Asset protection

For the U.S. Retirement Market Ponzi Scheme to continue, there must be a new group of suckers to pay for the individuals who are receiving benefits. Without a new flow of funds, the Ponzi Scheme comes crashing down. Such was the case for the individuals who invested in the $65 billion Bernie Madoff Ponzi Scheme that came crashing down in 2008.

Interestingly, the U.S. Securities & Exchange Commission (SEC) that investigated Madoff Securities in 1999, 2000, 2004, 2005, and 2006, found no evidence of fraud or the need for legal action by the commission. The failure of the SEC to find any wrong-doing by Bernie Madoff should provide Americans with plenty of reassurance and confidence that their 401k’s are the highest quality sound investments in the market.

Regardless, the concentration in equities by young Americans reached a record high since the 2008 financial crisis. According to the most recent data put out by the Investment Company Insititute (ICI), Americans in their twenties who participated in 401k plans, 75% of the group invested more than 80% of their funds into equities in 2015 versus 48% of the group in 2007:

In just eight years, Americans in the 20’s age group invested in 401k’s, increased their equity exposure (80+%) from less than a half to three-quarters. Furthermore, those in the 30’s age group increased their equity concentration from 55% to 70% in the same period.

All this means is that younger Americans participating in the 401k Retirement Market have considerably increased their exposure to stocks while net benefits paid out have now gone into the red. I wrote about this in my article, Something Big, Bad and Ugly Is Taking Place In The U.S. Retirement Market:

As we can see in the chart, the Private Defined Contribution (DC) Plans paid out $28.7 billion more than they took in in 2014…. the last year the Investment Company Institute provided data. Simply, Private DC Plans are mostly 401K’s.

Unfortunately, the ICI only has data on 401k net benefit withdrawals up until 2014. However, young Americans invested in the 401k Market have no idea that their funds are being used to pay off those who are retired. Moreover, the record concentration of 20-30’s age group into equities hasn’t been enough to support the 401k Retirement Market as more money is going out than is coming in. That is extremely bad news.

Regrettably, nowhere in the ICI’s new report on the U.S. 401k Market do they include the data showing the net benefit withdrawals in 2014 were more than benefits paid. Instead, they included the following information in the “Key Findings” area at the beginning of the report:

This is an alarming trend. More 4o1k plan participants held equities at the end of 2015 than they did before the financial crisis in 2007. What is even more troubling is the percentage of young Americans who have “ZERO” exposure to equities in the 401k Market.

According to the ICI data, Americans in their 20’s participating in the 401k Market with zero exposure to equities fell from 19% in 2007 to 7% in 2015:

What this chart is telling us is that young American 401k plan participants with no exposure to equities (stocks) before the 2008 financial crisis were much higher than it was in 2015. While the 30’s age group change shown in the chart above change is much less, we can still see that younger Americans are putting more of their 401k funds into stocks than ever before.

This next chart from the ICI report shows the different age groups and their equity concentration in the 401k Market:

While Americans in their 50’s-60’s have decreased their (80+% in BLUE) exposure to equities since 2007, the overall trend, shown as “All” on the right-hand side of the chart, has increased from 43.5% to 47.5%. Furthermore, the 50’s-60’s age group with “zero percentage” exposure to equities (in DARK BLUE at the bottom) has decreased since 2007. Thus, older Americans participating in the 401k Market have increased their exposure to stocks when they should be more conservative.

I look at what is taking place in the U.S. Retirement Market as the final stage of the Greatest Ponzi Scheme in history. Unfortunately, Americans invested in the 401k Market have no idea they are apart of just another Bernie Madoff Ponzi Scheme, but 100 times larger. If the SEC couldn’t find any fraud in the Madoff Securities Investments via ongoing investigations between 1999-2007, what kind of reassurance does that say about protecting Americans in the U.S. Retirement Market?

The Federal Reserve and Wall Street have done an excellent job steering Americans away from sound physical investments like precious metals and into the largest Paper Retirement Market Ponzi Scheme in history. Even though Americans in the 401k Market have increased their exposure to equities, it hasn’t been enough to offset the net deficit as more money is now being paid out than is coming in.

What happens when the stock market finally cracks? Falling stock prices will motivate 401k plan participants to either cut back funds they invest or reduce their equity exposure. Thus, the collapse of the U.S. Retirement Market will be swift as Americans finally get Precious Metals Religion.

Check back for new articles and updates at the SRSrocco Report.

I have made countless posts lampooning the mainstream media and its eyeball harvesting, click baiting content. This content and especially the associated headlines (let’s recall the classic R.I.P. Bond Bull Market as Charts Say Last Gasps Have Been Taken, dated Dec. 2016 as but one example) are designed to whip up emotions, draw attention and thereby gain traffic and ad dollars (diminishing though they are these days). nftrh.com is and always will be ad-free, by the way.

So sure, the bond bull market may well have ended in the Brexit and NIRP dominated summer of anxiety (in fact I believe it did), but any good contrarian would have seen the trade setup to go bearish on bonds in the middle of that hysteria, not a half a year later when Bloomberg used Louis Yamada’s chart to make a big headline. From a post in June 2016 about the Silver/Gold ratio and the prospects for a future ‘inflation trade’ right at the height of the bond bull…

“All of this as the world sits in Treasury bonds and global NIRP garbage. Perfect. More and more it is looking like Brexit may have been an exclamation point.”

We later were compelled to do a 180° on that analysis after Trump mania drove ‘reflation’ expectations too high, aided by the likes of this sentiment setup (mark ups mine on a graphic courtesy of Sentimentrader) against bonds. This was not so surprisingly right around the time of the “R.I.P. Bond Bull Market” headline stated the obvious. Bonds have risen ever since.

‘Why drag we poor readers, with more than enough on our plates through all of this?’ you might think. Well dear reader, I am marketing to you right now. I write these articles for the purpose of getting the word out on what I think is the best market service of its kind. Marketing does not need to be a 4 letter word (mark) if the marketer is telling the truth and is 100% honest in his assertions (hint: I’ve never promised to be the best stock picker, chartist, trader or macro analyst around; I only promise to provide service to the best of my ability and let my customers form their own conclusions).

The funny thing about the financial market is that it seems so scientific, so beyond the grasp of the regular individual. It alternates over time between doing some very scary things and some very exhilarating things. What it also does is humble everybody at one time or another. All of us as market participants have been humbled. Here in this post I talked about the day of my biggest humbling.

Media headlines like the above, and the seamier end of the financial advice realm seek to give you the confidence you rightly lack (again, the market eventually eats alive anyone who is cocky or chronically over confident) by making firm statements. People think that this is a science instead of a black art. P/E ratios this and chart support that… ‘let me enlist an expert on those areas’ (fundamental and technical analysis). The stock market and financial media realm are filled with confidence men. Oh and ladies, I haven’t forgotten about you. There are plenty of shysters of the female variety out there too.

But in order to avoid becoming a perma-‘mark’, it is of utmost importance to think for yourself, to learn and to Deprogram Yourself. Sure, we can all benefit from the sound input of others, but in this confusing realm it is important to figure out who’s real and who’s Memorex (that reference may be beyond many of you younger readers, but it must have been marketing genius to still be rummaging around in my head decades later). But confidence men abound and the financial media and financial advice industries are designed to give the lowly participant firm answers in a realm that by its very nature makes us feel insecure. The mark wants to feel good and ooh, if a headline says it, it must have some validity! After all, if I just capitulate and sell bonds in December of 2016 the pain of holding them will stop… and, I won’t be alone! That’s what a herd is.

The reason for this article is that I saw this thing posted in financial social media today. I just shook my head and decided to write a post. You know the gold bug “community” * is a herd, ripe for the promotions. For privacy, I’ve blacked out the author of this goofy thing. Hear that? Time to load up on gold! It just never ends. You may ascribe this to the individual who posted it but really, how often have you seen similar things in the mainstream media or packaged as advice from supposedly serious analytical sources?

And finally, we’ve all seen the pitches that pop up out there in little ads served at every major media outlet. On Bloomberg just now… ads disguised as non-ads under the heading From The Web…

Self-made Millionaire Boils Stock Success Down to 1 Pattern

Reclusive Millionaire Warns Americans: “Get Out of Cash” –Stansberry Research

Get it? They are millionaires and you are not. Now listen up chump!

Each of the above were served by none other than Taboola, but it may well have been Outbrain or any of the other companies raking in the bucks to disguise advertisements as content on the internet.

The ads noted above are actually relatively cartoonish and easy to see for what they are by people employing functioning brain cells. But believe me when I tell you, there are plenty of associations and agreements out there between news and analysis entities that have as the primary goal your eyeballs first, and getting the content right second; a distant second.

The bottom line is there is no easy way in the financial markets and anyone who tells you they have a secret sauce should be either avoided or thoroughly vetted. In many ways the internet is still like the wild west, where anything goes.

* The term “gold community”, used so often by “Mr. Gold” James Sinclair, is a dead giveaway.

NFTRH.com and Biiwii.com

Strengths

- Typical of FOMC meeting weeks, we tend to see the precious metals take a hit. The best performing precious metal for the week was palladium, off 0.43 percent on little market moving news. Ford announced that it will add more downtime to five North American automobile plants due to a decrease in demand as inventories rise on dealer lots.

- The gold price could soon recover, says Jason Schenker, president and founder of Prestige Economics, the reason being that the Federal Reserve might raise rates less rapidly because of low U.S. inflation. “The fact that the Fed members lowered their forecast for their own future Fed funds rate indicates that the Fed may again kind of undershoot what they’re predicting they’re going to do for rates,” Schenker told Bloomberg. This could end up being neutral to bearish for the dollar, which would help support the gold price.

- Gold has begun to climb back toward $1,300 an ounce on safe-haven demand now that tensions between Washington and Pyongyang are steeply escalating. Following new U.S. sanctions against North Korea, the rogue Asian country’s leader Kim Jong-un threatened to detonate a hydrogen bomb in the middle of the Pacific Ocean. With the back-and-forth rhetoric intensifying, investors’ interest in safe havens, gold included, has been renewed.

Weaknesses

- The worst performing precious metal for the week was platinum, off 3.77 percent. Platinum prices has been out of favor for the last couple of years, recently prompting Impala Platinum, the world’s second largest producer, to propose some job cuts in South Africa that could lead to supply disruptions if labor is not on the same page. Earlier this week, gold dropped below $1,300 an ounce as risks receded of another hurricane striking the mainland U.S. and as major stock market averages continued to hit record highs on a near-daily basis. In addition, a diplomatic resolution to the nuclear standoff with North Korea appeared likely, with Secretary of State Rex Tillerson saying the U.S. is seeking a peaceful conclusion.

- The gold price responded negatively to Fed officials’ announcement that the central bank would begin unwinding its $4.5 trillion balance sheet as soon as October and also signaled additional rate hikes in 2018 following a December hike. Speaking with Bloomberg, RJO Futures’ Bob Haberkorn said that “the unwinding, coupled with the hawkish tone for December and the three hikes next year, could weigh on gold for the time being.”

- The world’s 20 leading gold producers’ share of metal output is expected to fall to its lowest level in a decade in 2019, according to Bloomberg industry analyst Eily Ong. The mining group’s share of world output fell from 47 percent in 2010 to 39 percent in 2016, and could fall even further by 2019. “As gold producers’ focus shifts from volume to profitable ounces, their existing gold mines’ life expectancies have also continued to declined,” Ong writes.

Opportunities

- Thursday and Friday of last week, Klondex Mines hosted a visit to its operations in Nevada to update the market on Hollister, Fire Creek, and Midas. We attended the site visits. Klondex is in a unique situation, having three, high-grade mines filling one centrally located mill at the Midas site. Overall, we would say investors and analysts came back with a favorable outlook. The share price outperformed the major gold equity ETF’s by over 550 basis points this week as several more positively toned analyst reports made the rounds. What we also think is noteworthy, was the quality of new people that have been attracted to Klondex, as operations have expanded, and the buy-in to the values of Klondex’s culture of safety at its operations. Prior to the trip, Klondex Mines completed the donation of the Rock Creek Lands to the Western Shoshone. For thousands of years, the Rock Creek Lands, about 20 miles northeast of Battle Mountain, Nevada, were used by the Western Shoshone. This was a goal of management and the board of Klondex to repair community relations with the Native Americans in the area which the previous owner of Hollister had ignored. Consequently, Klondex received drilling permits to now drill from the surface at Hollister to expand the exploration potential of the land package more cost effectively.

- Wesdome Gold Mines announced management changes driven by the CEO, Duncan Middlemiss, with full support of the board. The current CFO, COO and VP of Corporate Development & Exploration were all replaced immediately, which completes a realignment of staffing started by the addition of Chairman Charles Page to the board a little over a year-and-a-half ago. We see Wesdome Mines, with its Kiena Deeps exploration target, becoming more catalyst rich heading into the fourth quarter.

- With two of the bigger gold mining conferences for the year being held this week and next, there has been a swath of news releases distributed. Barsele reported a drill hole that intersected 19.75 meters grading 5.07 g/t gold, indicating continuity along a 100-meter gap between two lobes of the deposit. Jaguar Mining rose in excess of 25 percent on drill results that showed down plunge continuity of the principal ore body contained within the Banded Iron Formation. Both Golden Star and Red Pine Exploration reported double-digit grades from their respective orebodies that should lead to resource additions. In addition, Roxgold increased its production guidance for the year from 105,000-115,000ounces, up to 115,000-125,000 ounces.

Threats

- According to U.S. Trade Representative Robert Lighthizer, President Donald Trump’s chief trade negotiator, China poses an “unprecedented” threat to world trade, highlighting the country’s massive subsidies to “create national champions” and “distort markets.” Because current global rules are too inadequate to address the problem, Lighthizer adds, the president should unilaterally impose tariffs on China and any other country that practices “unfair” trade policies. Doing so, it should be noted, could lead to a U.S. trade war with China, the second-largest economy in the world, causing dramatic price swings in commodities and other raw materials.

- B&N Bank, a top-five closely held lender in Russia, has asked the country’s central bank for a bailout, reports Bloomberg, making it the second nationalization in less than a month. This highlights the complications accompanying the Bank of Russia’s efforts to clean up the financial sector after the dual economic shocks of a collapse in oil prices and international sanctions in 2014, the article continues. “The story of Otkritie, and now B&N, seriously raises questions about the actual state of private banks,” Dmitry Polevoy, chief economist for Russia at ING Groep NV in Moscow said.

- With the debt-cap suspension expiring on December 8, Bloomberg reports that there is a growing sense among investors and analysts that the Treasury will have to “slow or hold off on the inevitable.” It is unknown how the Treasury will respond to the Federal Reserve’s tapering. “The mix of maturities it decides on has far-reaching implications for the world’s biggest bond market, with the potential to alter the shape of the yield curve for years to come,” the article reads.

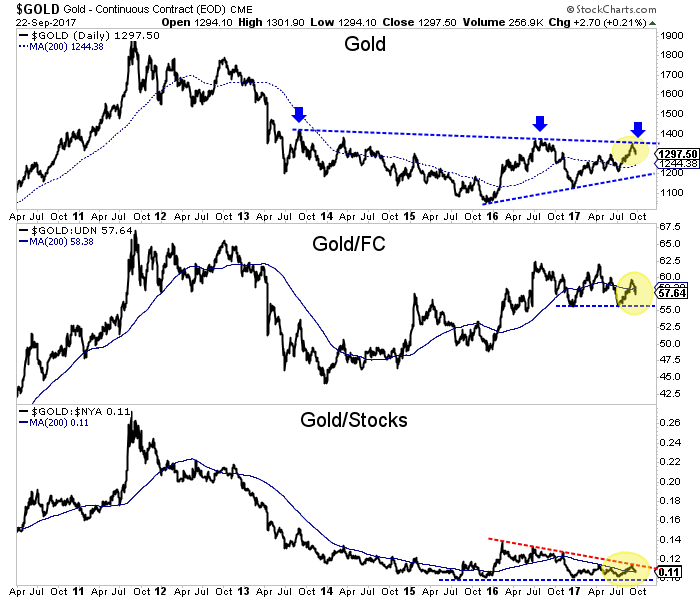

In recent weeks both metals and miners have declined somewhat sharply after reaching resistance. Gold peaked just below major resistance near $1375/oz and GDX, the biggest ETF for gold miners peaked at its October 2016 and February 2017 highs. If precious metals can break through this resistance then a major move higher would begin. However, the recent selloff, coupled with a lack of relative strength suggests the road to a breakout could lead well into 2018.

On the daily chart shown below, we can see that Gold has retreated after testing important trendline resistance. Although Gold’s long-term technical structure leans bullish, Gold is currently showing relative weakness. Gold against foreign currencies (Gold/FC) did not make a higher high and Gold/Stocks barely made a higher high. Both ratios may need to hold their blue support lines in order for Gold to remain above $1260/oz.

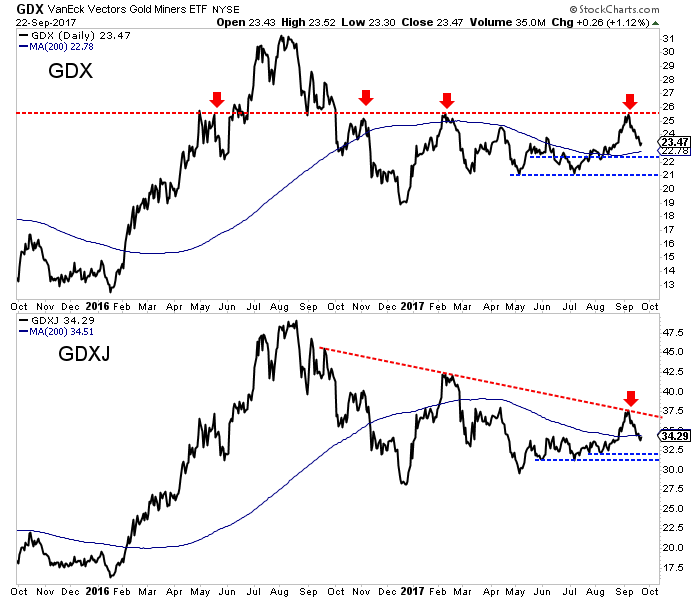

Turning to the stocks, we see that GDX, like Gold was turned back at major resistance. GDX has now tested $25-$26 three times in the past year. On a clean break above that resistance, GDX should retest its 2016 high. It has key support above $22 and at $21. GDXJ will not gain any momentum until it breaks above the September high around $37.50. It has support at $31 and $32.

There are two things that concern us with respect to the medium term outlook. The precious metals complex did not surpass its 2016 highs even though the US Dollar index made a new low. That is a negative divergence. Secondly, both miners and metals have formed a bearish reversal on the monthly charts. That is more significant than a daily or weekly reversal.

While Gold could eventually be headed for a major breakout (potentially in 2018) the road ahead could be difficult. A breakout anytime soon is unlikely. The relative weakness of the sector in the face of a weak US Dollar and the inability to hold gains into the end of the quarter suggests that Gold and gold stocks will remain mired in their long-term bottoming patterns. As we noted several weeks ago, we want to continue to accumulate the best opportunities in juniors on weakness. That is what we have done since last December and it has served us well.

Jordan Roy-Byrne CMT, MFTA

Local Mess

The Uneven Distribution of Pension Problems

Personal Storm Planning

Change Your Scenery

Chicago, Lisbon, Denver, Lugano, and Hong Kong

If you’re idly conversing with someone you don’t know well, the weather is usually a safe topic. It affects everyone in some way, so it’s a shared experience – but there’s something else, too. The weather is no one’s fault. It is what it is, so you need not worry that the other person will blame you for it. None of us can control the weather. And lately, the weather has been interesting, unless you had to live through its more extreme manifestations. Then it’s been hell. Before this week, I would’ve said that Harvey and Irma wrought devastation in Texas and Florida. But then Maria thrashed Puerto Rico and took devastation to a whole new level. I have a lot of friends who live in Puerto Rico, and I’m not sure how things are going to go for them over the next few months.

We can prepare for storms when we know they’re coming, but we can’t stop them in their tracks or change their path. That’s true for both hurricanes and the public pension problem I wrote about last week. Where pensions are concerned, we have the financial equivalents of weather satellites and hurricane hunter aircraft feeding us detailed data. We know the barometer is dropping fast. The eyewall is forming. But we can’t do much about the growing storm, except get out of the way.

Problem is, the coming pension and unfunded government liabilities storm is so big that many of us simply can’t get out of the way, at least not without great difficulty. This holds true not just for the US but for almost all of the developed world.

Financially, we’re all trapped on small, vulnerable islands. Multiple storms are coming, and evacuation is not an option. All we can do is prepare and then ride them out. But as with recent hurricanes, the brewing financial storms will have different effects from country to country and region to region.

I did a lot of thinking after we published last week’s letter – especially as I was reading your comments – and I wished I had made my warning even more alarming. Being a Prophet of Doom doesn’t come easily for me; I’m known far and wide as “the Muddle Through Guy.” I think the world economy can handle most anything and bounce back, and I still believe it will handle what’s coming over the horizon. But some parts of the economy won’t bounce at all. Quite a few people will see their life savings and ability to support themselves utterly disappear, or will be otherwise badly hurt, and through no particular fault of their own.

I mentioned last week that the next few issues of Thoughts from the Frontline would outline my vision for the next two decades. We’ll get back to that next week. But today I want to continue with the hard-hitting analysis of our public pension problems and say more about personal storm preparation. We all have some very important choices to make.

As I’ve said, the state and local pension crisis is one that we can’t just muddle through. It’s a solid wall that we’re going to run smack into.

Police officers, firefighters, teachers, and other public workers who rightly expect to receive the retirement benefits that their elected officials promised them are going to be bitterly disappointed. And the taxpayers of those jurisdictions are going to complain vigorously if their taxes are raised beyond all reason.

Pleasing both those groups is not going to be possible in this universe. Maybe in some alternate quantum alternate universe where fuzzy math works differently and lets you get away with stuff, but not here in our very real world. It just can’t happen.

So what will happen? It’s impossible to say, exactly, just as we don’t know in advance where a hurricane will make landfall: We just know enough to say the storm will be bad for whoever is caught in its path. But here’s the twist: This financial storm won’t just strike those who live on the economic margins; all of us supposedly well-protected “inland” folk are vulnerable, too.

The damage won’t be random, but neither will it be orderly or logical or just. It will be a mess. Some who made terrible decisions will come out fine. Others who did everything right will sustain severe hits. The people we ought to blame will be long out of office. Lacking scapegoats, people will invent some.

Worse, it will be a local mess. Unlike the last financial crisis where one could direct anger at faraway politicians and bankers seen only on TV, this one will play out close to home. We’ll see families forced out of homes while neighbors collect six-figure pensions. Imagine local elections that pit police officers and teachers against once-wealthy homeowners whose property values are plummeting. All will want maximum protection for themselves, at minimum risk and cost.

They can’t all win. Compromises will be the only solution – but reaching those unhappy compromises will be unbelievably ugly.

In the next few paragraphs I will illustrate the enormity of the situation with a few more details, some of which were supplied this week by readers.

The Uneven Distribution of Pension Problems

I keep using the fabulous William Gibson line that “The future is already here. It’s just unevenly distributed.” Well, paraphrasing, “The state and local pension crisis is already here; it’s just unevenly distributed.”

One reader noted that he has no sympathy for Houston when right next door, Katy, Texas, is building a $72 million football stadium for its high school.

That’s an aberration, and I might just mention that a few years back Allen, Texas, built a high school stadium for $60 million – 18,000 seats, which they fill every weekend they play. And the Eagles play really well, with several state championships in the 5A division (the biggest schools) in the last five years. There are other such examples. Sadly. I am not a fan of extravagant high school football stadiumsprograms. But then again, I am a former high school nerd turned curmudgeon.)

(Sidebar: Texas, and especially smaller towns and cities, takes its high school football and “Friday Night Lights” seriously. There is a reason that Texas high school football players are among the most highly recruited in the nation.) Though I will say that it is personally offensive that the only reason Oklahoma University can field a decent football team is because of the large number of Texas players on their team. And they have the ill grace to come in and kick UT derriere from time to time at the annual Cotton Bowl game during the Texas State Fair in October. But I’d better get back to the letter.)

Allen and Katy, coupled within contrast to Dallas and Houston, illustrate what I mean by the uneven distribution of state and local pension problems. Allen had 8,000 residents in 1980 and only 18,000 in 1990. The police department in this peaceful rural town was small in those days, and the pension benefits that built up were insignificant for a town that numbers over 100,000 today. But that’s 100,000 and growing. Allen lies in the path of massive growth spilling over from North Dallas into Plano, Frisco, McKinney, and then Allen. The city could easily double in the next 15 years. Estimates are that 10 million people will move to the North Texas area within the next 30 years, which will double or triple suburban-city and public school revenues from taxes. At times, Frisco has been the fastest growing city in America. This year, Money magazine proclaimed Allen the second-best place to live in America. Residents of Allen don’t have to worry about legacy pension issues, because the town is growing faster than whatever pension issues they have.

Ditto for Katy.

So when my reader says he doesn’t feel sorry for Houston because Katy built a $70 million high school football stadium, he needs to realize that Katy doesn’t have Houston’s legacy pension problem. Nor its high crime rate, nor all its other big-city problems. And this urban vs. suburban situation is mirrored across all the United States. The big inner cities have these monstrous legacy pension problems; and the suburbs, which have prospered on the back of the growth that has come from the big cities, feel no obligation to pitch in and help.

Residents of Houston and Dallas (and Chicago and New York and LA and on and on), on the other hand, are going to feel pain. Their taxes will keep going up, while their populations will continue to flee to the surrounding suburban areas to escape those crippling taxes and high real estate costs.

Let’s look at a few more hard facts. Pension costs already consume more than 15% of some big-city budgets, and they will be a much larger percentage in the future. That liability crowds out development and infrastructure improvement, not to mention basic services. It forces city leaders to raise taxes and impose “fees.” Let me quote from the always informative 13d letter(their emphasis):

Consider the City of Los Angeles, which Paul Hatfield, writing for City Watch L.A., recently characterized as being in a state of “virtual bankruptcy.” After a period of stability going back to 2010, violent crime grew 38% over the two-year period ending in December 2016. Citywide robberies have increased 14% since 2015. One possible reason for this uptick: the city’s population has grown while its police department has shrunk. As Hatfield explains:

The LAPD ranks have fallen below the 10,000 achieved in 2013. But the city requires a force of 12,500 to perform effectively… A key factor which limits how much can be budgeted for police services is the city’s share of pensions costs. They consume 20% of the general fund budget, up from 5% in 2002… It is difficult to increase the level of service while lugging that much baggage.

What about subway service in New York City? The system is fraying under record ridership, and trains are breaking down more frequently. There are now more than 70,000 delays every month, up from about 28,000 per month five years ago. The city’s soaring pension costs are a big factor here as well. According to a Manhattan Institute report by E.J. McMahon and Josh McGee issued in July, the city is spending over 11% of its budget on pensions. This means that since 2014, New York City has spent more on pensions that it has building and repairing schools, parks, bridges and subways, combined.

There are many large, older cities where there are more police and teachers on the pension payroll than are now working for the city. That problem is compounding, as those workers will live longer, and the pensioners typically have inflation and other escalation clauses to keep their benefits going up.

Further, most cities do not account for increases in healthcare costs (unfunded liabilities) that they will face in addition to the pensions. Candidly, this is just another “a trillion here, a trillion there” problem. Except for the fact that the trillion dollars must be dug out of state and local budgets that total only $2.5 trillion in aggregate.

Now, add in the near certainty of a recession within the next five years (and I really think sooner) and the ongoing gridlock in national politics, plus the assorted other challenges and crises we face. I won’t run down the full list – you know it well.

I’ll abbreviate since this is a family e-letter, but I just have to wonder, WTF are we going to do?

You know I don’t light my hair on fire every time someone says “Crisis!” I believe that most of the time, most of us will be fine. Together we have enough spare resources to help the people who really need it.

However, as I look out into the future I see an extraordinarily wide gap between the crisis I’ve been describing and the golden age that I truly think is coming, post-crisis. No one will find that gap easy to cross. Some of us won’t make it. Others won’t even try because they won’t see the need. They think the future will look like the past. It won’t.

Personally, I intend to make it across the gap, and I want you to get there, too. The rewards will be magnificent, but attaining them will take extensive preparation. What should you do?

I’d like to give you a 10-step checklist of all the steps you should take… but I can’t. Your situation isn’t like mine, nor is your neighbor’s situation like yours. We each have our own unique combination of talents, experience, resources, family structures, location, and more.

The best I can do is to help you see the world as I see it. And then give you some of the resources you need. Once you have them, your answers will develop naturally. You’ll be able to prepare as I would if I were in your shoes.

So how do we do that?

You’re taking step one right now by reading this letter. I hope you’re a regular reader. (I know the letter’s length got a little out of control the last couple of years. My partners and editorial team have impressed upon me the need for brevity.) So, keep reading Thoughts from the Frontlinefor my latest thoughts. And consider subscribing to the great analysis from the rest of my Mauldin Economics team – Patrick Watson, Jared Dillian, Patrick Cox, Robert Ross – we’ve got a deep bench!

Reading our analysis and recommendations helps, but it’s not enough. You have to act on it, which means you have to be confident at a deep, personal level. How do you get there?

A few months ago, my Mauldin Economics colleague Patrick Watson cited Harvard research on travel’s cognitive benefits. It seems that leaving your normal environment actually makes your brain work differently. Because you don’t know what to expect, every little act becomes a problem-solving exercise. This promotes creativity and cognitive flexibility.

With that research in mind, Patrick speculated that my extensive travel might be what sparks my energy and creativity. I don’t know for sure, but it makes a certain sort of sense. Some of my best ideas come to me while I’m on the road. Maybe seeing new places and meeting new people activates neurons I don’t normally use at home.

Getting together with people who are trying to think through the coming crisis is one of the most important things you can do. Being in a place with like-minded people who are all seeking solutions is extraordinarily productive. There is a reason the most successful investors and “family offices” regularly get together at conferences and share ideas. The open sharing and debate helps focus our critical thinking.

Now, let me get a little promotional. With what I think is justifiable reason.

Frankly, this sort of space for sharing and growing is what I try to do with my Strategic Investment Conference. I think of it as the perfect place to synchronize your unique needs and my best ideas – along with the best ideas of a unique and powerful mix of speakers. I try to get everything together in one place: You, me, and hundreds of others like us, along with my hand-selected A-list of economic, investment, and geopolitical experts. They’re the source of many of the ideas I share in these letters. At SIC, you get their latest and best thinking directly. Better yet, SIC is small enough that you can usually find the speakers in the hallway or after hours and ask them your own questions.

In addition, we have a couple of hundred “core” SIC attendees who come every year. They represent a remarkable range of talent, experience, and wisdom. Some of them really ought to be on stage. Instead, they’ll be sitting with you, and you’ll find them remarkably friendly and willing to swap ideas. We’ve seen countless business relationships form at SIC, and more happen every year.

As I think about the many challenges we’re all going to face, I want to help as many of you as possible. The Strategic Investment Conference is my best platform for doing that. So, I’m setting a personal goal to get as many first-time attendees as possible to SIC 2018. The dates are March 6–9, 2018, at the Manchester Hyatt in San Diego. It will be an amazing four days, and I want to share them with people who will appreciate them the most.

We will be opening registration in just a few weeks. We have limited space, and I don’t want to turn away our SIC veterans. That means it will be very important to register as soon as possible.

To be fair to everyone, here’s how it will work. Visit this web page and enter your name and email address. That will put you on the notification list. You aren’t committing to anything yet – we’ll alert you when registration is open and tell you how to proceed.

Note: Sign up on the notification list even if you’ve been to SIC many times. That will ensure you are among the first to know that registration is open. I don’t know how quickly people will register. Last year in Dallas we sold out, so I suggest you don’t wait too long.

Also on that page you’ll see a space where you can enter questions and comments. I really want to know why you’re coming to SIC and what you hope to learn. I’m still finalizing the agenda and speaker list, and your input will help me design a program that targets your needs.

And understand, SIC is not just about understanding the coming crisis. It’s about looking at new opportunities. The world has a fabulous abundance of opportunities for investment and diversification that are outside of the traditional money management space. If you are using a buy-and-hold, 60/40 typical portfolio as your basic investment approach, it is my personal opinion that you are not going to be happy a few years down the road. You really, really need to understand that past performance of the markets (for the last 70 years) will not be indicative of future results. The world is going to change in fundamental ways that we can’t predict but can prepare for. We are going to need to make course corrections and adapt on the fly. If you or your investment advisor can’t do that today, you need to rethink how you’re approaching your future.

Having a secure shelter doesn’t make storms any less dangerous, but it does make them less dangerous to you. Every week you put off preparing, you are running out of time to build and stock that shelter.

When I was a kid, there was a tornado shelter next door, where the local neighborhood came together when the siren sounded. We lived in Tornado Alley. I distinctly remember looking up at the sky in Bridgeport, Texas, and seeing two tornadoes, not just one. At nine years old, I wanted to stay and watch. I was completely fascinated! My mother wisely hauled me off to the shelter.

What I’m telling you is that the Great Reset is going to make the recent Great Recession look like a volatility picnic. Add in massive technological and demographic shifts. And the future of work? There’s another vast, turbulent, murky cloud right up ahead.

But let me make this emphatic point: The world is not coming to an end. It is simply changing faster and in a more extreme fashion than we have seen in the past. For those who take the proper precautions, the future is going to be exhilarating and highly rewarding. My personal mission is to help you earn that fabulous future for yourself.

Don’t be a nine-year-old kid, immobilized, gawking at tornadoes. Figure out how to build your own storm shelter, not just to withstand the coming crisis but to take advantage of the opportunitiesthat the crisis (and ultimately the Age of Transformation) will present.

The Strategic Investment Conference will help you with the knowledge and the motivation to take the next critical steps. I look forward to seeing you there.

Chicago, Lisbon, Denver, Lugano, and Hong Kong

I will be in Chicago the afternoon of September 26, meeting with clients and friends, and then I’ll speak at the Wisconsin Real Estate Alumni conference the morning of the 28th, before returning to Dallas that afternoon and flying with Shane to Lisbon the next day. My hosts are graciously giving us a few extra days to explore Lisbon, and Portugal is one of the last two Western European countries I have never been to. After this, only Luxembourg is left, so the next time I’m in Brussels or Amsterdam on a Sunday, I’m going to hop on a train and go have lunch in Luxembourg.

On Wednesday morning the 27th I will be on CNBC with my friend Rick Santelli. As usual, we’ll talk about whatever’s on the top of Rick’s mind at the moment. It makes for a hellaciously fun discussion.

I return to Dallas to speak at the Dallas Money Show on October 5–6. I will speak at an alternative investments conference in Denver on October 23–24 and return to Denver on November 6 and 7, speaking for the CFA Society and holding meetings. After a lot of small back-and-forth flights in November, I’ll end up in Lugano, Switzerland, right before Thanksgiving. Busy month! Then there will be a (currently) lightly scheduled December, followed by an early trip to Hong Kong in January. It looks like Lacy Hunt and his wife, JK, will join Shane and me there. Lacy and I will come back home exhausted from trying to keep up with the bundles of indefatigable energy that JK and Shane are.

Shane is in New Jersey with her son, so I am home alone “batching it” for a few days. Food preparation has been a little less extensive, shall we say, but the schedule is no less busy.

It’s hard to believe, but in less than two weeks I turn 68. I don’t feel the way my 30-year-old self thought I would at 68. I still think and breathe the future optimistically, if perhaps with a more cautious outlook; but I really do think that the world in general will Muddle Through and that you and I can thrive.

OK, it’s time to hit the send button. Have a great week. And maybe sit down with friends and talk about how they see the future and what they are doing to plan for it. Share your own ideas. Who knows, maybe you’ll end up helping each other in a big way.

Your planning to do more than Muddle Through analyst,

John Mauldin

subscribers@MauldinEconomics.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair