal high.

Agricultural prices suffered a hit last week, but not enough to break the chart out of the narrow trading range. Coffee clearly needs a jolt as it has given up most of the huge gain to April last year. It seems that the sector is being keep together by strong action in soybeans and soybean meal. These are becoming rather overbought at close to last year’s highs.

After mid-year, adverse credit spreads, a slowing global economy and a firming dollar could trash most commodities – again. The chart shows three “over-boughts” – at 474 in 2008, 370 last April and at 326 in February.

Currencies

Bernanke renewed his vows to depreciate the dollar, which brought the DX back into its trading range. However, this is still within the pattern leading to a significant advance.

Getting above overhead resistance at 81 could set the launch button. For day-traders May is a long time away, but for investors it is nearby and could record a reversal in credit spreads and forex markets.

BOOM SAYERS to OOOPS!

Signs of the Times:

We ran “Boom Sayer” exclamations for four weeks and considering the nature of volatility it is reasonable to conclude that current excesses will eventually be followed by “Doom Sayers”.

But, let’s not be hasty – usually the next step from complacency is “Ooops!”.

And that might have begun with this week’s discovery that the “fix” on Euroland debt won’t last as long as even the shorter maturities become due.

Pity.

This Year

“The biggest wave of state-and-local government debt refinancing in two decades is helping fuel the longest winning streak for municipal bonds since 2007.”

– Bloomberg, April 2

“Taxable municipal bonds are poised to extend their best rally in 18 years.”

– Bloomberg, April 4

“Across the Eurozone, and beyond, hedge fund managers are now pointing to ‘significant’ pricing anomalies not seen since 2008.”

– Bloomberg, April 6

“JP Morgan trader of credit-derivative indexes [linked to the health of corporations] has amassed positions so large that he is driving price moves in the $10 trillion market.”

– Bloomberg, April 6

Of course, these preceded Tuesday’s setback, but their significance is that there is considerable speculation in credit markets. As we have been noting, favourable trends in corporate spreads ended in February. This could reverse to widening over the next four to six weeks.

As we have been noting, “Boom Sayer” exclamations from March and April last year were remarkably similar to this year’s list. The best of last year’s have been published and, essentially, they ended in April, which suggests a pattern.

Stock market action in both years set a momentum high in February with positive sentiment recorded in March and April – accompanied by bullish raves.

This week saw some “sudden” exclamations of dismay. Does it indicate a new trend?

Link to April 13 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2012/04/gold-gloom/

“The question is not whether this is a correction, the correction has got underway. We may easily have a correction of 10% to 20% here.”

also:

Marc Faber : There is no Deflation in the system today except in the housing market

Quotable – “The darkest places in hell are reserved for those who maintain their neutrality in times of moral crisis.” – Dante Alighieri

Commentary & Analysis

[Warning: I am feeling a bit dark this week. So if you want to join me in depression, feel free to read. Otherwise, skip this one. Thanks. Jack]

I finally figured it all out. Our global policymakers are nothing more than Wizard of Oz aficionados (the movie as the book is way over their collective heads). They just love happy endings. Let’s just get all the little people to follow down the yellow brick road and it will all turn out just fine, our pols want to believe.

Of course our politicos’ fairy tale is validated each day by those they love the most–the big people leading us down this path–financial types (defined as anyone who benefits from the financial world, not the real world). It is what it is. Big people are big for a reason. And the big people want that path paved with yet another layer of green paper. Simple!

What is this talk of recession, say the big people? And they say it with their Super Pacs and $40,000 –$50,000 a plate dinners to help elect the top Republicans and Democrats (read totally vetted shills who pledge behind closed doors to keep the status quo the status quo; nothing more than different colored horses from the same stable it seems to me). After all, the financial economy is doing just fine; great in fact, is the refrain from Mr. Financial Big Whig.

But even Mr. Financial Big Whig has a few laments: 1) The price of houses in Greenwich or London; 2) His driver’s parking problems in Davos last year; and 3) The damn 5-minute wait in line at the lift in St. Maritz. What is this recession crap?

I asked JR yesterday (as we watched the local news of Mitt Romney in Palm Beach for a reported $50k a plate stop-over); who is more sickening, the shills panhandling for $40-50k a pop or the crony-istic dregs who actually pony up that much? Decisions, decisions….

To say it is a bifurcated world culturally and materially is to understate the obvious. It is bifurcating down the path of the financial economy versus the real economy, to a large degree. [And if you read Charles Murray’s new book, you get a very bad feeling in the pit of your stomach as to where this is leading.]I realize it is what it is and always has been. But watching it all play out so transparently with such hubris flowing from the top makes it that much more revolting. For example, a bit off point, but if are disgusted with US politics, you have to be stunned to watch the US State Department chastise other countries about the need to “improve their election system”? What a farce! Sorry. These dark thoughts creep in whenever I consider hedge fund managers and pols in the same sentence.]

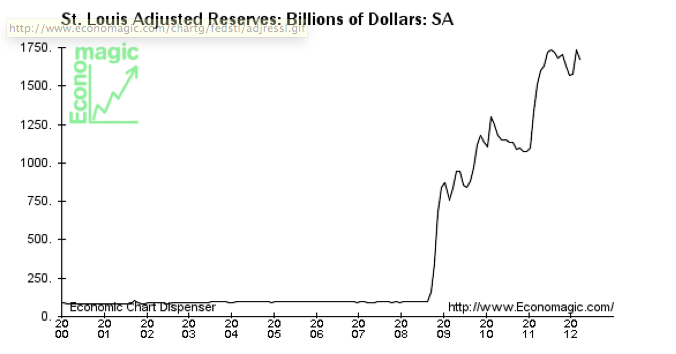

Back to point, assuming I have one here. Joseph Goebbles would be proud of our central banking wizards. Goebbles, the Nazi propaganda chief, understood the big lie told again and again will sooner or later be believed as truth. All Pols follow this theory. But even Goebbles would be stunned to see how often the Big Lie is used by central banks as the truth stares everyone in the face; the face of those who know how to find US Banking Reserves as listed by the St. Louis Feds research department:

1. If Fed liquidity worked the US would be in the midst of the biggest post-recession boom in history. Instead, we are in the slowest post-recession recovery since Stalin-loving Roosevelt stacked the Supreme Court. Let’s let the reserves speak once again for themselves:

If real growth is taking hold, we should have seen a fall in all these reserves sitting on bank balance sheets.

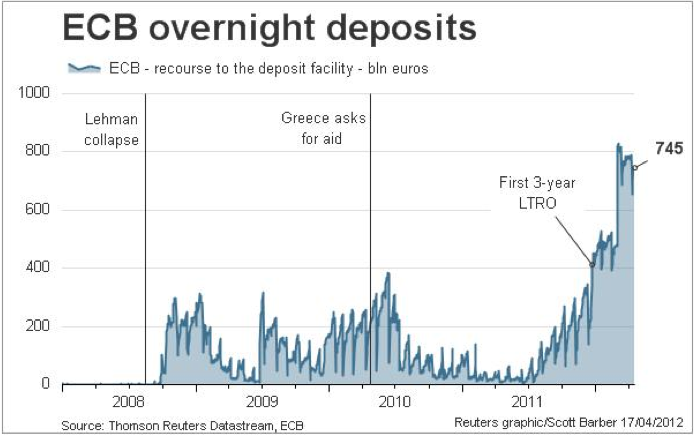

2. Déjà vu all over again from the ECB. Gee, it did nothing for the US real economy, so why don’t we try it here in Europe, say the Wizards running the European Central Bank (ECB).

The argument to my rant is obvious: So what would you do Jack, let the banking system go bankrupt? Well, yes I would, thank you for asking. One by one and every stinking banker who led his firm down the prim-rose path of derivatives would be history. Super-regional managers would step up to the plate and take their turn. After all it is the regionals and local banks that really know what banking should be anyway…credit and relationships. It isn’t rocket science. [Just look at how massively the powers-that-be, pols and their handlers in the banking system, have attacked Paul Volcker’s very good ideas of what banking should be. Nothing has changed!]

There’s an evenin’ haze settlin’ over town Starlight by the edge of the creek The buyin’ power of the proletariat’s gone down Money’s gettin’ shallow and weak Well, the place I love best is a sweet memory It’s a new path that we trod They say low wages are a reality If we want to compete abroad

My cruel weapons have been put on the shelf Come sit down on my knee You are dearer to me than myself As you yourself can see

While I’m listening to the steel rails hum Got both eyes tight shut Just sitting here trying to keep the hunger from Creeping it’s way into my gut

Meet me at the bottom, don’t lag behind Bring me my boots and shoes You can hang back or fight your best on the frontline Sing a little bit of these workingman’s blues

Well, I’m sailin’ on back, ready for the long haul Tossed by the winds and the seas I’ll drag ’em all down to hell and I’ll stand ’em at the wall I’ll sell ’em to their enemies I’m tryin’ to feed my soul with thought Gonna sleep off the rest of the day Sometimes no one wants what we got Sometimes you can’t give it away

Now the place is ringed with countless foes Some of them may be deaf and dumb No man, no woman knows The hour that sorrow will come

In the dark I hear the night birds call I can feel a lover’s breath I sleep in the kitchen with my feet in the hall Sleep is like a temporary death

Bob Dylan, Workingman’s Blues

At some point, this game must end. The financial world CANNOT continue to widen its gap with the real world ad infinitum. Sooner or later, I think we will learn the path to hell, not Oz, is indeed paved with green paper.

Jack Cooks Black Swan www.blackswantrading.com Currency Currents Blog

Black Swan Capital’s Currency Currents is strictly an informational publication and does not provide personalized or individualized investment or trading advice. Commodity futures and forex trading involves substantial risk of loss and may not be suitable for you. The money you allocate to futures or forex trading should be money that you can afford to lose. Please carefully read Black Swan’s full disclaimer, which is available at http://www.blackswantrading.com/disclaimer

By John Rubino on April 17, 2012

The in-laws own a gas station in Miami that they’ve wanted to sell for years. But they dithered when the market was hot and ended up being stuck with it when interest evaporated in 2009.

Lately, though, the phone has begun to ring again. It’s not exactly a feeding frenzy but real offers are coming from legitimate buyers for the first time in three years.

That’s actually a pretty good description of real estate in general, where low interest rates have convinced a growing number of people that it’s time to buy. See this upbeat story on the home builders:

Pulte, Lennar jump as survey shows housing rebound

NEW YORK (MarketWatch) — Shares of U.S. homebuilders rallied on Wednesday after a Wells Fargo analyst’s research report said data from 20 select markets nationwide are showing strength across the board.

“For the third consecutive month, our survey points to an improvement in orders suggesting 2012 may be the long-awaited recovery year for housing,” the note said.

PulteGroup PHM -1.39% added more than 8%, Lennar Corp. LEN -1.47% gained 5%, D.R. Horton DHI -2.44% rose 4.2% and Toll Bros. TOL -0.86% gained 3.8%.

The bellwether industry ETF, the iShares Dow Jones U.S. Home Construction Index Fund ITB rose 3.4%.

Wells Fargo’s monthly Neighborhood Watch Survey, which tracks 150 sales managers at housing tracts in 20 markets, showed that March results were strong across all measured metrics. In particular, the survey noted that March’s numbers surpassed poll participants’ expectations by the widest margin since the survey started, in 2001.

Wells said that pricing in the 20 markets also improved, both month-to-month and over year-ago figures. Sales managers’ commentary on market activity indicated that buyer confidence seems to be improving as inventory shrinks.

“Sales managers suggested there is a sense of urgency in the marketplace as buyers anticipate higher home prices and/or mortgage rates,” the report said.

Bidding wars are even returning to some markets:

Market squeezing homebuyers

Home shopper Dian Schneider was four houses in on a whirlwind tour of local homes for sale Friday when her real estate agent issued her a warning.

“Now if you like this one you’ll need to move today because there are already two offers on it, and they’re both above list price,” said Anna Hernandez of McKinzie Nielsen Real Estate. “They’re not crazy high, but you’ll have to go in high, too, if you’re serious about it.”

Schneider nodded knowingly as she peeked inside closets, flushed toilets and opened cabinet doors.

The 50-year-old single mom had already missed out on two homes she’d made offers on. She was outbid on one, and pulled out of a second over concerns about its dated electrical system.

“In hindsight, I probably should have taken that one,” Schneider said.

Almost all the available inventory in her price range is badly in need of repairs, and upgrading the electrical on the home she passed up wouldn’t have cost as much as she’d assumed, she later learned. But back then, she didn’t fully appreciate how lucky she’d been to find something.

The Bakersfield area had only 583 single-family homes for sale in March, about a third fewer than in March of last year.

Bidding war return

The result has been fierce bidding wars and almost immediate turnover for anything of quality that’s priced reasonably, whether it’s a modest starter home or a mansion.

“Everybody’s pretty much in the same boat right now, regardless of price,” said Robert Morris, who sells for Watson Realty ERA. “The supply keeps dropping and dropping and there’s nothing replacing it.”

Broker Nancy Harper of Nancy Harper Realty recalled listing a home the day before Easter. By Easter Sunday, it had six offers on it, and when she called the losing agents to tell them their offers had been rejected, two of them burst into tears.

“They told me they’d written something like 14 offers for clients and just couldn’t get one accepted,” Harper said. “When you have agents bursting into tears, boy, that’s low inventory.”

So is the housing bubble back?

To Read More CLICK HERE

Source: Brian Sylvester of The Critical Metals Report

Simon Moores Graphite is the Next Big Thing for resource investors, but as in any sector, due diligence is a prerequisite for success. Enter Simon Moores, graphite market specialist with Industrial Minerals in London. In this exclusive interview with The Critical Metals Report, he explains why graphite is “the perfect mineral,” why we’re still going to be talking about it years from now and which companies to watch in this emerging industry.

Companies Mentioned: Archer Exploration Ltd. – Focus Metals Inc. – Imerys – Northern Graphite Corporation – Strategic Energy Resources Ltd. – Zimtu Capital Corp.

The Critical Metals Report: You once called graphite the perfect mineral. Why?

Simon Moores: It’s conductive; it’s a lubricant; it’s resistant to high temperatures and it’s a strong mineral. This means it doesn’t have just one major market; it has an abundance of markets and uses. It’s key to existing technologies that have been around for 100 years as well as new technologies, like lithium-ion batteries.

But despite what many think, it’s not a niche industry. Rare earths and lithium are niche industries. Each year, 1.1 million tons (Mt) of graphite is produced. It’s bigger by volume than molybdenum, vanadium, cobalt, tungsten, rare earths and lithium combined.

Graphite miners operate all around the world in Canada, Brazil, Europe, India and, of course, China, which accounts for 80% of production. That’s a new figure that our research at Industrial Minerals has just uncovered for the new Natural Graphite Report 2012. China’s grip on graphite production is greater than people thought previously.

TCMR: What is China’s next move in the graphite market? Do you think there will be more quotas and export restrictions?

SM: There are no rare-earth style quotas at the moment. China doesn’t say, “We are only allowing 400,000 tons (t) of graphite to be exported every year.” But the country is doing things that could restrict the raw materials supply. The government doesn’t like exporting raw materials that other people make money from. It is trying to build a value chain to unlock the value in its natural resources.

For example, China exports flake graphite to Japan. Japan turns it into battery-grade graphite, which is then used to make anodes, which is then used to make batteries, which Japan then ships for a much higher cost than the raw graphite. Now China is trying to build those finished products domestically. As a result, less raw material will come out of the country. In addition, China is trying to control its sprawling mining industry by forcing consolidation. Graphite is a perfect example of a sprawling Chinese mining industry.

TCMR: China is already encouraging foreign companies who depend on rare earth elements (REEs) to set up shop in the country. Do you see the same story unfolding in the graphite industry?

SM: The difference with rare earths is that China is the only place you can get good supply. It operates the world’s only mine in Inner Mongolia until Molycorp and Lynas truly get underway.

China is aware that companies can get graphite elsewhere. It is also aware that at the moment it makes good business sense to sell quality raw material at high prices for the short term. Longer term, the story is different.

TCMR: China’s had environmental problems with some of its rare earth operations. You visited some graphite mines in China. Are the graphite mines environmentally problematic?

SM: No, it’s basic mining that has been around for centuries—extracting from the ground, crushing and grinding. You then put it in a floatation tank with reagents. This part of the process requires chemicals, but these are well known chemicals used in many other industries. Finally, graphite processors dry it and bag it. Graphite is an inert mineral, so it’s not harmful. There are no underlying environmental problems in graphite mining.

The only area that holds some controversy is processing into spherical graphite, which requires additional chemical and physical treatment. Acid treatment is quite intensive and there could be future controversy surrounding the disposal of acids used.

TCMR: Are the Chinese mines primarily producing large-flake graphite or a lower-end product?

SM: It’s almost a 50-50 split. Flake graphite mining exists all the way down the country’s spine. This is good-quality material suitable for both domestic and international refractory and battery markets.

The Hunan province, in the south, is home to amorphous graphite, the old-style graphite people first started mining around the world. Amorphous is more common because the graphitization is lower and closer to coal, whereas flake graphite is closer to diamonds. Amorphous graphite supplies lower-end markets that produce products like pencils and lubricants.

TCMR: You describe the graphite market as having “layers” of demand. What does that mean?

SM: When graphite first came into use, it was mainly employed in lubricants and pencils. Those were the primary demands until after World War II, when the steel industry, driven by construction, became an additional end user, forming a second layer that boosted demand by about 30%. In the 1960s, the auto boom and car construction, especially in North America and Europe, formed yet another layer. Throughout graphite’s industrial history, new technologies keep emerging while demand from traditional industries hasn’t dropped off. This has built graphite into the 1.1 Mt industry it is today.

TCMR: Are there any graphite substitutes for these new technologies?

SM: Synthetic graphite is a substitute. Cost is still prohibitive, and people prefer flake graphite’s properties. Batteries, for example, require a good porosity and surface area so the lithium ions can flow through the anode and generate the charge. Man-made graphite doesn’t really provide that.

TCMR: What are some characteristics of an economic graphite deposit?

SM: The carbon content throughout the deposit is very important. A lot of companies are reporting the top range of carbon content, but because mining needs to stretch over many years, carbon content needs to be consistent throughout and not just good for three months.

The type of graphite is critical—flake and vein graphite are the best. Flake is the good stuff. Vein graphite is even better—it is found in lumps in the ground and is “cooked” by long geological processes. It is the form closest to diamond mineralization, and for this reason is much rarer, only found in Sri Lanka today.

A third key factor is infrastructure. Transportation makes up a large portion of the costs of large-scale graphite production. Currently, graphite is going through a high price peak, so existing producers are enjoying themselves. Producers have to prepare for the worst: If the price comes back down to perhaps half of its current market value, a producer’s logistics are critical because that’s where it either spends a lot of money or saves a lot of money.

TCMR: We didn’t hear much about graphite even a year ago, certainly not from publicly listed companies. Are we still going to be talking about graphite in three years?

SM: We will. Lithium is a perfect comparison, because, in 2009, it had the same boom graphite is now having. In 2010, it reached a peak. Lots of juniors entered the industry. Everyone got excited about it. In 2011, nearly all of the juniors fell away, and the remaining players were focusing on their projects and not making as much noise. This year, we’re seeing consolidation in the industry. Graphite will follow the same pattern.

TCMR: Has the boom in the price of high-quality graphite over the last year or so surprised you?

SM: Not really, because you have to look at the fundamentals. Graphite supply has been neglected for a generation yet it’s still used in a lot of growing markets. Graphite’s demand security is in its diversity: when one market drops off, another steps up.

When you only have this situation with a handful of active mines and no new operations planned, then there’s only really one outcome: Eventually prices are going to rise, because there’s going to be a supply squeeze. China adds a huge element of future supply uncertainty as well.

TCMR: The last graphite boom was in the 1990s. But then prices fell, and a number of mines were mothballed. Who’s to say that won’t happen again?

SM: It could happen again. That’s always the risk, when you have so many potential mines coming online.

China caused the bust in the 1990s. New producers flooded the world market and put a lot of people out of business with low-cost production. Today, in a twist of fate, China could now be the cause for making these mines viable again. We have to look at how much production China controls, and its long-term goals, what it wants to do with its economy and its raw materials. Any new bust, however, is not going to be as drastic as the one in the early 1990s.

TCMR: One of the graphite derivatives that is very misunderstood is graphene, which is a single layer of graphite that is created in labs. How close is the industry to commercial-scale graphene production?

SM: The industry is some way off. A Google search will throw up many companies claiming they can produce graphene. But I wouldn’t call it graphene—I’d call it nano-graphite. There may be three, four, five layers of graphene in their products.

Graphene is used in intelligent inks, for example, which are used for security systems on bank cards. That’s its first market, and others may emerge in the next few years. But I believe the production of true graphene is many years away—commercially producing true graphene one-molecule thick—is extremely challenging, one of the biggest materials scientists will face. But if they crack it, the possibilities for its use are almost endless and it would revolutionize they way we live our lives. But to get graphene’s super properties we all read about, you need to peel away and isolate a one-molecule layer. It’s almost impossible to do that on a commercial scale. In terms of serious large-scale commercial use, it’s at least 15 years away, and predicting 15 years into the future is like trying to predict 1,500 years into the future.

TCMR: Will the steel and battery industry end users drive another layer of graphite’s growth?

SM: Yes. The steel industry uses refractories, which are protective layers for vessels that hold molten steel. If you pour molten steel into metal, it’s going to melt through. So refractories are lined with bricks that can handle extreme temperatures. A big component of brick is graphite—up to 15% per brick. The steel, cement, petrochemical, glass and ceramics industries all use graphite in this way.

TCMR: What about lithium-ion batteries for electric cars—that’s a significant amount of graphite in those products, too, correct?

SM: Electric vehicles are not a big demand driver today. But that’s where the potential lies. In an electric car battery 1.8 kilograms (kg) graphite is used per kilowatt hour (KWh). Then take a battery pack equating to 24 KWh (like Nissan’s LEAF), that’s 38kg natural graphite per battery. It’s a long way off, but if a manufacturer were to sell a million of these cars, that amounts to 3.8 Mt natural graphite. The natural graphite market is 1.1 Mt a year at the moment. So you can see why people are excited about it.

TCMR: What are some companies with graphite projects that could fill the supply gap for natural graphite, especially large-flake graphite?

SM: I’d look first at the companies that are actually producing graphite now. There’s Timcal Ltd., which is publicly traded by Imerys (NK:PA), based in Paris. Imerys is a big minerals company; graphite is just one small area of its business. But its mine in Quebec is the only major active mine in North America. In December, Imerys announced plans for three new mines in the area, which shows that existing companies have the ability to do it straightaway.

TCMR: Canada in general seems to have a lot of potential for economic graphite deposits.

SM: Exactly. It’s got a handful of leading juniors: Focus Metals Inc. (FMS:TSX.V), Northern Graphite Corporation (NGC:TSX; NGPHF:OTCQX), Ontario Graphite Ltd. (private) and Mega Graphite Inc. (IPO expected by the end of Q112).

Focus Metals’ primary graphite operation is the Lac Knife deposit in Quebec. The deposit is famous and has been on our radar for more than 20 years. It’s a large, high-quality graphite deposit with about 8.1 Mt flake at 16% average carbon content, which is strong. And the company is investing in technology to make graphene, which sets it apart.

TCMR: How close is that project to production?

SM: It’s at least two years from production, the same as any other new junior. Building a new mine anywhere in the world is never a quick process.

TCMR: Let’s move on to Northern Graphite, the darling of the industry. It was publicly listed last year, and the trajectory has been steadily upward.

SM: Its Bissett Creek project in Ontario is great. Northern Graphite has been around for a while, under different names. Bissett Creek has also been on our radar for a long time – before others were interested in graphite, work was being conducted on the deposit which says a lot for its quality even in down times. The company has ramped up drilling and marketing activities in the last two years.

Northern Graphite’s selling points with its project are the size of the flake and the purity of the carbon content. The company, like many others, still needs the funding to build the mine. That’s the challenge for all these juniors in Canada. Bissett Creek is still a very good project. You can’t deny that.

TCMR: Northern Graphite is also doing some research on graphene—what do you make of that?

SM: It’s a new battleground for some of these juniors. They’re battling not only for funding but for share of the headlines. Any company with a high-quality graphite deposit naturally lends itself to mechanical exfoliation production of graphene.

TCMR: The other junior you mentioned is Ontario Graphite, which has a project not far from Bissett Creek.

SM: Ontario Graphite is a bit different, because it’s a mine-reactivation project. For that reason, I would think that it will be quicker to bring production onstream. The company will need a new plant and new equipment, which is relatively straightforward to install. It is scheduled for commissioning in September this year. I could see Ontario Graphite processing product within 2012. The resource is also a good size—43.5 Mt Measured and Indicated resources, 12.3 Mt Inferred resources.

TCMR: Are there enough metallurgists available to create the end product?

SM: Yes. It’s not like the rare earth industry, in which North America lost all its intelligence and skilled workers. Graphite has been a consistent, worldwide mainstay, which means the knowledge base has been retained thanks mainly to U.S.-based companies like Asbury Carbons and Superior Graphite. The challenge may lay with higher-value graphite grades for the battery market. Spherical graphite is a key raw material for battery anodes and this is still a new process for everyone.

TCMR: You also mentioned Mega Graphite.

SM: Mega Graphite bought an Australian company called Strategic Energy Resources Ltd. (SER:ASX) and that gave it a fast track route into the graphite industry. Its Uley Mine is actually a big stockpile of processed and unprocessed material because, similar to Ontario Graphite, back in the early 1990s the mine was closed. It wasn’t economical enough to compete with cheaper products from China.

Mega Graphite has upgraded the plant with modern equipment and is reprocessing the stockpiled material to make the various grades of graphite. It has the potential to produce about 20,000 tons good-quality graphite from that stockpile over the next three years. But it will need to start mining to replenish these stocks.

TCMR: Is there a significant mining industry in Australia? Will Mega Graphite and Strategic Energy face some competition?

SM: At the moment Australia has no graphite mining industry. Zimtu Capital Corp. (ZC:TSX.V) is buying up a lot of deposits there and has an impressive portfolio of assets around the world. Archer Exploration Ltd. (AXE:ASX) is another company that has a project as part of a larger portfolio of mineral assets. But Mega Graphite is far more focused on producing graphite so the company shouldn’t encounter much production competition in the near term.

TCMR: What’s the infrastructure like at Uley?

SM: It’s fine. Australia is mining friendly. It is used to this kind of industry.

TCMR: It’s not going to face any mining royalties there? Australia has implemented one on iron ore and coal.

SM: Australia will try to target its big businesses like iron ore and coal. Graphite is never going to be a comparatively big business there. If Australia heavily taxes the smaller mining companies, then it won’t have much of a mining industry left. It needs to encourage these. Mining is the sole reason Australia didn’t slip into recession.

TCMR: What advice would you give to investors who are interested in the graphite story?

SM: The resource is everything. The larger the flake and the higher the purity of carbon the more critical it will be to high-tech applications. Also look at what the company’s plans are for selling this material and if it is targeting specific markets—co-operation with Japan and South Korea will be key here. Traders from these countries are usually the most savvy of long-term investors.

The most interesting graphite plays are those that are focused on technology end uses. Producing high-tech-compatible materials for emerging markets, like spherical graphite for batteries, will add the serious value.

Industrial Minerals is working on the Natural Graphite Report 2012, which should be out in the next two months. It’s an extensive world overview of production, prices and demand and should answer any more questions readers may have.

TCMR: Thank you for speaking with us today.

SM: My pleasure.

Simon Moores has been reporting on, researching and analyzing the non-metallic minerals sector since 2006, when he joined London-based publishing and research house Industrial Minerals. He has specialist knowledge in critical and strategic minerals including graphite, lithium, rare earths and titanium.

He led the research and publication of the market study, The Natural Graphite Report 2012: data, analysis and forecast for the next five years. One of the study’s key findings was China’s dominance of production was significantly higher than previously thought, accounting for 80% of supply. He has chaired conferences and given keynote presentations around the world. He has also been interviewed by international press including London’s The Times regarding Chinese control on world graphite production, and The New York Times with regard to rare earths after breaking the story that China blocked exports to Japan in 2009.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair