Timing & trends

Lance also answers the question on everyone’s mind, is the 9 year bull market in stocks over? He also updates current market trends and highlights shorter-term investment strategies, risks, and potential opportunities. – R. Zurrer for Money Talks

The big question for investors at the moment is whether the 9-year old bull market has finally come to its inevitable conclusion or is it just a “pause that refreshes?”

While the optimistic “hope” is that this is just a pause within a continuing “bull market” advance, from a money management standpoint getting the answer “right” is vastly more important to long-term investing outcomes.

The easiest way to approach this analysis is to start with the following basic premise:

“Bull markets are born on pessimism, grow on skepticism, and die on euphoria.” -Sir John Templeton

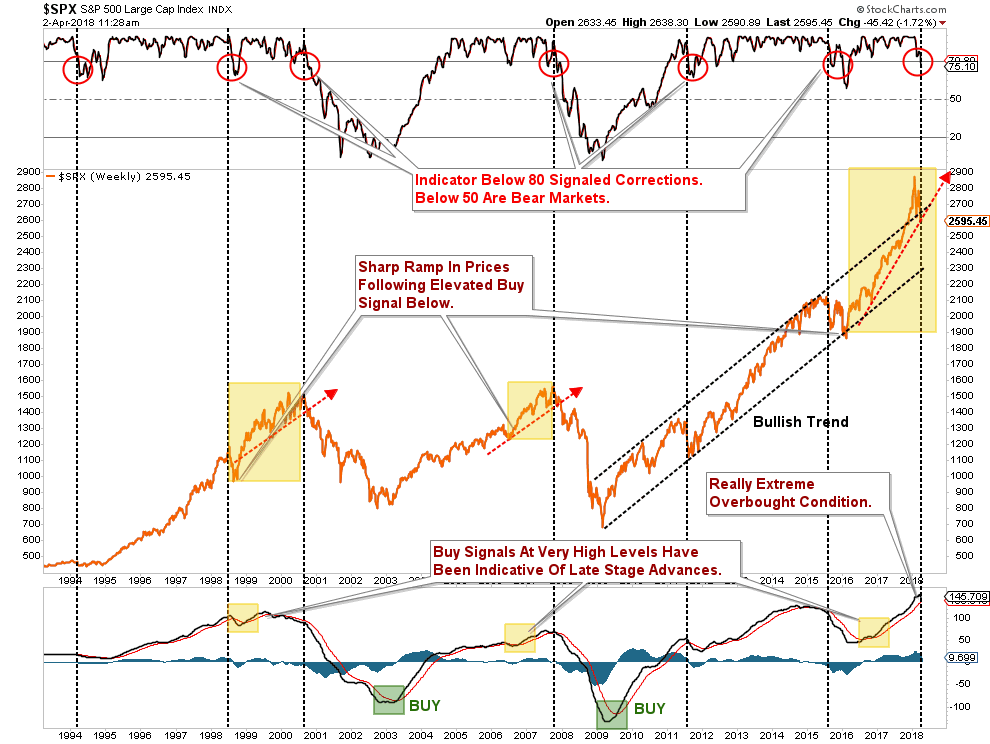

Take a look at the chart below which is Robert Shiller’s monthly data back to 1871. The “yellow”triangles show periods of extreme undervaluation while the “red” triangles denote periods of excess valuation.

Not surprisingly, 1901, 1929, 1965, 1999, and 2007 were periods of extreme “euphoria” where “this time is different” was a commonly uttered phrase.

What about today? Is this another period of “euphoria” or are investors still maintaining enough “skepticism” to fuel the bull market further? Unfortunately, there is little evidence investors are “skeptical” of much of anything right now.

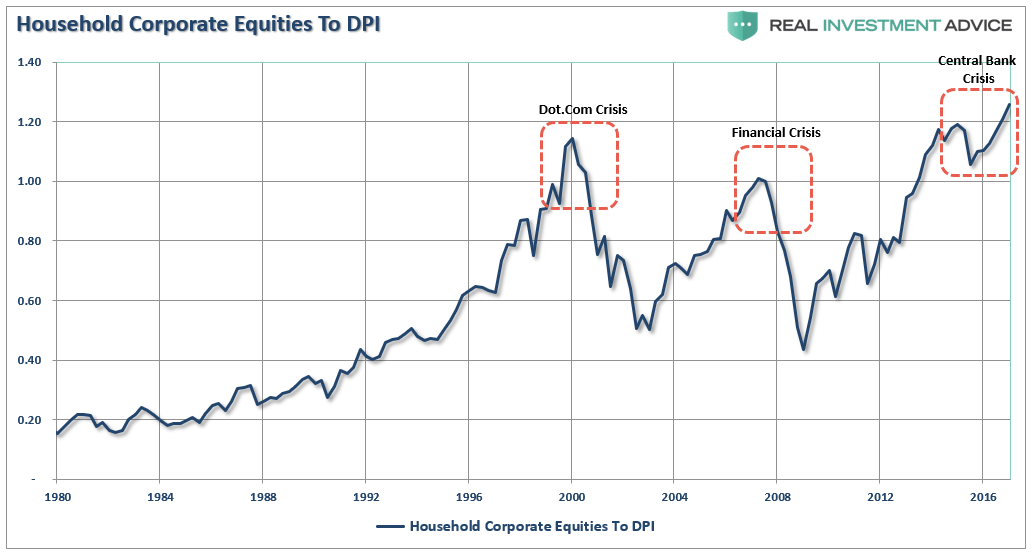

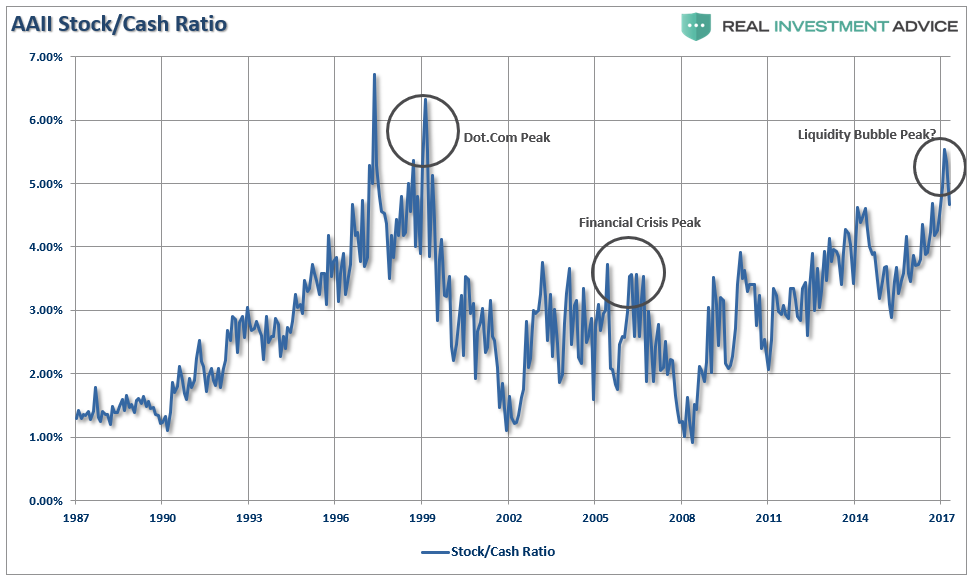

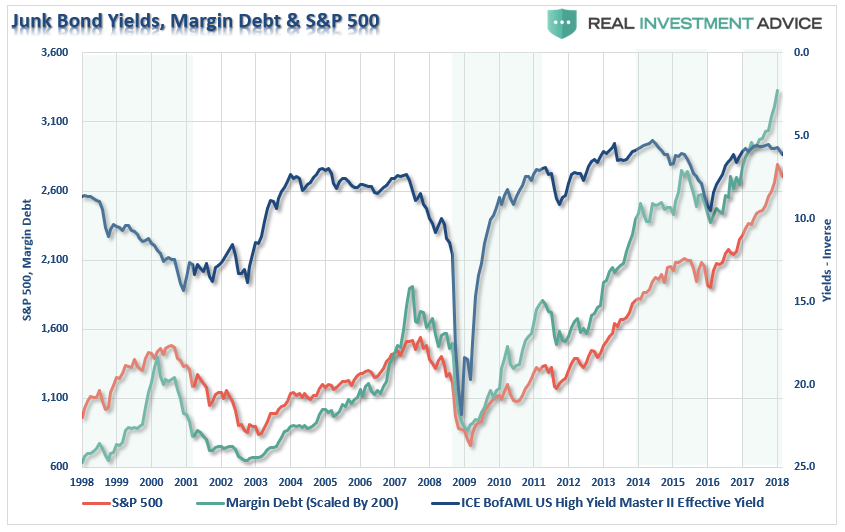

“However, for now, there is little doubt the bullish bias exists as individuals continue to hold historically high levels of equity and leverage, chasing yield in the riskiest of areas, and maintaining relatively low levels of cash as shown in the charts below.”

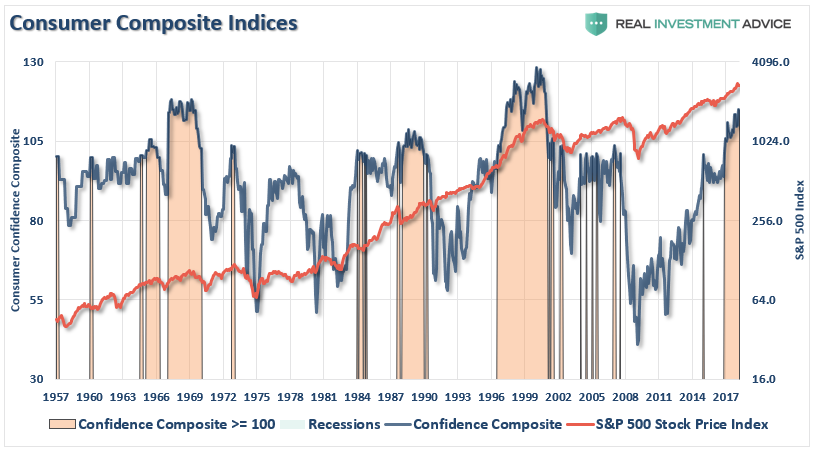

But the “euphoria” of individuals is not just solely related to the stock market, but to the whole economy as well. (The chart below is a composite index of the University of Michigan and Census Bureau measures.)

So, why shouldn’t there be “euphoria?”

The stock market has been surging for the last 9-years, unemployment claims are at the lowest levels in more than 30-years and the housing market seems to be firing on all cylinders.

What’s not to love? But that’s the point.

Bull Markets Die Of Euphoria

The reason that bull markets die of euphoria is that market prices, particularly in the “momentum”stage of the investing cycle, are based on the assumption the current cycle will continue into perpetuity. Earnings, the economy, sales, etc. will continue to expand in a linear fashion…forever.

Since the economy, as well as virtually everything in life, is cyclical, it is only logical that eventually the disappointment of those assumptions sparks the beginning of the next bear market cycle.

Currently, the list of things that could disappoint the markets continues to grow:

- The ongoing rhetoric from Washington over “trade wars” combined with complete fiscal irresponsibility,

- The reduction in support from Central Banks in terms of liquidity support.

- The continued insistence of the Fed to hike rates which continues to reduce the “low rate supports higher valuations” argument.

- The risk of further contagion from Facebook and other “big data” companies on the technology sector (which comprises roughly 25% of the S&P 500) as global threats of “internet taxes” or other data collection policies are considered.

- Revenue growth continues to remain week which is leading to downward revisions in earnings estimates.

- Both domestic and international economic growth has peaked.

- Inflationary pressures from wage growth remains non-existent while the cost of living continues to rise (this will be exacerbated by Trump’s “trade wars.”)

- The yield curve continues to deteriorate and LIBOR has blown out which have typically been early warning sides of bad outcomes.

From a fundamental perspective, the bulls are losing much of the argument there as well. As my friend David Rosenberg recently penned (via Mauldin Economics):

“Dave Rosenberg used four different S&P 500 valuation metrics:

- Forward Price to Earnings Ratio

- Price to Sales Ratio

- Price to Book Value Ratio

- Enterprise Value to EBITDA Ratio

He then calculated the percentage of time that each of these had been at its present level or below. Here’s the result for P/E ratio.

The S&P 500 forward P/E ratio has been below its present level 83% of the time since 1990. Repeating that exercise for the other three metrics and then averaging them, Dave found the index is presently at a 92ndpercentile valuation event.

Here’s Dave, from the transcript, with my bold added:

In other words, only 8% of the time in the past has the stock market in the United States been as richly priced as it is today. And if you want to come up with reasons why that’s the case, that’s fine. But just understand that we are extremely pricey. We’re more than just a one standard deviation event versus the historical average.

Dave then showed this surprising table, comparing historic bull markets with GDP change during the same period.

The 2009–2018 bull market from trough to peak averaged 17.3% annually. Nominal GDP rose 3.6% annually during that time, and real GDP rose 2.1%. Go up the table to the 1982–1990 bull run. It reached a similar magnitude at 17.5%, but nominal GDP rose 7.6% and real GDP 4.2%.

Yes, GDP has its flaws. Today’s economy isn’t like the 1980s. Nonetheless, how is it that stocks rose the same amount on half as much economic growth? Dave said that if the stock-GDP ratio today had remained what it was back then, the S&P 500 would be around 1,550 today.

That’s how excessive valuations are now.”

Okay. you get the idea. There is little evidence to support the “bullish case” other than “sentiment based” data which can, and does, change very rapidly.

When that change in sentiment is combined with extremely elevated, extended and bullish prices, the subsequent “mean reverting” event has been exceptionally nasty. Even with the recent “pause,” the market remains extremely extended and overbought.

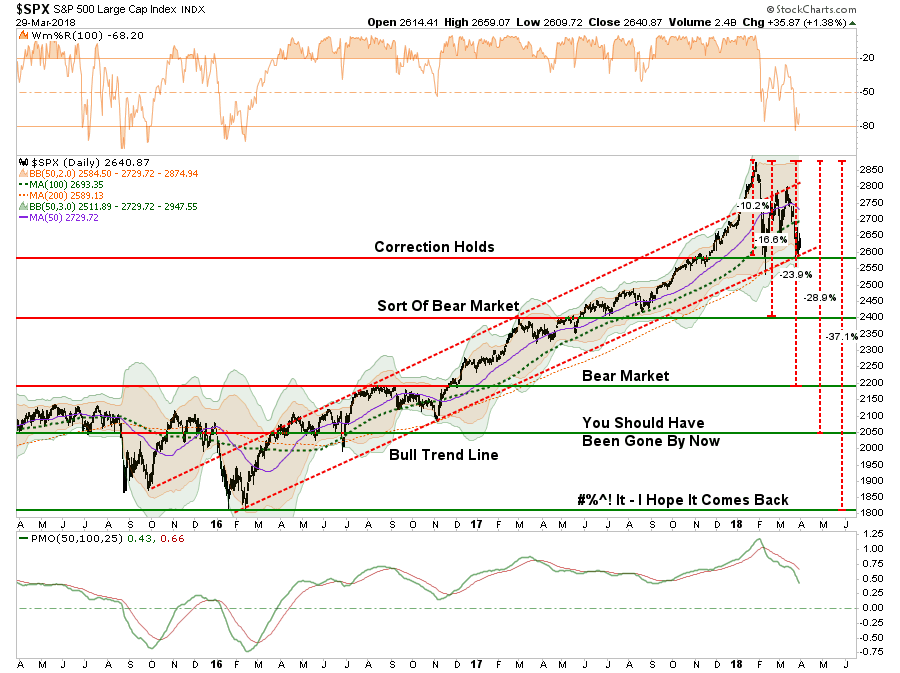

Just how big of a correction from these levels would it be? As I detailed this past weekend:

“The key levels from a price perspective are as follows:

- 2600 – Market holds at current correction levels and resumes bullish trend (optimistic)

- 2400 – Good support lies at 2400 but a 16% correction is painful. Long-term bullish trends remain intact.

- 2200 – Strong support from previous correction breakout. Official “bear market” with near 24% decline.

- 2050 – Economy likely in a recession at this point. Bear market grows with a 29% decline

- 1800 – There is likely a lot going wrong at this juncture and a 37% decline has destroyed most portfolios.

The important lesson here is not to debate on why the bull market will likely resume. Such could very well be the outcome particularly if global Central Banks leap back into action. The lesson is to understand the varying degrees of portfolio risk and have a plan to react if things go wrong.

As I noted last week, missing out on a rally in the market is extremely easy to make up. Recouping lost capital is an entirely different matter.”

Managing Past The Noise

There are obviously many more arguments for both camps depending on your personal bias. But there is the rub. YOUR personal bias may be leading you astray as “cognitive biases” impair investor returns over time.

“Confirmation bias, also called my side bias, is the tendency to search for, interpret, and remember information in a way that confirms one’s preconceptions or working hypotheses. It is a systematic error of inductive reasoning.”

Therefore, it is important to consider both sides of the current debate in order to make logical, rather than emotional, decisions about current portfolio allocations and risk management.

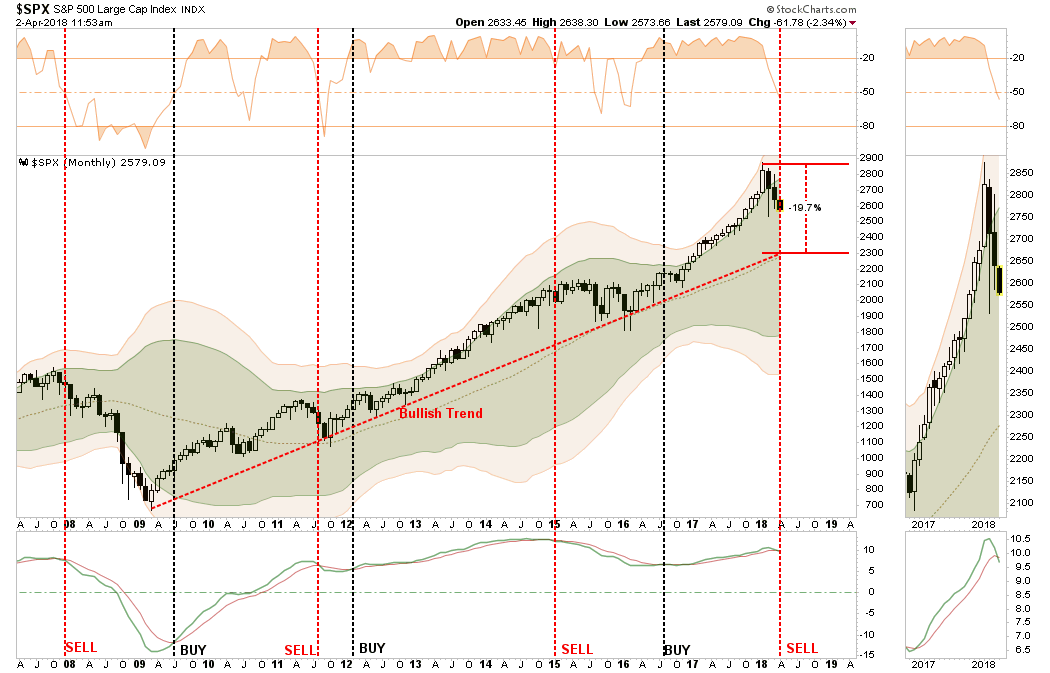

Currently, the “bulls” are still in control of the market. The long-term running bull trend remains intact…for now. The chart below is a MONTHLY chart of the S&P 500 from 2008 to present. What you see is that the bullish trend that began in 2009 remains at the moment and a correction back to that trendline would encompass a nearly 20% decline from recent highs.

However, the real questions is whether this is simply a correction within the longer-trending bull market, or is the initiation of the monthly “sell signal” coincident with the previous late-2007 signal that developed into a major “mean reverting” event? (As a side note, the monthly “sell signal” was also triggered in mid-1999 and no one paid attention then either.)

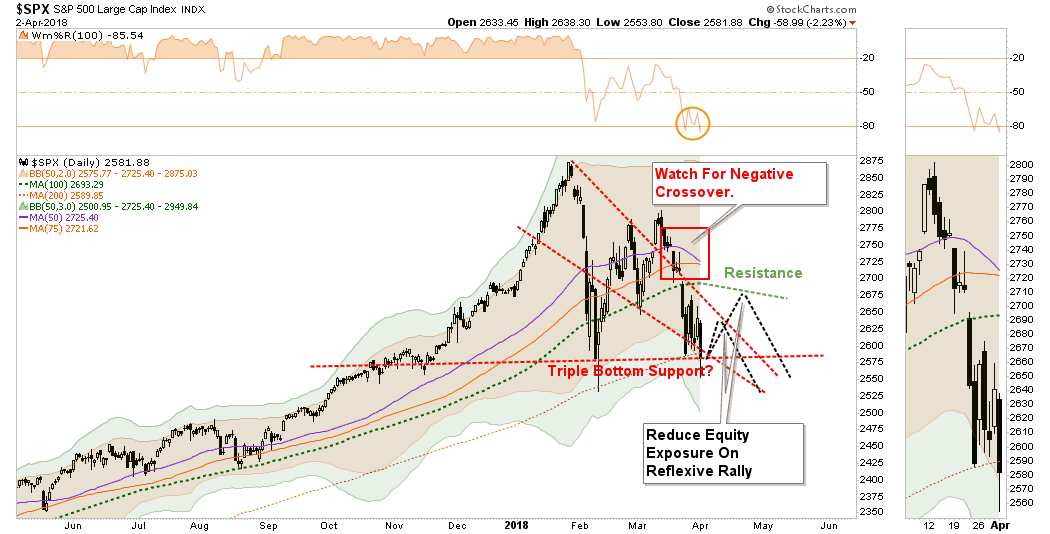

I am not willing to “ride this out” waiting to see what happens. As noted in the chart below, the market is oversold enough on a short-term basis for a reflexive rally to either the top of the current downtrend channel (2625ish) or the 100-dma (2675ish). In both cases, we will be further reducing equity exposure, rebalancing risks and adding hedges to portfolios.

If the market “heals up” and begins a stronger, fundamentally based recovery, we will redeploy capital accordingly. If not, and the market enters a bigger corrective process, the excess levels of cash will hedge portfolios against further destruction of capital.

Here are some basic guidelines we follow in our process.

- Sell positions that simply are not working. If they are not working in a strongly rising market, they will hurt you more when the market falls. Investment Rule: Cut losers short.

- Trim winning positions back to original portfolio weightings. This allows you to harvest profits but remain invested in positions that are working. Investment Rule: Let winners run.

- Retain cash raised from sales for opportunities to purchase investments later at a better price. Investment Rule: Sell High, Buy Low

These rules are hard to follow because:

- The bulk of financial advice only tells you to “buy”

- The vast majority of analysts ratings are “buy”

- And Wall Street needs you to “buy” so they have someone to sell their products to.

With everyone telling you to “buy” it is easy to understand why individuals have a such a difficult and poor track record of managing their money.

While “bearish” concerns are often dismissed when markets are rising, it does not mean they aren’t valid. Unfortunately, by the time the “herd” is alerted to a shift in overall sentiment, the stampede for the exits will already be well underway. Just remember, the process of “getting back to even” is not an investment strategy that will work over the long term.

Is the current bull market dead? I don’t know, and trying to predict the market is quite pointless. The risk for investors is the “willful blindness of change” until it is far too late to matter. Just remember, no one thought the “bull market was dead” in 1999 and 2007 either.

I don’t need to remind you what happened next.

Lance Roberts

While everything else has been getting smashed down, Gold and Silver were two of the few assets that were up within the overall carnage. This analyst makes the case that this is the result as investors begin to switch from building wealth to protecting wealth – R. Zurrer for Money Talks

MARKET MELTDOWN CONTINUES: Gold & Silver Prices Begin To Disconnect

As the BLOOD continues to run on Wall Street, gold and silver were the few assets trading in the green today. As I have mentioned in past articles and interviews, investors need to get used to this sort of trading activity. Even though the Dow Jones Index ended off its lows of the day, it shed another 458 points while the Nasdaq declined 190 points and the S&P fell 60.

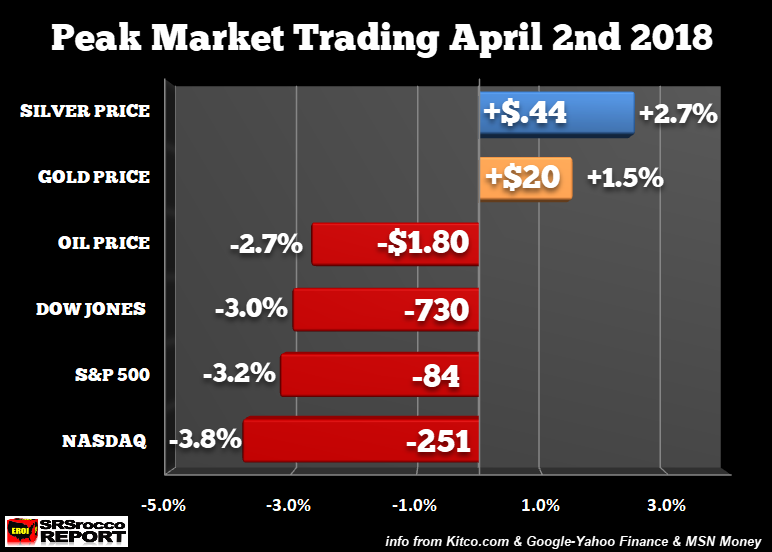

As the broader markets sold off, the gold price increased $15 while silver jumped by $0.25. However, if we look at these markets during their peak of trading, the contrast is even more remarkable:

At the lows of the day, the Dow Jones Index fell 730 points or 3%, while the S&P 500 fell 3.2% and the Nasdaq declined by 3.8%. Also, as I expected, the oil price fell along with the broader markets by dropping 2.7%. If individuals believe the oil price will continue towards $100, due to supply and demand fundamentals put forth by some energy analysts, you may want to consider one of the largest Commercial Net Short positions in history. Currently, the Commercial Net Short position is 738,000 contacts. When the oil price was trading at a low of $30 at the beginning of 2016, the Commercial Net Short position was only 180,000 contracts.

Furthermore, if we agree that supply and demand forces are impacting the oil price to a certain degree, does anyone truly believe oil demand won’t fall when the stock market drops by 50+%??? I forecast that as market meltdown continues, the oil price will decline as oil demand falls faster than supply.

Now, when the markets were at their lows today, gold at its peak was up $20 while silver increased by $0.44. Of course, this type of trading activity won’t happen all the time, and we could see a selloff in all assets some days. But, once the Dow Jones Index falls below 19,000, investors will likely start to move into gold and silver in a much bigger way.

If we look at the following stocks and indexes from the peaks set in 2018, clearly, there’s a long way to go before the bottom is in:

The infamous FANG stocks are down between 14-20% from their highs while the broader markets are down 10-11%. When the Dow Jones Index fell from its high of 14,100 in 2007 to its low of 6,600 in 2009, it lost 53%. However, due to a higher degree of leverage in the markets today, I wouldn’t be surprised to see the Dow Jones Index fall by 60-75%. A 60% decline in the Dow Jones Index from its peak would put it at the 10,000 level… perfectly reasonable in my opinion.

So, what would a 60% selloff in the broader markets due to the gold and silver price?? That’s a good question. If just 1% of the $400 trillion in global assets moved into the precious metals, we could see some insanely higher prices. But, I don’t like to put out price targets because analysts who have done so in the past only frustrate themselves and their followers.

The next two charts show the beginning stage of the MARKET MELTDOWN as it pertains to the grossly overvalued stock called Netflix. When I posted this stock a few weeks ago, Netflix was trading at $310 a share. I mentioned that its recent stock trend resembled the antenna on the Empire State Building in New York City:

Unfortunately, the top of Netflix’s antenna must have been chopped off by some low flying 747 jetliner over the past two weeks:

Since March 19th, when Netflix was trading at $310, it has lost $30 or nearly 10%. If investors believe Netflix is a good BUY THE DIP setup, well then I gather you would be too stupid to consider buying gold and silver instead. So, I am not going to waste my breath. However, if you are beginning to get worried that the market has a long WAY TO GO DOWN, then you may want to consider switching from BUILDING WEALTH to PROTECTING WEALTH.

Mark my words… 2018 will be the year that investors started switching from building wealth to protecting wealth. Unfortunately, those who make this change will likely only be a small percentage of the market. Thus, we are probably going to see a lot more BLOOD IN THE STREETS.

This analysis as well as Martin Armstrong’s Quarterly Closing Post clearly state that it is just not Gold’s time to explode upwards. Jordan indicates below the factors that will have to fall into place before Gold can begin a long term bull swing upwards – R. Zurrer for Money Talks

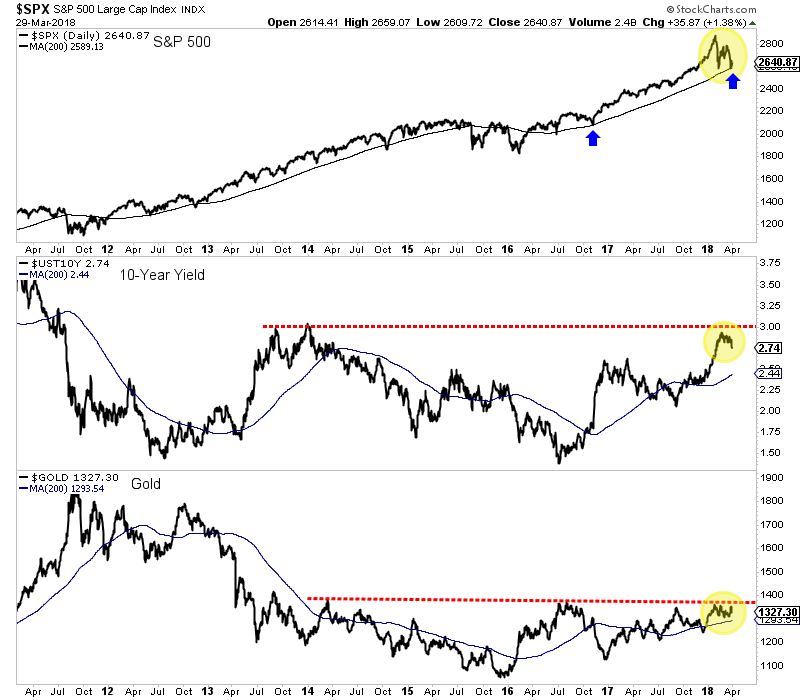

Last week we noted that Gold’s quarterly close would be a key marker for Gold’s immediate breakout potential. Gold was seemingly on course for its highest quarterly close since 2012 until it reversed back below quarterly resistance at $1330/oz. Hence, an imminent break to the upside is unlikely and gold watchers will have to remain patient. It’s not yet Gold’s time. It will be soon enough.

One catalyst for the most recent strength in Gold (the correction in equities) appears to have faded as the S&P 500 has held its 200-day moving average. A sustained rebound in equities while bond yields correct would not be particularly bullish for Gold. The obvious reason is capital is flowing into equities and not Gold. A rebound in equities amid a temporary reduction in inflation expectations would equate to stable or rising real yields.

{kind=link}

The other scenario is bond yields do not break to the upside, there is a slowdown, the stock market declines and the Fed has to reverse course all together. As we predicted in past editorials, long-term yields are trending lower and that could continue. In the meantime, Gold will not break to the upside unless the stock market experiences more turmoil.

In addition to the current macro-market backdrop, history suggests that it may be too early for Gold and gold stocks to begin another bull move. In November we discussed how the gold stocks were following the pattern that other markets followed after a “mega-bear market” (which we define as multi-year and +80% in price).

Take a look at those examples and note the time between the end of the bear market and the next significant low (from which the bull resumed). In most cases the time between those lows is two years and seven to nine months. For the gold stocks it has only been two years and two months since that epic January 2016 low.

Assuming stocks rebound and long-term bond yields continue to moderate, then Gold is unlikely to breakout this spring. However, that is perfectly okay as our historical study suggests the miners (while facing little downside) may not begin a real bull move for several months. Gold Investors should not be discouraged as they could panic at the absolute worst time (I’m already seeing it anecdotally). Regardless of whether the bull move begins in a few months, five months or whenever, we continue to remain patient while accumulating the juniors we think have 500% return potential over the next 18-24 months.

Jordan

With the Federal Reserves declared intent to drive interest rates back to normal to save pension funds, a rising interest rate scenario immediately reopens that 8th wonder of the world, compound interest, as an investment strategy to pursue. This grapic pounds home the incredible power of compound interest as a wealth building strategy – R. Zurrer for Money Talks

Double Click on image Below for Larger Version

Tech investment expert Blake Corbet has some buy recommendations and what stocks to drop like a hot potato after the revelations about Facebook and other companies harvesting and selling your personal data makes waves throughout the world. What should you be selling? Where are the opportunities as FB and others get hammered?

….also from Michael: Federal Liberals Blackmail Canadians

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair