Currency

As we go through the first significant pullback in the market for 2012, the dollar seems to be at a turning point that should influence market trends for the next few months. Going all the way back to 2002, there has been a strong inverse correlation between stocks and commodities, and the US dollar. For the most part, the dollar has been falling during this period, which has helped drive cyclical bull markets in stocks and commodities. More recently, the stock market panic of 2008 and the first euro crisis of 2010 drove significant countertrend rallies in the dollar, and corrections in stocks and commodities.

Michael is going to comment on the subject in this article in tomorrow’s Market Minute and he’d like anyone who listens to have this article posted here to refer too. “TODAY is my last day at Goldman Sachs. After 12 years, the environment now is as toxic and destructive as I have ever seen it.” (Greg Smith is resigning today as a Goldman Sachs executive director and head of the firm’s United States equity derivatives business in Europe, the Middle East and Africa.)

(Click on image or HERE to read the whole article or continue reading below)

Why I Am Leaving Goldman Sachs

To put the problem in the simplest terms, the interests of the client continue to be sidelined in the way the firm operates and thinks about making money. Goldman Sachs is one of the world’s largest and most important investment banks and it is too integral to global finance to continue to act this way. The firm has veered so far from the place I joined right out of college that I can no longer in good conscience say that I identify with what it stands for.

It might sound surprising to a skeptical public, but culture was always a vital part of Goldman Sachs’s success. It revolved around teamwork, integrity, a spirit of humility, and always doing right by our clients. The culture was the secret sauce that made this place great and allowed us to earn our clients’ trust for 143 years. It wasn’t just about making money; this alone will not sustain a firm for so long. It had something to do with pride and belief in the organization. I am sad to say that I look around today and see virtually no trace of the culture that made me love working for this firm for many years. I no longer have the pride, or the belief.

But this was not always the case. For more than a decade I recruited and mentored candidates through our grueling interview process. I was selected as one of 10 people (out of a firm of more than 30,000) to appear on our recruiting video, which is played on every college campus we visit around the world. In 2006 I managed the summer intern program in sales and trading in New York for the 80 college students who made the cut, out of the thousands who applied.

I knew it was time to leave when I realized I could no longer look students in the eye and tell them what a great place this was to work.

Over the course of my career I have had the privilege of advising two of the largest hedge funds on the planet, five of the largest asset managers in the United States, and three of the most prominent sovereign wealth funds in the Middle East and Asia. My clients have a total asset base of more than a trillion dollars. I have always taken a lot of pride in advising my clients to do what I believe is right for them, even if it means less money for the firm. This view is becoming increasingly unpopular at Goldman Sachs. Another sign that it was time to leave.

How did we get here? The firm changed the way it thought about leadership. Leadership used to be about ideas, setting an example and doing the right thing. Today, if you make enough money for the firm (and are not currently an ax murderer) you will be promoted into a position of influence.

What are three quick ways to become a leader? a) Execute on the firm’s “axes,” which is Goldman-speak for persuading your clients to invest in the stocks or other products that we are trying to get rid of because they are not seen as having a lot of potential profit. b) “Hunt Elephants.” In English: get your clients — some of whom are sophisticated, and some of whom aren’t — to trade whatever will bring the biggest profit to Goldman. Call me old-fashioned, but I don’t like selling my clients a product that is wrong for them. c) Find yourself sitting in a seat where your job is to trade any illiquid, opaque product with a three-letter acronym.

…..read next page HERE

Now is the time when we Juxtapose:

For years now, US government bonds have looked like terrible investments, what with those trillion-dollar deficits and multiple wars and all. But Treasuries just kept rising, earning their owners nice returns and making their critics seem like financial illiterates who didn’t know a AAAA credit when they saw one.

Check out the chart for TBT, a 2X negative long-term Treasury ETF (in other words, a fund that bets against Treasury bonds). In case the price numbers are hard to read, this fund peaked at 70 in 2008 and has since fallen steadily if irregularly to less than 20. Far from being the short of the decade, Treasuries, especially if you were using leverage to bet against them, have been a sound-money investor’s nightmare. …

(Click on image for further reading)

….read more HERE

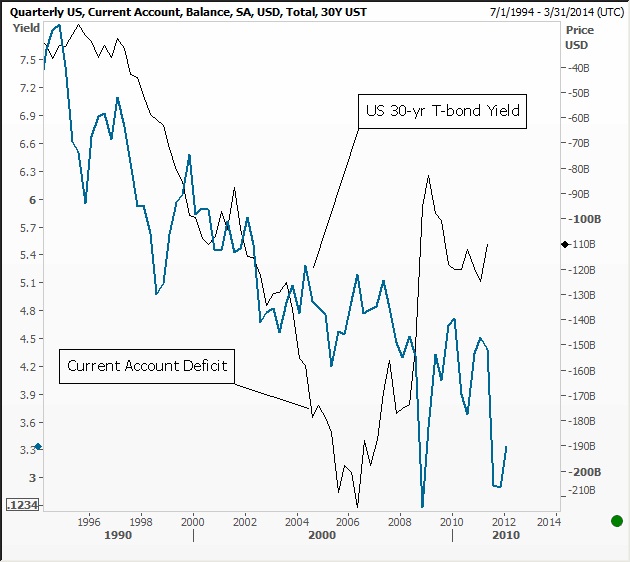

Watching the rise in US long-bond yields got me to wondering: What if the fall in the Japanese and Chinese current account surpluses continues, i.e. this trend is for real?

US Current Account Deficit (black) vs. 30-yr US Treasury Bond Yield (blue):

If so, it means both countries recycle less of their yen and yuan, respectively, back into the US capital markets. It means the global economy could finally see some rebalancing between the major deficit country, the US and surplus country, China. It means the US current account deficit, which seems to worry many people and economists alike, is likely to improve, as Japan and China morph increasingly into capital importers instead of capital exporters.

Has this rebalancing begun? We don’t know yet. But interestingly, given the needs for Japan to rebuild and China to change its growth model, it could very much be the next major global macro trend for the global economy. If so, there are three major implications, and several investment themes spawned:

Has this rebalancing begun? We don’t know yet. But interestingly, given the needs for Japan to rebuild and China to change its growth model, it could very much be the next major global macro trend for the global economy. If so, there are three major implications, and several investment themes spawned:

1) US long bond yields have likely bottomed (price topped), and

2) The next major growth phase for the global economy will be the rise of the Asian Consumer.

3) Global capital and trade flow will become a two-way street.

Some additional comments:

-

Japan may be morphing into a capital importer (first year-on-year trade deficit since 1980 was recorded in 2011). Interestingly, the tsunami and its devastation may have been the catalyst that leads to a normalization of the Japanese economy, i.e. rising interest rates, local commercial bank lending, and local business investment.

— Because of Japanese nuclear power going offline, Japanese imports of crude oil is up 350% compared to the same month last year.

— Normalization is part and parcel to a weaker yen as the game of risk aversion and “hiding” large pools of capital goes away.

-

China’s GDP growth will likely continue to fall (inherently reducing its giant reserve surplus), but this will not likely be a disaster if China’s growth model changesto support consumers (enriched consumers don’t care about GDP numbers; they care about reality) and moves away from State Owned Enterprises, which includes massive capital investment projects and consistent export subsidies of companies operating in the red or on wafer thin margins.

— No need to recycle surpluses and keep buying US Treasuries in order to keep the currency suppressed, because …

— A stronger yuan will increase consumer wealth, relatively, making the transition to a new model more efficient, i.e. benefiting import industries at the expense of exporters.

-

Asian-block countries will be relieved if China signals it is serious about making a transition that empowers its consumers. Asian-block nations who have implicitly and explicitly suppressed the value of their own currencies over the last several years thanks to China’s explicit currency suppression and growth model. Asian-block countries compete against China for the same Western demand. Thus, in the process of that competition, consumer market development across Asia as a whole has been stymied. Thus, China’s signaling of a change in its local growth model will likely be reinforced strongly across the region.

-

Stronger Asian consumer demand and stronger Asian currencies mean Western consumer goods flow more freely to the East and the US trade balance improves dramatically, and it will be quite good for Europe too. Thus, the US trade balance and need for external capital to close the current account gap will decline naturally as Asian consumer demand increases.

Risks to this rosy long-term scenario are many; here are just a few examples:

-

Contagion to emerging markets triggered by the European debt crisis could be severe …

-

Potential financial crisis in China as debt grows to dangerous proportions and unrest is met with more internal crackdowns on its citizens …

-

A major debt crisis in Japan, triggered by its need to import funds, but inability to see long-term interest rates rise (which is part and parcel to attracting funds from international investors) …

-

US remains mired in its seemingly “never-ending” war policy and do little to improve its unsustainable fiscal deficits …

Net-net if this major trend plays out, it means the US may avoid its fiscal train-wreck destiny and paradoxically if Chinese leaders trust their average citizens more, they will gain even more control of their own destiny.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair