Stocks & Equities

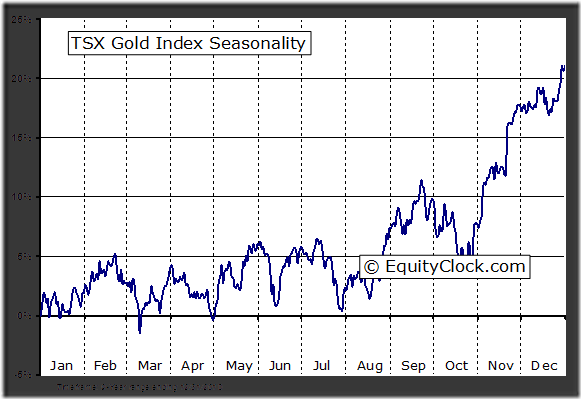

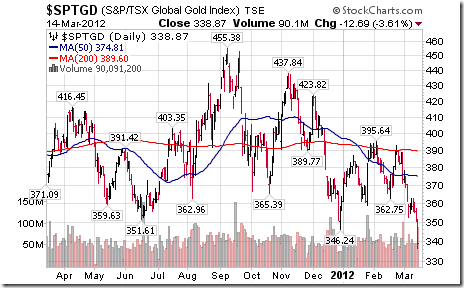

The PDAC Curse continues! Canadian gold equities have a history of moving higher from the last week in December until the third week in February in anticipation of encouraging news to be released just before or during the annual Prospectors and Developers Association Conference in Toronto early in March. Thereafter, Canadian gold equities tend to move lower. They followed their seasonal pattern once again this year. The TSX Gold Index from its low on December 29th to its high on February 23rd gained 13.4%. Subsequently, the Index plunged 13.4% by this Wednesday to reach a 20 month low. Moreover, next major support for the Index on the charts is 14% below current levels.

Weakness in gold equities this week is related to a $US68 per ounce plunge in the price of gold from last Friday to this Wednesday. On Wednesday, gold fell below its 200 day moving average at $1,679, a technical level that previously had provide strong support. Gold was responding partially to strength in the U.S. Dollar following news that U.S. Non-farm Payrolls in February continued to recover from depressed levels. The U.S. Dollar also strengthened following encouraging news from the Federal Reserve on Tuesday confirming slow, but steady economic growth in 2012. The Federal Reserve also noted its intention to maintain an easy money policy until the end of 2014.

The TSX Gold Index did not respond well to the news. Weakness in the Gold Index was the main reason why the TSX Composite Index dropped sharply on Wednesday when major U.S. equities indices were reaching multi-year highs. Moreover, prospects for gold and gold stocks are not encouraging between now and November 6th, the day when the next U.S president is elected. The U.S. Dollar has a history of moving higher between the end of March and the end of October during a U.S. Presidential election year. Not surprising, gold and gold stocks have a history of moving slightly lower during this period. Normally, gold and Canadian gold stocks have a period of seasonal strength from the end of July to the end of September followed by a second period of strength from the beginning of November to the third week in February. The latter period is likely to be the better period for re-entering the gold trade this year.

Preferred strategy is to look for better opportunities than gold and gold equities between now and November. Silver, platinum and their related equities are preferred over gold if your investment focus is on precious metals. Silver and platinum benefit from a growing demand for industrial purposes and have a history of outperforming gold between now and May..

The Gold Bugs Index fell another 33.44 points (6.56%) last week. It broke support at 477.93 to confirm an intermediate downtrend. Strength relative to gold remains negative.

After Mar. 20 Close:

TSE Gold Index Seasonality:

Via Don & Jon Vialoux’s Equity Clock

Good As Gold!

Just as a matter of reference on January 1, 2010 the Dow was at 10,550 so to date it has risen 25.42% while gold has moved from 1,100.00 for a gain 50.54%! So in spite of the Fed’s best efforts to pump the stock market up with a barrage of fiat currency while at the same time suppressing the price of gold with relentless intervention, gold has out performed the Dow two to one!! That tells you all you need to know.

They say a picture is worth a thousand words so if that’s true

…..read the rest & view more charts HERE

(also don’t miss Mark Leibovits daily gold comment HERE

A Big Relative Decline

Since April of 2011, gold stocks have entered a notable downtrend relative to the prices of gold and silver. Various theories have been advanced as to why this is the case and all of them have some merit (e.g. the fact that ‘resource nationalism’ is increasing all over the world, that costs are ratcheting higher, that metal-backed ETFs give investors exposure to the metals while avoiding the hassles gold mining companies have to deal with, and so forth).

GOLD – ACTION ALERT – BUY

Continue to look to take delivery of the physical metals on further weakness. The gold/silver snake is coiling. The ‘gangsters’ at the Plunge Protection Team, JP Morgan Chase, and the CME will do their best to drive prices lower, but will get ‘bit’ by a venomous and revengeful market. There will be no tears here.

Gold and silver were recently knocked down to distract from the Greek bond default and that there is a huge movement away from the U.S. dollar as a trade settlement currency. The United States is waging economic nuclear war against Iran and threatening to do the same against India and is likely to suffer similar counterattack against its own vulnerabilities, and a lot more.

We may have hit support levels in both gold and silver, but I am awaiting further confirmation that lows are in place. Such lows may only be trading lows. Recall, we’ve entered a negative ‘seasonal’ time of year for gold and silver that could carry into the summer. There is, however, the possibility of another shot higher into May, but I would hope upside volume would confirm the advent of that move. Except for those of us who are long-term holders or for those who have no positions whatsoever, there is nothing to do here without a renewed upside trigger.

I urge you to subscribe to my VR Gold Letter for much greater detail at www.vrgoldletter.com. Call our office, we can offer you a discount for subscribing to more than one service.

For now, I am as psychologically prepared to see silver at 20 as to see it at 60 in the next twelve months. The big numbers for silver are 26 support and 37.60 resistance. The big numbers for gold are 1521 support and 1792 resistance – above which we could see 2500. As Ed Hart used to say on the old Financial News Network in the 1980s, ‘we will know in the fullness of time’.

VRTRADER.COM Trial Signup:

THE RENEWAL OF YOUR SUBSCRIPTION IS AUTOMATIC. YOUR CREDIT CARD WILL CONTINUE TO BE BILLED UNLESS YOU NOTIFY VRtrader.com SEVEN DAYS PRIOR TO SUBSCRIPTION EXPIRATION EITHER VIA EMAIL POSTING THE WORD ‘UNSUBSCRIBE’ IN THE SUBJECT BOX OR TELEPHONE US AT (928) 282-1275 OF CANCELLATION. NO REFUNDS ARE AVAILABLE ON SILVER, PLATINUM OR VR FORECASTER (ANNUAL FORECAST MODEL) SUBSCRIPTIONS.

Welcome and congratulations on choosing VRTrader.com as a source for your stock market commentary, information and analysis for the U.S. Stock Market. Needless to say we are very happy that you are joining us for AT LEAST the next 30 days days and look forward to providing you rewarding and inciteful information that will help you toward your goal of succeeding in the markets.

Here is the Special Trial Offer: Use this month to kick our tires. Pay 50% for the first 30 days (No refund) and sample our Silver or Platinum service and then decide what works best for you. If you aren’t 100% ready to move forward, simply email us to cancel one week before your 30 day 50% off trial subscription ends and it will be canceled and you will not be charged ANY FURTHER, no questions asked. Just send an email to mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com or call 928-282-1275 to cancel. You will receive an emailed confirmation of your cancellation at that time.

The 30 day trial is allowed one time only. By taking this 30 day 50% trial, you agree to be charged the full cost of the monthly Silver or Platinum service (choose one only) at the end of the 30 day trial subscription period, unless you cancel first. The regular Silver monthly rate is $49.40 and the Silver quarterly rate is $133.50. The regular Platinum monthly rate is $129.95 and the Platinum quarterly rate is $350.85. The special trial 50% off trial rates are listed below. Sign up today!

There are no refunds or pro-rata refunds offered at VRTrader.com for any subscription. You are being offered a 50% discount for trying our service for the first 30 days only!

Some companies in the oil and gas business get more appreciation in the market than they perhaps deserve. Others labor away building their assets and cash flow with little market recognition. In this exclusive interview with The Energy Report, Josh Young, founder and portfolio manager of Young Capital Management, brings us up to date on several of his favorite undervalued plays and talks about his newest discovery, which he believes to be an amazing value.

The Energy Report: When we last spoke three months ago, West Texas Intermediate (WTI) crude was trading at around $98 per barrel (/bbl). Since then we’ve had a spike up for a combination of reasons. Do you think that all the talk of $5 per gallon (/gal) gasoline is real or just hype by oil companies and traders; and where would the oil price need to go for $5/gal gas to become a reality?

Josh Young: Five-dollar/gal gas is a real possibility as prices are linked to the price of oil, which now seems to be driven by tight supply and demand dynamics. We saw that recently when there was an apparently false news report that a pipeline in Saudi Arabia had been blown up, affecting a couple of million barrels a day. Oil spiked $2 in the space of 15 minutes, despite the fact that the report was false. When that kind of news can cause that amount of price movement in that amount of time, it indicates that there really isn’t a lot of available capacity in the event of production shortage. Supply and demand are matched pretty tightly. On the flip side, the economy is still pretty weak and high oil prices produce some demand destruction. These are two big factors that are just barely counterbalancing each other.

TER: Do you think there’s some resistance around $110/bbl oil or can the price just shoot up astronomically?

JY: It really depends upon the scenario. I think things should be somewhat in balance around current prices, but if there is a bad economic crash, prices could come down potentially to $70 or $80 or even lower as they did in ’08 or ’09. If you see a big shock like a bombing in Iran for example, prices can spike.

TER: This being an election year, if oil prices go much higher, do you think President Obama might release supplies from the Strategic Petroleum Reserve to cool down the markets?

JY: If the U.S. or Israel bombs Iran, that obviously would be a consideration, and I wouldn’t be surprised if that happened. I would be surprised if there would be a release of those petroleum reserves in the absence of a world event along the lines of a major supply disruption.

TER: With these higher oil prices, many players in the oil business are benefitting. What has been the general market performance for the whole industry group since we last spoke?

JY: I read a recent Wall Street Journal article addressing that issue, and it reported that price performance of stocks of publicly traded oil and gas companies had not followed the price performance of oil. Looking down market, smaller-cap stocks have actually moved a lot less than larger-cap stocks. It seems investors are using larger stocks to track the price of oil. The preference for liquid stocks and larger companies has left behind some of the smaller companies that I tend to focus on. There hasn’t been the kind of across-the-board movement that one might expect with higher oil prices. Therein lies the opportunity; the longer oil prices stay high, the more likely there will be a small-cap oil stock rally.

TER: Can you bring us up to date on some of your favorite names that we discussed in the past?

JY: Sure. Gastar Exploration Ltd. (GST:NYSE) just reported that it is now producing approximately 1,000 barrels per day (bpd) of condensate and natural gas liquids (NGLs) in West Virginia. And that’s up from almost no oil production this time last year. It seems Wall Street is just starting to see the value here—almost every analyst covering the stock had higher than market price targets and reiterated their buy ratings after the recent news.

Gastar has drilled only a fraction of the locations it will be able to drill in West Virginia, has been adding acreage at a reasonable cost and has about $100 million (M) of capital available on its bank line, which it hasn’t drawn much of yet. So it’s borrowing money at 4–5% interest to drill wells that are generating in excess of 40% rates of return. Having shown that it can grow in a cost-effective manner without stock dilution, I think the company will start to attract more attention. It seems that Gastar offers investors a more cost-effective way to get Marcellus exposure, natural gas price leverage and oil production growth than larger companies, such as Cabot Oil & Gas Corp. (COG:NYSE), EQT Corp. (EQT:NYSE) and Range Resources Corp. (RRC:NYSE).

TER: Is that reflected in the price?

JY: Absolutely not. Gastar has been drilling these excellent wells in West Virginia, growing its production, and proving up the value of an asset that is worth a multiple of what the whole company is trading for, yet the stock has been drifting lower. Also, Encana Corporation (ECA:TSX; ECA:NYSE)drilled a well adjacent to Gastar’s East Texas properties that came on at an initial production rate of 750 bbl/day. That well’s production flattened out at about 250 bbl/day, which is very exciting. There is the potential that Gastar is right in the middle of a highly economic oil shale play. Gastar’s West Virginia Marcellus play is worth roughly $5 per share. If the East Texas oil play and the recently announced new mid-continent oil play work out, there could be substantial upside to $5, versus a recent stock price of ~$2.75.

TER: How about some of the other companies you’ve been following?

JY: Molopo Energy Ltd. (MPO:ASX) is another company I’ve talked about before. The stock is still stuck in a morass, despite an exciting deal in the works. Its CEO has been telling investors that he expects an ongoing asset sale process that the company has been involved with in Queensland, Australia to close in March. There are a number of reasons to expect a high sale value for the Australian asset. The price of liquid natural gas (LNG) in Japan, which is the primary market for Australian natural gas, has seen prices as high as $18 and $20 per thousand cubic feet (mcf). A nearby competitor in Queensland recently announced an offer that would imply a very high value for Molopo’s assets—as much as $150–200M. I don’t expect the assets to sell for quite that much, but could come in at a higher price than people expected.

TER: Where is that stock trading these days?

JY: Molopo trades around $0.70, with a market cap of around $150M. The company has $100M in cash, no debt and is currently producing net around 500 bbl/day. Combining the current production value plus its cash, you get everything else for free. It could easily sell the Queensland asset for $80M, plus it has development locations across 20,000 net acres in the Permian basin and a potential Bakken play on 50,000 net acres in southeast Saskatchewan. Analysts covering the stock estimate its value at $1.00-1.50.

TER: What about some of the other ones we talked about?

JY: Another company we’ve talked about is Sonde Resources Corp. (SOQ:NYSE). It’s a Canadian oil and gas company with an oilfield offshore North Africa. Sonde hired Bank of America Merrill Lynch to sell or joint venture its offshore North Africa assets. The local political situation is still a mess, but international oil companies seem to have acclimated to the situation. There are a lot of unstable countries where companies drill for oil and pay high valuations for reserves in the ground. Management has guided to a sale value of the North Africa assets of $2-5 per recoverable barrel of oil in the ground, which could yield $140-350M, versus the company’s current market cap of $150M. Sonde sold another asset recently and it’s sitting on $50M net cash. There’s a lot of opportunity to deploy that cash if oil prices fall or there is some sort of economic crisis. The CEO is excellent. He’s led other very successful oil and gas companies, including a position as co-CEO for Samson Investment Co, which was bought out for over $7B last year.

TER: Do you have any other companies worth talking about?

JY: I’ve recently found a very attractively priced, rapidly growing oil company, Gale Force Petroleum (GFP:CVE). Gale Force is trading at a 50+% discount to its Proved Developed Reserve value, is growing production by roughly 300% per year and has a small debt load. I invested in the company in a private placement, in addition to buying stock in the open market, and was retained as an advisor to help identify new deals and advise on hedging strategies and capital structure. Gale Force’s micro-cap peers typically trade for their PV-10 value, and in many cases they trade for many times their PV-10 values. The potential for that valuation uplift is part of what attracted me to the situation.

Gale Force’s market cap is only $12M, it has $6M of debt, over 300 barrels oil equivalent per day (boe/d) production and management believes they’re on track to produce 600 boe/d in September and 1,000 boe/d by the end of the year. And that’s over 80% oil, with the rest liquids-rich gas. I’ve looked extensively and have not found any other companies or assets where you can buy flowing barrels of oil with an exit rate implying a $20,000 per flowing bbl price. It has already achieved tremendous growth, from under 100 boe/d a year ago, to 300 boe/d now. Yet it is still under the radar and the company hasn’t been actively marketing its stock, preferring to focus on deal execution and property level operations. But as Gale Force grows production, people will start to pay attention. Even if no one ever cares about the stock, when the company grows to 1,000 boe/d, someone could come along and pay the industry standard of $100,000 a flowing bbl and you could see Gale Force being bought at the end of the year for a $100M. Other rapidly growing oil companies with similar size production have much higher valuations per flowing barrel—Voyager Oil & Gas Inc. (VOG:NYSE.A) produced approximately 420 boe/d last quarter and currently has a $180M market cap and Samson Oil & Gas (SSN:NYSE.A; SSN:ASX) produced 315 boe/d last quarter and has a $225M market cap. While not a perfect comparison, Gale Force is trading for roughly 1/10 of the value of those companies on a flowing barrel basis.

TER: Where is its production?

JY: It’s primarily in East Texas and some in South Texas. Gale Force also recently did a deal in the Marcellus, funding the development of non-operated working interest right next to Gastar. My fund and an energy private equity fund financed most of the deal, and Gale Force took the rest. So far so good, as the Marcellus wells are producing twice the condensate and NGLs as we were expecting.

Gale Force Petroleum’s growth opportunity and main business focus is in East Texas. It buys and operates underperforming fields, typically producing anywhere from 10 to 50 bbl/day. It reworks wells, increases their production, drills infill wells and then does it over again. Gale Force recently announced its next two acquisitions and should be up to 10 properties soon. It has a lot of production and is actually cash-flow positive.

Most similarly sized companies have high production decline rates, whereas Gale Force’s production is pretty flat because these are conventional wells with shallow decline rates, allowing Gale Force’s production to be more predictable, and for cash flow to be deployed for growth rather than to replace rapidly declining production. Gale Force has been able to achieve growth similar to shale players, but with mature assets at a fraction of the capex, and in my opinion with substantially lower risk. I get the best of both worlds—lower risk and rapid growth. As more investors discover Gale Force and as it delivers on production and executes operationally, I expect the valuation to improve substantially.

TER: That’s what people are looking for. Maybe this will be the next big winner. Any final thoughts you’d like to leave us with?

JY: I think there are interesting opportunities among small-cap oil and gas companies. And the smaller you can go, assuming the company is solvent and growing, and the more undervalued you can go, the higher the potential return and the lower the fundamental risk. And with high oil prices, perhaps that potential return is forthcoming.

TER: Thank you, Josh. We appreciate your insights.

Josh Young is the founder and portfolio manager of Young Capital Management, LLC, which launched Young Capital Partners, LP in 2010. He previously served as an analyst at Karlin Asset Management, a multibillion-dollar single-family office in Los Angeles. Prior to that, he was an investment analyst at Triton Pacific Capital Partners. He was also a corporate strategy consultant at Mercer Management Consulting and DiamondCluster. He holds a Bachelor of Arts in economics from the University of Chicago.

Amid the bustle of the 80th Prospectors and Developers Association of Canada (PDAC) convention in Toronto, The Gold Report sat down with PDAC President Scott Jobin-Bevans for his take on the challenges the mining industry faces. In this exclusive interview, he covers a wide range of topics, from skilled labor shortages to the trials of mining in remote northern Canada.

COMPANIES MENTIONED: AVALON RARE METALS INC. – MAGMA METALS LTD. – NORTH AMERICAN PALLADIUM LTD. – PROPHECY PLATINUM CORP. – TIEX INC.

The Gold Report: What are the key challenges the mining industry faces in 2012–2013?

Scott Jobin-Bevans: PDAC, under the leadership of newly appointed Executive Director Ross Gallinger, will be conducting a strategic review involving the board of directors, staff and gathering membership input. There are a number of issues facing the association and the industry, and I am sure that human resources challenges will surface as a key issue.

TGR: When you say human resources, what are you talking about specifically?

SJ-B: It’s the skilled workforce: geologists, geophysicists, process engineers, mining engineers, miners and skilled labor. There’s a huge gap between the young people who are out there now and the older ones who know those skill sets from years ago. For instance, we’re nearly missing the 35-to-45 age bracket.

There is a tremendous opportunity for industry associations such as ours, the government, private sector and educators to work together. This is a hugely important sector that represents nearly 3.5% of our national GDP and pays billions of dollars in tax revenue and royalties to the various levels of government.

It presents an opportunity to university students, but it also presents a challenge to the industry. The Mining Industry Training and Adjustment Council led an industry-sponsored study released in 2005 that found that the Canadian mining and mineral industry would need at least 80,000 people in the next 10 years just to replace current jobs. The industry has grown quite a bit since 2005. So, the estimates in Canada are now something like 100,000 jobs will need to be filled in the next 10 years.

TGR: Where are those numbers coming from?

SJ-B: You can find them on the Mining Industry Human Resources Council of Canada’s (MiHR’s)website. The PDAC supported a more recent sector study by MiHR, “Unearthing Possibilities,” which looks specifically at the exploration sector; it’s important to understand that mineral exploration is different than the mining sector. In this study, we were able to show how many women are in mineral exploration, how many people are employed overall and the demographics on the age distribution.

You can see the late ’80s downturn in the 35-to-44 age group when the industry and the economy tanked. People left the industry and never came back. You can also see the effect of the Bre-X scandal and market decline in 1997, which saw the departure of record numbers of professionals from the industry. The report does show an increase in the 25-to-34 age group coming into the industry, which is really encouraging.

The connection between human resources and supplying the metals of tomorrow is that we can still find the mines but we can’t put them in production because we simply don’t have the people. The only way we survive now is by poaching from other projects, so it’s not a healthy environment for industry success.

PDAC has been making efforts in terms of our support for educating the work force of tomorrow. We have a strong program that we support through PDAC Mining Matters that has helped educate nearly 500,000 school-age children about the sector. We’ve got a number of university programs and scholarships but the industry needs to do more.

TGR: What are some of the other challenges facing the industry?

SJ-B: I’m not sure it’s a challenge so much as a new opportunity in Canada in terms of working with First Nations and aboriginal communities, which ties into land access. Canadians are leaders in developing strong dialogues with our aboriginal partners and PDAC is very committed to ensuring our members are equipped and prepared to have those conversations, whether in Canada or abroad.

TGR: Is this a global issue?

SJ-B: I think we need to understand this in a different context. This isn’t a problem as much as it is a reality that companies need to adjust to. The issue of aboriginal and indigenous people’s rights is extremely complex and extends into places like Chile, for example, which is not dealing with the issue to the same degree as Australia or Canada; but it recognizes that it must be dealt with soon. The major mining companies and Codelco, the state-owned enterprise in Chile, haven’t had to deal with it because most of their mines are in remote areas where there are very small villages; companies tend to be good corporate citizens by making donations and providing infrastructure and job training to the local villages. But, as the industry expands in Chile, I believe there will be more focused attention on indigenous peoples.

Another issue is profit sharing and the desire for local communities to want a piece of the pie, a portion of the production royalty. We also see this happening in India, Peru and many other countries, as well as in Canada. India has proposed that iron ore and copper miners set aside 26% of the royalty they pay to states to share with locals affected by mining. The PDAC is in favor of resource revenue sharing as long as it is introduced in a fair and sustainable manner.

TGR: On another subject, Canadian Natural Resources Minister Joe Oliver spoke at PDAC. Do you think we’ll ever see a national securities regulator, like the SEC in the U.S.?

SJ-B: PDAC supports having a single regulatory system administered by one regulator, applying one set of rules in a consistent manner across Canada. We would welcome a one-window central process. But it isn’t easy because each province has the right to control the regulatory process and collect fees in its own jurisdiction. This results in duplication and higher cost for financings and ongoing compliance. We need to have a system that allows all potential Canadian investors the equal opportunity to participate.

TGR: What is another industry challenge?

SJ-B: Mine permitting and the related regulatory process. This is a global issue. Governments often don’t have the capacity to administer their own acts and legislation. I believe we are going to see this capacity issue in Ontario with the current revision of its Mining Act. We see capacity issues in British Columbia and the Yukon Territory, largely brought on by increased industry activity and record mineral claim staking. We also see a lack of capacity within the provincial governments and within First Nation governments to deal with the required paperwork, which is becoming more and more onerous. Minister Oliver spoke at length about this at the Association for Mineral Exploration British Columbia Roundup in January and again at the PDAC Convention. He believes that regulation should be practical, useful and not overly bureaucratic, and I, for one, support that.

Another example is Finland. Finland is a great jurisdiction for mining. It embraces and promotes it. The GTK or Geological Survey of Finland actively maps, explores and even drills holes to build up resources, which it then puts out to auction. It recently introduced a new mining act and at the same time made changes to staff size and location, which almost overnight resulted in license granting going from a 6–12 month window to a 3–5 year time frame to establish land tenure. This is very discouraging to mineral exploration companies thinking about investing exploration dollars in Finland. My recent discussions during the PDAC convention with the Federal government does suggest that they are committed to improving the system in the very near future.

TGR: I guess this makes Ontario and Nevada look better all the time.

SJ-B: Finland still beat Ontario in the Fraser Institute’s annual survey of the best jurisdictions for mining in the world. We also saw New Brunswick being ranked as number one and for the first time ever we saw Ireland in the top 10 along with the Yukon Territory.

The survey ranks jurisdictions on things like administration, corruption, environmental regulation, duplication, fair trade, transparency, taxation etc. The most recent survey came out in the last few weeks.

TGR: Northern Ontario’s Ring of Fire region includes chromite, base metals and gold deposits. There are billions of dollars of potential revenue there, but there is zero infrastructure. You have to have rail to get the minerals out of there. All these different deposits have been found and they have NI 43-101 resources on them, but they’re not going anywhere.

SJ-B: I think we have to see the various levels of government as partners in the extraction of our mineral wealth and my view is that there really is an opportunity for the government to partner with industry and help build infrastructure in the north. There is a huge discovery that could be world-class size. The potential for northern development—for wealth generation in the province—is very real. I think both federal and provincial governments are still recovering from the financial crisis and at this point are not able to invest the dollars today for the long term in spite of the economic development opportunities that exist. Economic development is all based on favorable returns and future earnings through increased taxation and other revenue, and right now governments have a tremendous opportunity to show that measure of foresight for this industry.

We think that we finally got the Feds to understand the importance of mining to this country. We have had Minister Oliver at the conference, a record number of members of Parliament, members of Provincial Parliaments, senators and we were really pleased to see Jean Charest, the Premier of Québec, join us at the conference.

TGR: Most of the readers of The Gold Report are precious metals investors. Can we talk about your personal view as to what you see as opportunities for North American investors right now who like resource stocks? What are some of the commodities that you see really gaining traction in 2012? Do you see particular interest in micro caps, in the near-term producing stories?

SJ-B: Certainly, I’m in agreement with gold and silver being the mainstay of the industry and, of course, copper. There’s a big push with anything having to do with country- or economy-building commodities, iron ore, for instance. Rare earth minerals are a complicated commodity, but I think a lot is going to happen in that space.

For example, Germany canceled its nuclear power program and is now having to look for alternative green energy. It recently created an alliance for securing critical raw materials after it essentially closed down the mining and metals industry 20 years ago, thinking that mining was a sunset industry.

TGR: Well, it’s pretty clear that Europe is waking up to the idea that these critical metals are very important for growing clean energy.

SJ-B: For sure. Germany is a good case in point because the German market is really hunting for those metals, not only for internal consumption but also for building the technologies that it exports. To produce a windmill for instance, you need neodymium for the magnets and so a source for this rare metal needs to be secured to be a successful producer. The Germans asked Canada what we have. Well, the short answer is nothing because we basically shut down all of those operations years ago. To bring any production on-line in the near term is going to be very costly.

Look at Thor Lake’s Avalon Rare Metals Inc. (AVL:TSX; AVL:NYSE; AVARF:OTCQX).

PDAC Director Don Bubar is heading up the company and PDAC Past President Bill Mercer is also involved. Avalon has a great story, a great deposit in Thor Lake. Infrastructure-wise it is fairly remote. In the global size of rare earth deposits, it’s small and has a very specialized suite of minerals that are desirable, but it will take very high production costs to extract and build a plant. Doing that in Canada is challenging. I don’t believe that there is enough critical mass in Canada to justify such a high capital expenditure. I am, of course, always hopeful that it will work, but it’s not like a copper or nickel discovery or a base-metal discovery where you have five or six deposits in one general area that you can then aggregate to feed a smelter or a processing facility. In the case of most rare earths in Canada you have a relatively small deposit with complex metallurgical challenges that would be feeding a $1 billion production facility.

TGR: How do you feel about copper, silver and gold?

SJ-B: Canada is a fantastic jurisdiction in which to explore and I think people are realizing that we still have the opportunity to make discoveries in commodities like copper. We’re seeing the copper porphyry business come back to British Columbia (B.C.) with interest from Newmont Mining Corp. (NEM:NYSE). We’ve also got interest in the region from Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE) and even BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) is known to be watching the area. The majors are taking note of projects that until recently have been considered too small a target for copper-gold or copper-moly porphyries. I’m involved with junior explorer Tiex Inc. (TIX:TSX.V) working in B.C. in the Quesnel Trough.

We believe we are sitting on a brand new Cu-Au porphyry discovery that is off-trend from the traditional Quesnel Trough past producers. We have another project that is right next to Spanish Mountain Gold Ltd. (SPA:TSX.V), so there is great gold in sediment opportunities.

Overall, I would say that we are seeing a resurgence in Canada. Most people I speak to are saying it’s a great opportunity for copper-gold in B.C. and gold in the Yukon, and strong interest continues in Quebec and Nunavut. I find B.C. is particularly interesting because it has a recent track record of actually permitting mines. With almost half of Canada’s proposed mining projects located in B.C., it has shown the industry that exploration and development projects can be moved into mine permitting–a step that many other jurisdictions in Canada are failing to make. Plus, in Canada you’ve got diamonds, and we are well positioned to become the third-largest diamond producer in the world.

TGR: Do you mean the third-largest producer by value?

SJ-B: Yes, we do produce some of the highest quality diamonds in the world, but we are also gaining on total production with additional projects turning into mines. In terms of gold, we still have the prolific Abitibi gold camps in Ontario and Quebec. I think around half of the Abitibi Greenstone Belt is covered by clays and impermeable surface material that you can’t see through with traditional exploration techniques such as geophysics and geochemistry. So you have to drill it. This is the world’s largest continuous greenstone belt with some 160 million ounces of production with about 50% of it covered. So the opportunities for gold and base metals in that region alone in Canada are huge.

TGR: You are saying that investors looking for opportunities in the junior mining space have plenty of opportunities in their own backyard?

SJ-B: Absolutely. Canada is politically stable, reasonably well regulated and has a fairly streamlined process to put the mines into production. Minister Oliver said he is committed to making the process even tighter. So, it will become a less-than-two-year process.

Also on the list of metals to watch, I would add platinum group metals (PGM).

TGR: In Canada or elsewhere?

SJ-B: In Canada. I think that although we have a high palladium-to-platinum ratio in our deposits, it’s usually 2:1 or 3:1. The sustained price in platinum, and now palladium, is great for the industry.

TGR: What are the names in that space?

SJ-B: There are Magma Metals Ltd. (MMW:TSX; MMW:ASX)

and North American Palladium Ltd. (PDL:TSX; PAL:NYSE) near Thunder Bay. North American Palladium is our only producer.

Also there isProphecy Platinum Corp. (NKL:TSX.V; PNIKD:OTCPK; P94P:FSE), which is working on a project in the Yukon and on projects in northern Manitoba.

TGR: There are definite supply and demand issues with PGM because of conflict in South Africa.

SJ-B: South Africa controls 80% to 90% of the world’s platinum. And Russia still has a significant portion of the world’s palladium. But, my consulting group does not have clients in South Africa because there are issues in working in that jurisdiction that most junior exploration companies are not comfortable with. Most of our work in Africa is elsewhere such as Tanzania, Zambia, the Democratic Republic of the Congo, Ghana and Mali. There has been a big rise in interest from Canadian companies in Western Africa. I also predict that we can see a significant increase in interest from Canadian explorers and investors in the Dominican Republic.

TGR: Well, that’s another whole topic.

SJ-B: It is. For example, we are seeing Sierra Leone coming back on the map in a big way.

TGR: I think that is a perfect ending to today’s conversation. Thank you so much, Scott.

Scott Jobin-Bevans is the president and a director of the Prospectors and Developers Association of Canada (PDAC) and an exploration geologist with more than 20 years of mineral exploration industry experience. He is a director and founding partner of Caracle Creek International Consulting Inc. (CCIC) where from 2001–2008 he served as managing director. Since May 2011 he has been at Caracle Creek as a director and vice president of corporate development, Latin America. He is also a director of numerous companies including Maudore Minerals Ltd., Tiex Inc., Strike Minerals Inc., Jiminex Inc., Lakeside Minerals, Mukuba Resources Ltd., Ateba Resources Inc. and Northern Skye Resources Ltd. Jobin-Bevans has also served as president, CEO and a director of Treasury Metals Inc., vice president of exploration of Takara Resources Inc., a director of Absolut Resources Corp. and vice president of exploration of Pacific North West Capital Corp.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

1) Sally Lowder and Brian Sylvester of The Gold Report conducted this interview. They personally and/or their families own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Prophecy Platinum Corp. Streetwise Reports does not accept stock in exchange for services.

3) Scott Jobin-Bevans: I personally and/or my family own shares of the following companies mentioned in this interview: Lakeside Minerals, Tiex Inc., Ateba Resources, Mukuba Resources. I personally and/or my family am paid by the following companies mentioned in this interview: Caracle Creek International Consulting Inc.; Northern Skye Resources Inc. I was not paid by Streetwise Reports for participating in this story.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair