Timing & trends

Overall Perspective

- At the end of September the prevailing panic atmosphere could no longer drive down stocks, commodities and corporate bonds. Some of our technical work was indicating a large and growing number of individual stocks registering very oversold conditions. The gold/silver ratio which had signaled the pending decline in April resisted going higher.

- The conclusion was that choppy, but rising action for orthodox investments could run to a good high at around January.

- For the past few weeks we have been reviewing the question “Are we there yet?”

- Yes we are – and then some!

Credit Markets

- Excess is again evident in the credit markets and a couple weeks ago an outstanding performer–municipal bonds (MUB) – registered an Upside Exhaustion. As the reversal comes in, we’ve thought that it would represent the potential reversal in bullishness for most spread products.

- This would include corporate and sub-prime mortgage bonds.

- A few days ago the MUB dropped a couple of points from 113.67 to 112.50. This is the sharpest plunge since the one in October 2010 that led to the “Muni-panic” that ended in January 2011.

- Monday’s Financial Times headline indicated that bullish sentiment is rampant with “Record Global Sales of Junk Bonds”.

Stock Markets

Checklist for a Top

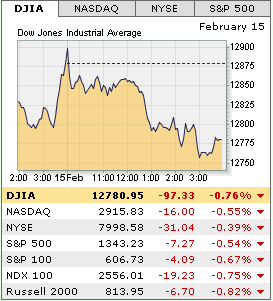

- Is it up when it should be?

Yes.

- Are there signs of enthusiasm?

The AAII ratio of bulls and bears has soared to 74 and the Rydex Bull/Bear ratio is almost at a new record high (chart follows). This confirms Ross’s work on the VIX reviewed in the ChartWorks “Complacency Abounds Oh-Oh!” of January 24th.

- Momentum is also very high as the RSI on the S&P reached 75 – the highest since February 2011.

- The “Sequential Sell” pattern has completed.

- Ross notes that the number of individual stocks registering Upside Exhaustions is soaring, typical of an important top. The gold/silver ratio has been unable to break below 50.

Currencies

- The US dollar is in a pattern that can lead to an outstanding rally. The January 27th ChartWorks “Pulling Back To A Buy Zone” is the latest update.

- A significant rally in the dollar would likely be associated with increasing concerns in the credit markets. Perhaps the season when “fixes” by desperate policymakers seem to be working is ending.

INSTITUTIONAL ADVISORS

WEDNESDAY, FEBRUARY 15, 2012

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The above is part of report that was

published for our subscribers February 9, 2012.

Link to February 10, 2012 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

Gloom Boom Doom Report publisher Marc Faber with his latest thoughts on Greece, China, stocks, U.S. real estate, and some creative ideas for male real estate investors during these troubled times.

“It’s a symptom of a wider problem that we have over-indebted governments in the Western world and Japan, and this is just a small plate, a small appetizer to much larger problems and a much larger crisis,” Faber said about strained Greece negotiations with the EU. Sign-up for my 100% FREE Alerts

As for stocks, generally, the Swiss pony-tailed expat from Thailand believes the rally from the December lows has been too strong to jump on board, yet, especially during the seasonally weak month of February for equities. He also has been watching the weakest sectors of the economy (home builders and banks) for clues to the overall market direction for the coming weeks.

“Basically, what has happened, the market peaked out last May in 2011, then it dropped to 1,074 on October 4th on the S&P. Now we’re up 25 percent,” Faber explained. “The market is very overbought right now, and any excuse for profit taking is now being taken. And I think February is traditionally a weak seasonal month, so we’ll go down first for a while.

“I would just wait a little bit [before buying stocks] because, take for instance the home builders and the banks: the home builders, in some cases, are up 100 percent from the lows, last October [and] November; the banks are up 60 to 70 percent from the December lows. I would just wait here a little bit because, we don’t know how bad the correction will look like—could be 100 points on the S&P, could be 200 points.”

Like Peter Schiff of Euro Pacific Capital, Faber likes high-yielding foreign stocks, especially in the area of the world that which Faber is most knowledgeable and comfortable—Asia.

“Well I bought some shares in November [and] December of last year, and I’m not going to sell them because they are high dividend shares in Asia, and I quite like the Asian markets.”

Faber especially likes “Singapore REITs and real estate related companies in Thailand, because they knocked off the industrial park companies following the flooding of the Thai … some Thai industrial states,” adding, “and some shares in Hong Kong.”

Following the lows in December, globally, stocks have move up in tandem as the so-called ‘risk-on’ trade drew investors off the sidelines back into stocks, as investors anticipated a loosening of monetary policy among the world’s dominate central banks.

Moreover, India, whose currency took a mini-crash last year of approximately 20 percent within a one-month period, has rallied back from its nearly 54 rupee level low against the U.S. dollar at the end of 2011, now trading at the 49 handle, as the risk-on trade flows back more strongly into emerging markets once again.

“Actually, what is interesting, in this rally, since early January, emerging markets have done best,” Faber pointed out. “India is up 14 percent, and the currency has strengthened. So you’re up almost 20 percent, in essentially, a month’s time. So all these markets have become overbought—near term.”

Generally, Faber doesn’t like stocks in the U.S.; he likes the battered down residential real estate market, instead.

“I like real estate in the U.S… Just buy a house,” he chuckled.

In typical Faber style, he went on to share an anecdote from his most recent destination. This time, the vignette takes place in Phoenix, a city among the worst hit by the across-the-board U.S. residential real estate crash.

“I was in Phoenix the other day,” Faber began. “Then, the taxi driver took me to the hotel, nice hotel, Fairmont. And then he told me the person that I just drove before you—I drove him to a five-bedroom house. He told me he just bought it for $120,000. Where in the world can you buy a five-bedroom house for $120,000? I would buy it, live in one bedroom and rent out four bedrooms to concubines.”

But he wouldn’t rent out spare rooms to any foursome of concubines, according to Faber; the concubines must pay rent to him so that the property would throw off cash.

“If you take a very bearish view of the world, then at least—if you own property, you still own it—you pay for cash and get the cash flow as I suggested [from the concubines]. And if you are very bullish about the world, it means the demand for real estate will go up.”

Faber continued, sharing his observation from his earlier stop in Miami. There, Faber said he witnessed the ‘crane index’, firsthand.

“I was three days in Miami. Three years ago, I counted 47 cranes, building highrises,” he said. “This time around, I counted one crane, destroying a building. So, the market has cleared, actually, in Miami.”

Faber noted the frustrations that foreigners across the globe face when seeking overseas bank accounts outside their native countries—which has been a growing trend since the Asian currency of 1997-8, and magnified by the current ruse by many nations disguising capital controls with ‘fighting terrorism’.

“A lot of money has come from Latin America, from Russia because, if you want to open a bank account somewhere, they ask so many questions. But as a foreigner, you can go buy a condo,” Faber said.

Globally, Faber is less concerned with the drama playing out in Greece. His concern focuses upon the only economy primarily responsible for driving global growth (mostly from resources purchases) since the collapse of Lehman Brothers in 2008. That country, of course, is China.

“When we talk about Greece, the major issue for the world economy is China,” he explained. “And China has been slowing down. Industrial production is down; electricity consumption is down; exports were down; and cement production is down; steel production is down. So, many indicators point to a meaningful slowdown in the [world] economy.”

According to Faber, the countries of Australia and Brazil are most vulnerable to a marked decline in Chinese consumption, especially of raw materials—which has recently given rise of talk among some analysts that the Aussie dollar and Brazilian real may be due for a decline due to a China slowdown.

At the end of the interview, the two Fox Business hosts thanked Faber for his appearance and for “the information about the concubines.”

Faber replied, “Yes, yes, yes [about the concubines]. It’s most important; it’s an urgent matter.” Sign-up for my 100% FREE Alerts

The move comes days after Iran’s Oil Minister Rostam Qassemi said Tehran could cut off oil exports to “hostile” European nations as tensions rose over suggestions that military strikes are an increasing possibility if sanctions fail to rein in the Islamic Republic’s nuclear ambitions.

Iran argues that the EU oil embargo will not cripple its economy, claiming that the country already has identified new customers to replace the loss in European sales that account for about 18% of Iran’s exports.

Members of Iran’s parliament have been discussing a draft bill, although not finalised, which would cut off the flow to the European Union before the latest EU sanctions on Iran go into effect this summer.

Iran has said it is forced to manufacture nuclear fuel rods, which provide fuel for reactors, on its own since international sanctions ban it from buying them on foreign markets. In January, Iran said it had produced its first such fuel rod.

Iran’s unchecked pursuit of the nuclear programme scuttled negotiations a year ago but Iranian officials last month proposed a return to the talks with the five permanent UN Security Council members plus Germany.

TSX flat amid rising commodities, Greek assurances that it can get bailout

Obama Proposes Massive Tax Hikes, Still Comes Up With $1.33 Trillion Deficit

President Obama made a pledge to cut the deficit in half by the end of his first term. Instead it exceeded a trillion dollars for four straight years.

Indeed, the president could not even make a pledge made in September to reduce the deficit to $956 billion. Finally, just to keep the deficit at $1.33 Trillion, look at the tax hikes Obama proposes.

Details below summarized from the Bloomberg article Obama Sends $3.8T Budget to Congress

Obama Proposed Tax Hikes

- Expiration of Bush-era tax cuts for couples earning $250,000 or more a year

- Limiting the value of itemized deductions to 28 percent couples earning $250,000 or more a year

- Imposing a minimum tax for individuals with annual incomes of at least $1 million

- Raise taxes on dividends received by the wealthy to 39.6 percent from the current 15 percent

- $61 billion “Financial Responsibility Fee” imposed on banks

- Increase in the terrorism-security fee charged to airline passengers

It takes all that just to hold the deficit to $1.33 Trillion. Chance of passage would appear to be about zero percent.

….read more : Republicans Miss Golden Opportunities on “Hard Choices”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair