Stocks & Equities

Over the years, we have discussed the various ways that companies utilize their free cash flow to generate a return for their shareholders. In our small-cap universe, we have traditionally focused on companies that reinvest their earnings back into the business to generate sustainable growth. More recently the markets have started focusing on companies that payout their cash flow to shareholders in the form of dividends or distributions. Even better are those companies that generate so much cash that they can afford to invest in growth as well as pay a dividend. But there is also a third method of allocating capital that is often misused and even more often misunderstood – share repurchases (buybacks).

The consensus is mixed on whether or not share repurchases are in fact a viable strategy for generating shareholder returns. When a company has excess cash and they believe their shares are undervalued, they will often issue a normal course issuer bid which allows them to purchase and cancel a predetermined maximum number of shares of their own company. The idea is that if you believe that your own company will provide you with the best risk-adjusted return on your capital then why would you invest your capital anywhere else.

Warren Buffet recently said in his 2012 letter to shareholders (http://www.berkshirehathaway.com/letters/2011ltr.pdf) that in addition to generating strong earnings growth he also typically hopes that the stock prices of the companies he purchases languish in the markets for several years after he buys them. Using an example of IBM, he explained that if the company were to spend $50 billion over a 5 year period to repurchase its shares that his current interest of 5.5% in the company would growth to 7% if the share price were to average $200 over the period, but only 6.5% if the share price where to average $300. Since Warren has no intention of selling his shares during that period his best case scenario would be if the cash flow remained strong but the stock price plummeted. This is a wide diversion from the mentality of many retail investors who require constant validation from the market in the form of appreciating stock prices.

The reason that share repurchases are often criticized is because they are very commonly misused. Very often companies will publicly disclose that they have received exchange approval to proceed with a share buyback but then fail to repurchase any shares. The hope is that the announcement alone will garner investor interest. The more common problem is when share repurchases are made by companies that are not undervalued. Warren Buffet said, “I favor repurchases when two conditions are met: first, a company has ample funds to take care of the operational and liquidity needs of its business; second, its stock is selling at a material discount to the company’s intrinsic business value, conservatively calculated. We have witnessed many bouts of repurchasing that failed our second test.” The CEO and Board of Directors commonly have a tendency to view their own company as undervalued, particularly if it has suffered a large decline in the share price. This bias can lead firms to repurchase stock when it is in fact overvalued, an activity which has the impact of destroying shareholder value.

The key to assessing a share repurchase strategy is to analyze the metrics of the individual situation. Does this company have the available liquidity to repurchase shares? Is the company clearly undervalued on the basis of free cash flow and will a share repurchase have the intended impact of improving performance on a per share basis? If the answer to these questions is yes then a share repurchase may be a very viable strategy for creating shareholder value long term.

Not if you’ve Mark Leibovit who argues that “Gold retraced into the mid 1600s as hoped, silver did not quite reach the desired 30-31 level. Meanwhile, should spot gold clear 1792 and spot silver clear 37.60, fasten your seat belts – a moon shot will then likely unfold before our eyes.“

The Financial Times – Bernanke’s QE silence a blow to gold price

The 5 per cent fall, gold’s largest daily drop in more than three years, has triggered a nervous reappraisal of the precious metal among some investors: how strong can the fundamentals of the market be, they ask, if a non-denial from the Federal Reserve chief can have such a marked impact? The nervous shake-out has continued this week with gold on Tuesday dipping below its 200-day moving average, a technical indicator closely watched by traders, for the first time since mid-January to touch a low of $1,664 a troy ounce. Many analysts and investors believe the eventual shift to monetary policy tightening by the Federal Reserve will mark the end of gold’s decade-long rally, which has lifted prices from less than $300 an ounce in 2001 to almost $2,000 last year. By promising to keep rates at zero until 2014, therefore, the Fed has pushed back the gold price peak, which many analysts had expected to come in late 2012 or early 2013. “The consensus within the Fed to extend the zero interest rate policy to beyond 2013 does, all other things being equal, imply an extension of the gold bull market,” says Philip Klapwijk, head of metals analytics at Thomson Reuters GFMS, a leading precious metals consultancy. “Maybe in the short term QE3 matters,” agrees a gold specialist at a large hedge fund. “The more important thing is that rates are on hold and I don’t think that is going to change.”

Marc Faber – Gold Far From Bubble Phase: Marc Faber

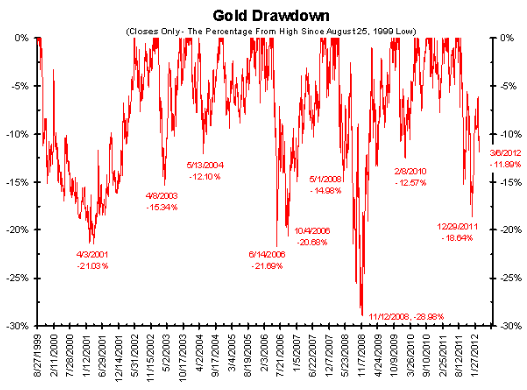

With more than 40 years as an economist to his credit and claiming gold as the “biggest position in my life,” Gloom Boom & Doom Report Publisher Marc Faber assures us that gold is nowhere near a bubble phase, but cautions that corrections of 40% are not unusual in a bull market. At the end of March, Faber will share his secrets for surviving corrections at the World MoneyShow in Vancouver. In advance of that appearance, he sat down with The Gold Report for this exclusive interview where he discusses his bias for portfolio diversification in terms of geographies as well as asset classes.

Also from Marc Faber March 9th/2012 –Marc Faber : Gold Price may not exceed the $1,922/oz in 2012

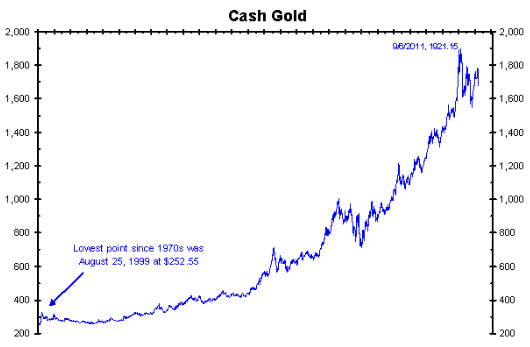

“This year the Gold Price may not exceed the $1,922/oz high that we reached on Sept. 6. Maybe it will. I’m not a prophet. I’m just telling people that I’m Buying Gold and holding it. I don’t speculate in gold. If you Buy Gold, you better understand that the price could always move to the downside. If you don’t understand that, don’t invest in gold—or in anything.”Mark Leibovit’s Daily Gold Comment (More on Mark’s services is available at http://www.vrtrader.com/login/index.asp including a Trial Offer. Mark was #2 Gold Timer for 2011 and the #1 Gold Market timer for the 5 year period ending in 2010)

Mark Leibovit’s Daily Gold Comment via Don Vialoux’s Timing the Market:

–GOLD – ACTION ALERT – BUY (Continue to look to take delivery of the physical metals)

Short-term, gold and silver are continuing to bounce off oversold positions. While gold retraced into the mid 1600s as hoped, silver did not quite reach the desired 30-31 level. Meanwhile, should spot gold clear 1792 and spot silver clear 37.60, fasten your seat belts – a moon shot will then likely unfold before our eyes. The sell-off was clearly ‘engineered’ and the scoundrels could easily engineer another one at a moment’s notice. This is why I encourage ‘stacking’ silver and gold. In other words, using weakness to accumulate the physical metal and put it in a place where government can’t get it or find it. I’ve been asked when will be the time to sell silver or gold. Will it be when it hits a particularly high price such as $11,000 in gold or $500 in silver? I cannot answer that question with any great certainty this morning, but my gut feeling is the time to sell will likely be when THE ENTIRE STRUCTURE OF THE WESTERN FIAT BANKING SYSTEM COLLAPSES AND SOMETHING ELSE IS ABOUT TO REPLACE IT!

Recent recommendations by Mark include purchases of Taseko (TGB), Smith & Wesson(SWHC), Market Vectors Gold Index(GDX), North American Palladium(PALL) and the High Yield Bond ETF(JNK)

MINING.com editor Andrew Topf sits down with mining analyst Mickey Fulp, who topped the site’s list of recommended mining bloggers and newsletter writers. In this brief interview on the sidelines of the PDAC convention in Toronto, Fulp touches on gold stocks, current market volatility, and two metals he likes best right now: uranium and graphite.

Andrew Topf: What metals are you bullish on right now?

Mickey Fulp: Copper, gold and uranium, and I’ll put graphite into that too.

Andrew Topf: Right, graphite seems to be the belle of the ball right now.

Mickey Fulp: It is, it’s the next big thing it reminds me very much what happened with REEs in 2009. We’re building a bubble in graphite, every snake oil salesman, shark and charlatan is swimming aorund in Coal Harbor in Vanouver right now. Every Vancouver promoter is scurrying around trying to find a shell to throw a graphite project in, so it looks very much like the next big thing. Like other area and commodity plays the juniors will rush in and 95% of them will fail and the ones with good deposits and good business plans will succeed.

…..read the entire interview HERE

Food prices are skyrocketing all across the globe, and there’s no end in sight. The United Nations says food inflation is currently at 30% a year, and the fast-eroding value of the dollar is causing food prices to appear even higher (in contrast to a weakening currency). As the dollar drops in value due to runaway money printing at the Federal Reserve, the cost to import foods from other nations looks to double in just the next two years — and possibly every two years thereafter.

That’s probably why investors around the globe are flocking to farmland as the new growth industry. “Investors are pouring into farmland in the U.S. and parts of Europe, Latin America and Africa as global food prices soar,” reports Bloomberg magazine HERE. “A fund controlled by George Soros, the billionaire hedge-fund manager, owns 23.4 percent of South American farmland venture Adecoagro SA.”

Jim Rogers is also quoted in the same story, saying, “I have frequently told people that one of the best investments in the world will be farmland.”

That’s because demand for food is accelerating even as radical climate changes, a loss of fossil water supplies, and the failure of genetically engineered crops is actually reducing food yields around the globe. Ceres Partners, which invests in farmland, has produced astonishing 16 percent annual returns since its launch in 2008. And this is during a depressed economy when most other industries are showing losses.

….read (scroll down) “Why growing and storing your own food can be a goldmine” & “Lessons from post World War II Taiwan and why food is more valuable than gold” HERE

What Now

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair