Bonds & Interest Rates

Dollar jumps to 2-week high as Federal Reserve says it will start asset next month

Dollar jumps to 2-week high as Federal Reserve says it will start asset next month

U.S. stock benchmarks retreated Wednesday afternoon as the Federal Reserve announced that, for the first time in nine years, it would start reducing the size of its $4.5 trillion asset portfolio starting in October.

The U.S. central bank kept interest rates unchanged, as widely expected, but said it would start to shrink its balance sheet by $10 billion a month. The start of the asset unwind also places another rate increase before the end of the year by the Fed back on the table, signaling more definitively an end to the easy-money policies in the U.S. and an unprecedented unwind of crisis-era asset purchases that had helped to buoy markets over the past decade.

During a news conference to detail its policy plans, Yellen described the unwind would be conducted “gradually and predictably.”

“Even though this is a slow and deliberate and thoughtful unwind plan, it is not without its potential to rattle markets,” said Kristina Hooper, global market strategist at Invesco.

The Dow Jones Industrial Average DJIA, -0.01% was down 41 points, or 0.2%, at 22,337, after hitting a fresh intraday record at 22,399.33.

The S&P 500 index SPX, -0.15% was down 8 points, or 0.3%, at 2,597, after briefly touching its own fresh intraday day record at 2,508.85.

The Nasdaq Composite Index COMP, -0.39% meanwhile, was down a firmer 43 points, or 0.7%, at 6,420.

Meanwhile, 10-year Treasury note yield TMUBMUSD10Y, +1.34% jumped to 2.28%, compared with 2.23% earlier in the session, with expectations for higher rates and additional monetary tightening, via the portfolio decrease, encouraging selling in government bonds, pushing yields, which move in the opposite direction to prices, higher. The dollar, which draws bidders in a higher interest-rate regime, enjoyed a fillip, up 0.7% at 92.475, based on the ICE U.S. Dollar Index DXY, +0.93% which measures the buck against a half-dozen currencies.

Read: Why stock market investors shouldn’t sweat a shrinking Fed balance sheet

The Fed kept its targeted federal-funds rate between 1% to 1.25%, and said the devastation caused by Hurricanes Harvey and Irma isn’t likely to materially alter the course of the economy over the medium term.

The Fed’s interest rate projections, known as the so-called dot plot, suggests an interest-rate hike in December and three more in 2018.

A news conference hosted by Chairwoman Janet Yellen was set for 2:30 p.m. Eastern.

Some industry participants have been describing the asset reduction as the “great unwind” and worrying that it might roil markets. “It is the start of something unknown, it is going to start jitters. It is going to make us tremble,” said John Manley, chief equity strategist at Wells Fargo Funds Management.

However, the Fed is aiming to offer as little disruption as possible, he noted.

Several central-bank officials already wanted to start winding down the Fed’s portfolio of government securities in July, but the majority wanted to hold until a later date. Traders now expect the FOMC on Wednesday to reveal details on a balance-sheet reduction that could start as early as October.

JP Morgan CEO Jamie Dimon calls Bitcoin a fraud.

JP Morgan CEO Jamie Dimon calls Bitcoin a fraud.

Bitcoins have captured the imagination of everyone. Even people who have never invested in stock markets have started talking about the crypto currency. Bitcoins are the talk of the town right from college students to diamond brokers to housewives.

If the whole world is talking about Bitcoins then how can CEO of a top notch investment bank miss it? Bitcoins crashed recently after JP Morgan Chase CEO Jamie Dimon called it a fraud.

“It’s worse than tulip bulbs. It won’t end well. Someone is going to get killed,” Dimon warned. Apart from this China also announced that it will shut down all the Bitcoin exchanges in the country.

This double whammy pushed Bitcoins from a high of 4,950$ on 2 September to a low of 2,950$ on 15 September. That’s a drop of 40% in a fortnight. Bitcoin has bounced back smartly from the lows but it’s nowhere close to the prior highs.

The price action for the last month or so has been too hot to handle for many. It’s exciting to see the price double or triple quickly. But it’s worse when it falls forty percent in a fortnight.

Following the financial crisis, the Federal Reserve purchased bonds as a way to stimulate the economy. Then Fed Chair Ben Bernanke explained the intent of this policy, known as quantitative easing, in 2010:

“Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” 1

But the Fed is now ready for a return to more normal monetary policy. At the Federal Open Market Committee (FOMC) meeting in June 2017, the Fed announced a strategy to reduce the size of its balance sheet by letting the bonds mature, a process called balance sheet normalization. And at a subsequent meeting in July, the Fed said it plans to begin this process relatively soon. Given the recent commentary from Fed officials, we expect this process to kick off at the September FOMC meeting.

It remains to be seen how this change will affect markets. Patrick Harker, president of the Federal Reserve Bank of Philadelphia, described it as the policy equivalent of watching paint dry.2 But we suspect that the effect it could have on markets may not be so boring.

The Fed grew its balance sheet by purchasing primarily U.S. Treasury bonds and mortgage-backed securities. Now, it plans for its balance sheet to decline at a rate no faster than $50 billion per month. This equates to a decline of $600 billion per year.

Growth and projected decline of the Fed’s balance sheet

Source: Federal Reserve and Columbia Threadneedle Investments as of June 30, 2017.

But what does this mean?

To understand the effects this change has on the bond market, it’s helpful to translate the $600 billion annual decline in balance sheet assets into interest rate terms. When short-term interest rates reached zero in 2008, researchers at the Federal Reserve constructed a so-called shadow rate that translated bond purchases into interest rate equivalent units.3 The Fed purchased $2.2 trillion in assets from 2009 through 2014, and research indicates that the shadow rate reached -2.81% by the time asset purchases were completed in September 2014. In other words, purchasing these assets had the same effect on markets as if they had lowered interest rates by 2.81%.

To take the analysis a step further, the Fed’s planned balance sheet decline of $600 billion would be equivalent to an increase in the Fed funds rate of 0.76% or about three hikes of a quarter-point (0.25%). Every year.

The effects are likely to be uneven across markets:

- Longer maturity U.S. Treasuries may be most at risk, particularly if supply begins to increase just as the Fed is exiting the market.

- Corporate bonds may fare better for now given strong demand from overseas. However, foreign central banks are a wildcard for the corporate market if they follow the Fed and return to normal monetary policy.

- Mortgage-backed securities (MBS) sit in the crosshairs of the Fed’s plan, but may actually be better positioned than some expect. Investors are being rewarded for taking risks in MBS more so than other sectors, and over the past five years the volume of MBS bonds has increased by less than 3% per year. This could be good news: people selling MBS won’t need to try too much harder to find new buyers to take the place of the Fed.

The bottom line

The Fed is hopeful that its balance sheet normalization plan can run on autopilot, but whether this will occur without disruption remains to be seen. The asset purchase plan was adjusted many times post-crisis, altering the size, timing, maturity and pace of asset purchases along the way. As the economy progresses, it’s likely that the asset reduction plan may have to be tweaked as well.

Download this article as a PDF

1 Bernanke, Ben, “What the Fed did and why: supporting the recovery and sustaining price stability,” Washington Post, 11/04/10

2 Harker, Patrick, “Economic Outlook: The Labor Market, Rates, and the Balance Sheet.” Market News International Connect Roundtable, 05/23/17

3 Wu, Jing Cynthia and Xia, Fan Dora, “Measuring the Macroeconomic Impact of Monetary Policy at the Zero Lower Bound,” Chicago Booth Research Paper No. 13-77, 05/18/15

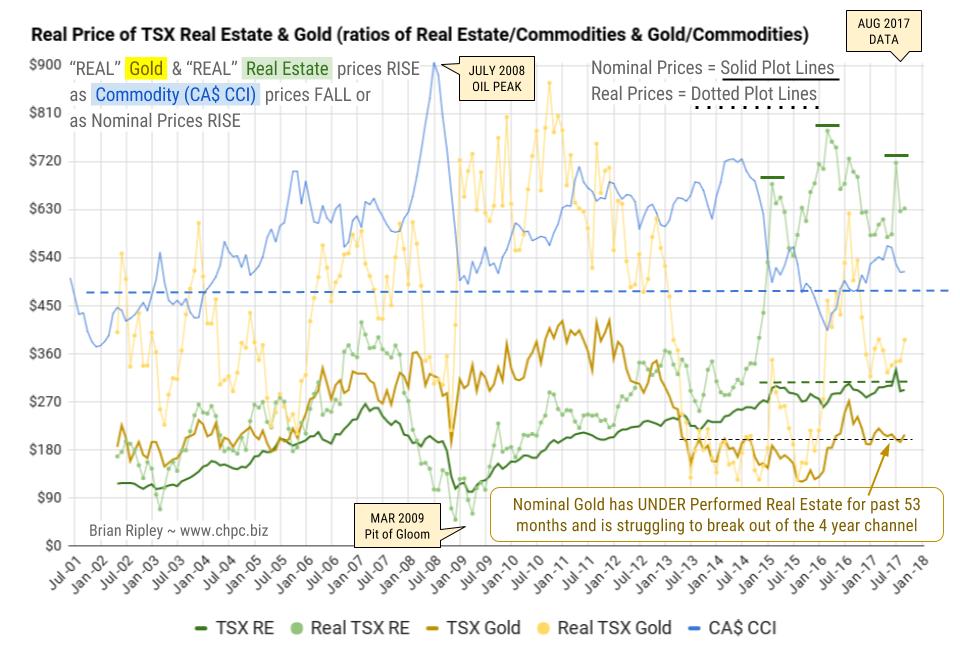

“Real” Gold (click image)

The chart above shows the “real” price of the TSX real estate index (RE/CCI green dotted plot line) and the “real” price of the TSX gold index (Gold/CCI yellow dotted plot line).

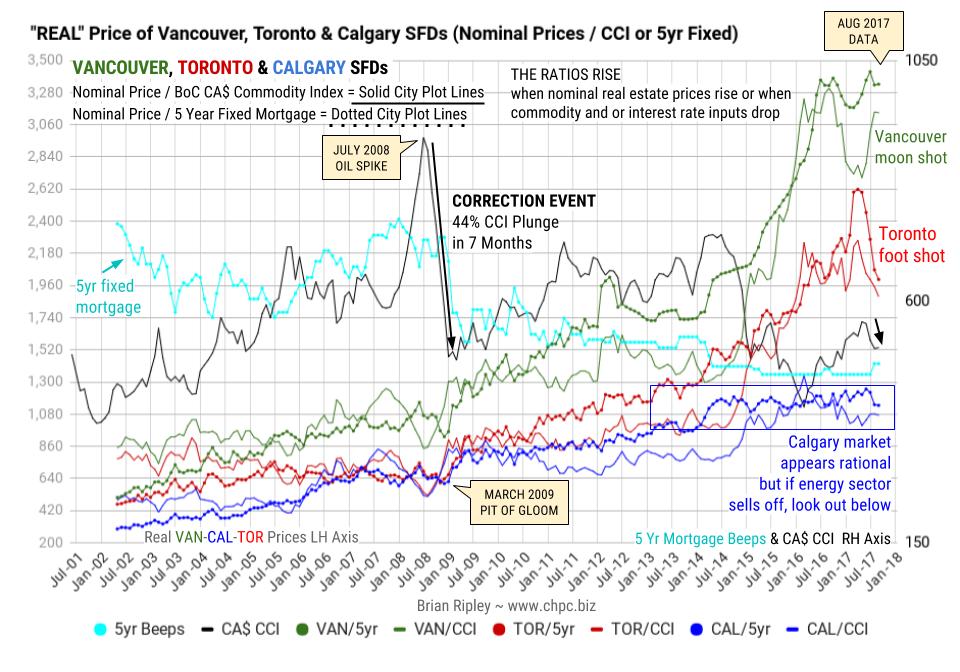

Real Housing Price (click image)

The chart above shows the “real price” of Vancouver, Toronto & Calgary SFDs when looked at from the point of view of the BoC Canadian Commodity Index (CCI) and Borrowing Costs (retail 5yr Mortgage) which are the main input costs apart from operating expenses and tax.

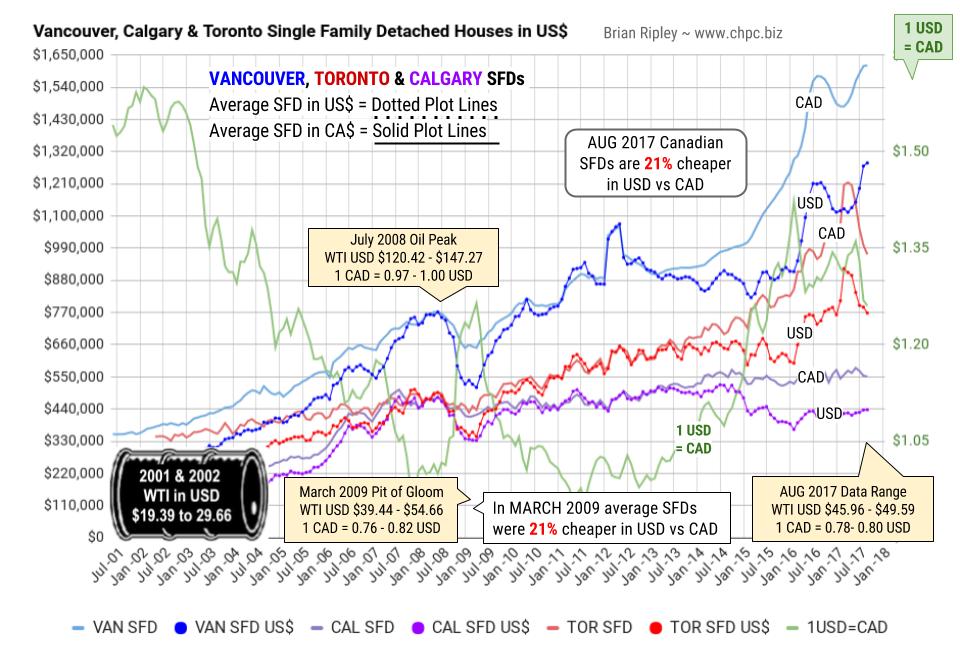

Real Housing Price (click image)

In August 2017 a single family dwelling in the hot metros of Vancouver, Calgary and Toronto is 21% cheaper if purchased in USD as opposed to CAD. They were 28% cheaper in February 2016 and at the March 2009 Pit of Gloom, prices were 21% cheaper in USD.

Also related:

The Toronto housing bubble: calm or carnage?

Recently Jamie Dimon of JP Morgan Chase made headlines by labeling Bitcoin a fraud. Whether those comments played any part in Bitcoin’s recent sell off is hard to say, but the true believers reacted with predictable outrage given that the comments came from the ultimate Wall Street insider whose financial supremacy is supposedly threatened by crypto currencies like Bitcoin.

Recently Jamie Dimon of JP Morgan Chase made headlines by labeling Bitcoin a fraud. Whether those comments played any part in Bitcoin’s recent sell off is hard to say, but the true believers reacted with predictable outrage given that the comments came from the ultimate Wall Street insider whose financial supremacy is supposedly threatened by crypto currencies like Bitcoin.

Although my critical comments on Bitcoin over the years have not received nearly as much attention, they have been just as summarily dismissed by the crypto currency crowd. But I am a well knowlibertarian and follower of the Austrian School of economics. I am not a member of the banking establishment, nor am I a fan of fiat money. I should be one of the good guys. But since I happen to own a company that sells gold, a metal that supposedly Bitcoin will soon make obsolete, the crypto crowd looks at me like a stubborn old buggy whip salesman who refuses to acknowledge that the future resides in horseless transportation.

Well, Bitcoin is not the automobile and gold is not a buggy whip. While Diamond’s comments were not 100% on the money, he is right about Bitcoin’s ultimate demise, just wrong about how it will meet its fate and why. While most fear that government will simply look to make Bitcoin illegal (which could be a possibility if Bitcoin could actually deliver on its promises), it is much more likely to die of natural causes.

The quest to replicate gold is not new. For centuries medieval alchemists tried to turn lead into gold – and now Bitcoin supporters believe they can succeed digitally where the alchemists failed chemically. But their solution will be just as fantastical.

Bitcoin advocates overlook the fact that gold did not become money overnight. It was a valuable commodity long before it became money. A money system based on gold represented a major advancement over the barter system in commerce and finance. It facilitated trade, savings, lending, insurance, and capital formation. Governments often coined gold, collected taxes in gold, and paid their bills in gold. They did this not because they preferred it, but because the people demanded it.

However modern governments have been able to subvert our momentary system by getting the people to accept paper as money rather than gold. This also did not happen overnight. It was a gradual process that began by the issuance of paper currency backed by, and redeemable in gold. Initially few people believed that the paper itself had any value. They knew that its value was derived from the gold that backed it up. However the United States eventually convinced other governments to back their currencies not with gold, but with dollars. Since the dollar was backed by gold, a currency back by dollars was de facto gold backed.

In 1971 President Nixon defaulted on that promise. But by that time, paper money had been in circulation for generations and the majority of people had forgotten that the paper simply represented claims to gold. Since prices, contracts, insurance policies bonds, etc. where already denominated in currency units rather than ounces of gold, the public accepted the switch. Though it was initially followed by substantial price increases, the transition was a success, at least from the government’s perspective.

But this nearly half century experiment in fiat money has been a disaster. Though it has certainly served governments, it has not served the public. It has led to a massive growth of government, pernicious inflation, rolling asset bubbles, booms and bust cycles, weak economic growth, and has transferred purchasing power from the poor and the middle class to financiers and speculators. It is a counterfeit of the gold-based monetary system it supplanted, and its demise now seems certain. Absurdities such as zero or negative interest rates and quantitative easing are sure signs the end is near.

There are many people who now believe that crypto currencies are the next evolution in money. But unlike the switch from gold to fiat, this swap will never take place. Although they have the virtue of arising from the private sector, crypto currencies have no actual value, and like fiat currencies derive their value solely from faith. They have no history of use, or price relationship with other commodities. Although individual crypto currencies like Bitcoin have self-imposed scarcity (which supporters claim is one of the sources of its value), the supply of virtually identical cryptos is limitless. In fact Bitcoin itself recently spun off Bitcoin Cash, which adds to the potentially infinite supply of crypto currencies. If Bitcoin Cash can be spun off, how many more Bitcoin spin off can we expect in the future?

Proponents of crypto currencies incorrectly point out that money need not have any intrinsic value. In fact they make the absurd claim that gold has no intrinsic value either. Every culture values gold for its unique decorative and ornamental value, and that’s not going to change anytime soon. Neither will industrial demand for gold in computers, electronics, airspace, medicine, or dentistry. Add that desirability to gold’s properties of scarcity, divisibility, portability, uniformity, and durability, and you have the perfect commodity for currency use. Bitcoin was created to replicate those properties, but lost is the fact that none of those properties matter without the underlying intrinsic value. Therefore Bitcoin is not digital gold, but digital fool’s gold.

Money must have a value other than its use as a medium of exchange. Like barter, it must transfer real value from one party to another. When gold is exchanged for a chair, one person gets a chair, and the other gets gold. Both parties get something of value independent of a future transaction. The fact that the party receiving gold never uses it as gold, but exchanges it for other goods or services, does not change the nature of the transaction. But if a chair is exchanged for a Bitcoin, the recipient of Bitcoin receives nothing he or anyone else can actually use. The only thing that can be done with Bitcoin is to exchange it for something else.

When gold was used as money, it was still used for other purposes, jewelry in particular. Since it is nearly certain that gold jewelry will always be desired, the owners of gold have little worry that its value will disappear. Gold does not derive its value from faith, confidence, or government decree, but from the market value of gold itself.

Even though fiat currency derives its value entirely from faith, the power of government, legal tender laws, widespread public acceptance, and tradition have provided a real basis for that faith. And since people do not want to go to jail, or have their assets seized, they need to accumulate fiat currency to pay taxes.

But Bitcoin has neither intrinsic value like gold, a history of use and public acceptance like fiat currencies, nor a government requirement that citizens pay taxes in it. There is also no historic precedent for a privately created irredeemable currency ever functioning as money.

To believe that despite these challenges Bitcoin will make the jump from a speculative, intangible financial asset to money is farcical. To do so Bitcoin proponents ignore all laws of money and economics, forget history, suspend common sense, and attack anyone who does not get it as being either biased or a fool. Fueling their arrogance is the fact that many have made paper fortunes based on greater fools making the same mistakes. But like all bubbles this one will end badly, and not only will those betting on its success lose a lot of money, but its failure will ironically make fiat currencies look good, and enhance the government’s ability to further discredit the free market.

But in their enthusiasm for Bitcoin, those looking for a true alternative to fiat currency are overlooking gold. More importantly they are overlooking the modern technology that has greatly improved gold’s utility as money. For example Goldmoney Inc. allows its customers to buy gold, store it in Brinks vaults worldwide, and use their gold as money without ever taking delivery. They can use an app on their cell phones to easily transfer any amount of gold to any third party that maintains a Goldmoney account. Or they can use a free Goldmoney debit card to quickly convert their gold to fiat, and spend the proceeds. All of the problems that Bitcoin proponents claim exist with gold, and which they believe Bitcoin has improved upon, are actually solved by Goldmoney. But the meteoric rise in value in Bitcoin over the past few years has obscured these simple facts in cloud of recently gained wealth. Unfortunately much of that wealth will soon be lost just as quickly.

Bitcoin fans like to suggest that the security and anonymity features of crypto currencies make them superior to gold. But this is a false sense of security. While governments may not be able to hack into Bitcoin’s programming, they can certainly make crypto transactions illegal. It would not be hard for the IRS to determine if a company is conducting business in Bitcoin. Just one vote in Congress could force all crypto currencies into the black market where it will never make a major impact on the broader economy. Bitcoin proponents also claim that gold is less efficient because of the risks and fees associated with third party storage, problems that the cryptos don’t face. But these hurdles are far less onerous than what they would have you believe. Brinks, the storage firm that has contracted with Goldmoney has been storing gold for more than 150 years, and no clients have ever lost a single ounce. The need to safely store gold has never stopped it from functioning as money in the past, and it won’t in the future. But the reason it must be stored is that it has actual value. Bitcoin needs no storage because it has no value to store. Yet try explaining this simple fact to anyone who owns it.

********

Peter Schiff is a best-selling author and CEO of Euro Pacific Capital. See his other commentaries here

Euro Pacific Capital, Inc. archives and reviews outgoing and incoming email. Please click here to read our full email disclosures.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair