Mike's Content

Greg on the giant air pockets that could open up in the market as massive pension funds attempt to liquidate 10’s of thousands of $100 plus tech stocks. When there are no buyers the market collapses, often with no trades taking place as happened in 1987 when the Stock Market dropped 22% in one day. Trouble is, Greg thinks it will be much worse this time and explains why. Bottom line, Greg issues a major warning that the game’s changed) – Robert Zurrer for Money Talks

02:50 – 19:24 Featured Guest: A word to the wise – big name analyst, Greg Weldon issues a major warning for investors. Hint: the game’s changed.

….also from Michael: Dr. Michael Berry Ph.D: Prepare Yourself For Higher Rates

Put options are how you protect your investments from devastation yet allow yourself to participate in all upside a market has in store. For information on how to use them well, go watch Michael Campbell’s “How to Invest in Options”. Just register as for Michael’s Free E-Service on moneytalks.net and bingo,navigate to the Options video and watch – Robert Zurrer for Money Talks

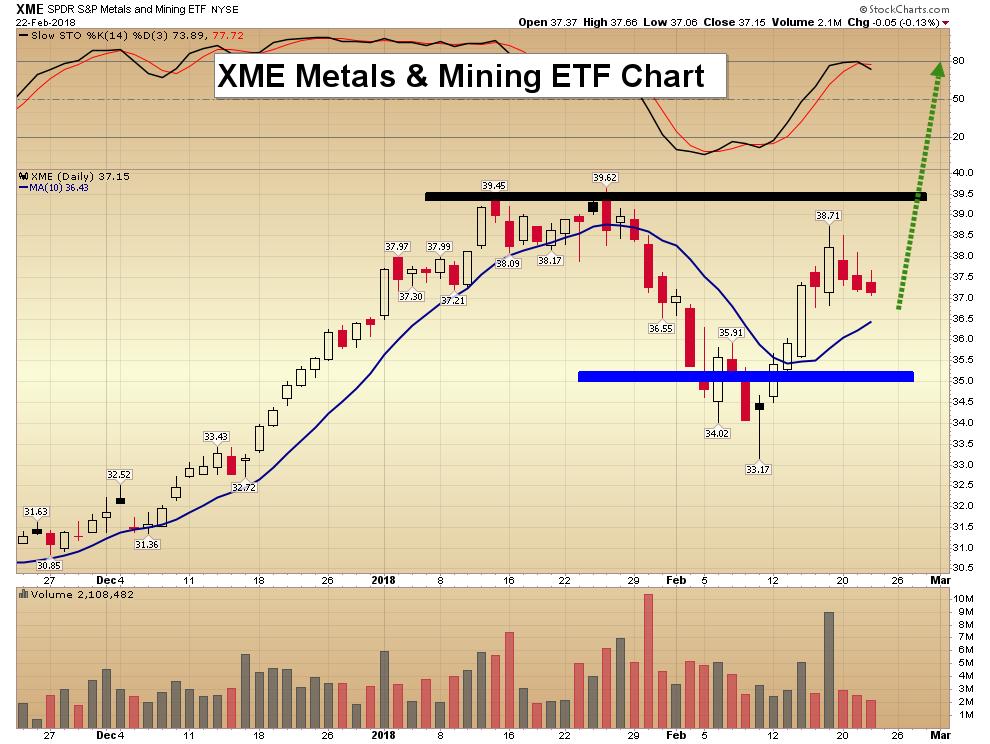

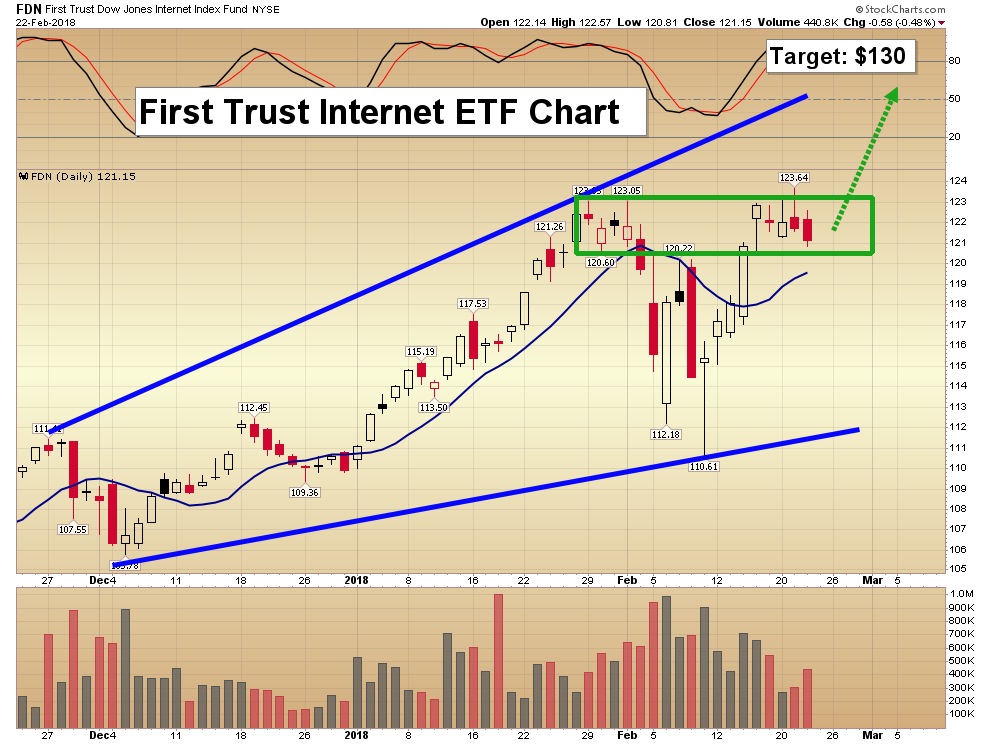

Today’s videos and charts (double click to enlarge):

SF60 Key Charts & Video Update

SF Juniors Key Charts & Video Analysis

SF Trader Time Key Charts & Video Analysis

Morris

website: www.superforcesignals.com

email: trading@superforcesignals.com

email: trading@superforce60.com

|

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

|

|

When Government hikes taxes it’s always a negative for growth and job creation, especially when they are raised on business. The NDP Government just raised taxes 5.5 Billion with 3/4’s aimed at business so… there will simply be less money to spend on hiring. Wait, it gets worse….

….related from Michael: The Dangers of Gov’t Cooling Real Estate

Martin Armstrong, who has been very accurate on rising interest rates, and he impact they are having on pensions and Europe. He sees another banking crisis coming just as the United States is looking at a new radical bank rescue policy that will effect depositors rather than taxpayers – Robert Zurrer Money Talks

![]()

While the stock market crashed as the pundit looked in their bag to try to come up with an excuse, they blamed rising inflation and interest rates. Yet, nobody is really paying attention to the underlying trend. The cost of carrying debt has been rising gradually and there are noticeable measurable impacts that the pundits are of course oblivious to since they have to explain every day’s movements and not the real trend.

Already, the 10-year rate is piercing above the 2.6% area. There is an impact on the currency once people begin to comprehend the trend. The 10-year German bond rate is 0.70%, and this has been maintained by the ECB buying 40% of European government debt to no avail for nearly 10 years.

The real crisis comes when they realize that the ECB will not be there to buy government debt. The bidders will demand a higher yield so rates will rise very rapidly.

Meanwhile, the Fed will pursue higher interest rates as they need to be normalized to help pensions funds that are rapidly collapsing. This idea of a lower dollar will raise the price of imports and with tariffs, inflation in consumer products will rise.

Mueller is still not ending his investigation. Why should he? He would have to go get a real job in the private sector. Keep the investigation alive to pay the light bills. He shows no sign of embracing unemployment. His pretend indictment is dancing between raindrops, indicting people in Russia knowingly there will never be a trial. We cannot count him out yet as a factor that will undermine the economic confidence.

So we stand at the threshold of rising rates that will then feed into the market and create a bid for the dollar it appears after March.

The Coming Banking Crisis & The End of Bailouts

Behind the curtain, there is a growing concern about a serious banking crisis beginning once again in Europe. Many governments are talking about the crisis behind-the-curtain and we are now beginning to see steps that are being taken to end the TO-BIG-TO-FAIL policies that dominated the 2007-2009 Crash.

The United States is looking at a new radical bank rescue policy where the government is proposing to revise a central pillar of the idea of bailing out banks creating new financial regulation with a new Chapter 14 bankruptcy procedure. They are looking at eliminating the risk of taxpayers’ costs to bail out banks. They are investigating the means for an orderly resolution so that the taxpayers do not have to bail out the banks. This development is causing some concern among the high-flying Wall Street banks, for if that is the case, then another crisis as 2007-2009 will result in even Goldman Sachs closing. The proposal looks to shift the burden to the shareholders and creditors of that bank. This means depositors who are thus creditors.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair