Timing & trends

Rio Tinto has employed the first fully autonomous train, which many are calling the world’s largest robot. Rio Tinto’s project has eliminated humans and that saves on pensions and salaries. This is the way of the future because of exponentially rising human costs. The train completed its first delivery of iron ore between the company’s Australian Mount Tom Price mine and the port of Cape Lambert on the Western coast.

Rio Tinto spent $940 million to develop this project. The train consists of three locomotives and carries around 28,000 tonnes of iron ore making a journey of 280km with no human driver. The trip was monitored remotely by operators at Rio’s Operations Centre in Perth more than 1,500km away. Effectively, this is not so dissimilar from the drone used in the military that is also being monitored from a far away location.

The high cost of socialism is driving the field of robotics. The higher the costs of pensions and their lack of feasibility when central banks play with interest rates pretending to be managing the economy has driven the technology into the hands of automation. Governments are in a state of denial and they will continue to raise taxes to try to cover their costs. They fail to look at this crisis straight in the eyes. There is no hope of maintaining socialism and more than there was communism.

…also from Martin: Why CONFIDENCE is the Backbone of the New Monetary System

and

Violence from the Left is Starting – It will be Their Way or No Way

Man, I love catching a big move early. And there’s a metal that is just making a turn out of a long, brutal bear market right now.

It’s not gold. It’s not platinum. Nope, this metal glows in the dark.

It is still moving slowly, like a giant rousing from a deep slumber. Investors who hop aboard this giant now stand to make humongous profits.

I’m talking about uranium.

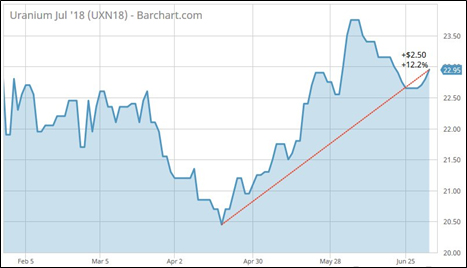

Uranium has rallied more than 12% from a low it hit in April. You might remember that was when I started pounding the table about this white-hot energy metal.

Recently, uranium was at $22.95 per pound, as you can see from this chart …

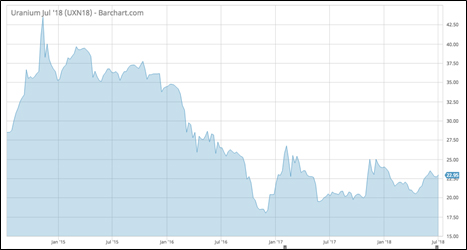

Is that the end of this rally? Heck, no! As this longer-term chart shows, uranium can get a lot more expensive, and in a hurry, too.

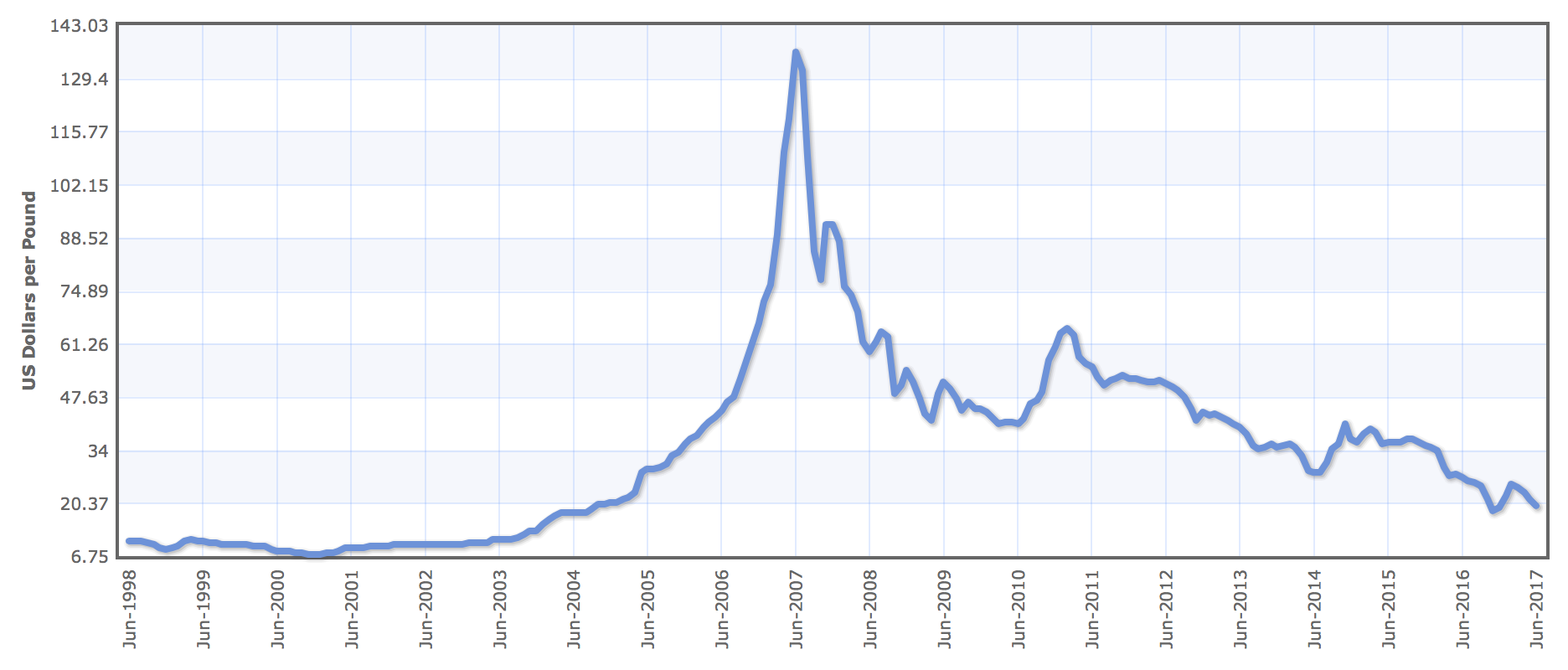

I expect uranium could rise to $40 a pound in a hurry. And from there, well … this sizzling metal did soar to over $140 a pound in the last bull market.

BLAM! Did that get your attention? And why is uranium so cheap, anyway?

Well, commodities are cyclical. The last great uranium bull market ended in 2008. I should know. I made my subscribers a heck of a lot of money in that magnificent bull run.

But as often happens, if a mineral stays high enough, long enough, new mines come online.

Still, uranium prices were pretty good. That is, until 2011, when an earthquake and tsunami in Fukushima, Japan, sent three reactors into meltdown. That pushed uranium off a cliff. For a very long time.

The real crush came in the past few years. The price was cut in half, and the spot price of uranium hit a 13-year low of $18.60 in 2016. It bounced … a little … but kept scraping bottom.

The price of uranium went up 17% in 2017. That’s the first time the needle moved in years.

That’s only the third time uranium prices have gone higher in the past decade.

And this year? This year, the uranium market is looking to be really hot. White-hot!

Why is that? Well, there’s the fact that one miner after another has shut down production because it’s literally cheaper to buy uranium on the spot market than it is to mine it.

That’s a huge disconnect. It was only made possible because Japan’s idled reactors were selling their fuel reserves into the market. Now, Japan is turning reactors back on. It recently restarted its eighth reactor and is looking at bringing a bunch more back online.

That’s a major shift in the fundamentals.

But let’s look at the global picture. Now, there are 450 reactors in operation. Another 57 are under construction. Most of them are in Asia. Another 154 are on order or planned, and a further 284 proposed.

You need about 200 metric tons of uranium to run a typical 1,000-megawatt (MW) reactor for a year, and about twice that to start one up.

Globally, there are about 395,000 MWs of nuclear power installed. That means we need around 79 million metric tons a year of uranium.

The supply from mines, currently, is straining to meet this. About 65 million tons of uranium was mined in 2017. The rest is met from stockpiles.

But then there are all those new reactors I mentioned. The new reactors that are under construction will produce another 62,000 MWs of power. And that will require 12.4 million more metric tons of uranium per year.

And if we add in all the nuclear power plants on order or planned — that’s another 31.6 million metric tons of uranium required every year.

To be sure, nuclear power plants can’t run forever. And bears will point out that the U.S. has an aging nuclear fleet, and isn’t planning to build many more.

Yet.

But I’ll counter that with the fact that operating licenses for those old plants keep getting extended. That’s because nuclear power is cheap. Very cheap. And it’s needed as a backup for the next generation of sun and wind power, and more.

Now let’s add in the fact that there is a very tiny universe of only about 40 uranium producers, developers, and explorers. More will grab picks and shovels, sure. But right now, it’s like shooting fish in a barrel.

The white-shoe crowd on Wall Street is sleep-walking as the uranium giant rises from its slumber. The stampeded will begin soon enough.

If you’re doing it on your own, please be careful, and do your own due diligence. But don’t miss this extraordinary rally to come.

All the best

Sean

Masayoshi Son, the Korean-Japanese, University of California, Berkeley-educated founder of one of Japan’s most successful companies, SoftBank Group:

Masayoshi Son, the Korean-Japanese, University of California, Berkeley-educated founder of one of Japan’s most successful companies, SoftBank Group:

Like Buffett, Son is a tremendous capital allocator with a highly impressive record: Over the past nine and a half years, SoftBank’s investments have delivered a 45% annualized rate of return. A big chunk of this success can be attributed to one stock: Chinese e-commerce giant Alibaba, a $100 million investment SoftBank made in 2001 that is worth about $80 billion today.

Though you may put Alibaba in the (positive) black swan column, Son’s success as an investor goes well beyond it – the list of his investments that have brought multi-bagger returns is long. The 57-year-old Son is Japan’s richest person, and SoftBank, which he started in 1981 and owns 19% of, has a market capitalization of $72 billion.

Like Apple co-founder Jobs, Son is blessed with clairvoyance. He saw the internet as a transformative force well before that fact became common knowledge. In 1995 he invested in a then-tiny company, Yahoo!, earning six times his investment. But he didn’t stop there; he created a joint venture with Yahoo! by forming Yahoo! Japan, putting about $70 million into a company that today is worth around $8 billion. (Yahoo! Japan is a publicly traded company listed in Japan.)

What is shocking is that Son saw that the iPhone would revolutionize the telecom industry before Apple announced it or even invented it. See for yourself in this excerpt from an interview with Charlie Rose, where Son describes his conversation with Jobs in 2005 – two years before the iPhone was introduced:

I brought my little drawing of [an] iPod with mobile capabilities. I gave [Jobs] my drawing, and Steve says, “Masa, you don’t give me your drawing. I have my own.” I said, “Well, I don’t need to give you my dirty paper, but once you have your product, give me for Japan.” He said, “Well, Masa, you are crazy. We have not talked to anybody, but you came to see me as the first guy. I give to you.

Like Virgin Group founder Branson, who created Virgin Atlantic Airways in the U.K. to compete against the state-owned behemoth British Airways, Son started two telecom businesses in Japan – one fixed-line and one wireless – with which he challenged the state-owned NTT monopoly. In 2001, disgusted with Japan’s horrible broadband speeds, he convinced the government to deregulate the telecom industry. When no other companies emerged to rival NTT, Son took it upon himself to start a fixed-line competitor, Yahoo! BB (broadband). Thanks to him, now Japan enjoys one of the highest broadband speeds in the world and Yahoo! BB is a leading fixed-line telecom.

It took Son four years to bring his broadband business to profitability. This is how the Wall Street Journal described that period in 2012: “The problems at the broadband unit contributed to losses for the entire company for four consecutive years. Mr. Son set up an office in a meeting room 13 floors below his executive suite to be closer to the problem unit. He slept in the office at times and routinely summoned executives and partners for meetings late at night. . . . He worked out of the meeting room for 18 months, until the broadband unit had cut enough costs and moved enough customers to more lucrative plans.”

A normal person might have taken a break and enjoyed the fruits of his labor at that point, but not Son. Just as his broadband business went into the black, Son executed on his vision for the internet and bought Vodafone K.K., a struggling, poorly run wireless telecom in Japan. SoftBank paid about $15 billion, borrowing $10 billion.

Fast-forward eight years, and SoftBank Mobile is a success. It is one of the largest mobile companies in Japan, even faster-growing than DoCoMo (a subsidiary of almighty NTT). Today it spits out about $5 billion in operating profits annually – not bad for a $5 billion equity investment.

Son has a highly ambitious goal for SoftBank: He wants it to become one of the largest companies in the world. Unlike the average Wall Street CEO, whose time horizon has shrunk to quarters, Son thinks in centuries: He has a 300-year vision for SoftBank. Practically speaking, 300 years is a bit challenging even for long-term investors, but at the core of his vision Son is building a company that he wants to last forever (or 300 years, whichever comes first).

Son views SoftBank as an internet company and is committed to investing in internet companies in China and India. He believes that as these countries develop, their GDPs will eclipse those of the U.S. and Europe.

Jobs, Branson, Buffett – it is rare for somebody to embody strengths of each of these business giants. None of them has the qualities of the other two. Buffett is a business builder but does not run the companies in his portfolio. Branson is not a visionary – in his book Losing My Virginity he admits to not seeing analog music (CDs) being destroyed by digital music (iTunes) and demolishing his music store business. Jobs probably came the closest, as both a visionary and a business builder, but he was not known for his investing acumen.

Valuation (updated)

You’d think SoftBank would be priced to reflect Son’s premium. Instead, its stock currently trades at around a 50% discount to the fair value of its known assets (SoftBank has about 1,300 investments, many of them not consolidated on its financials).

The gap between what SoftBank is worth (its fair value) and its stock price has widened substantially over the last few years despite the stock’s appreciation. Our fair-value estimate of SoftBank shares is about $80.

Frustrated with SoftBank’s valuation, Son has begun to make strategic moves to de-lever SoftBank. Last February, SoftBank announced it may take its Japanese telecom business public. SoftBank is expected to sell about 30% of its stake and should raise about $20 billion.

SoftBank owns a large chuck of Didi, the largest Chinese ride-hailing company, a Chinese version of Uber, which in fact bought Uber’s assets in China. Didi is a privately held company.

Recently SoftBank announced that it is going to sell its shares of Didi to Vision Fund for $20 billion. Vision Fund is a $100-billion private equity-like investment vehicle created by Son. SoftBank owns one-third of Vision fund and has an even larger economic interest in it.

And then there is Sprint – SoftBank owns 82% of its publicly listed shares. After dating T-Mobile for almost a year, Sprint and T-Mobile finally decided to merge. There is a chance that the government might not approve this merger, but we think the probability of approval is high. The telecom industry requires scale: the cost of a network (cell towers, equipment, and spectrum) is mostly fixed, and profitability of a carrier is for the most part determined by the number of users.

T-Mobile and Sprint are each half the size of giant incumbents Verizon Communications and AT&T, which achieved their size through dozens of acquisitions. The combination of Sprint and T-Mobile would reduce competition in the short run, but in the long run it would create a strong and viable competitor and thus stable prices for consumers. T-Mobile and (especially) Sprint on their own would eventually get marginalized into irrelevance by AT&T and Verizon by the large cost of 5G rollout.

If the merger goes through it would improve the optics of SoftBank’s balance sheet. SoftBank owns 82% of Sprint and thus has to consolidate Sprint’s $30 billion of debt on its balance sheet. Despite SoftBank’s control of Sprint, in the event of bankruptcy SoftBank is not liable for Sprint’s debt. After the merger SoftBank will own around 27% of the combined entity and thus, magically, the debt of the new company will migrate from SoftBank’s balance sheet to the balance sheet of Deutsche Telecom – the majority owner of T-Mobile.

Between the sale of Didi, the Japanese telecom IPO, and the Sprint/T-Mobile merger, SoftBank should see its debt drop by about $70 billion. The current discount between the fair value of SoftBank’s assets and its stock price is caused by the perception of enormous leverage, and as the leverage gets cured so will the perception.

Conclusion

There are many ways to look at SoftBank. You can think of it as buying a stock at a roughly 50% discount to the market value of its assets or as a way to buy Alibaba at less than half its current price. Alibaba is a great play on the Chinese consumer who is spending more and more money shopping online. Alibaba is synonymous with Chinese online shopping, whose growth may accelerate with higher smartphone penetration and, just as important, the ongoing rollout of a fast wireless LTE network.

You can also look at SoftBank as a vehicle through which to invest in emerging markets – not just China but India as well. It is almost like hiring the combination of Buffett, Branson and Jobs to go to work for you investing in markets whose economies in a few decades will surpass that of the U.S., while also investing in a segment of the economy – the internet – that is growing at a much faster rate than the overall economy. And, of course, you have Masayoshi Son, the Buffett-Branson-Jobs fusion, making these investments for you. With SoftBank at this valuation, you can ditch your emerging-markets mutual fund.

Additional thoughts

I don’t expect every bet Mr. Son makes in Vision Fund to work out. Not at all. I look at Vision Fund as a portfolio of bets. For instance, his investment in WeWork and WeWork’s valuation make me cringe. I am also concerned that he feels the need to spend $100 billion all at once. There will be a time when this money will buy a lot more than it does today.

I feel uneasy that the $100 billion will be like a pig going through the python of Silicon Valley, inflating the prices of technology companies. But a few things let me sleep well owning Softbank: First, Mr. Son owns 20% of the company – every dollar Softbank spends, 20 cents are his. As Nassim Taleb would put it, Mr. Son has skin in the game. Second, the discount of Softbank stock to the fair value of its assets is so huge that it could absorb the blow-up of Vision Fund. And finally, I remind myself that I’d probably have had a similar feeling of uneasiness about Mr. Son’s decisions at any time in his 30-plus-year career (PCs in the ’80s, Internet in the ’90s, telecom Japan and internet in China in the ’00s). And this is when I remember Einstein’s quotes.

U.S. equity futures are flat, alongside European and Asian stocks as global markets recovered some ground on Tuesday after oil prices stabilized and as trade war fears subsided with attention still squarely focused on Trump’s Putin summit, even as global tech stocks, Nasdaq futs and FAANGs – or is that FAAGs now – felt the pressure from yesterday’s NFLX earnings bomb…. CLICK for the complete article

Sales of electric vehicles (EVs) and plug-in hybrids in Europe’s top car markets rose by just 33 percent in the first half this year, compared to a 54-percent surge in the same period last year, as customers are still wary of limited driving ranges of the models and an insufficient…..CLICK for the complete article

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair