Stocks & Equities

There’s a really unique investment company in Europe you ought to know about… because they are insanely profitable.

There’s a really unique investment company in Europe you ought to know about… because they are insanely profitable.

|

|

|

|

|

Jan 1st has come and gone, and wow was it a busy December. Most in the industry reported Jan 1st when the new stress test arrived (you can read more about the stress test by reading the previous article here). So, now that the new rules are in effect, how may you be impacted?

First off, its important to note that Credit Unions are NOT affected by the new guidelines as they are provincially regulated, not federally regulated. The Credit Unions have confirmed that they will not be following suit with the movement to change qualification criteria. Mortgage Brokers have never before been so important, being able to shop banks but also non-banks and Credit Unions to source loans.

Borrowing power with the bank is now reduced by about 20% for those choosing to take a 5 year fixed rate mortgage. All other terms were already stress tested, but previously choosing a 5 year fixed was a way to get around to tighter qualification guidelines and now that option has disappeared.

Some banks have confirmed that anyone with a contract dated prior to Jan 1, 2018 will be grandfathered under the old rules. This is important for those of you who have presales completing in the next few years. There was no clarity on this rule for many banks until very close to the deadline. In some cases, as late as Dec 29th!

One item that is interesting here is that shorter term rates like variable and 1-3 year fixed terms will now qualify at a lower interest rate, which will incentivize some borrowers to take shorter term rates. This is something that is likely an unintended consequence of the new rules and likely something that the government didn’t quite think through when introducing the new rules. One of the last things the government wants is for borrowers to be assuming short term debts in an environment where interest rates are so low and rates rising too quickly will have many of these borrowers seeing increases to their payments in just 1-2 years instead of ~ 5 years (as many borrowers were previously to maximize borrowing power).

All in all, these rules are intended to make it harder to qualify, yes, but are also here to protect the value of your real estate assets from a collapse like what was seen down in the US in the subprime crisis. If you are seeking financing, it may be wise to jump in sooner rather than later as the Credit Unions may see more volume than they can handle and start to taper their guidelines as well.

Andrew Ruhland examines the three Ts: Time, Training and Temperment to help you identify any pitfalls in your self-directed investing.

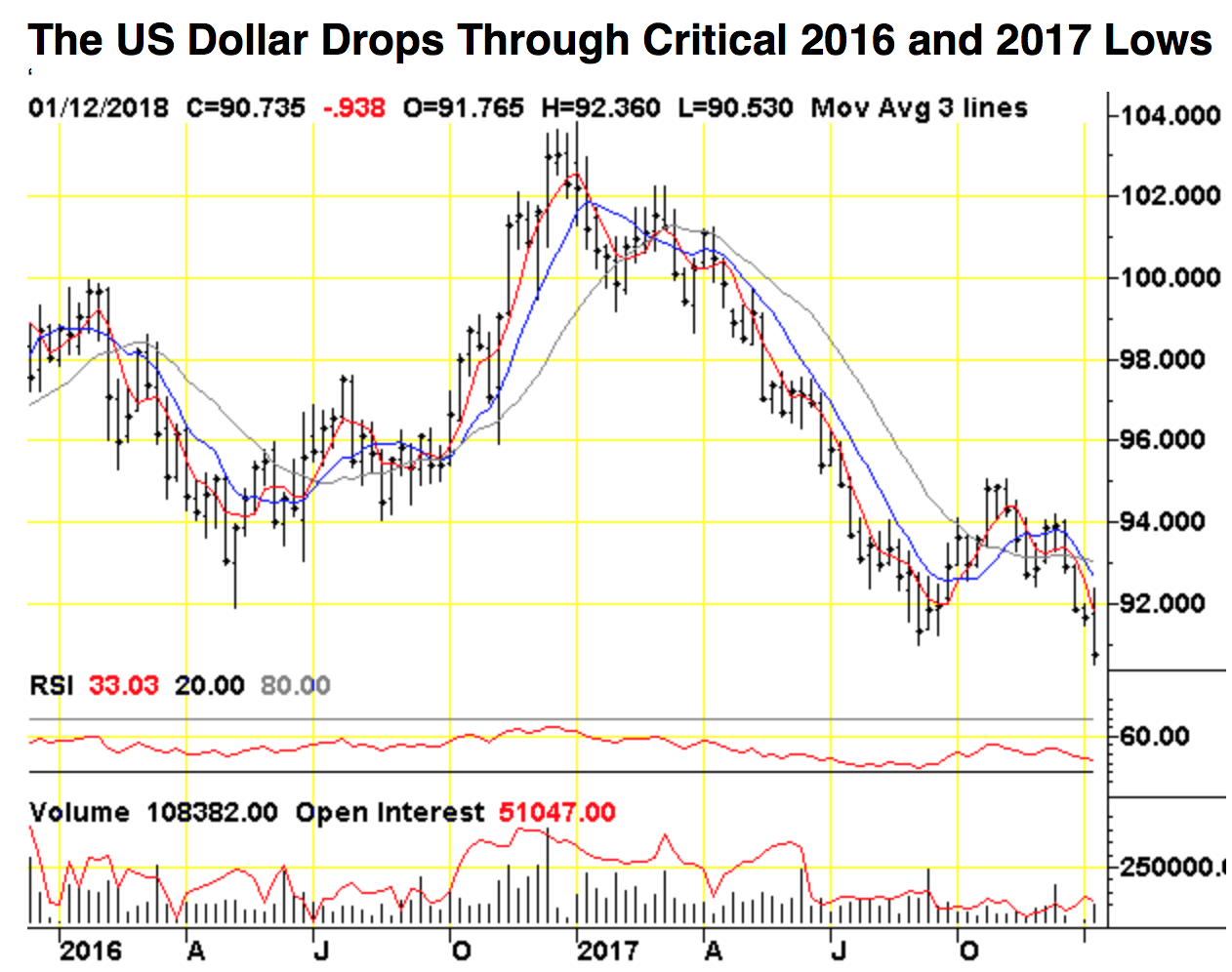

Victor Adair on the US dollar Index breaking down sharply lower below the 2016 & 2017 lows in first few weeks of 2018 while stocks, crude oil, interest rates & Gold move sharply higher

Two years ago Martin Armstrong’s Computer Model predicted the Trump Presidential win and the Brexit vote. In 2013 at the World Outlook Financial Conference, Martin gave the date in February, 2014 for the Russian invasion of Ukraine. This year Marty’s model predicted the independence vote in Catalonia – but that wasn’t the one that blew me away.

Two years ago Martin Armstrong’s Computer Model predicted the Trump Presidential win and the Brexit vote. In 2013 at the World Outlook Financial Conference, Martin gave the date in February, 2014 for the Russian invasion of Ukraine. This year Marty’s model predicted the independence vote in Catalonia – but that wasn’t the one that blew me away.

In September, I asked Marty about Bitcoin. He told me it was tough to get a read because of the lack of historical trading data and volume numbers. With that in mind, he said the short-term chart looked like the uptrend could carry much further than most people expected but – and it was a big BUT – his computer model was forecasting a top starting the week of December 18. (The actual peak was December 17th and 18th.)

I don’t know why I was surprised. I’ve been following Marty’s model since 1983 and in that time it has accurately predicted so many major events from the date of the fall of the Berlin Wall to the top of the Nikkei Index in 1989.

I could go on but allow me to share one more story. Forgive me if you’ve heard me tell it before but it’s worth repeating. The first time I saw the documentary about Marty – The Forecaster – in 2014 I was shocked to see a slide from our 1998 World Outlook Conference in one of the scenes.

The slide read:

- 1998 Collapse of Russia

- 1999 Low in oil and gold

- 2000 technology collapse (like railroads in 1907)

- 2002 Bottom US share market

- 2007 Real Estate Bubble – Oil hits $100

- 2009 Start of Sovereign Debt Crisis

- 2011 – 2015 Japan Economic Decline

- Euro begins to crack due to debt crisis

- 2015.75 – Sovereign Debt Big Bang

There it was…all of it happened…absolutely amazing – so maybe I shouldn’t have been surprised with the Bitcoin call.

So What Now

Regular attendees of the World Outlook Financial Conference heard Marty’s forecast in 2013 that the Dow Jones was on its way to 18,000 and once breaking that barrier would hit 23,700, which it did this year. And when it broke through that number – another major move to the upside would take place. In November, in anticipation of the speed of which the markets are moving, Marty published a new report called How To Trade A Vertical Market… obviously great timing given the Dow just added the fastest 1000 points in history. But for how long and how far?

We’ll get the answer this year as Marty’s model has already predicted that 2018 will feature a Panic Cycle, which could come shortly after the World Outlook Conference. More importantly The Panic Cycle will feature major moves in both directions depending on the specific market. As Marty says, Panic Cycles are notorious for trapping people on the wrong side of the market, so obviously it’s essential to be on the right side in order to protect yourself and profit from what’s coming.

Adding to the volatility is that Marty forecasts 2018 as the beginning of the Monetary Crisis Cycle, which impacts every market.

We’re already seeing it in the weakness of the US dollar and the accompanying strength of the euro and to a lesser extent the loonie. But is the US dollar weakness an opportunity to buy? Conversely is the euro strength an opportunity to play it to go down? Get those questions right and you can make a lot of money.

Marty’s Summation

“This is going to be a crazy year that seems to be divided into two trends in many markets but not all.” And by the way, he is responding to a ton of requests, including one from me, and he is producing a special report on Canada that will be available at the Outlook Conference.

Marty will be with me Friday night, February 2nd and again on Saturday afternoon, February 3rd. We’ll cover stocks, gold, interest rates, the bond market, currencies and oil.

It’s an incredible opportunity to hear who I consider the top forecaster in the world.

One More Question: Why Does He Do It

Armstrong Economics is in demand throughout the world. They advise on literally trillions of dollars worth of investments. The Wall Street Journal called him the highest paid financial advisor in the world. So why does he find the time for us no matter where he is in the world?

Simply put, there are two reasons. First off, we’ve been friends for over 35 years and he has always been generous with his time and support. And secondly, he has a major commitment to helping individuals, (especially our children who are inheriting this financial mess), navigate through these increasingly volatile and chaotic times.

I hope you to take advantage of the opportunity. If you already have your ticket great! Tell a friend, tell a family member too!

Sincerely,

Mike

P.S. Getting the chance to hear Marty is one of the best reasons to bring a younger person to the conference. It will be an amazing eye opener that he or she won’t get at university or in the mainstream media. That’s why we have a special offer – if you buy a ticket – you can bring a student absolutely free. The only thing is that we ask you to let us know that you want a student ticket when you purchase your ticket. We have only 23 of these tickets left so please don’t wait.

P.P.S Date: The World Outlook – Friday, February 2nd and Saturday, February 3rd.

Place: The Westin Bayshore, Vancouver, B.C.

Tickets: – Go to www.moneytalks.net/events/world-outlook-conference-2018.html

P.P.P.S There are still a handful of special rate rooms available at the Westin. The special rate expires tomorrow! CLICK HERE to reserve

Can’t make it in person? Subscriber to our HD Video archive – get unlimited viewing of all our mainstage speakers including both of Marty’s presentation on any device from anywhere in the world. CLICK HERE to order

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair