Energy & Commodities

There is a huge problem in the Copper Market. Despite strong demand growth from electric cars and battery production about 40% of the world’s current copper production will close over the next 10 to 20 years. In other words demand is going up while supply is scheduled to shrink. Check out The world’s top 10 highest-grade copper mines for investment opportunities after reading this analysis – R. Zurrer for Money Talks

The next big commodity story isn’t some exotic metal like cobalt or palladium…

It’s much more simple and important. The next boom in natural resources is copper.

Copper demand is soaring. You know the story. Electric cars, municipal-scale batteries and millions of other electronics out there. They all need copper.

While we know the story, the numbers are incredible. The price of copper is up 44% in the last two years.

If you don’t have a position in copper mining, you should buy right now.

A Huge Problem for the Copper Market

Monthly demand for copper rose 82% since January 2000, as you can see from the chart below:

As you can see, the trend works out to about 3.4% annual growth in copper demand. That’s setting up a huge problem for the copper market in the next 10 years.

According to a mining analyst with CRU, around 220 mines — about 40% of the world’s current copper production — will close over the next 10 to 20 years. In addition, mines that continue to produce will do so with lower grades — less metal per ton of rock moved.

Mines can only produce so much material in a year. If the rock has less copper, then the supply will fall. That’s happening at BHP Billiton and Rio Tinto’s giant Escondida mine. After a $7.6 billion upgrade in 2015, the output fell by 200,000 metric tons per year.

The average mined grade fell from 1.4% per ton in 1990 to under 1% today. That works out to a decline of 8 pounds of copper per ton of ore.

In other words, demand is going up, and supply is struggling to keep up. They will diverge soon. While demand growth is 3.4% per year, supply growth will struggle to hit 1% per year.

By 2028, the market will be 15 million metric tons short. Mining analysts at CRU forecast a 25% increase in demand by 2025. That’s 1.1 million metric tons more than we used in 2017.

This Natural Resource Bull Market Is Rolling

The best analog to this situation was the period from 2000 to 2015. During that time, the three-year average price of copper rose 400% from $0.74 per pound to over $3.70 per pound in 2013. The projected demand growth will send copper prices soaring higher over the next 10 to 15 years.

While some substitution will occur (we can substitute metals like aluminum in place of copper in some cases), the price escalation is coming.

Real Wealth Strategist readers are prepared. We own a suite of high-quality copper miners, and we will be adding new names to that list over the next year. If you haven’t done the same, you absolutely should start now.

The bull market is rolling, and you can profit from it today.

Good investing,

Matt Badiali

Editor, Real Wealth Strategist

One of the most common investing mistakes people make is in their trade allocations. This is especially true when they are going for home run type trades. Instead of investing a small amount and trying to turn it into a large amount, many investors invest a large amount, and it ends up turning into a small amount.

One of the most common investing mistakes people make is in their trade allocations. This is especially true when they are going for home run type trades. Instead of investing a small amount and trying to turn it into a large amount, many investors invest a large amount, and it ends up turning into a small amount.

Just last week I got a call from an old high school friend named Brian. He was asking me about a penny stock that was rumored to be a takeover target.

He was talking about putting half of his trading account into this trade. I told him I would never put half of my account in one trade. I also told him I would look at it for him.

After I looked at the company and analyzed the trade, I told him that I personally wouldn’t make the trade in my own account. Brian said: “If you wouldn’t make the trade, I won’t make the trade.”

A few days after that conversation, I was talking with Paul Mampilly. We were talking about trade allocations, and how many hedge funds take small allocations and have them turn into a large part of the portfolio. On the other hand, many individual investors, like my friend Brian, take a large allocation and let it become a small part of the portfolio.

Which would you rather do: Take a big investment and have it become small, or take a small investment and have it become big?

Small Investments Can Make a Huge Difference

The obvious answer to the question above is the first option. No one wants one of their large investments to become a small one.

I can show you how an allocation of as little as 2% can still have a big impact on the total return of a portfolio. But you have to have patience and discipline. You also have to be willing to take some total losses if you are going to have really big winners.

I am not just talking about 100% and 200% winners. I am talking about investments that go up 10, 12, 15-fold and more.

To show you how this can work, I put together the following table. The table shows how you can take 2% allocations from a $50,000 portfolio and make a great return. You can even have three 100% losses and two 50% losses, and still enjoy great overall returns.

In this scenario, we made 10 trades and allocated only 2% to each one. Three of the trades were total failures, 100% losses. Two trades were 50% losses, and two were breakeven trades. There is one 100% winner, one 500% winner and one 1,500% winner.

After all is said and done, the portfolio gained 36% with only three winning trades out of 10.

We also only used 20% of the total portfolio value to make these trades. We could repeat this same pattern four more times.

By making small allocations, we limit the downside. But there is unlimited upside.

You may be saying: “1,500% gains don’t happen very often.” And you would be right, they don’t. You have to be patient and disciplined.

As an example, let’s look at a stock that Paul and I have both traded and recommended over the past seven years or so, the Federal National Mortgage Association (OTC: FNMA). It is better known as Fannie Mae.

The stock was languishing between 20 cents and 41 cents for over a year back in 2012 and early 2013. But after the company reported $50 billion in profits in March 2013, the stock jumped sharply higher.

If you had bought in the middle of the range at 30 cents, you would have gained over 1,700%. If you bought at the low end of the range, you gained over 2,600%.

However, you would have had to have the patience to wait through the range period, and you would have had to have the discipline to see the stock jump to its peak.

Too many investors want home run trades, but don’t have the patience and discipline to actually achieve them. They get tired of waiting, or they see the stock jump by 100% or 200% and sell it before it has had the chance for the big move.

If this trade would have been in the sample portfolio above, a 2% allocation would now be worth approximately 25% of the portfolio. That is using the 1,700% gain to replace the 1,500% gain above.

Triple-Digit Gains

Gains of 100% or 200% are pretty easy to get, quite honestly.

I used to write a newsletter for penny stock investors. All of the stocks had to be under $10 and listed on an exchange. Those were the only two requirements the publisher gave me.

I looked back at the track record recently, and there were so many 200% to 300% winners.

There was one 15-trade stretch where six of the recommendations reached at least 200% gains, three of the six reached 300% and two of them were close to 400%.

However, I doubt if any subscribers actually achieved those gains.

Why? Because they weren’t willing to wait for them. I doubt they had the patience or discipline to wait.

A New Service for a New Approach: The $10 Million Portfolio

Now that I have told you about this downside-up approach to investing, I want to tell you about a new service that Paul and I are running. It isn’t fully launched yet, but it will be soon.

We are going to use our combined talents and experience to run the service, and we are going to use the methodology described above to help guide investors. We are going to suggest small allocations to aggressive trades that will take patience and discipline. But we expect the rewards to be huge.

The service is called The $10 Million Portfolio. We call it that because our goal is to help subscribers grow their portfolios from $10,000 to $10 million.

And hopefully we can change the way investors think when it comes to home run trades. We want to teach investors how to take small allocations and turn them into large portions of their portfolios.

Perhaps having two guys with over 50 years of combined investment experience will help change the way investors think.

We are all looking forward to the launch, and we can’t wait to help readers make money. But we all have to be patient.

Regards,

Rick Pendergraft

Senior Analyst, Banyan Hill Publishing

According to the Game Plan for Late-Cycle Investing, as the economy moves towards its latter stages, commodities tend to outperform equities and other asset classes. Frank Barbera—market technician & portfolio manager believes we’re likely in that process right now & if Gold pushes through $1,365 the first push up will take it to $1,480 to $1,525 – R. Zurrer for Money Talks

Listen to this podcast on our site by clicking here or subscribe on iTunes here.

Volatility Is a Return to Normal

Stock market volatility has picked up this year, though in percentage terms this really just a return to historical norms, Barbera explained.

The real anomaly occurred over the last 2 years where the market was moving straight up in parabolic fashion before culminating in a blow-off top late-January.

“Think of this more as a return to normal than anything else,” Barbera said. “Comparatively speaking, it is a rise in volatility, but at least so far we really haven’t seen the stock market averages breakdown below major key levels.”

Possible Topping Process

One disquieting point is that after the big break we saw in early February, we swung from very high momentum to deep oversold conditions without anything in between, Barbera noted.

“We had this abrupt break in the market,” he said. “That’s very historically unusual. Usually, when you have high momentum, you’ll get a pullback, getting a push to new highs or maybe two pushes to new highs before you get a decent-sized break, and this just flipped on a dime.”

Larger Chart – Source: Bloomberg, Financial Sense Wealth Management

This is consistent with a parabolic move, and it can sometimes mean that we’ve seen the final peak. Even if that were the case, however, Barbera believes we’ll likely see an approach or retest of the highs before the market definitively turns down.

“For the time being, I would give the stock market the bullish benefit of the doubt, but I don’t think we’re going to see another runaway advance on the upside,” Barbera said. “I think what you’re seeing here is the market moving into a distribution top. There is some potential for a double top … but the real message is it’s getting very late in the cycle.”

Gold and Bonds May Shine

Barbera thinks we’re likely in the process of a late-cycle run in commodities.

If the economy turns down, this does pose a risk for most industrial commodities, but we’re not quite there yet, he said. Bonds, on the other hand, especially Treasuries and high-grade corporates, appear to be making a base. Now might be a good time to follow traditional risk-off bonds, high-grade corporates and some of those funds that can do really well in a down cycle.

Gold recently attacked the $1,365 area, which has been key resistance, while $1,305 to $1,310 has been key support. If we go through $1,365, gold may target $1,480 to $1,525 on the first push up, Barbera believes.

For more information about Financial Sense® Wealth Management and our current investment strategies, click here. For a free trial to our FS Insider podcast, click here.

In this very detailed proposal Michael Ballanger outlines what he thinks is a superb shorting opportunity. He provides the rationale, and the specific size and nature of the trade using ETF’s. In one scenario he expects a return on investment of 50.35%, another scenario yields 1.08% – R. Zurrer for Money Talks

Precious metals expert Michael Ballanger discusses the gold and silver ratio.

There is a famous quote about short-selling that comes from Olde English business folklore that goes something like this:

“He who sells what isn’t his’n.

Must deliver or goes to prison!”

That old horse chestnut was used to frighten the Rothchildian short-sellers that used to hang out on the old New York “curb” back before governments and influence- peddling lobbyists conspired to change the rules. I used to love to find overvalued stocks or commodities and get our trading desk to call over to the loan post to see what it would cost to borrow a few thousand shares of some pumped up bowser of a stock and then attempt to catch it on an uptick in order to sell it. The entire concept was rather civilized because everyone would know that there was a highly visible bear out there trying to get short something and invariably, the principals like the CEO or CFO would find out and then the ancient game of cat-and-mouse would begin.

It would begin with the phone calls from someone at the target company introducing themselves and asking you out for coffee or a beer if you were borrowing a puny 2,000 shares with the venue morphing decidedly if the number was north of 100,000 shares. (If it was a MILLION, it was a weekend in Vegas.) I would put on my most gracious persona as the rep from the overvalued company tried in vain to change my intention of hammering his pig of a stock into the ground, but what made it a study in human behavior was that the higher the gratuity, the more maniacally I wanted to sell the stock.

Needless to say, short-selling is not the fun it used to be because everyone and their uncle are “hip” to the notion of shorting overvalued garbage thanks to terrific books and movies like “The Big Short” that really showed the world how extremely difficult it can be and how the market-makers can artificially create a squeeze on a short player by simply fiddling with the “marks” at the end of every month. I, for one, long for the old days of finding some piece of Vancouver garbage that had a $500,000 annual travel and entertainment budget and a $500 annual exploration budget and a property “next door to Friedland” (!) whose founders held all the one-cent stock that was coming out of escrow next week. Adding insult to injury and turning the ridiculous to the sublime, the CEO has just paid out an egregious amount of money and stock to the telephone room owners whose job it was to “pump up the volume.” Alas, the Elon Musks of theorld learned how to magnificently “manage” their stocks by way of social media and sweetheart deals with all the top 50 hedge fund managers that conspire daily to monitor the share price so that nothing “untoward” can ever happen to threaten the uptrend line, despite being the most over-priced, money-losing auto manufacturer in world history.

The same thing goes for gold and silver with massive quantities of paper gold being traded as if in a virtual reality pit of digital outcry. To say that being long the gold and silver markets since 2013 has been “interesting” is like saying that having root canal surgery without Novocain is “interesting,” when we both know that the proper descriptive should be “agony” or “maddening” but one adjective to most-accurately describe these past five years of shenanigans is “costly” for many people and for all the wrong reasons. Banks cannot sanction gold or silver because there is no counterparty to the transaction. Once it leaves the bank, it is gone.

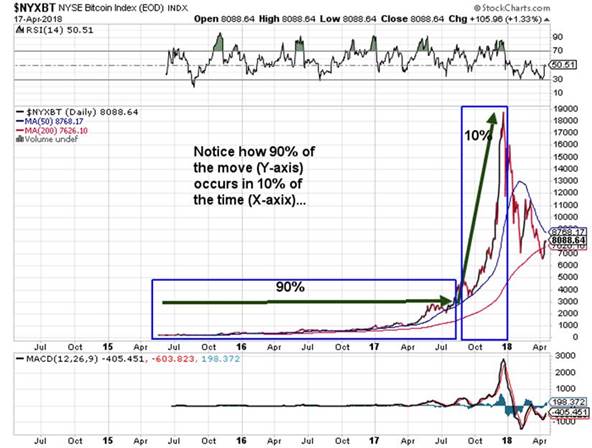

I have one idea for all of you that is, in my humble opinion, one of the greatest “short” set-ups that I have seen in over 40 years trading markets. Because I am leery of interventions and manipulations carried out constantly under the blinded eyes of regulators, I need to short something that would not be exposed to directional risk. The best example of being right about something and wrong at the same time was mid-2017 when I took one look at Bitcoin and determined that it was a bubble of the highest order. That was at $10,000 per coin. It went to $19,891 and then got bombed to under $7,000 and had we shorted it in mid-year, we still would have made money but had we shorted it on December 19, we would have made a fortune. What I knew from my short-selling experiences on the Nikkei in the late 1980s was that the most difficult part of shorting is execution (TIMING) because the biggest move on a chart comes in the last 10% of its journey along the x-axis. (Classic “bubble” chart pattern).

Getting back to my version of “The Big Short,” I would not want to EVER be on the other side of a Goldman “mark” (where they could arbitrarily price your position wherever they want) and we all saw how much pain they went through until the subprime bubble was finally pricked. Instead, I like the idea of risk arbitrage, something I studied at the Wharton School in 1985 with a certain professor named Dr. Jeremy Siegel. Finding relationships between two assets that are either inordinately stretched or compressed can provide the most comfortable returns imaginable when they normalize. If there are two car companies and one is trading at 22 times earnings and the other is at 11 times earnings and they are both pretty much the same in terms of market share and growth, then being short the former and long the latter eliminates the need to be right about the direction of the automotive sector or the broad market a whole. Similarly, if live hog futures are priced too far above live cattle futures, demand for pork declines and demand for beef increases, causing the spread to narrow. Now, it doesn’t matter if human meat consumption shifts in favor of fish and chicken and BOTH pork and beef decline, live hogs will crash harder than live cattle and you will have made a lot of money.

So, the Great Debate amongst the stock and USD bulls is that with the weekly chart showing RSI in the 37 range and with MACD and the Histograms turning up off a deep trough seen in February, the USD is going to rally. Since gold (and silver) are negatively correlated to the USD, is there not a hidden land mine under the metals despite an excellent COT structure and positive technical? The answer is “Maybe” so in order to take the directional risk out of the metals, what is it here in April 2018 that resembles an aberration of sorts? Surely it is the real dollar prices of silver and gold relative to equities and relative to Bitcoin and relative to Toronto real estate that remain an aberration—BUT—even greater than these disparities is the value of silver relative to gold—OR—the Gold-to-Silver-Ratio (GTSR)!

The Gold-to-Silver-Ratio

With the thousands of ETFs covering everything from soybeans to dog food to body parts, you would think that someone could create an ETF for the GTSR but the only tried-and-true method of taking the directional risk out of the precious metals at any time in history is when the GTSR is above 80:1. Last week it hit 86:1 and has quickly retraced but any level above 80 has proven to be a superb entry point. The two most liquid ETFs are the SPDR Gold Trust (GLD:US) and the iShares Silver Trust (SLV:US),and both track physical bullion. With GLD closing at $127.75 and SLV closing at $15.80, you can buy 8.08 shares in SLV with one share of GLD. To get the actual 80:1 ratio, you have to own ten (10) SLV for every one (1) GLD you are short. Assuming you are looking at a big dollar trade, you do the following:

Net Proceeds (-Cost) Margin Required

Short 1,000 GLD at $127.75 $127,750 $63,875 (Ed Note: GLD closed yesterday Apr. 18th at $127.75)

Buy 10,000 SLV @ $15.80 -$158,000 $79,000 (Ed Note: SLV closed yesterday Apr. 18th at $16.27)

Total margin required (Ask your broker about this) $142,875

You are now short the GTSR at 80.80:1

Assumption A:

USD crashes; stocks crash; commodities spike; gold and silver advance; gold is at $1,577.50 per ounce; silver is at $25.95; GTSR is at 60:1

Net Proceeds (-Cost) Profit (Loss)

Buy 1,000 GLD @ $157.75 -$157,750 ($30,000)

Sell 10,000 SLV @ $25.95 $259,950 $101,950

Profit $71,950

Funds committed: $142,875

ROI: 50.35%

Assumption B:

USD rallies hard; stocks explode to new highs; commodities crash; gold and silver decline; GLD is at $107.75; SLV is at $15.35; GTSR is at 70.

Net Proceeds (-Cost) Profit (Loss)

Buy 1,000 GLD @ $107.75 $107,750 $20,000

Sell 10,000 SLV @ $15.35 $153,500 (4,500)

Profit $15,500

Funds committed: $142,875

ROI: 1.08%

Gold and silver under Assumption B have 15.6% and 2.8% declines and the trade remains profitable. Because the relationship between gold and silver was stretched, the directional risk was removed from the initial trade set-up.

The generational range for the GTSR is as follows:

- 2007 – For the year, the gold-silver ratio averaged 51.

- 1991 – When silver hit its lows, the ratio peaked at 100.

- 1980 – At the time of the last great surge in gold and silver, the ratio stood at 17.

- End of 19th Century – The nearly universal, fixed ratio of 15 came to a close with the end of the bi-metallism era.

- Roman Empire – The ratio was set at 12.

- 323 B.C. – The ratio stood at <12.5 upon the death of Alexander the Great.

You have all read my missives on gold and silver and stocks and bonds and the VIX and my dog and my two vices until you all basically know me better than my own children so know this: shorting the GTSR is the best, low-risk trade you can ever get in today’s algo-driven world. As you all know, I took my VIX profits in February and as huge as they were, they did not allow me to parlay the winning in their entirety to my beloved silver. I had to think about what would happen if I was wrong (God forbid) so I put 25% into Fortuna Silver May $5 calls and 25% into the SLV June $15 and $15.50 calls at various prices lower than here. The problem is that since those two positions represent only a portion of the profits on the UVXY trade ($9.38 to $25 in eighteen days), I still have the principal to put to work and I really did not want to give back those winnings as I have done countlessly since 2011.

So I scoured around my thumb-drive memory stick of all the “Greatest Trades of History” and found things like U.S. Secretary of State William H. Seward’s purchase of Alaska from the Russians for $7.2 million and the Dutch West India Company’s Peter Minuit buying Manhattan for “60 gilders” worth of “sophisticated modern (then) European tools” worth (possibly) U.S.$15,000 and, of course, the now-famous “Big Short” trades in the sub-prime derivatives in 2008 and George Soros’ short of the British pound in 1992 (which George would say “broke the Bank of England” but actually simply forced it to abandon the European “Exchange Rate Mechanism”).

These were all “great trades” but what earns them “legendary” status is that they were at once both laughably unpopular and comically contrarian (as was buying the UVXY in late January). Going against the crowd is not very much fun. It is psychologically taxing and emotionally draining. Nevertheless, I believe that the gold-silver “pair” is going to be a shockingly good trade and I have gone “ALL-IN” with my remaining VIX profits and whatever else I can muster after the lawyers and accountants and CRA (and ex-wives) have had their way with me.

So, do your best to look deep into the inner vault of psychological awareness and assess, as I have, what, pray tell, might be the reason that we all take hard-earned, after-tax dollars and try to be heroes. I know I have taken risk throughout my life and in my career so now is the time to invest with “the house.” The current market environment is nothing more and nothing less than a “sanctioned casino” and I might add that it has “forward guidance” in respect of “future actions” that are in demonstrative favor of “the house,” so while I love buying “20 cars of beans” or a “sliver of silver futures,” the trade I am taking shown above will be a huge winner, on a risk-adjusted basis.

Invest with “the House” that HATES gold and cares NOTHING of silver.

If you do, you are long “the House.” Not such a bad trade.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

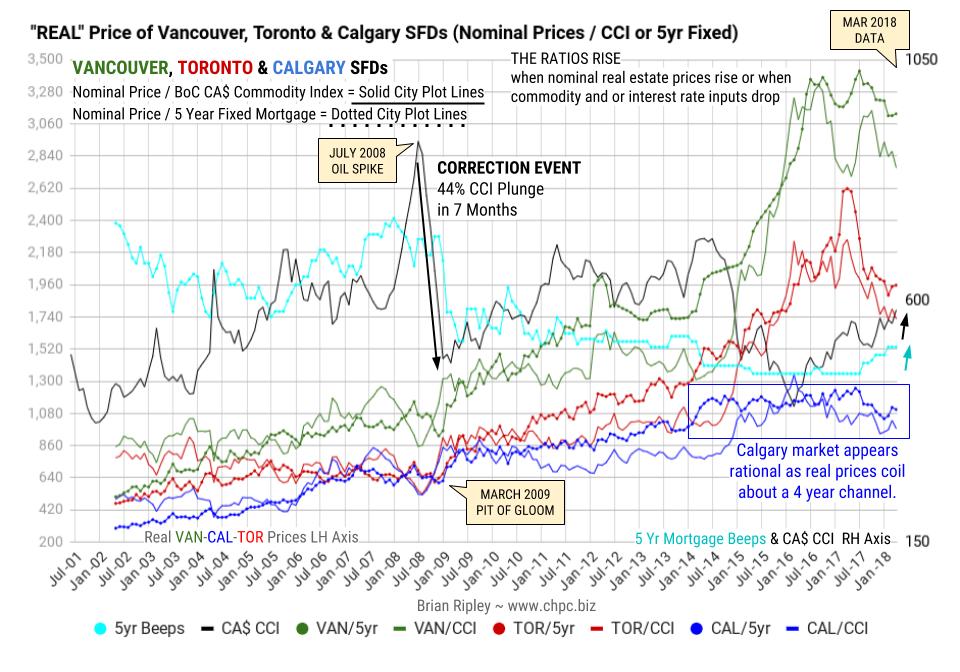

The end is in sight for “fire sale” mortgage rates as Banks begin to push their rates up. In the meantime BC’s & Toronto’s unaffordable mania now leaves only one rational market left in play, where the last 4 years prices have been sideways and winding up for an eventual advance – R. Zurrer for Money Talks

The chart above shows the “real price” of Vancouver, Toronto & Calgary SFDs when looked at from the point of view of the BoC Canadian Commodity Index (CCI) and Borrowing Costs (retail 5yr Mortgage) which are the main input costs apart from operating expenses and tax.

REAL PRICE of HOUSING of Vancouver, Toronto and Calgary Single Family Detached and the Bank of Canada $CAD Commodity Index & 5 Year Fixed Mortgage

In March 2018 commodity prices are still rising and have added to the recent mortgage rate rise in keeping real prices on a downtrend. In Calgary, although prices look rational, the pending seasonal slowdown in the energy sector should limit the nominal purchasing power of weak hands in Alberta but will lift real prices as the cost of energy drops.

There should be no more surprise BoC rate cuts if the federal government mandate plan is to use their fiscal powers, but as we know, the government can surprise us at any time, eg: the new Mortgage Stress Test, the CMHC credit tightening and offloading of risk onto the retail lenders; the threat of new chilling tax and CRA penalties and of course policy flip flops by the federal government like its reversal on electoral reform.

The last 9 years of ZIRP & NIRP monetary policy combined with CMHC’s out-of-control insurance scheme (also add in the BC Gov’t Sub Prime Cash give-away) has been a terrible social experiment in the service of political power and it has replaced affordable housing with indentured mania. Is there a better way?

In a commodity crash, producers lose pricing power as international competitors drop finished prices neutralizing any gains for Canadian exporters from a withering CAD/USD while the +/- 70% of Canadian employees working in the consumer and service sectors look for ways to leverage their deflating earnings at the supermarket and or job fair.

The other major cost input, the retail 5 year fixed mortgage rate (aqua dotted plot line) and last July it moved up off its outstanding record low of 4.64% to 4.84%. This month the Bank of Canada rate remains at 5.14% although street vendors are still pushing sub 3% short term mortgages while the stress test weeds out the weak hands.

The end is in site for fire sale mortgage rates as the major banks push their rates up which forces the real cost of housing (dotted city plot lines) relative to those rates to turn down.

Calgarians are wary of the Trumpster who vows to unleash energy supply 2.0. And when credit is a lifestyle employer as it continues to be in Canada, appraisers will eventually be in demand again.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair