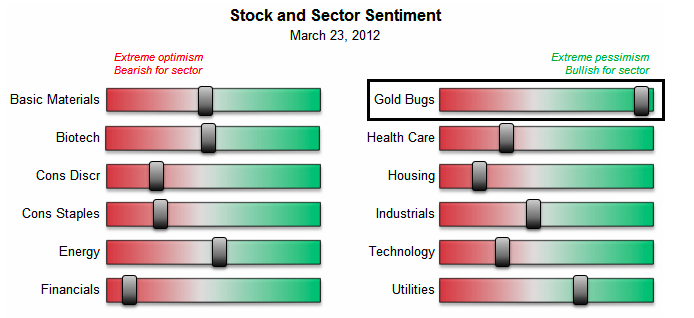

Gold & Precious Metals

We hear calls of market manipulation and intervention and calls to abandon gold stocks and only own physical metal. We heard these calls in 2008-2009 and now we hear them again, which would only prove disastrous for those who heed such advice. The miners are not only extremely oversold but recent price action suggests a bottoming process is beginning.

The struggle of the mining stocks has surprised many including us. We thought record profits and a bullish environment would catapult the miners out of a consolidation and into a major breakout. The perception of an enduring recovery and the endurance and persistence of the wall of worry stage has left the gold stocks unloved and under-owned and for far longer than we expected. We do have to remember that the miners exploded in 2009 and 2010 and it is normal for a bull market to spend months in consolidation. As a result

I constantly jot down trading ideas….anticipating what may happen in a particular market, and why. Each trading idea has a time frame within which I expect it to play out and that time frame is very important in determining how or when to make the trade.

For instance, if my trade idea is to sell the AUD short because I think it’s run up too far on the “China growth” story, then the time frame implies that NOW may not be the best time to initiate a short position….the time frame on that trade idea is a month-to-month time frame and if the trade starts to work then the AUD could fall for months….NOW…this moment…may not be the best time to initiate the trade because the AUD could rally a few cents from present levels just on “noise” and yet still be within the parameters of that short AUD trade idea….meanwhile, I’ll be increasingly uncomfortable if I’m holding a losing short position!

Last year, I was at a dinner with a bunch of fertilizer analysts from Wall Street and Toronto. To my right was a guy who was really getting on my nerves:

Annoying analyst: We have PotashCorp at overweight. We believe with the structural deficit in potash that —

Me (interrupting): I have a sell on it and dropped coverage.

Annoying analyst: You did what? What did you do that for? Is your firm making a strategic change in direction? You can’t cover fertilizers and drop PotashCorp! (chuckling incredulously.)

Me: I can. I don’t have to cover anything. I cover what I like. When the Street hates the stock, I’ll put it back at buy.

I think the other analysts thought I had six heads. But I do remember one analyst made a point of coming around to me afterward and asking for my card.

Most of the time I just go with the flow. I am an easygoing fellow. But every now and then I like to tweak these clowns. I remember I was at a conference in which about a dozen companies presented. After one company’s presentation, I got tired of hearing all the softball questions and the overly promotional CEO fielding them. Listening to him, you’d think his company were the greatest thing since sliced bread, instead of a flimsy money loser.

So I got in the queue to ask a question. Finally, I got the chance to ask the obvious:

Me: This may seem like a simple question, but I hope to get a serious response… Why doesn’t your company make any money?

CEO: Excellent question!

But sometimes the Street is overly pessimistic. I remember being at a conference in February 2009. There were about 16 companies presenting. The mood was glum. One CEO stood up and said, “It feels like a funeral.” It did. The world was ending. In six weeks, we’d all be eating dog food and howling at the moon. So everyone seemed to think.

At lunch, at about the midway point, I was just trying to make conversation with the analyst next to me:

Me: So you have any favorites you like so far?

Analyst: How about none of them.

I’ll always remember that. Here were some great little industrial companies selling cheaply. And no one was excited. I left that conference determined to recommendFlowserve (NYSE:FLS), which has done very well since. I met the CEO after his presentation, standing alone in the hallway drinking his ice water. I was the only one who came up to him.

A year later, I went to the same conference. The stock had doubled. But the room was full and the CEO wasn’t alone standing in the hallway after giving his talk.

Sometimes I have to hurdle some skepticism from people who are not sure what I’m up to. I remember I called up one CFO of a small company. I told him who I was and what I did and that I was thinking of recommending his stock, but I had some questions first. I remember he said, “Well… How much is this going to cost me?”

Ha! Obviously, he had been approached by others before who wanted some kind of compensation for writing favorably about his stock. The idea that I was truly independent, beholden only to my subscribers, was refreshing and unusual to him.

Anyway, enough of my reminiscences. It is good to rub elbows with the Street now and then. Sometimes you do get some good nuggets…

Recently, I wrote about the big opportunity shaping up in Europe as its banks look to unload assets. I recently listened to Dan Och give a presentation at a Goldman Sachs conference in New York, which had a little more insight into that idea.

Remember, Och is a pretty darn good investor himself. His Och-Ziff Master Fund has returned nearly 10% annually since inception in 1998. And it’s done so with about a third of the volatility of the market as a whole. So Och’s opinions are not like some random CEO popping off about the market.

Let’s get to the presentation…

Asked about the investment landscape in 2012, Och had this to say about Europe:

“We are starting to see certain areas [that] we consider to be asymmetric opportunities. There’s been some substantial dislocation in credit and structured credit in the US and Europe that are very good opportunities for us… Longer term, we see some big opportunities. For example, European banks at some point are likely to start selling substantial amount of assets, and we’re well positioned for that…

“The vast majority of assets that have to be sold have not been sold. If you look at the proposal that was made in late October by the various European authorities that talked about increasing Tier 1 capital on their banks, a big part of how they intend to do that is selling assets…”

“We’ve been in London for 14 years. We have 65 people. We have a distressed credit team. We have a structured credit team. We have a real estate team. We have all of the resources and capabilities. We’ve done an enormous number of transactions there.”

After hearing this, I started to think OZM itself might also wind up being a good play on the “Biggest Fire Sale in History.”

Regards,

Chris Mayer,

for The Daily Reckoning

Joel’s Note: As we mentioned last week, we ain’t never met a mob we wanted to join, nor a trend we wanted to follow. In investment, as in life, it pays to just make like that annoyingly catchy Fleetwood Mac song and just go your own way.

Of course, that’s not always easy. There’s the persistent temptation to feel like a real jackass when you look around and find yourself the only one buying stock ABC, or wearing t-shirt XYZ, or listening to music 123. But if your analysis is good, if your convictions are true, you’ll quite often find the world eventually coming around to your side.

In fact, going his own way has taken Chris Mayer around the world on a seemingly never-ending investment field trip. He’s pounded the pavement in India and China and across South East Asia, South America, South Africa, Australia, New Zealand and his travel agent knows where else. The resulting material colors Chris’ next book, due out any week now, titled World Right Side Up: Investing Across Six Continents.

Now that’s due diligence.

If you’d like to take part in our first ever free book launch, simply head to this link for more info.

Also, Chris will be on RT tomorrow around 4:30pm to chat about his World Right Side Up investment perspective tomorrow. Be sure to check it out.

——————————————————–

Here at The Daily Reckoning, we value your questions and comments. If you would like to send us a few thoughts of your own, please address them to your managing editor at joel@dailyreckoning.com” title=”joel@dailyreckoning.com” target=”_blank”>joel@dailyreckoning.com

Thursday, April 5th at 6:30pm at the Vancouver Club.

Neil McIver has been a regular guest on Michael Campbell’s MoneyTalks and recently presented to a standing room-only audience at the 2012 World Outlook Financial Conference in February. Neil and his team at McIver Wealth Management have had a remarkable track record of investment success. At our request he has agreed to present this full length investment seminar exclusively for our audience AT NO COST!

Find out how to profit from:

- Myths propagated through the media

- Bullish myths after a rally

- Long term bear market myths and the price you pay

- Cheerleading driven gains and give-backs

- Dazed and confused commentators

- Short term blindness

As one of Canada’s most successful discretionary investment service providers Neil and portfolio manager Mark Jasayko will show how they use market myths and contrarian indicators to their advantage and offer specfic recommendations on stocks, sectors and countries for 2012 and 2013.

To register email Neil or Mark directly

Mark.Jasayko@RichardsonGMP.com

Or call 604.694.7735

Seating is limited so your must register early. We urge you to take advantage of the this special FREE opportunity.

“The (Trade) data has proven my point. Just as the prosperity of the ’90s and ’00s blinded us to the coming crisis in ’08, the current talk of recovery is distracting investors, commentators, and even academics from rapidly degrading fundamentals. This course can only lead to a greater crisis, that I have dubbed in my latest book “The Real Crash.”

This article was revised on March 23, 2012.

Earlier this month, the Department of Labor reported that 227,000 new jobs were added to the economy in February, marking the third consecutive month of positive jobs growth. Many observers have taken the news as evidence that the recovery is underway in earnest, helping send the S&P 500 index to the highest level in nearly five years. However, the very same day, the Commerce Department reported that after surging for much of the last year, the U.S. trade deficit increased to $52.6 billion for January – the largest monthly trade gap since October 2008. This second data point should dampen enthusiasm for the first.

From 2005 through mid-2008, those monthly figures almost always topped $50 or $60 billion, setting a monthly record of $67.3 billion in August 2006. But when the housing and credit markets imploded, attention was focused elsewhere. At that time, I was one of the few economists to raise a red flag about the dangers of growing trade deficits. In any event, the faltering economy took a huge bite out of imports, pushing the trade deficit down 45% in 2009. Even those people who were still paying attention to trade assumed that the problem was solving itself.

However, after reaching a monthly low of $35.7 billion in May of 2009, the trade deficit began to grow again, expanding 31% in 2010 and 12% in 2011. While the $52.6 billion deficit in January is still about 10% below the monthly average seen in 2006-2008, if GDP continues to nominally expand, as many assume it will, we may soon find ourselves in the exact same place in terms of trade that we were before the financial crisis began. That’s not a good place to be.

If the jobs that we have created over the last few years had been productive, our trade deficit would now be shrinking, not growing. But the opposite is happening. These jobs are being created by the expenditure of borrowed money, and are not helping to forge a newer, more competitive economy. In the years before the real estate crash, our economy created millions of jobs in construction, mortgage finance, and real estate sales. But as soon as the bubble burst, those jobs disappeared. Today’s jobs are similarly being built as a consequence of another bubble, this time in government debt. And, likewise, when this bubble bursts they too will vanish.

Throughout much of the last decade, I had continuously warned that the growing trade deficit was an unmistakable sign that the U.S. was on an unsustainable path. To me, monthly gaps of $60 billion simply meant that Americans were going deeper into debt (to the tune of $2,400 per year, per citizen) in order to buy products that we were no longer productive enough to make ourselves. I pointed out that America had become an economic juggernaut in the 19th and 20th centuries on the back of our enormous trade surpluses, which allowed for growing wealth, a stronger currency, and greater economic power abroad. This is exactly what China is doing today. Deficits reverse these benefits. (To learn how China is spending its surplus, see my latest newsletter.)

My critics almost universally dismissed these concerns, typically saying that our trade deficits resulted from our economic strength and that they were a natural consequence of our status at the top of the global food chain. I pointed out that even highly developed, technologically advanced economies still need to pay for their imports with exports of equal value. Instead, all that we have been exporting is debt and inflation.

The financial crisis initiated a painful, but needed, process whereby Americans spent less on imported products while manufacturing more products to send abroad. But the countless government fiscal and monetary stimuli stopped this healing process dead in its tracks. Government borrowing and spending redirected capital back into the unproductive portions of our economy. Health care, education, government, and retail have all expanded in the last few years. But manufacturing has not grown at the pace needed to solve the trade problem. In short, these jobs are creating more consumers and less producers, they are making us poorer rather than richer.

Job creation at home has been like vegetation sprouting along the banks of rivers of stimulus. These artificial channels may help temporarily, but they prevent trees from taking root where they are needed most. Our economy has yet to restructure itself in a healthy manner. The recession should have forced us to address the problem of persistent and enormous trade deficits. We have utterly failed to do this. So while the job numbers look good for now, the pattern is ultimately unsustainable.

The last time the monthly trade deficit was north of $50 billion, the official unemployment rate was under 6% and our labor force was considerably larger. Should this artificial recovery actually return millions of unemployed workers to service-sector employment, our monthly trade deficits could go much higher – perhaps eclipsing the previous records of 2006. It is possible that the annual deficits could top the $1 trillion mark, thereby joining the federal budget deficit in 13-digit territory.

Also, last week, we got news that our fourth quarter current account deficit widened 15% to just over $124 billion. The $500 billion of annual red ink is actually reduced by a $50 billion surplus in investment income (resulting primarily from foreign holdings of low-yielding US Treasuries and mortgage-backed securities – however, when interest rates eventually rise, this surplus will quickly turn into a huge deficit). At anything close to a historic average in employment and interest rates, today’s structural imbalances could produce annual current account deficits well north of $1 trillion. As higher interest rates would also swell the federal budget deficit, it is worth asking ourselves how long the world will be willing to finance our multi-trillion dollar deficits?

Back in the late 1980s, when annual trade and budget deficits were but a small fraction of today’s levels, the markets were rightly concerned about America’s ability to sustain its twin deficits. This anxiety helped lead to the stock market crash of 1987. But with the boom of the ’90s, all talk of trade deficits was dropped. Though I spoke out about the danger of having consumption chronically outstripping our productivity, the general feeling of prosperity meant my warnings fell on deaf ears – even as the deficit figures hit all-time record highs. This was a major factor in the economic implosion of 2008. However, even when the imbalance had reared its head, mainstream economics predicted that the economic contraction would slow consumption sufficiently to significantly close the gap. Once again, I took to the airwaves warning that if the government tried to solve the crisis by encouraging consumption instead of production, the trade gap would only get worse – causing a greater crisis in the near future.

The data has proven my point. Just as the prosperity of the ’90s and ’00s blinded us to the coming crisis in ’08, the current talk of recovery is distracting investors, commentators, and even academics from rapidly degrading fundamentals. This course can only lead to a greater crisis, that I have dubbed in my latest book “The Real Crash.”

To save 35% on Peter Schiff’s new book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, pre-order your copy today.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair