Bonds & Interest Rates

Written by: The Inflation Trader

The phrase “paradigm shift” is meant to sound dramatic. Like the sudden slipping of tectonic plates, a paradigm shift moves mountains (metaphorically). Deregulation of airlines caused a paradigm shift, transforming airplanes from airborne luxury cruises to cattle cars. Decimalization of equity bid/offers caused a paradigm shift, dropping bid/offer spreads about 90%.

Economic paradigm shifts can also be dramatic, as when the credit crisis of 2008 caused lending to contract almost overnight. But not all shifts are dramatic. The paradigm shift from horse-drawn carriages to ‘a car in every garage’ brought the world dramatically closer together. But it took a long time before it happened…before, anyway, it was obvious that it had happened. The paradigm shift was clear in retrospect, but not in prospect. It wasn’t as if people were waiting for the world to change: Henry Ford famously said that if he’d asked his customers what they wanted, they’d have said “faster horses.”

Core inflation, by its nature, rarely produces good surprises. Friday’s release was a case-in-point. Forecasters were looking for a +0.2%, and got a +0.2%, but they were actually looking for about +0.17% and got +0.23% instead. It doesn’t even look like a surprise, when the rounded data is announced, but it assuredly was one. The y/y core CPI, which decelerated last month for the first time in 16 months, rose back to 2.3% (although just barely, and shy of the high from January), after last month’s decline had produced a chorus of predictions that core CPI for the year would end up being in the low-to-mid 1% range.

It is hard to imagine that, following the 2008 collapse of Lehman Brothers, there were very many who didn’t see the paradigm shift. On the other hand, Henry Ford churned out millions of Model Ts before the wagon-wheel manufacturers went bust. Could we be in the midst of an inflationary paradigm shift without knowing it? Put another way, does the fact that many economists deny such a shift imply that there isn’t such a shift? Well, would the fact that many analysts still projected record profits for buggy-whip producers, which could plausibly have happened if our current research structures existed back then, have implied that there was no revolution happening in locomotion? I personally think it would have been very remarkable if an analyst covering such companies had deduced that the Ford (F) development would change the demand/supply balance for automobiles in such a dramatic way.

To Read More CLICK HERE

The bond market traded in a fairly narrow range last week, as it held key support at 140 through the period. The 10 Year Treasury Note yield is back below 2% again, kicking around the bond bears in the process. There was no renewed talk of QE3 from any talking Fed Heads, but the nervousness in stocks coupled with rising European Sovereign yields was more than enough to provide solid support for bonds in spite of the heavy issuing calendar and negative seasonal influences. The auctions last week were mediocre, but good enough not to cause any concern. Traders were astute enough again to take down the 30 year tranche at the lowest prices of the week. The bond market was relatively stable considering the roller coaster we had in stocks and a few other things. Stocks and bonds are quite close to fair value. So there is no compelling reason to stick our neck out on that front other than the momentum that is rolling from stocks into bonds.

For the past couple of months I’ve been anticipating that the rally in “risk assets” would run out of steam but I have been waiting for confirmation…I think we are seeing that confirmation over the last two weeks or so…trade accordingly.

Over the past couple of years I’ve frequently asked the question, “What are we trading?” And my answer has been “perceptions of central bank liquidity.” I think the rally in stocks since the lows of Oct 4 has been fuelled by liquidity injections from the G4 (US, Euro, UK, Japan) and by anticipation of more liquidity injections to come. These injections have created false optimism in the markets.

The LTRO injections in the Euro zone in Dec and Jan created a “Lull” in the Eurozone bank/sovereign debt crisis….it appears the “Lull” is over as yields rise on the weaker credits, Spain in particular. I think we will see stress build in Europe in reaction to austerity programs, weak economies, elections, and high unemployment. The weaker Euro countries are headed into a vicious cycle of faltering economies and higher interest rates. Social unrest will rise, populist politicians will call for “re-negotiations” and possibly a withdrawal from the Euro.

The S+P 500 and the DJI made a “M” double top around the end of March/early April with (very nearly) perfect weekly key reversals down last week…both have fallen ~3.5% from last week’s highs to today’s close.

The psychology change this past week was interesting. Stocks fell sharply on Monday in response to the weaker-than-expected UE data released on Easter Friday. On Thursday, stocks rallied sharply on anticipation of fresh Fed liquidity injections (two Fed Governors made dovish speeches) but today those gains were reversed as the Euro crisis moved back to centre stage.

To Read More CLICK HERE

![]()

By Dave Gonigam

Gold is ending the week doing a little more backing and filling. After yesterday’s run-up, the spot price has pulled back to $1,665.

$2,000 looks far off in the distance. To say nothing of last September’s $1,900 high.

Then again, it could happen with the snap of a finger.

“A push on toward $2,000 is definitely on the cards before the year is out,” says Philip Klapwijk, “although a clear breach of that mark is arguably a more likely event for the first half of next year.”

Mr. Klapwijk is global head of metals analytics at the consultancy Thomson Reuters GFMS. The catalyst for $2,000 might well be, in his estimation, Spain. A meltdown there — coupled with continuing strong demand from China — could give gold a whole new “safe haven” glow.

That said, he also sees a short-term dip to the year-end 2011 level of $1,550 within a couple of months. You’ve been warned.

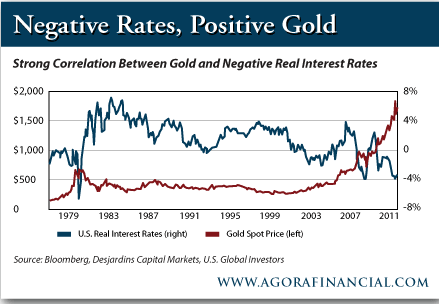

“U.S. investors might sleep better at night with an allocation to gold in the face of continued negative real interest rates,” says U.S. Global Investors chief and Vancouver stalwart Frank Holmes.

“The chart below shows how gold has historically climbed when interest rates fell below 0%, with a ‘strong correlation from 1977-84, and again recently when rates turned negative in early 2008,’ according to Desjardins Capital Markets.”

Read More HERE

By Marin Katusa, Casey Research

My most recent trip to Calgary gave me a welcome chance to catch up with friends and colleagues in Cow Town’s oil and gas sector. I found out about new projects, investigated companies of interest, and came away with an improved feel for the current state of affairs – what’s hot, what’s not, and why.

I also came away reminded of one of the dangers that lurk within troubled markets – and today’s markets are troubled. Since mid-March, North America’s exchanges have struggled, with the Dow Jones losing all the momentum that had propelled a spectacular 17% gain over the previous five months while the Toronto Stock Exchange also sputtered and slid, turning downward to lose its slight gains from January and February. Fundamental economic problems remain unresolved in the United States and Europe, while uncertainty grows over China’s ability to control inflation and maintain growth.

The outlook from here is not great. When markets turn bearish, investment strategies often turn toward income stocks, and rightly so: if market malaise is expected to keep share prices in check, dividends become a very good place to look for profits. But whenever a particular characteristic – such as a good dividend yield – becomes desirable, it also becomes dangerous. The sad truth is that scammers and profiteers jump aboard the bandwagon and start making offers that seem too good to refuse.

It was just such an offer that reminded me of this danger. In the question-and-answer period following my talk in Calgary at the Cambridge House Resource Conference, an audience member asked my opinion of a new, private company that was offering a 14.7% monthly dividend yield.

Yes, you read that right: a 14.7% monthly yield, from a new, private, natural gas company.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair