Stocks & Equities

Let’s face it – investors around the world are nervous. Everywhere they look, read, and hear – someone is warning about the the stock market.

Let’s face it – investors around the world are nervous. Everywhere they look, read, and hear – someone is warning about the the stock market.

Yes, stock markets occasionally go down. But so do other markets as well.

The challenge today, is that the 2000 Tech Bubble and the 2008 Housing Bubble is fresh on everyone’s mind. And since these bubbles eventually manifested themselves in the stock market – people today believe every financial crisis must eventually be reflected in the stock market.

Of course, this is linear thinking. And considering bond, interest rate and currency markets dwarf the stock market – investors better understand that the tail doesn’t wag the dog.

Since the risk today is in the bond market – investors should prepare for an investment experience that is completely different than their expectations.

In this issue of the IceCap Global Outlook, we explore major investment markets and using music from the legendary 1980s rock band – The Clash, help guide you along the way to a better understanding of where market risk truly lies.

Read PDF here: IceCap Global Market Outlook

If you’re looking for action, the commodities sector has traditionally been a good place to find it.

With wild price swings, massive up-cycles, exciting resource discoveries, and extreme weather events all playing into things, there’s usually never a dull day in the sector. That being said, it’s hard to remember a more lackluster period for commodities than in the last couple of years.

For commodity bulls, the good news is that the sector is no longer tanking. The bad news, however, is that all the recent action has been in relatively niche sectors, as metals like cobalt, zinc, and lithium all have their day in the sun.

At the same time, the big commodities (gold, oil, copper) have all slid sideways, having yet to revisit their former periods of glory.

ARE COMMODITIES CHEAP?

From the post-crisis bottom in 2009 until today, the S&P 500 is up a staggering 215.4%.

During that same timeframe, most major commodities crashed and then went sideways. The Goldman Sachs Commodity Index (GSCI) is down roughly -31.2%, which is a strong juxtaposition to how equities have done.

This extreme divergence can be best seen in this long-term chart, which compares the two indices since 1971.

In other words: despite the lack of action in commodities that we noted earlier, the sector has never been cheaper relative to equities even going back 45 years.

That means that there could be some much-needed action soon.

COMMODITY WINNERS SO FAR

Before we highlight why commodities could still be cheap, let’s look at recent performance to get some context. Here are the commodities that have positive returns in H1 2017 so far:

Palladium is the best performer in 2017 so far, and it has now almost passed platinum in price. That would be the first time since 2001 that this has happened, and for the stretch of 2007-2012 it was even true that palladium traded at a $1,000 deficit to platinum.

Agricultural goods like rough rice, lean hogs, oats, and and wheat have also gotten more expensive so far this year. Meanwhile, metals like gold, copper, and silver have seen modest gains – but these are only after dismal performances from the last part of 2016.

THE LOSERS SO FAR

Here is the scoreboard for the commodities in negative territory, with the most noticeable losses in sugar and energy.

….also from Morris Hubbartt:

Long Term Outlook For Commodities

Centralized banking and all other forms of intermediary rentier skims are presented as solid. If history is any guide, these supposedly solid entities may well melt into air.

Janet Yellen’s term as Federal Reserve chair ends on February 3rd. President Trump is expected to announce the new Federal Reserve Chair very soon, perhaps even this week. He said that we’ll get to know his choice before a tour in Asia in early November. Since that has not taken place so far, we would like to prepare you for the outcomes of Trump’s possible decisions. Moreover, we will analyze which candidate would be the best for the gold market.

The list of pretenders is rather short:

- Gary Cohn;

- Kevin Warsh;

- Janet Yellen;

- John Taylor;

- Jerome Powell

We will start with Gary Cohn, as his odds are the smallest, just about 2 percent, according to PredictIt. This is because Cohn, who is the president’s chief economic adviser, has neither formal economics background nor experience in central banking. He also worked years for Goldman Sachs, making a decent fortune, which may be not welcomed in Senate, and especially not by the Democrats. Last but not least, he criticized Trump’s response to the protests in Charlottesville. It’s difficult to categorize him as hawk or dove, as very little is known about his view on monetary policy. But as he is pragmatist and stands not very far from Yellen’s stance, his choice – which is very unlikely – would not significantly affect the gold market (but there might be some volatility at the beginning until his views would become clear for the investors – and because it would surprise markets).

Kevin Warsh has greater chances – PredictIt assigns him a 11 percent probability of becoming the next Fed chair. He was an economic adviser to President George W. Bush from 2002 to 2006 and a Fed governor from 2006 to 2011, so his experience is better suited than Cohn’s. Warsh’s impact on the gold market could be significant as he is considered to be among the most hawkish of the contenders. He opposed the second round of quantitative easing, so he might try to accelerate the quantitative tightening a bit. He will also support the deregulation of the financial industry. Hence, his choice would increase the interest rates, a bearish factor for the gold prices. Indeed, when he led the polls two weeks ago, the short-term interest rates moved higher.

Janet Yellen has about 19 percent odds to be reappointed as the Fed chair. It would be in line with tradition, and we would not be surprised if Trump eventually nominates her after all this fuss. He said that he liked low interest rates, so dovish Yellen (who is actually not so dovish, given her focus on tightening) could be fine. However, Yellen’s Democratic views, opposition to less discretionary monetary policy and far-reaching deregulation of the financial sector might be serious obstacles to her being picked. Her choice would not shake the gold market, as it would keep the status quo. And from the long-term point of view, Yellen should be, well, neutral for the yellow metal, which could remain in the sideways trend (big price swings could still happen, but gold would not be likely to stay away from the current price levels for long). As the chart below shows, the price of gold is now very close to the level seen in February 2014, when Yellen was appointed.

Chart 1: Gold prices during Yellen’s term (London P.M. Fix, monthly average).

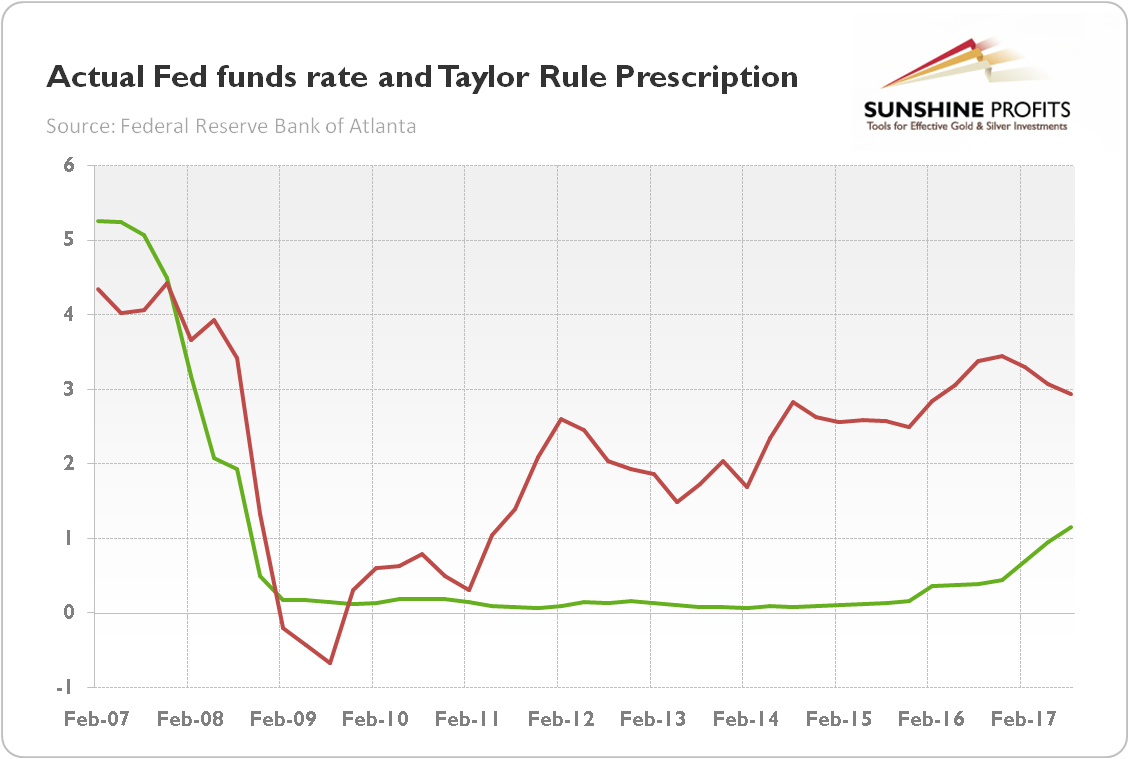

As we write these words (October 21), John Taylor’s odds are the same as Yellen’s. However, he has recently gained momentum after press reports that Stanford University economist impressed Trump and his team during a meeting at the White House. Actually, the White House spokeswoman told reporters on Friday that Trump was considering nominating John Taylor for either the Chair or the Vice Chair (and Powell for the Fed’s second top job). Taylor’s nomination would be very interesting and could have a lasting impact on the gold market. This is because he is a strong supporter of a rule-based framework for interest rates policy. Have you heard about the Taylor rule? Yup, it was created by our candidate. And the key thing is that this rule suggests that rates are still far too low. Far, far too low: according to Taylor’s model, the Fed should raise its policy rate to about 3 percent (or even higher, as there are several versions of Taylor’s rule) from 1.15 percent currently, as one can see in the chart below.

Chart 2: Actual Fed funds rate (green line) and Taylor Rule prescription (red line) over the last ten years.

We are skeptical as to whether Taylor – if nominated – would immediately hike interest rates to the level suggested by his rule. Nevertheless, his belief in a rule-based monetary policy makes him a hawk (in the eyes of markets). Hence, his nomination would support the U.S. dollar and real interest rates, which would be bad news for the gold market.

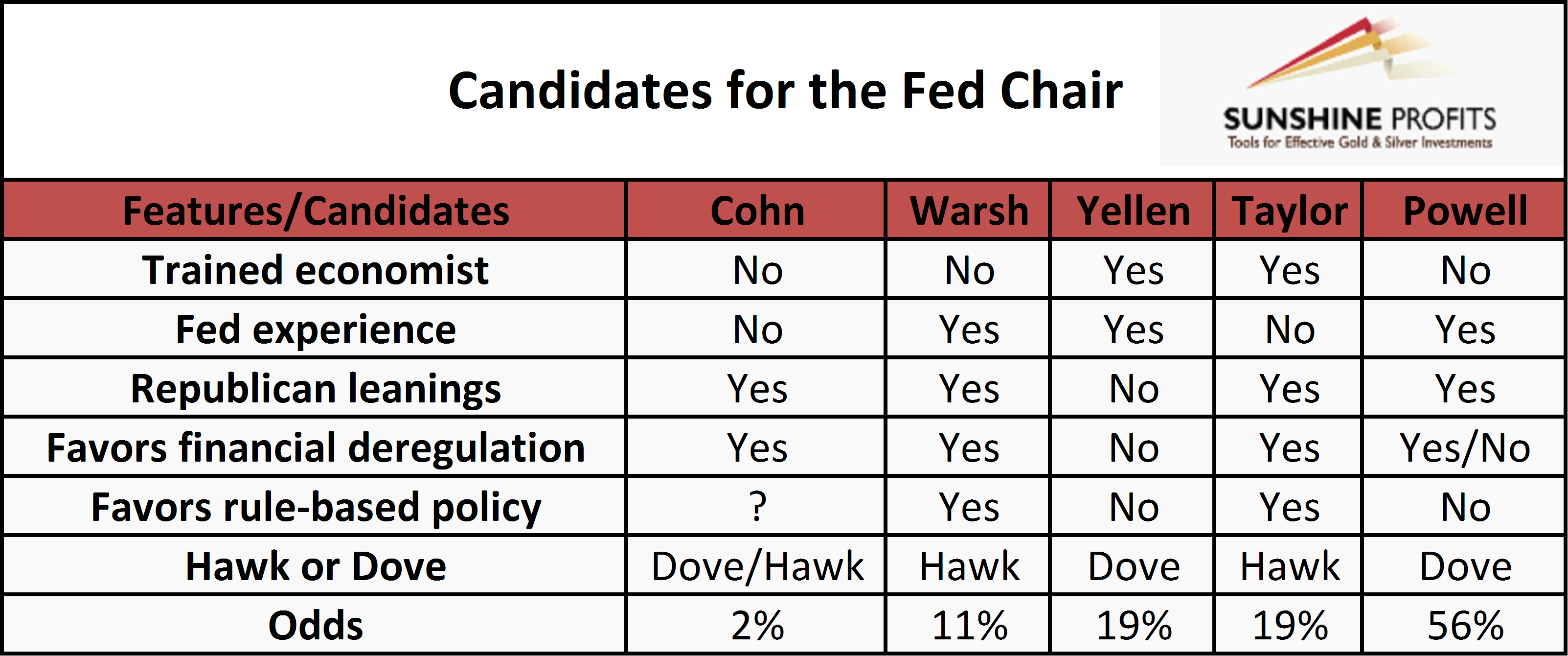

And finally, Jerome Powell – the front-runner in the race – with odds as high as 56 percent. He is the current Federal Reserve Governor, so he has needed experience and he would provide continuity. And he is allegedly favored by Treasury Secretary Steven Mnuchin. How would his nomination impact the gold market? Well, not so much. First, he leads the polls, so that choice would not surprise the market. Second, he has been in line with Yellen. Actually, he never dissented at the Fed, so his nomination would result in a de facto keeping of the status quo. The only difference is that Yellen is a Democrat, while Powell is a Republican – but it might be crucial for Trump and his team. The brief comparison between the candidates is presented in the table below.

Table 1: Comparison between candidates for the next Fed Chair.

To sum up, Trump is going to announce the next Fed chair in the coming days. Taylor and Warsh are the most hawkish (the worst candidates for gold), while Yellen and Powell the most dovish (theoretically, the best for gold, but keeping the status quo should not affect the markets significantly). Cohn is somewhere in the middle, but he is practically out of the equation. Currently, Powell decisively leads (but his nomination is not a done deal). Hence, any other choice could surprise markets and affect the price of gold. Taylor is behind him and there are rumors that these two may now rule the Fed. Indeed, it makes sense: Powell as the Fed Chair could provide continuity and would continue his gradual approach to normalizing policy, while Taylor as the Fed Vice Chair would please monetary hawks and supporters of the rule-based monetary policy among Republicans. That scenario is already priced in to a significant extent, so the initial effect on the gold market may be limited. However, in the medium-term, the Fed would be more hawkish than under Yellen and Fischer, which is negative for the gold prices at the margin.

And one final remark: it is of course important who leads the Fed. But investors should not overestimate the importance of the upcoming nomination. The FOMC is a collegial body and the next Chair will face the same dilemmas as Yellen. The Fed Chair plays as the conditions allow him (or her). It may be one of the most important jobs in the world, but even the Fed chair cannot control the economy – and the broad macroeconomic outlook will be the most important driver of the gold prices. Stay tuned!

PS. At the beginning of November, Powell’s chances increased even further. His nomination will be more dovish event than Taylor’s nomination, as Powell will continue Yellen’s gradual approach to tightening and cautious approach toward monetary policy. However, investors should not forget that John Taylor is expected to become the Fed Vice Chair. Why is it important for the gold market? Well, Powell-Taylor duo will be more hawkish than Yellen-Fischer, which is not good news for the yellow metal.

If you enjoyed the above analysis and would you like to know more about the impact of the changes in the Fed’s policy on the gold market, we invite you to read the November Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It’s free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron, Ph.D.

Man, the S&P 500 is on a roll. It’s up 14.2% this year so far. But you know what’s doing even better? Copper! Just look at this chart.

Copper’s up 27% so far this year. Wow!

Prices are up because demand for copper is red-hot. And global copper demand is led by China. China’s copper demand is projected to increase 3.1% this year alone. That leads the 2.5% rise in global copper demand.

In fact, on Monday, Goldman Sachs raised its 2018 price target for copper by 28%. The bank now expects a global copper deficit of 130,000 tons in 2018.

Here’s where it gets really interesting. Copper is said to have “Ph.D. in economics.” We call the metal “Doctor Copper” because it takes the pulse of the global economy.

The Pulse of a Megatrend

What this pulse might be measuring now is a megatrend — the big shift to electric vehicles.

See, there’s no copper in lithium-ion batteries. But there’s a heck of a lot more wiring in electric cars. In fact, an electric car can have three to four times the total electric wiring of a car running on an internal combustion engine (ICE).

And China’s government has mandated that one out of every five cars sold in the country be “new energy vehicles,” or NEVs, by 2025. (NEV is China’s category for pure electric and plug-in hybrid electric cars.)

Estimates are that 35 million vehicles will be sold in China by 2025. That’s up from 28 million last year. So we’re talking about 7 million NEV cars. That’s up from 500,000 this year. And only 295,000 of those are fully electric.

A Copper-plated Bombshell

And here’s the copper-plated bombshell. Those surging estimates may be too low.

I’m not talking about the fact that the growth of electric cars has exceeded even the wildest estimates so far. Though sure, there’s that.

I’m talking about the fact that the chairman of China’s leading seller of electric vehicles, BYD Co. (OTC Pink: BYDDF), let slip a secret when he talked to the press last week.

What, you’ve never heard of BYD? Well, you know who has heard of it? Warren Buffett. Yep, ol’ Warren is a big investor in BYD.

Buffett first bought BYD in 2008. The stock is up 73% in 2017 alone.

Anyway, BYD Chairman Wang Chuanfu told the press that all new vehicles in China will be “electrified” by 2030.

That is WAY ahead of any previous estimates. Heck, when Great Britain and France said they will ban new gasoline and diesel cars starting in 2040, that seemed pie-in-the sky.

But if anyone would know what China’s leadership is thinking about electric cars, that would be BYD’s chairman.

Could China have all its new cars electrified in some way by 2030? Experts say yes. They say that if anyone can do it, China can.

Put the Pedal to This Metal to Profit

What’s that going to do to copper demand?

I’d say it will shift into higher gear.

You can play this through the iPath Bloomberg Copper Subindex Total Return ETN (NYSE: JJC). It tracks copper nicely.

Or you could buy up-and-coming copper miners that are leveraged to the metal. Just do your due diligence before you buy anything.

We’re on the highway to this megatrend. The future for electric vehicles is wide open, and China is putting the pedal to the metal.

Make sure you’re along for this profitable ride.

All the best,

Sean Brodrick

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair