Stocks & Equities

Marc Faber, editor and publisher of The Gloom, Boom & Doom Report, said he would not be surprised if Indian markets corrected 20% from current levels, but did not give a timeline for such a correction. In a phone interview from Chiang Mai, Thailand, the Swiss investor expressed concerns over the trade war, and said it is not beneficial to anyone.

Marc Faber, editor and publisher of The Gloom, Boom & Doom Report, said he would not be surprised if Indian markets corrected 20% from current levels, but did not give a timeline for such a correction. In a phone interview from Chiang Mai, Thailand, the Swiss investor expressed concerns over the trade war, and said it is not beneficial to anyone.

What do you think could be the repercussions of global trade war on the world economy and markets?

There is less or hardly any growth in Europe. The Chinese economy has been slowing down, as well as other Asian economies. The US stock market by any measure is highly priced.

We have recessions in Argentina, Brazil and Turkey. We have currency weaknesses around the globe in dollar terms, which is a sign of monetary tightening, and now we have also this so-called trade war. Some people may suffer more, and some less but a trade war cannot be beneficial for anyone. In general, it is not a positive for the global economy or the financial markets.

Indian markets recorded new high today (Thursday). Do you think the rally in India is sustainable or do you think there is a correction in the offing for benchmark equity indices?

When (Indian) market hit a high earlier this year in January, my sense was that high would be an important one, but we made a new high.

Let’s put it this way, when I travel around the world and I visit financial institutions, first time India is really a subject. For the first time, investors think that India has an experience and a meaningful fundamental improvement due to the Modi government. They are not sure if it is the right time to invest now in India. Over the next 10 years, we want to have some money in India, regardless.

If you look at the S&P (500), and Indian stock market over the next 10 years, you will make more money in India than American shares. This has been my view for the last three years, and this remains my view.

Of course, if the global stock markets are going down— all the major markets, except India are going down. When everything is weak, and India is still strong, I will be reluctant to buy the market which is strong. It (rally) may last a little bit longer but it doesn’t mean it is good value. Valuations are not attractive other than a few exceptions.

The bull market in India started in late 2015, We have seen a big move, I wouldn’t be surprised if there is a 20% correction. I cannot give you a date though.

If you put all your money now in Indian stocks, the reward in my opinion will not be great, as there are internal and external risks.

It’s time for our annual August report, “Charts for the beach.” Each year we highlight five of our favorite charts we think consensus is currently overlooking. Remember to ask your RBA representative for your official RBA eyeglass cleaning cloth to keep your sunglasses spotless!

Profits (not GDP or politics) drive the stock market.

At RBA, we approach the current environment by staying disciplined, slowing down the investment process, and by staying dispassionate with respect to politics.

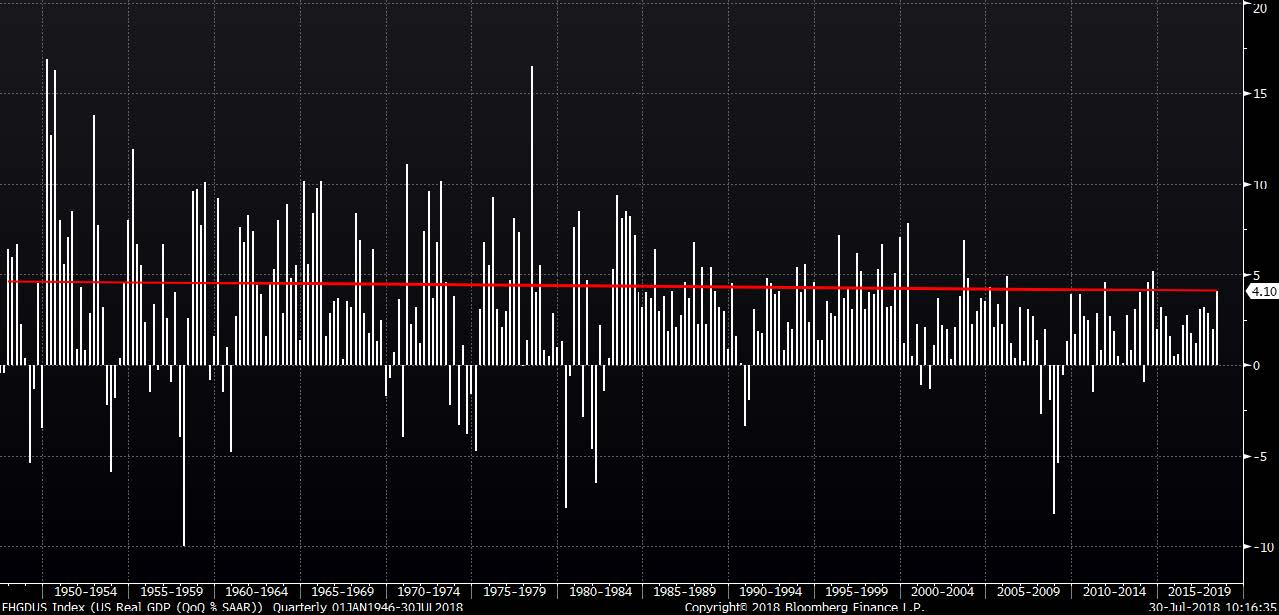

Along those lines, our first two charts show US real GDP and corporate profits through time. There has been considerable hoopla about the strength of GDP growth during the second quarter, but US real GDP growth remains within a slow-growth band that has existed since the bursting of the Technology bubble in 2000 (See Chart 1).

CHART 1:

US Real GDP

(QoQ % Jan. 1946 – Jul. 2018)

Source: Bloomberg Finance L.P.

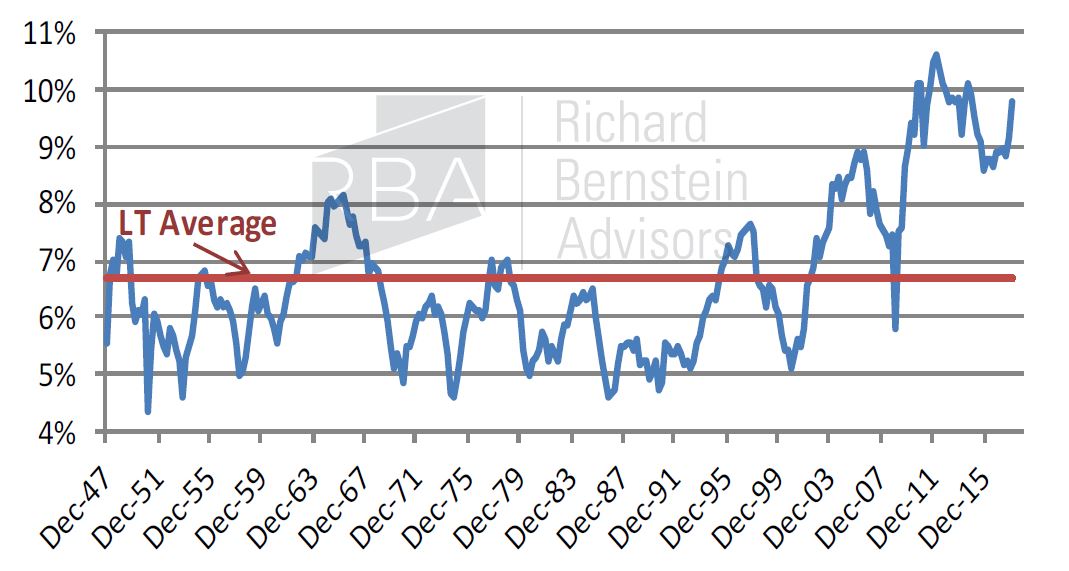

Chart 2 helps explain why the US bull market has been so powerful despite continued anemic GDP growth by highlighting corporate profits as a percent of GDP. The corporate sector’s proportion of national income rose to all-time highs post-2010. This ratio has smartly rebounded, which has fueled the more recent leg of the bull market.

Contrary to popular belief, the corporate sector (upon which the stock market ultimately focuses) has been historically healthy relative to the overall economy. The combination of tremendous liquidity provided by the Federal Reserve and an historically healthy corporate sector seems to justify both the length and magnitude of the 9-year bull market.

CHART 2

US Corporate Profits as a Percentage of GDP

(4Q 1947 – 1Q 2018)

Source: Richard Bernstein Advisors LLC, BEA, Bloomberg Finance L.P.

We prefer fixed liabilities, not fixed income, during inflationary periods.

Data demonstrate that investors continue to focus on disinflationary asset classes and have yet to re-orient portfolios toward assets that outperform during periods of accelerating inflation. Unfortunately, inflation expectations troughed more than two years ago, and asset classes that benefit from accelerating nominal growth (stocks and commodities) have appreciated significantly whereas broad fixed- income has provided negative total return.

Chart 3 compares the returns of stocks, commodities, and various popular fixed-income benchmarks since July 2016. The ongoing popularity of income-oriented investments shows investors have yet to understand the implications of higher potential inflation.

Household and corporate balance sheets constructed with general combinations of fixed asset values and floating liabilities tend to outperform during periods of disinflation/deflation. However, a combination of floating assets and fixed liabilities has proven more beneficial during periods of inflation. FIXED-income is unlikely to be a successful core holding if we are correct and inflation continues to be higher than investors expect. Inflation is the kryptonite of income.

CHART 3

Stocks, Commodities and Fixed Income

(Total Returns Jul. 2016 – Jul. 2018

Source: Bloomberg Finance L.P. For Index descriptors, see “Index Descriptions” at end of document

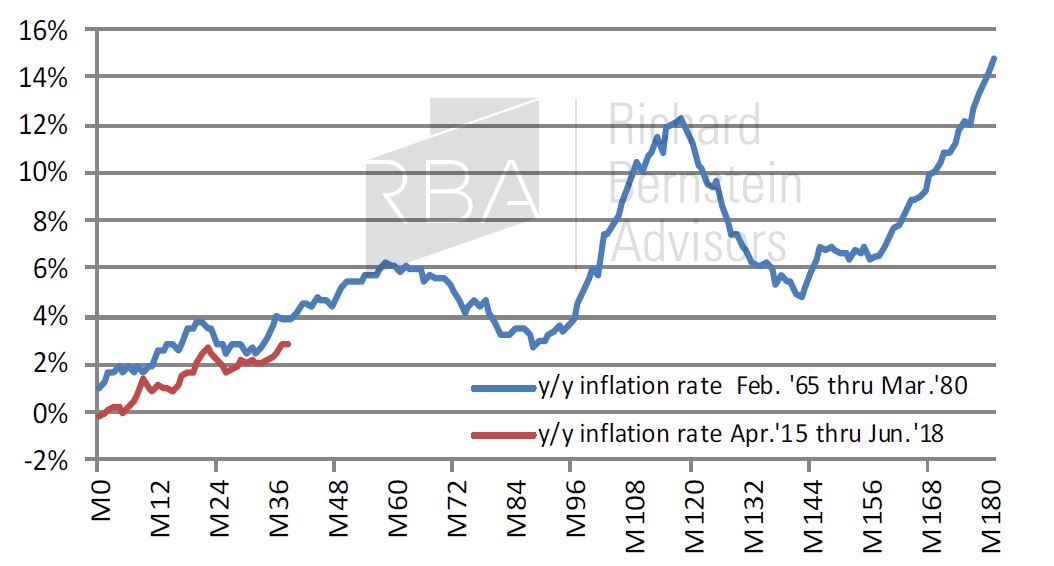

Secular inflation?

We’re not wild about these types of charts, but Chart 4 compares the current cycle’s inflation with the secular period of inflation from the 60s and 70s. We are not showing this chart to suggest that inflation will follow a definitive pattern. Rather, we show it to demonstrate how benignly one of the worst inflationary periods in US history started. That might be worth considering simply because investors remain quite sanguine about inflation given the economic and policy backdrop. (http://www.rbadvisors.com/images/pdfs/ Overheating_Ahead.pdf).

CHART 4

Secular Inflation:

Feb. 1965 thru Mar. 1980 vs. Current

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

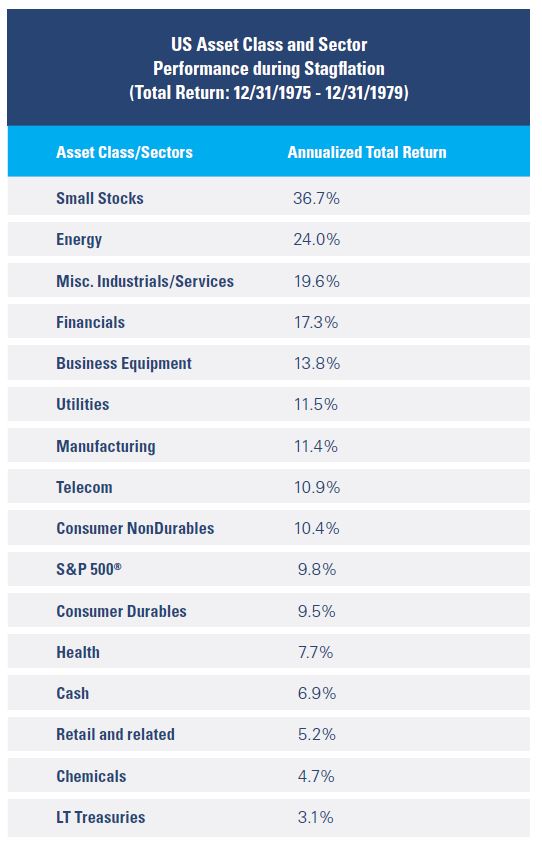

Quick history lesson

RBA believes that there could be considerably more inflation than investors currently expect, but we do not believe there will be secular stagflation. Nonetheless, it is a good history lesson to review what asset classes and sectors outperformed during the stagflation of the late-1970s (see Table 1 on the following page).

TABLE 1

Source: Richard Bernstein Advisors LLC, Kenneth R. French, Morningstar Ibbotson SBBI

To learn more about RBA’s disciplined approach to macro investing, please contact your local RBA representative. www.rbadvisors.com/images/pdfs/Portfolio_Specialist_Map.pdf.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Commodities: S&P GSCI® Index: The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

Bloomberg Barclays US Aggregate Bond Index: The Bloomberg Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government- related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

Bloomberg Barclays EM USD Aggregate Total Return Index: The Bloomberg Barclays Emerging Markets Hard Currency Aggregate Index is a hard currency Emerging Markets debt benchmark that includes USD-denominated debt from sovereign, quasi-sovereign, and corporate EM issuers.

Bloomberg Barclays US Floating Rate Notes Total Return Index Value Unhedged USD: The Bloomberg Barclays Capital US Floating Rate Notes Total Return Index Value Unhedged USD measures the performance of USD denominated, investment-grade, floating-rate notes across corporate and government-related sectors.

LT Treasury: Long-term Treasuries are represented by the Morningstar Ibbotson Long-Term Government Bonds Index Series which is composed to the greatest extent possible of a one bond portfolio with a term of approximately 20 years and a reasonably current coupon was used each year.

Small Stocks: Small Stocks are represented by the Morningstar Ibbotson Small Company Stocks Index Series which is composed of stocks making up the fifth quintile of the NYSE by market capitalization.

Cash: Cash is represented by the Morningstar Ibbotson US Treasury Bills Index Series which is composed of a one bill portfolio rebalanced monthly to the shortest-term bill having not less than one-month to maturity.

Sectors represented by the Fama French 12 Industry Series as described below.

Consumer Non Durables: Fama French NoDur: Consumer NonDurables—Food, Tobacco, Textiles, Apparel, Leather, Toys

Consumer Durables: Fama French Durbl: Consumer Durables—Cars, TV’s, Furniture, Household Appliances

Manufacturing: Fama French Manuf: Manufacturing—Machinery, Trucks, Planes, Off Furn, Paper, Com Printing

Energy: Fama French Enrgy: Oil, Gas, and Coal Extraction and Products

Chemicals: Fama French Chems: Chemicals and Allied Products

Business Equipment: Fama French BusEq: Business Equipment—Computers, Software, and Electronic Equipment

Telecom: Fama French Telcm: Telephone and Television Transmission

Utilities: Fama French Utils: Utilities

Retail and related: Fama French Shops: Wholesale, Retail, and Some Services (Laundries, Repair Shops)

Health: Fama French Hlth: Healthcare, Medical Equipment, and Drugs

Financials: Fama French Money: Finance

Misc. Industrials/Services: Fama French Other: Other —Mines, Constr, BldMt, Trans, Hotels, Bus Serv, Entertainment

© Copyright 2018 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

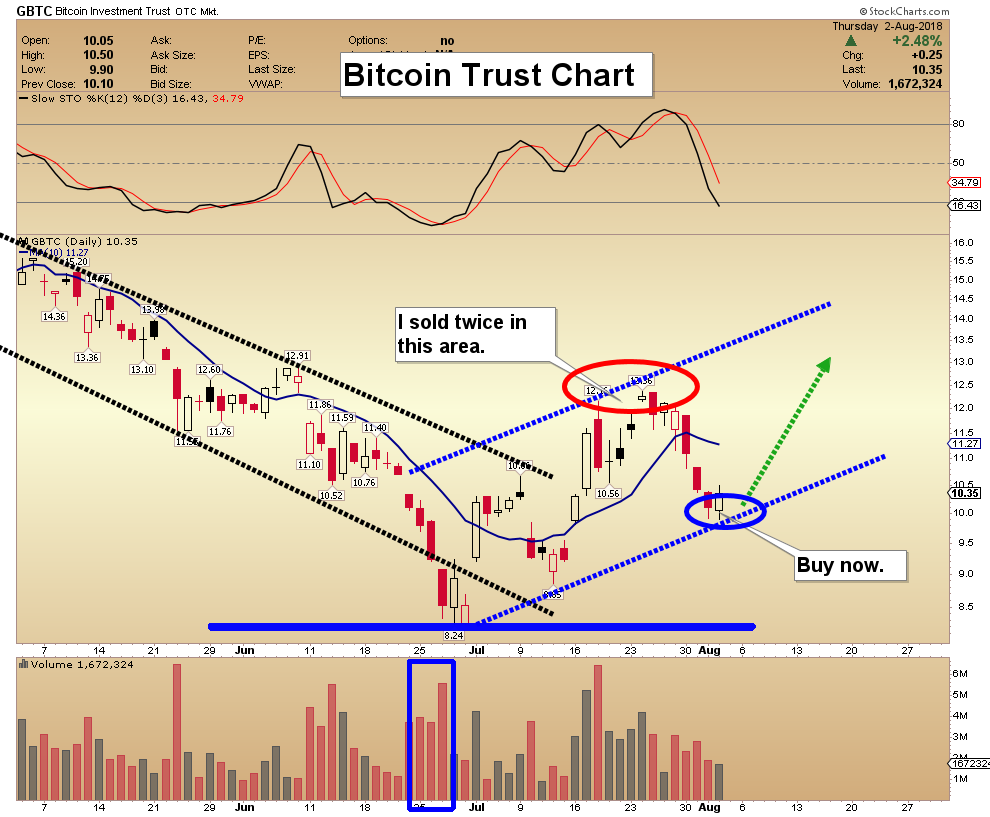

Today’s videos and charts (double click to enlarge):

SFS Key Charts & Portfolio Analysis

SF Juniors Key Charts & Video Analysis

{kind=link}

SF Trader Time Key Charts & Video Analysis

{kind=link}

{kind=link}

Morris

| Friday, Aug 3rd 2018 Super Force Signals Unique Introduction For 321Gold Readers: Send an email to trading@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you! |

Today, Apple became the first American company valued at $1 trillion, following its strong third-quarter earnings report. Despite the rise of tough competition, Apple has remained steadfast in its focus on loyal users. This news reveals a stable company that not only encompasses a strong yearly growth rate of 5-10 percent, but also returns a majority of profit to shareholders…. CLICK for the complete article

Warren Buffett’s favorite indicator is telling us that stocks are more overvalued right now than they have ever been before in American history.

That doesn’t mean that a stock market crash is imminent. In fact, this indicator has been in the “danger zone” for quite some time. But what it does tell us is that stock valuations are more bloated…. CLICK for the complete article

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair