Timing & trends

1. Lest We Forget

1. Lest We Forget

by Michael Campbell

Would Prime Minister Trudeau and the NDP’s Jagmet Singh be lauding Castro if they understood what our veterans fought and died for? .

2. Canada’s Clinton Inspired “Deplorable” Moment

by Michael Campbell

It took Governor General Julie Payette only a few moments to dismiss and denigrate a huge portion of the Canadian population. And the Prime Minister loved it. It’s the same attitude that has produced massive political, economic and financial repurcussions through-out the Western World.

3. New Mortgage Regs Could Lower Borrowing Power

After a lot of deliberation over the spring and summer, the Office of the Superintendant of Financial Institutions has come out with new regulations that will make it harder to qualify for mortgages once again.

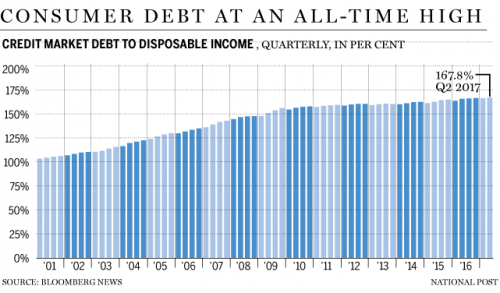

As Canadian household debt hit an all-time high in 2017 (see chart), a new study by TD Bank finds that 97% of Canadian homebuyers say they wish they’d factored in their other financial obligations when determining the mortgage they could afford. (Too bad their mortgage broker/architect/advisor was not required to factor these ‘obligations’ into their loan approval consideration either.) We are not talking about extraordinary, unexpected expenses here: 54% of those surveyed wish they’d considered property taxes and maintenance costs, and a third cite overall lifestyle expenses.

Lenders have been encouraged to be more lax in their approval process, because Canadian taxpayers are backstopping some 55% of Canada’s $1.6 trillion residential mortgage loans –$496 billion through CMHC, plus 90% of the $400 billion+ underwritten by Genworth MI, plus an undisclosed exposure through Canada Guarantee co-owned with the Ontario Teachers’ Pension.

Presently Canadian mortgage defaults are near cycle lows: less than .5% of residential mortgages held by the largest lenders are today considered delinquent (behind on monthly payments). But as acknowledged in the CMHC Q2 financial report:

The most important vulnerability is Canada’s high level of household debt, which could amplify the impact of an economics shock if indebted households begin to deleverage or struggle to repay their debt balances…

With property prices in major Canadian markets today considered the most over-valued in the world, it is prudent to consider what happens if when property prices mean revert, potentially taking prices below outstanding mortgage amounts so that owners are ‘underwater’ as seen in the 2006 US housing bust.

All insured residential mortgages in Canada are ‘full recourse’ meaning that if a borrower defaults and the property sale recoups less than the mortgage, the insurer pays to make the lender whole, and then sues the borrower to recoup the shortfall. But with so many high-ratio mortgages outstanding (minimal owner equity) along with other large unsecured consumer debts, and typically low liquid savings, the incentive for the debtor to file for bankruptcy is large.

As Canadian insolvency manager Scott Terrio points out in MacLeans this week, in the event of a shortfall (and default), the balance owing becomes unsecured—just like any credit card or unsecured line of credit—and the lender must then rely on the civil court to collect on the loss (shortfall). But a lender cannot take court action when a Canadian insolvency proceeding is underway, nor afterward as the debts are then legally discharged. See: Here’s how Canadians could walk away from their homes if house prices fall:

“…you can essentially walk away from your home in Canada, no matter the amount of the shortfall, if you file a bankruptcy or a proposal with a Licensed Insolvency Trustee. The estimated shortfall gets included as a normal unsecured debt for which the lender files a proof of claim, and it is discharged. No other recourse is available in the courts to the lender.

In my experience, this is a very little-known fact, even among those who are quite financially sophisticated…

The bottom line: in bankruptcy and creditor proposal filings, defaulting Canadian homeowners will leave losses to their lenders. And where those losses have been insured by the Canadian government, the losses will flow to us taxpayers. In the cleanup phase of the largest property bubble in Canadian history, this is likely to happen more than most imagine possible.

Following the surge in Bitcoin’s USD price after the suspension of the SegWit2x hard fork, the cryptocurrency has collapsed as traders exit ‘fork dividend’ trades.

Dennis Gartman had a few words of praise for the bulls right before the collapse…

Well “bully” for Those Who’d Gotten It Right: Our “position” on Bitcoin and the other cryptos is clear: we shall have nothing whatsoever to do with them, but “good on” those who’ve been long and right; but be careful… all Bubbles eventually end in tears.

As bitcoin fell, Bitcoin Cash – a clone of the original that was generated from another split on Aug.1 – surged, trading up as much as 35%, ahead of this weekend’s launch of Bitcoin Gold.

…also from ZeroHedge:

“This Looks More Frightening”: Global Stock, Bond Selloff Accelerates Amid Risk-Parity Rumblings

Here we go again…

Since June of 2013, I have been writing about the reasons why rates can’t rise much and why calls for the end of the “bond bull market” remain wrong.

Regardless, about every 3 months or so, there is a tick up in rates and you can almost bet that soon thereafter will be a litany of articles explaining why THIS time the “bond bull market” is really dead. For example, just from this past week:

- Great Ready For The Great Bond Bust Of 2020

- The Great Bond Bull Market May Be Coming To An End

- 700 Years Of Bond Data Forewarn Of Rapid Reversal From Low Interest Rates

What is the argument from low rates will rise?

It basically boils down to simply this – rates are so low they MUST go up.

The problem, however….

…also from Seeking Alpha:

Opinions in this report are solely those of the author.. The information herein was obtained from various sources;; however,, we do not guarantee its accuracy or com pleteness.. This research report is prepared for general circulation and is circulated for general information only.. It does not have regard to the specific investment objectives,, financial situation,, and the needs regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized..

Investors should note that income from such securities,, if any,, may fluctuate and t hat each security’s price or value may rise or fall.. Accordingly,, investors may receive back less than originally invested.. Past performance is not necessarily a guide to future performance.. Neither the information nor any opinion expressed constitutes an offer to buy or sell any securities or options or futures contracts.. Foreign currency rates of exchange may adversely affect the value,, price or income of any security or related investment mentioned in this report.. In addition,, investors in securities suc h as ADRs,, whose values are influenced by the currency of the underlying security,, effectively assume currency risk.. Moreover,, from time to time,, members of the Institutional Advisors team may be long or short positions discussed in our publications..

BOB HOYE,, INSTITUTIONAL ADVISORS

bhoye..iinstitutionaladvisors@@ttelus..nnet

WEBSITE

www..iinstitutionaladvisors..ccom

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair