Stocks & Equities

One of the fascinating things about financial bubbles is how they transform great companies into screaming short sale candidates. Put another way, bear markets tend to throw even the prettiest babies out with the bathwater.

Here, for instance, is what happened to Cisco Systems, the dominant maker of networking gear (the devices that run the Internet) when the 1990s tech stock bubble burst, bankrupting many of its customers and causing its earnings to miss expectations. Its stock fell by more than three-fourths and those who had bought it during the previous year’s euphoria got hosed.

Cisco recovered, as great companies do, and continues to lead its part of the tech world. Current market cap: $160 billion.

And here’s Bank of America, which was a rock-solid dividend paying machine during the 2000s housing bubble – until the bubble burst and everyone defaulted on their mortgages. B of A stock fell by 90% and it stopped paying dividends, leaving its (mostly retiree) shareholders with massive capital losses and zero current income.

It too subsequently recovered and, along with Goldman, Morgan and its other money center bank peers, is now back to manipulating markets with impunity and paying rich dividends. Its market value is a little north of $270 billion.

Which brings us to the current bubble, bigger and broader than its predecessors and so – presumably – full of more great companies about to morph into life-changing shorts. Consider Tesla:

You have to love this company. Founded and run by Elon Musk, who inspired the Tony Stark character in Iron Man, it’s a leading maker of electric cars (which are both insanely fun to drive and the solution to the oil part of the fossil fuels dilemma) and solar panels (solution to the coal part of fossil fuels). So it’s about as cool as a company can be.

But after rising by more than 1000% in the past five years it now trades at nearly 6x sales – an extremely rich multiple for an established company – and is having some dramatic production problems with its newest models:

Tesla: Model 3 production problems prompt electric Semi delay

(Green Car Reports) – Tesla’s aggressive goals for Model 3 production have run into a series of setbacks, and the knock-on effect spilling over into the company’s planned electric semi truck debut, which has again been pushed back from its overdue September launch.

Elon Musk announced the later, November 16 unveil date for Tesla Semi via Twitter, while blaming both “Model 3 bottlenecks” and the ongoing humanitarian situation in Puerto Rico for the delay.

Earlier this year, Tesla announced plans to produce up to 5,000 Model 3s per month by the end of 2017, though the announcement was met with skepticism at the time.

A report last week by The Wall Street Journal revealed the company is producing major components of the car by hand, and confirmed production is falling well short the stated goals.

Though Tesla claims the report overstates the extent of the problems facing the factory, Musk did admit on twitter that the Model 3 is “deep in production hell.”

Between the continued production difficulties and Tesla’s efforts to send battery packs to Puerto Rico, the company decided to “recalibrate” the timing for both Model 3 production and the truck’s official debut.

To sum up, Tesla is facing a combination of richly-valued stock, overvalued stock market, and failure to meet its goals for this and presumably the next couple of quarters. So it fits the profile of the great company with internal and external problems that make its stock price hard to justify.

Will it (and its Big Tech peers) be the next Big Short? That probably depends on when the current bubble bursts and whether governments this time around respond by directly buying large cap stocks. Those things are unknowable, but right now the shorts have a lot of data points on their side.

Full disclosure: Various members of the DollarCollapse staff are looking hard at shorting Tesla.

When I talk about Indians’ well-known affinity for gold, I tend to focus on Diwali and the wedding season late in the year. Giving gifts of beautiful gold jewelry during these festivals is considered auspicious in India, and historically we’ve been able to count on prices being supported by increased demand.

When I talk about Indians’ well-known affinity for gold, I tend to focus on Diwali and the wedding season late in the year. Giving gifts of beautiful gold jewelry during these festivals is considered auspicious in India, and historically we’ve been able to count on prices being supported by increased demand.

Another holiday that triggers gold’s Love Trade is Dussehra, which fell on September 30 this year. Thanks to Dussehra, India’s gold imports rose an incredible 31 percent in September compared to the same month last year, according to GFMS data. The country brought in 48 metric tons, equivalent to $2 billion at today’s prices.

As I’ve shared with you many times before, Indians have long valued gold not only for its beauty and durability but also as financial security. Indian households have the largest private gold holdings in the world, standing at an estimated 24,000 metric tons. That figure surpasses the combined official gold reserves of the United States, Germany, Italy, France, China and Russia.

A New Global Leader in Gold Investing?

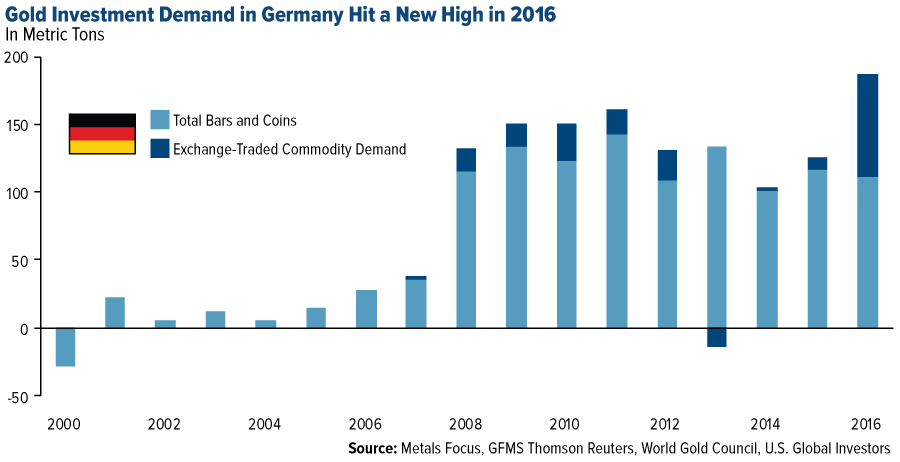

But as attracted to gold as Indians are, they weren’t the world’s biggest investors in the yellow metal last year, and neither were the Chinese. According to a new report from the World Gold Council (WGC), that title shifted hands to Germany in 2016, with investors there ploughing as much as $8 billion into gold coins, bars and exchange-traded commodities (ETCs). This set a new annual record for the European country.

Germany’s rise to become the world leader in gold investing is a compelling story that’s quietly been developing for the past 10 years. Before 2008, Germans’ investment in physical gold barely registered on anyone’s radar, with average annual demand at 17 metrics tons. The country’s first gold-backed ETC didn’t even appear on the market until 2007.

But then the financial crisis struck, setting off a series of events that ultimately pushed many Germans into seeking a more reliable store of value.

“While the world fretted about Lehman Brothers, German investors worried about the state of their own banking system,” the WGC writes. “Landesbanks, the previously stable banking partners of corporate Germany, looked wobbly. People feared for their savings.”

To stanch the bleeding, the European Central Bank (ECB) slashed interest rates. Banks began charging customers to hold their cash, and yields on German bunds dropped into negative territory.

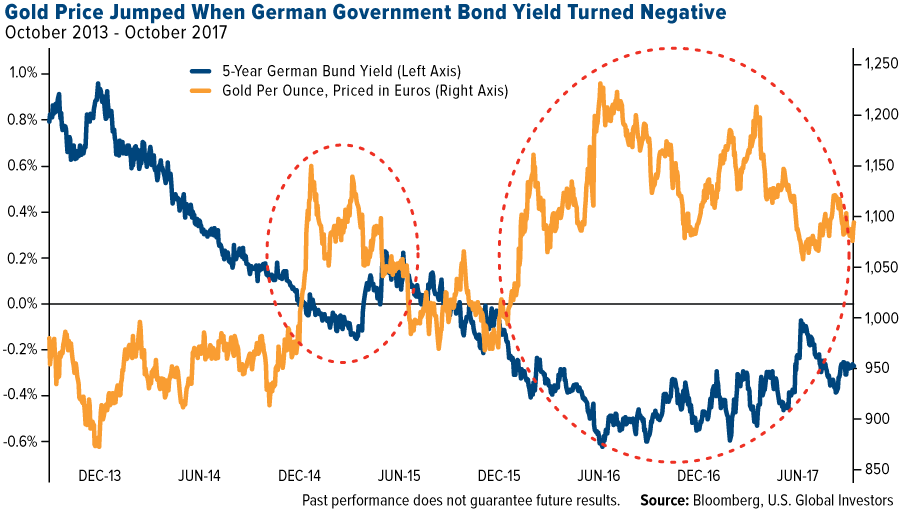

All of this had the effect of rekindling German investors’ interest in gold. As I’ve explained before, gold prices have historically surged in that country’s currency when real government bond yields turned subzero. What we saw in Germany was no exception.

Weakening Faith in Paper

As the WGC points out, Germans are acutely aware that fiat currencies can become unstable and lose massive amounts of value. In the 1920s, the German mark dipped so low, a wheelbarrow overflowing with marks wasn’t enough to buy a single loaf of bread. In the past 100 years, the country has gone through eight separate currencies.

It’s little wonder, then, that a 2016 survey found that 42 percent of Germans trust gold more than they do traditional money.

This is where Germans and Indians agree. The latter group’s faith in the banking system has similarly been eroded over the years by regime changes and corruption, and gold has been seen as real money.

It’s not just individual German investors who harbor a strong faith in gold. The Deutsche Bundesbank, Germany’s central bank, spent the past four years repatriating 674 metric tons of Cold War-era gold from New York and Paris. The operation, one of the largest and most expensive of its kind, concluded in August. Today the central bank has the second largest gold reserves in the world, following the Federal Reserve.

Room for Further Growth

With Germans’ demand for gold investment products having already reached epic proportions, what can we expect next? Will interest continue to grow, or will it recede?

Analysts with the WGC believe there is room for further growth, citing a survey that shows latent demand in Germany holding strong. Impressively, 59 percent agreed that “gold will never lose its value in the long-term.” That’s a huge number.

Regardless of whether or not investment expands in Germany, this episode shows that gold is still seen as an exceptional store of value, and trusted even more so than traditional fiat money. For gold investors, that’s good news going forward.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

In 1977 the Eagles spoke to us about “Hotel California.” Lyrics are here.

In 1977 the Eagles spoke to us about “Hotel California.” Lyrics are here.

A few lines from the song …

“On a dark desert highway, cool wind in my hair…

Up ahead in the distance I saw a shimmering light…

Then I was thinking to myself this could be Heaven or this could be Hell

Welcome to the Hotel California

Some dance to remember, some dance to forget

They’re living it up at the Hotel California

We are all just prisoners here of our own device

Relax, said the night man, We are programmed to receive,

You can check out any time you like but you can never leave.”

The lines have been rewritten to fit the Federal Reserve – the hypothetical “Hotel Marriner Eccles:”

“On a dark digital highway, QE rewarding my pals

Up ahead in the distance I saw a burning pyre of debt

I was thinking to myself this should be Heaven but it’s Hell

Welcome to the Hotel Marriner Eccles

Some pontificate to remember, some lie to forget

They’re living it up at the Hotel Marriner Eccles

We are all just prisoners here of our own device

Relax, said the chairman. We are programmed to deceive

You can check out any time you like but you can never leave”

Thanks to the efforts of the Federal Reserve:

- US national debt in 1913 was $3 billion. Today it exceeds $20,000 billion. There is no plan to reduce or eliminate debt.

- Money supply has grown similarly. Debt has grown far more rapidly than the economy which must support the debt. This model is not viable in the long-term.

- The debt will never be paid in today’s dollars, and debt cannot increase forever.

- Hence the debt will default via outright repudiation or default via inflation. Both will be painful.

- Who in their right mind believes that an economy can solve an excess debt problem with more debt? The “powers-that-be” don’t want the excess debt problem solved – THEY WANT MORE DEBT!

Like the Hotel California, the debt based currency system lives on, and we can never (without a traumatic reset) leave it.

Dishonest money created by politicians and bankers is profitable for the financial elite. It may look like heaven but it is HELL for the poor and middle class. The elite want the economic skim to continue. The rest of us must protect ourselves. Gold and silver come to mind.

The econometric models that supposedly guide the Fed are reminiscent of that edited line: “Relax, said the chairman. We are programmed to deceive. You can check out any time you like but you can never leave.”

In the financial world, where actions eventually have consequences, debt is growing explosively, fiat currencies are continually devalued and currencies are issued by insolvent central banks and insolvent governments.

There will be a reckoning. The reckoning will be less traumatic if we are prepared:

-

Understand the consequences of decades of bad monetary and fiscal policies.

-

Trust hard assets instead of promises.

-

Have gold and silver safely stored in a vault.

“We are all prisoners of our own devices.”

Gary Christenson

The Deviant Investor

In brief, six states are currently in outright depopulation. Another sixteen states are experiencing declining under 65yr/old populations only offset by surging 65+yr/old populations, and somewhere between 2/3rds and 3/4ths of all counties in America are likewise suffering one or the other.

America is in the midst of an ongoing and accelerating shift in demographics and population growth. These trends, long in place, are at a tipping point that are simultaneously driving urban economic growth (plus associated asset bubbles) and rural economic declines (plus associated asset collapses). The spin up and spin down are mutually interconnected, the result of movement in a zero sum game. But for select regions (and rural America in general), there is a surging quantity of sellers and a dwindling quantity and quality of buyers that will result in the primary asset of most Americans, their home, transitioning from an asset to an outright liability.

Many will point to record stock market valuations as an indicator of positive economic and/or business activity to refute my claims. Instead, I argue it is the Federal Reserve and federal government policies, in place as a quasi “life support” for the negatively affected regions and rural America at large, that are driving the asset valuation explosions of equities (chart below, representing all stocks publicly traded in the US) and urban housing. I will outline why the situation in the affected regions will only get worse and thus the Fed believes its hands are tied. Why any amount of normalization will only induce localized collapses across much of the nation. The total market capitalization ($ value) of the Wilshire has nearly doubled the acknowledged “bubbles” of 2000 and 2008 and is likely to continue rising further, precisely due to the worsening issues I detail below.

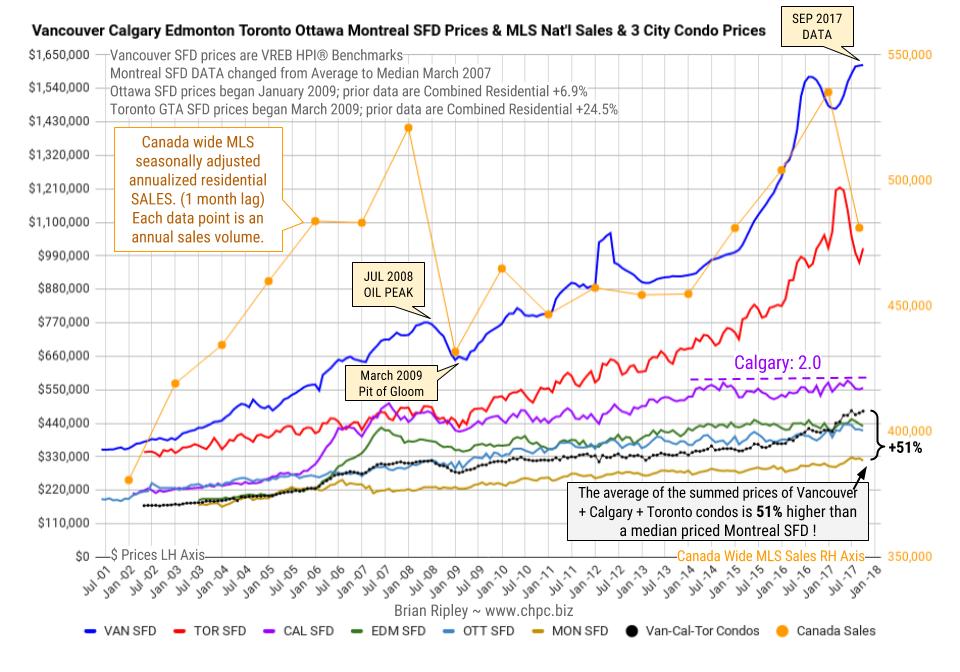

In September 2017 Toronto metro SFD prices found support after 5 months of selling below the March 2017 spike and peak price. The 2017 price gains have vanished. Vancouver prices defy gravity in all residential sectors with another HPI hat trick; FOMO and speculative pricing is still on.

also:

Brian Ripley’s Plunge-o-meter which tracks the dollar and percentage losses from the peak and projects when prices might find support. HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair