Currency

“Where there is a crisis, there may be opportunities – but not necessarily in the places one might expect.”

“the course Europe is on may avoid chaos now, but may lead to disintegration down the road. These are serious matters, as the odds of anarchy, followed by military control of Greece have increased substantially. When we suggest that the road to hell is paved with the best of intentions, we are serious.

What does it mean for the euro? Massive short positions previously built-up need to be unwound. As central bankers around the world hope for the best, but plan for the worst, lots of money is being printed: by the Fed, the ECB, the Bank of England (BoE) and Bank of Japan (BoJ), to name the prime instigators. Commodity currencies, i.e. the Australian Dollar (AUD), New Zealand Dollar (NZD) and Canadian Dollar (CAD) should be the main beneficiaries. While these currencies have performed well, Australia is undergoing some domestic political turmoil and Canada’s fate is closely linked to that of the U.S.; as a result, the NZD would be our favorite in that group. Having said that, geopolitical tensions and monetary easing have boosted oil prices in particular, causing headwinds to global economic growth and, with it, also to commodity currencies. If those headwinds play out further, we would make the Norwegian Krone (NOK) our preferred choice, as Norway benefits from rising oil prices, as well as providing investors with relative safety in Europe. It’s not surprising that gold, the one currency with intrinsic value, continues to appreciate in this environment.”

….read the whole article HERE

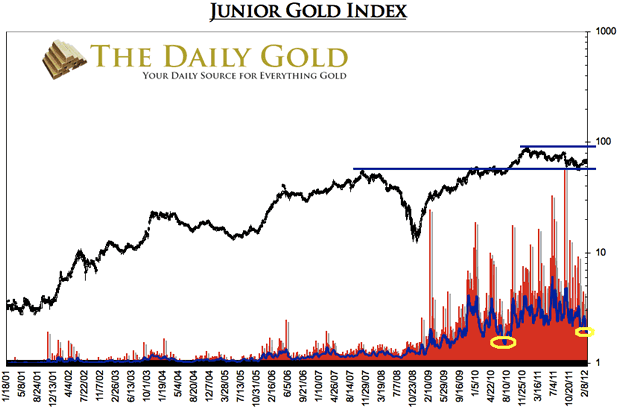

Juniors are typically micro-cap exploration companies. Yet, GDXJ the junior ETF is comprised of companies with market caps in the $500 Million to $1 Billion range. There is nothing junior about that. We notice there is a gap in terms of terminology. If Juniors are sub- $100 Million, and large caps are over $1 Billion, then what do you call those that fit the gap?

We prefer to use the term “established juniors” or small cap. After all, small caps by definition are in market cap between $100 Million and $1 Billion. These terms are most appropriate for those in the middle of said range rather than the bottom or top. We prefer the established juniors as being established (which is open to interpretation) they have less risk than the true juniors and if successful can grow to $1 Billion or more in capitalization.

In our opinion, small caps are the area to focus on as they have a much greater likelihood of growth and leverage to Gold than the large producers. Historically, the large producers do not outperform Gold on a consistent basis. The law of numbers combined with the difficulty of the mining business explains why.

Our junior/small cap index consists of 20 stocks equally weighted with a median market cap of about 600 Million. In the second half of 2010 the market broke to new highs for the first time since 2007. With every breakout comes a retest. Heading into 2011 we predicted the retest would last into the summer. The retest lasted the entire year but appears to be successful.

Our bet is that the small caps will work their way back to the high before the end of the summer. It will take the time to overcome resistance but the trend will remain higher. If and when the market makes a new all-time high it will be very bullish for several reasons. It would be the first sustained breakout to a new all-time high since 2005-2006. It would come at a time when the bull market is starting to transition out of the wall of worry phase. Finally, it would generate significant momentum when overhead resistance is basically nil.

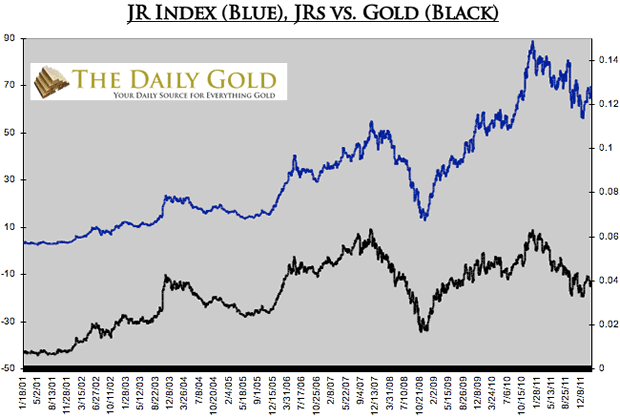

This is possible due to a combination of Gold rising and present low valuations improving. In the next chart we graph our index and the ratio of our index to Gold. Gold companies are generating record profits and the price of Gold is near its all-time high yet leveraged small caps are trading near a low relative to Gold. That, in our view is a function of market sentiment and evidence of the wall of worry stage.

f the ratio would rise back to its 2007 and 2010 highs at 0.065 and Gold would reach $2000, our small cap index would just about double. That is right, a potential 100% gain.

The bottom line is small cap gold stocks have completed a textbook breakout and retest. As we said, the market will likely have a hard slog for the next several months as it encounters supply from the 2011 correction. If and when the market nears its old high it will have built up the necessary strength and momentum to embark on an explosive breakout. Thus, now is the time to be doing your due diligence to find and research those candidates to lead the market in a potential rip roaring move into 2013.

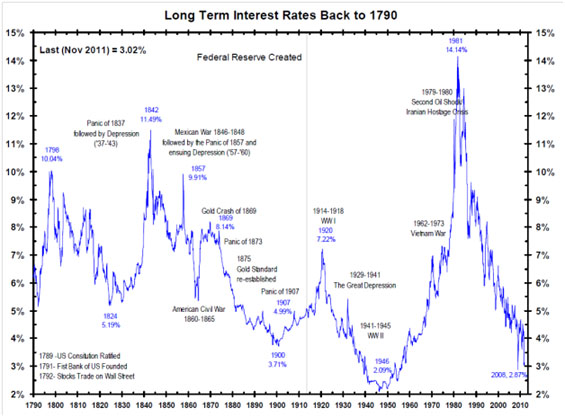

Danielle addresses the challenge posed by generational low interest rates and dividend yields, especially to retirees. The chart shows that in the past 220 years interest rates have been lower than the current 2.87% only once, in 1946.

TGR: In your book, Juggling Dynamite: An insider’s wisdom about money management, markets, and wealth that lasts, you advise against a buy-and-hold strategy. How can individual investors pick the right time to buy and sell stocks in a volatile market?

Danielle Park: When I talk about avoiding buy-and-hold, I mean being aware of this secular bear phase. We are in year 12 of a 15 to 20 year cycle. During secular bears you get recessions every three or four years, during which stocks tend to lose about 45% of their value. It is not a good reward for the risk to hold a stock on such a wild rollercoaster; even if it is paying you some dividends, the emotional and financial costs to your capital are just too extreme.

Today, I tell people: first of all, pay off your debt. Second, downsize your non-productive assets like personal use real estate. Third, figure out how to increase your income through your ingenuity and effort. Once you have a pile of savings you have a couple of choices.

You could decide to stay out of equity markets completely and put your money in short-term deposits. Even though they pay very little, they keep your capital intact to fight another day. This is a very reasonable approach and, frankly, is the one most people should take.

Another approach is to pare off a portion of your capital and trade with that. You might take 20% of your assets out of guaranteed deposits and hire a money manager or see if you can trade day-to-day swings. This is extremely hard to do with success, but if you can define the portion of your life savings you are willing to risk and maintain that discipline, it may be a reasonable idea to try with a controlled portion of your money.

The disastrous approach in my view, which many people are doing today is to give 50%, 60% or 70% of their life savings to brokers and financial planners to plop it into equities without paying any attention to the secular climate or to whether we are approaching the next recession or to where market prices are. They plop it in with reckless disregard, and within short order a huge chunk of capital could vaporize.

If that is the approach offered, then I say you are better off avoiding stocks altogether and sticking with interest-bearing, short-term deposits. Keep your capital safe and wait until conditions improve in the next few years.

TGR: Danielle, you recently wrote in EQ Trend Watch about the challenge posed by generational low interest rates and dividend yields, especially to retirees, illustrated with a chart showing that in the past 220 years interest rates have been lower than the current 2.87% only once, in 1946. When might that shift?

DP: That interest chart shows definite secular swings. Rates trend higher for 25 to 30 years and then lower for about the same time period. We are about zero-bound now, so we ought to be heading into a rising rate environment again.

TGR: Will global problems like the European debt crisis prolong low interest rates or cause inflation to rear back?

DP: We have a pretty complex little puzzle right now. I believe a global recession is coming in the next 12 months or is already underway. The U.S. was the only country in the developed world with any positive momentum in Q411. Even that was the result of trillions of dollars of deficit spending and debt. Going into 2012, the headwinds are mounting.

Most European countries are in recession. The austerity measures the International Money Fund and the EU are insisting on for Greece, Portugal and Ireland are a self-fulfilling prophecy of deep recession. China recently cut its reserve ratios for its banking system out of concern about a drop-off in shipments and demand from its best customers.

The other side of the coin is what happens when countries become so indebted that their bond yields suddenly begin to spike because of credit concerns. That is when central banks ultimately lose control of the bond market. We have the likelihood of policy rates remaining extremely low—Ben Bernanke says until 2014. The U.S. recently added another $1.6 trillion to its debt; the amount of money owed is mind boggling. For 20 years, Japan pushed rates to zero and tried to control interest expense because its economy was so indebted. However, despite or really because of its efforts the economic malaise continued and Japan is back in recession today.

Worse, today we have a world of Japans; there is nowhere to look for better yields. When all countries are going through a similar dynamic with credit agencies downgrading in concert, you have to wonder how the bond market will force rates higher when there are relatively few options to go to. Recently, global money has shown a strong appetite for the U.S. dollar and the U.S. bond market as a safe haven. But, at some point—and probably sooner than many people think—even that will become a credit risk.

TGR: Will anemic interest rates, fear of debt and inflation and currency problems continue to support rising commodity prices, particularly gold?

DP: Yes and no. Oil has been trading above $105 per barrel on fears about Iran. When oil appreciates dramatically, that puts a huge tax on an already weak consumption base; we have seen that in lower U.S. gasoline consumption for example. So yes, the geopolitical scenario may continue to feed a fear premium on sectors like energy.

However, in the liquidity crunches of 2001–02 and again in 2008–09, we saw levered players in equities and the commodity space sell across the board because cash became the desperate elixir that everybody wanted to meet margin and redemption calls. The selling becomes a self-fulfilling circle. When that happens, it hits everything, including gold. As a result, I think the price of commodities could fall off again and much harder than many people today are thinking possible.

TGR: You paint a pretty dark picture. Based on historic bear periods, how much downside do we have to go before we get into another bull cycle?

DP: We have had six secular bear phases in the last couple of centuries, each lasting 15 to 20 years, followed by a secular bull phase of similar duration. The secular bear market starts with massive overvaluation, anemic dividend yields, over-levered consumers and weak savings rates. We have to work our way through that. Debt gets paid down or written off. Consumers build up their savings. They learn to live on less. They become more resilient. At the end of the period, they are in better shape than at the beginning. This sets up the next secular boom phase.

From all the sign posts on this process, we are not through the bear phase yet. The price/earnings ratio on equities in general is still well above 20. That is not the valuation levels from which secular bulls are born. Dividend yields are below 3%. At the start of a secular bull phase, they are more likely to be double that. Saving rates need to be above 10%. They are now around 4% in the U.S. and Canada. We will not get into a period of greater economic strength until debt levels fall and savings are built back up.

I think the most important thing individuals can do is be self-protective, realistic and patient, because all of this comes full circle. We are now working our way through the healing process. We have probably another five years or so to get debt levels paid down and savings levels built up.

People do not have to be decimated by this. They need to realize this is not a time to embrace a lot of risk. It is not the time to retire on a couple hundred thousand bucks or even a couple million bucks. Be pragmatic and protect what you have. Keep working to augment your income. If you have too much non-income producing real estate or are over-levered, figure out how to pay it down. If you do this, you will have liquid assets, capital, savings and the ability to buy things when the opportunities arrive.

TGR: When the market comes back will certain sectors or subsectors improve faster than others?

DP: As an asset class, I call equities jelly beans. Do I like red jelly beans more than purple jelly beans or more than yellow jelly beans? They are all similar. My preference would be to earn income, first of all. You would like to have dividend-paying instruments and small caps tend to produce very little income. But price is also very important. If you buy something today for a 3% dividend and it drops 20% to 30% in value, it will not feel like you got a good deal or made a prudent move. What you want to do is let the price risk come out of the asset. Lower prices mean lower risk to capital. When dividend yields are twice what they are now, you can allocate some capital to jelly beans of all the colors you want. But, basically all of the jelly beans move together. When capital flow leaves the market, it leaves everything. When capital flow returns, it goes back into everything.

Central bankers are trying to stop asset values from declining. The status quo keeps trying to pump prices up and keep them at unattractive valuations. There is a push-and-pull going on. Eventually gravity wins. Central banks will not prevail, asset prices will continue to move lower and that will be a very healthy thing.

TGR: Can investors take some of the risk out by being active investors and being smart about what they invest in?

DP: Sure. There are lots of ways to be smart. I am a trained financial analyst and in the ’90s I spent a lot of time studying management, pouring over balance sheets and income statements. I came to the conclusion that it was a complete and utter waste of time.

I may decide a company is excellent and the management is wonderful. I think it is worth $20/share, but it is trading at $40/share. You have to decide: Will you buy it anyway or will you be disciplined about the price you are willing to pay? Very few people have the discipline to stick to a set of rules.

We follow a regimented set of rules that takes into account many factors, that looks for opportunities. We have successfully executed that discipline over many years, but it is not easy. Ours is not a day trading system, but a longer trend approach that selects sectors and indices rather than individual companies.

I describe it as a person holding a piece of paper right up to the end of her nose, trying to read what is on the paper. If she held the paper at arm’s length, it is much easier to read and understand the bigger picture. The minutiae rarely help you navigate the broader picture of capital market cycles.

Investing in a local business owner is different. You can see what he is doing. His company is not traded in the public auction of stock markets. If you want to invest in the triplex up the street, you can fix it up, monitor it and rent it. Individuals can be well-equipped to make those kinds of assessments. Publicly traded assets are a whole other kettle of fish.

TGR: If someone has a good, trained money manager, is it worth it to take advantage of some of these opportunities?

DP: Well, of course. I happen to be a money manager, so I hope people think it is still worthwhile to hire some of us. People need to ask themselves two questions. The first is how much capital should I apportion to that approach? The second is what were my money manager’s returns in 2001 and 2008 when the markets lost half its value?

Too many people ask, what was your return last year? What will you get for me? In a rising market, everything gets capital flow. You do not need much skill to allocate capital in a rising market. It does take skill to protect capital in a falling market. If a manager lost in step with down markets, it tells you his strategy is not worth the fee. That manager is simply riding flows up and letting your capital fall along with everything else. In a secular bear environment you will be one of the masses, devastated and trying to liquidate at the last moment. You will not have the psychological strength you need to maintain liquidity and to know what you want to buy when prices sell off. Only a handful of money managers exercise the discipline to protect your capital in this kind of environment and can participate in the upside where it presents.

TGR: Will you share your strategies for the down years?

DP: Sure. We actually have achieved positive returns throughout, but it has not been easy. Our investors have had to be content with years where they made 1% or 2% in order to be prepared for downturns in years like 2008, when we made more than 8%.

Mainstream economists, commentators and politicians never see recessions coming even though they are regular features of a secular bear market. They occur every three or four years and they are catastrophic for capital. Rather than focusing on being there for all the gyrations to the upside, it is far more important to be as protected as possible from the downside.

The only way to survive is to have your own set of rules that work for you, or to have an independent manager who does not work for the sell side. You want an absolute return manager who says, I don’t want to lose money in any particular year, so our benchmark is to always advance the capital, even if the advance is small in a given year. The whole focus is on not losing, because once you lose, it sets you back years.

TGR: What was the role of gold and gold equities in your strategy during the down years?

DP: I think it is a mistake to think of gold as a separate asset class that is impervious to the panic swings in the market. When things sell off in concert, these assets sell off, too. Gold has been in a secular bull run for a long while, and it may go higher. But secular bulls always come to an end. When you are 12 years into a secular run, you have to at least be thinking about the possibility of it coming to a peak like we did in 1980.

My second caveat is this nonsensical idea that gold is the only thing that cannot be manipulated. Anyone who has studied the history of gold could not make that comment with a straight face. Humans have always found ways to lie about how much gold is in reserve whether it be in bank vaults, Fort Knox or in the ground at a particular mine. The incidents of fraud and manipulation around gold are legendary. If you don’t realize that, you are in grave danger.

TGR: Your talk at the World MoneyShow in Vancouver on March 28 is called “The Best Way to Make and Protect Gains That Most Financial Advisors Will Never Tell You.” Can you give our readers a sneak preview?

DP: I start out with some big picture stuff. For example, the best way to make money in the stock market is not to be a buyer in the stock market but to be a seller to the stock market. Take an enterprise you built and sell it in an initial public offering (IPO) that creates billions of dollars for the original investors. But, the investment public should be extremely cautious and skeptical about IPOs because those instruments are always brought in at the peak of a valuation. After it is marketed to the investment public, it is common for those shares to lose 30%, 40%, 50% in short order.

Another example is the importance of knowing your sell point before you buy anything. Very few people do this. They see the stock market as an endless mountain. They think, if I start climbing today, 5, 10 or 15 years from now I will be higher than I am today. Not in a secular bear market. The secular bear market is range bound. You will climb up, then come back and retest, four or five times before that period ends.

I am not dispensing conventional wisdom. Yet, in the 20 or so years I have been managing risk for myself and others, these are the things I have learned that are most important to long-term success. I try to pull back that piece of paper stuck to the end of everyone’s nose and say, hey look, this is the big picture.

TGR: Any last thoughts for our readers?

DP: Good luck and I wish them well. And remember, it is not dark to be a realist and be a pragmatist. I believe it is the best way to survive and thrive through all market conditions..

TGR: Thank you so much for your time and your insights.

Portfolio manager, attorney, finance author and a regular guest on North American media, Danielle Parkis the author of the best selling myth-busting book Juggling Dynamite: An insider’s wisdom on money management, markets and wealth that lasts, as well as a popular daily financial blog Juggling Dynamite.Park worked as an attorney until 1997 when she was recruited to work for an international securities firm. Becoming a Chartered Financial Analyst (CFA), she now helps to manage millions for some of North America’s wealthiest families as a portfolio manager and analyst at the independent investment counsel firm she co-founded, Venable Park Investment Counsel Inc. In recent years Park has been writing, speaking and educating industry professionals as well as investors on the risks and realities of investment behaviors. She is a member of the internationally recognized CFA Institute, Toronto Society of Financial Analysts and the Law Society of Upper Canada.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

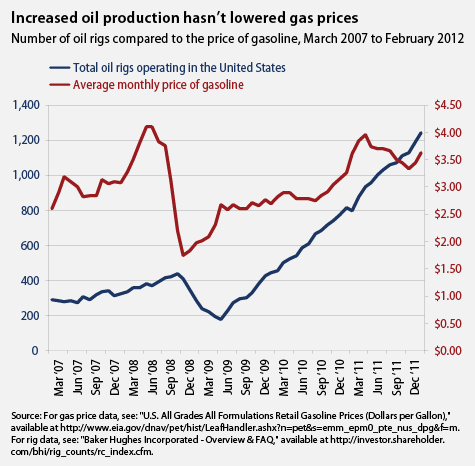

This month, as unleaded gasoline prices increased for 17 consecutive days (to a national average of $3.647 per gallon – up 11% thus far this year) and West Texas Intermediate crude joined Brent crude in breaking through a $100 per barrel level, energy prices emerged as a full blown political issue. While President Obama conveniently claimed that rising prices were the consequence of an improving economy (they’re not, and it isn’t) Republican fingers began to point sanctimoniously at current drilling policies. And while none of the accusers had any idea why prices were actually going up, the award for the most dangerous ‘solution’ must go to Bill O’Reilly at Fox News. The master of the “No Spin Zone” announced that high pump prices could be permanently brought down by a presidential order to restrict exports of refined gasoline. Not only does Mr. O’Reilly’s idea demonstrate contempt for the U.S. Constitution but it also displays a thorough lack of economic understanding.

Oil and gas prices are high now for a very simple reason: the U.S. Federal Reserve has gone on an unapologetic campaign to push up inflation and push down the value of the U.S. dollar. Just last week on CNBC James Bullard, the President of the Federal Reserve Bank of St. Louis, stated this unequivocally. What is somewhat overlooked is the degree to which an inflationary policy at home creates inflation abroad. Many countries who peg their currencies to the U.S. dollar need to follow suit with the Fed. As China, for example, prints yuan to keep it from appreciating against the dollar, prices rise in China. This is especially true for commodities like crude oil.

Many critics, such as Mr. O’Reilly, have relied on a limited understanding of the supply/demand dynamic to question why gas prices are currently so high at home. With domestic gasoline production at a multi-year high and domestic demand at a multi-year low, he logically expects low prices. But he fails to grasp the fact that the price of gasoline is set internationally and that U.S. factors are only a component.

O’Reilly’s loudly proclaimed solution is to limit the ability of U.S. refiners (and drillers) to export production abroad. If the energy stays at home, he argues, the increased supply would push down prices. Although O’Reilly professes to be a believer in free markets he argues that oil (and gasoline by extension) is really a natural resource that doesn’t belong to the energy companies, but to the “folks” on Main Street. What good would “drill baby drill” do for us, he argues, if all the production is simply shipped to China?

First off, the U.S. government has no authority whatsoever to determine to whom a company may or may not sell. This concept should be absolutely clear to anyone with at least a casual allegiance to free markets. In particular, the U.S. Constitution makes it explicit that export duties are prohibited. Furthermore, energy extracted from the ground, and produced by a private enterprise, is no more a public good than a chest of drawers that has been manufactured from a tree that grows on U.S soil. Frankly, this point from Mr. O’Reilly comes straight out of the Marxist handbook and in many ways mirrors the sentiments that have been championed by the Occupy Wall Street movement. When such ideas come from the supposed “right,” we should be very concerned.

But apart from the Constitutional and ideological concerns, the idea simply makes no economic sense.

In 2011 the United States ran a trade deficit of $558 billion. For now at least America has been able to reap huge benefits from the willingness of foreign producers to export to the U.S. without equal amounts of imports. China supplies us with low priced consumer goods and Saudi Arabia sells us vast quantities of oil. In return they take U.S. IOUs. Without their largesse, domestic prices for consumers would be much higher. How long they will continue to extend credit is anybody’s guess, but shutting off the spigots of one of our most valuable exports won’t help.

In recent years petroleum has become an increasingly large component of U.S. exports, partially filling the void left by our manufacturing output. According to the IMF, the U.S. exported $10.3 billion of oil products in 2001. By 2011, this figure had jumped nearly seven fold to more than $70 billion. How would our trading partners respond if we decided to deny them our gasoline?

Keeping more gasoline at home could hold down prices temporarily, but how much better off would the “folks” be if all the prices of Chinese made goods at Wal-Mart suddenly went up, or if such products completely disappeared from our shelves because the Chinese government decided to ban exports that they declared “belonged to the Chinese people?” What would happen to the price of energy here if Saudi Arabia made a similar decision with respect to their oil?

But most importantly, limiting the ability of U.S. energy companies to export abroad will do absolutely nothing to improve the American economy. As a result of our diminished purchasing power, American demand for oil has declined in relation to the growing demand abroad. Consequently, we are buying a continually lower percentage of the world’s energy output. Consumers in emerging markets can now afford to buy some of the production that used to be snapped up by Americans. If U.S. suppliers were limited to domestic customers, then prices could drop temporarily. But what would happen then?

With the U.S. adopting a protectionist stance, and with gasoline prices in the U.S. lower than in other parts of the world, less overseas crude would be sent to American refineries. At the same time lower prices at home would constrict profits for domestic suppliers who would then scale back production (and lay off workers). The resulting decrease in supply would send prices right back up, potentially higher than before. The only change would be that we would have hamstrung one of our few viable industrial sectors. (For more about how diminishing supplies could exert upward pressures on a variety of energy products, please see the article in the latest edition of my Global Investor newsletter).

Mr. O’Reilly can spin this any way he wants it, but he is dead wrong on this point. It is surprising to me that such comments have not sparked greater outrage from the usual mainstream defenders of the free market. To an extent that very few appreciate, America derives a great deal of benefits from the current globalization of trade. Sparking a trade war now would severely reduce our already falling living standards. And given our weak position with respect to our trading partners, such a provocation may be the ultimate example of bringing a knife to a gun fight.

Rather than bashing oil companies, O’Reilly, as well as other frustrated American motorists, should direct their anger at Washington. That is because higher gasoline prices are really a Federal tax in disguise. The government’s enormous deficit is financed largely by bonds that are sold to the Federal Reserve, which pays for them with newly printed money. Those excess dollars are sent abroad where they help to bid oil prices higher.

For years, mainstream economists argued that as long as unemployment remained high, the Fed could print as much money as it wanted without worrying about inflation. The argument was that the reduction in demand that results from unemployment would limit the ability of business to raise prices. However, what those economists overlooked was the simultaneous reduction in domestic supply that results from a weaker dollar (the consequence of printing money).

I have long argued that neither recession nor high unemployment would protect us from inflation. If demand falls, but supply falls faster, prices will rise. That is exactly what is happening with gas. The same dynamic is already evident in the airline industry. Fewer people are flying, but prices keep rising because airlines have responded to declining demand by reducing capacity. Since seats are disappearing faster than passengers, airlines can raise prices. At some point Americans will be complaining about soaring food prices as much more of what American farmers produce ends up on Chinese dinner tables. Because the Fed is likely to continue monetizing huge budget deficits, Americans are going to be consuming a lot less of everything, and paying a lot more for those few things they can still afford.

For full access to the March 2012 edition of the Global Investor Newsletter, click here

1. Ancient wisdom says, “your friend is your enemy and your enemy is your friend”. In the gold & silver market, this ancient wisdom may be particularly valuable for investors today.

2. Gold plays the role of punisher in this crisis, and punishes the debt-a-holics. The crisis is enormous, and could go on for decades, but just because the crisis may have decades to run doesn’t mean that gold rises forcefully, all the time.

3. The economy can have enormous bouts of strength while slowly disintegrating, and you have all seen the shockingly bullish economic reports pouring out, in recent months. Analysts continue to under-estimate the economic numbers.

4. Something has got to give here; either the analysts are correct and economic numbers are about to nose-dive, or the economy is surfing a much bigger up wave than the analysts comprehend.

5. You can click here to view a larger version of the current gold chart below. Note the small head and shoulders top pattern in play, and the broken uptrend line. I personally couldn’t care less about the microscopic fall in price implied by this technical action. I’m only interested in buying price sales of $100 or more.

{kind=link}

6. My interest lies with the divergence between gold and silver, and why that divergence may be occurring. Silver investors can click here for a larger version of the chart below. I’ve talked about the importance of silver investors holding your ground against “big sister gold”. Life as the little brother can be frustrating at times, but this could well be your time to shine, but not because silver is “poor man’s gold”.

{kind=link}

7. Last night the price of silver ripped thru its right shoulder high, and the price action is beginning to resemble the action of the Dow, even more so than that of gold. Click here to view a larger version of the Dow “chomping at the 13,000 point bit”. Silver’s price action in the $36 area is very similar to the price action of the Dow in the 13,000 point area.

{kind=link}

8. If we are on the cusp of an institutional capitulation, one that acknowledges that a much bigger recovery has started, then silver, platinum, and palladium could all out-perform gold.

9. If not, then silver is likely to resume its role as “gold’s sidecar”, and still fare pretty well. Platinum and palladium may not fare as well as silver if the crisis accelerates dramatically.

10. Gold appears to be silver’s best friend, but if a shocking economic revival is just around the corner, perhaps it is the supposed enemies of silver, the Dow and real estate, who will become silver’s friends, at least for a period of economic time.

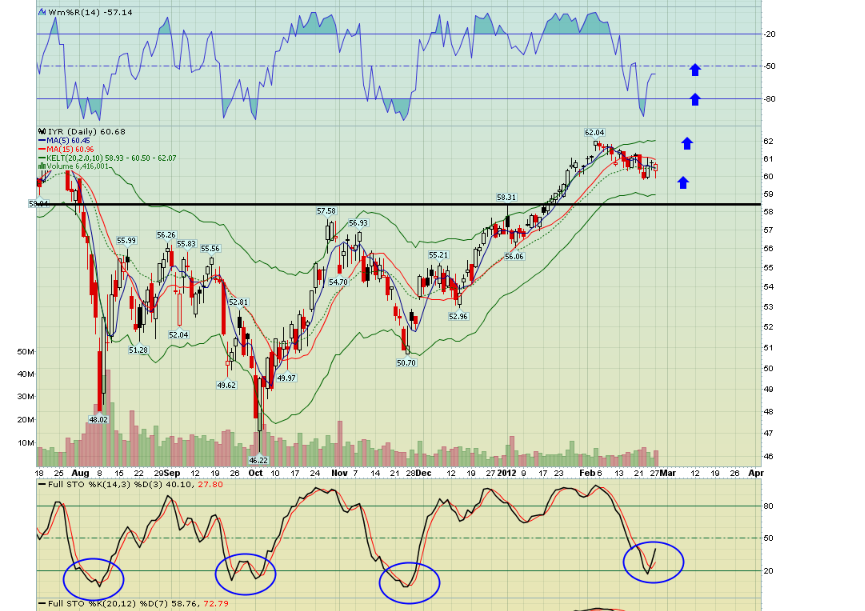

11. How big of an economic surge am I talking about? To view the shocking super-rally in real estate that I am predicting, click here for a larger chart.

{kind=link}

12. That’s the IYR-nyse real estate ETF from ishares, and I’m predicting a near-immediate rise in price to my $100 price target, a scenario that will cause 99% of the gold community to do the ultimate “double take”.

13. There’s an enormous head & shoulders pattern on the monthly chart, and the daily chart also looks extremely positive. Click for a larger chart here. Note the position of the Stochastics oscillator, and the solid support in the $58 price range.

14. Both real estate and the Dow may add surprising fuel to the silver rally, but that doesn’t mean you should buy today. Bullish price patterns reveal where price might go on the upside, but they are not buy signals.

15. It’s critical to understand that surprise is the theme of this crisis. It’s equally critical to understand that the markets are a fight more than an investment. You don’t really have “fellow investors”. You have opponents that you need to ravage and destroy. You can face that fact, or be destroyed by those who live the markets in fight-mode.

16. You can’t buy silver after it has skyrocketed, because you will be buying it from strong hands, and doing so alongside weak hands. If you don’t feel morbid when you buy, don’t buy.

17. What’s better, to feel morbid when you buy, or morbid when you sell out at a loss? Buy in the morbid zone and sell in your personal party and analysis zone. Those who want to feel good both on the buy and on the sell are likely living a pipedream.

18. If we are entering a period of shocking economic growth, albeit growth printed out of an electronic photocopier machine, then perhaps silver and other industrial-precious hybrid metals will substantially outperform gold for a period of time.

19. If real estate joins the Dow in ravaging the dollar, then gold stocks could also join silver in outperforming gold. I’m fully aware that most of the gold community is highly invested in gold stocks, with many in the community owning no gold bullion at all.

20. While the policy of holding no gold bullion is a bad mistake, that doesn’t change the fact that it could be your time to shine, if you are all-in on gold stocks. Real estate and the Dow, the gold stock community’s “enemies”, may soon become your trusted friend, for at least a period of time.

21. You can click here for a larger chart to view the GDX chart. I’m an immediate buyer at the $55.50 and $53.50 price points. Note the action around the $58 price point. GDX is attempting to blast over the red trend line. If the Dow surges through 13,000 and the IYR rips up through $61.68, I think GDX could experience a “price flash” to $70.

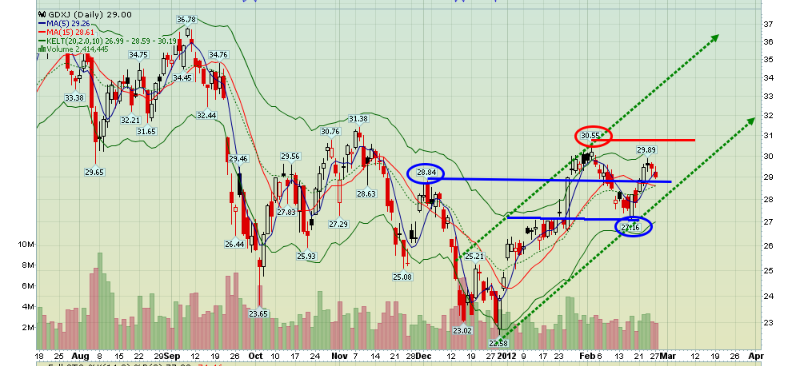

22. The incredible 35% rally in gold junior stocks, via GDXJ, has been all but forgotten, and with good reason. Most gold junior investors are 50-70% underwater, and more so in some cases. Just because the Dow investors of 1929 were wiped out didn’t mean the Dow couldn’t rise from the ashes, and it is the same with junior gold stocks today.

23. Click here for a larger chart to view the asset class most likely to continue the out-performance that it began two months ago. GDXJ has entered an uptrend channel and is showing light volume on this decline.

24. You should be an immediate buyer of GDXJ at $27.16, if you are lucky enough to see price go there. If you like gold junior stocks, stare hard into the copper, real estate, platinum, and palladium charts. Those asset classes look set to blast higher and may drastically outperform gold!

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

Tuesday Feb 28, 2012

Special Offer for 321Gold readers: Send an email to freereports@gracelandupdates.com and I’ll send you my free “Platinum & Palladium, Your Spaceship To Mars?” report!

Graceland Updates Subscription Service: Note we are privacy oriented. We accept cheques. And credit cards thru PayPal only on our website. For your protection we don’t see your credit card information. Only PayPal does.

Subscribe via major credit cards at Graceland Updates – or make checks payable to: “Stewart Thomson” Mail to: Stewart Thomson / 1276 Lakeview Drive / Oakville, Ontario L6H 2M8 / Canada

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair