Stocks & Equities

3:00 Pacific. Monday September 18, 2017

DOW + 63 on 384 net advances

NASDAQ COMP + 6 on 623 net advances

SHORT TERM TREND Bullish

INTERMEDIATE TERM Bullish

STOCKS: There is not a lot to analyze about the action on Monday. We thought it might pull back a bit as a reaction to the quadruple expiration on Friday, but no such luck.

There seems to be a group of institutional investors who have missed this rally and they are in a bit of a panic mode. They feel the need to buy every dip no matter how minor. Today for instance, the S&P 500 actually went negative late in the session, but it was bought.

On a fundamental basis, there is anticipation that the recent hurricanes are going to spur buying and repair work, thus increasing corporate profits in companies like Home Depot.

GOLD: Gold was down $14. The Wall Street Journal online attributed it to strength in the greenback. I’m not sure about this. The dollar wasn’t all that strong.

CHART: Sometimes analysts can over think the markets. They forget the “ultimate indicator”. And what is that? Price itself. Just look at the chart. Is that an uptrend? It surely looks like it to me and it has been going on for almost a year. Yes, it’s overbought, but in a bull market, it can stay that way for an extended period.

BOTTOM LINE: (Trading)

Our intermediate term system is on a buy.

System 7 We are in cash. Stay there for now.

System 8 We are in cash. Stay there for now.

System 9 We are in cash.

NEWS AND FUNDAMENTALS: The Housing market index came in at 64, lower than the expected 66. On Tuesday we get housing starts.

INTERESTING STUFF: Happiness is a choice that requires effort at times.—— Aeschylus

TORONTO EXCHANGE: Toronto was up 64.

BONDS: Bonds resumed their decline.

THE REST: The dollar had a minor bounce. Crude oil was down slightly.

Bonds –Bearish as of September 11.

U.S. dollar – Bullish as of September 13.

Euro — Bearish as of September 13.

Gold —-Bearish as of Sept. 11.

Silver—- Bearish as of Sept. 11.

Crude oil —-Bullish as of September 13.

Toronto Stock Exchange—- Bearish as of June 14, 2017.

We are on a long term buy signal for the markets of the U.S., Canada, Britain, Germany and France.

Monetary conditions (+2 means the Fed is actively dropping rates; +1 means a bias toward easing. 0 means neutral, -1 means a bias toward tightening, -2 means actively raising rates). RSI (30 or below is oversold, 80 or above is overbought). McClellan Oscillator ( minus 100 is oversold. Plus 100 is overbought). Composite Gauge (5 or below is negative, 13 or above is positive). Composite Gauge five day m.a. (8.0 or below is overbought. 13.0 or above is oversold). CBOE Put Call Ratio ( .80 or below is a negative. 1.00 or above is a positive). Volatility Index, VIX (low teens bearish, high twenties bullish), VIX % single day change. + 5 or greater bullish. -5 or less, bearish. VIX % change 5 day m.a. +3.0 or above bullish, -3.0 or below, bearish. Advances minus declines three day m.a.( +500 is bearish. – 500 is bullish). Supply Demand 5 day m.a. (.45 or below is a positive. .80 or above is a negative). Trading Index (TRIN) 1.40 or above bullish. No level for bearish.

No guarantees are made. Traders can and do lose money. The publisher may take positions in recommended securities.

|

The Bank of Canada announced another rate hike to the overnight lending rate (which is what the banks base their prime rate on) again by .25%, going to 1%. Subsequently, the banks moved up .25% as well. The reason for the move was impressive growth that was nearly triple the previous quarters’. After the previous rate hike earlier in the year, Stephen Poloz put the country on notice that they may be raising again during 2017 and with strong data in July and August, they decided to hike the rate. Now, this is in general good news for Canadians. It means that most provinces are not in a recession (with AB finally climbing out of the hole) with strong economic growth almost across the board. Keep in mind too that the reason for the rate decreases in 2015 was primarily due to oil price concerns, and with AB in the black again it was a fairly easy decision to go back to square one again. The question we’ve been getting a lot is should we lock in our variable rate mortgages? Keep in mind that fixed rates have gone up over the past few months, so you’ll likely be locking in to a rate over 3%. Many of you with variable rate mortgages will still be lower than the fixed rate you would be locking into. More importantly though, is the potential penalty to break a 5yr fixed rate mortgage compared to a variable rate mortgage. The penalty is max 3 months interest in a variable and either 3 months interest or an IRD (Interest Rate Differential) in a fixed rate. I wrote a good blog post about how the banks calculate these penalties (in an unfair way) that you can read here. We have found that currently this penalty is about 5x more expensive than the 3 month interest penalty. Recently we ran an estimation for a client who’s penalty would be $9,000 if they took a variable and between $47,000 – $54,000 to break a 5yr rate if they cancelled it in 1-2 years. WOW! Many of you are probably thinking that you won’t be breaking your mortgage. But believe it or not, 6/10 borrowers who take a 5yr mortgage break it early. That’s much higher than you would expect. Life happens. So what should you do? We are still advocating sticking with the variable. There will be ups and downs (right now is an up) but this world is still very volatile and there are still a lot of things that can happen. F |

Kyle Green

DLC Homeline Mortgages

Homeline Financial Services Inc.

Owner

Office: 604-229-5515

Toll Free: 1-888-531-8890

Fax: 1-866-551-8836

- Review & Update

- Bonds Send A Signal

- Sector & Market Analysis

Review & Update

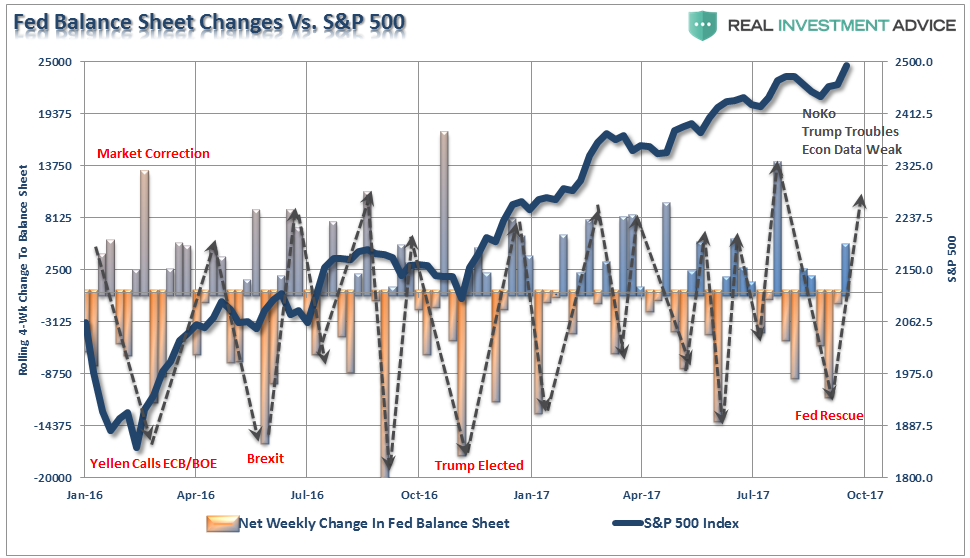

Two weeks ago, I noted:

“I have a sneaky suspicion that when I update the Fed Balance Sheet reinvestment analysis next week, shown below, we are going to find a substantial, well-timed, reinvestment by the Central Bank. Wanna bet? Well, here is the updated chart of the 4-week net change to the Fed’s balance sheet. As you can see, reinvestments have, once again, returned to the market in a very “timely” fashion. Of course, since the Fed claims they are not trying to, nor are they influenced by, the markets, this is purely coincidental. (#SarcasmAlert)”

Here is the updated chart this week as the markets broke out to new “all-time highs.” I changed the coloration to more clearly show balance sheet expansion periods more closely.

There are two things to take away from the chart.

- The current breakout of the market is likely limited given there is little room before the next down cycle in the balance sheet occurs.

- These reinvestments to “save” the markets from decline will be severely restricted IF the Federal Reserve actually proceeds with a “balance sheet reduction” program.

“That ‘gap up’ opening occurred Monday morning as ‘relief’ spread through global markets due to the reduction of geopolitical stress as the U.S. once again ‘caved’ to the threats of North Korea.”

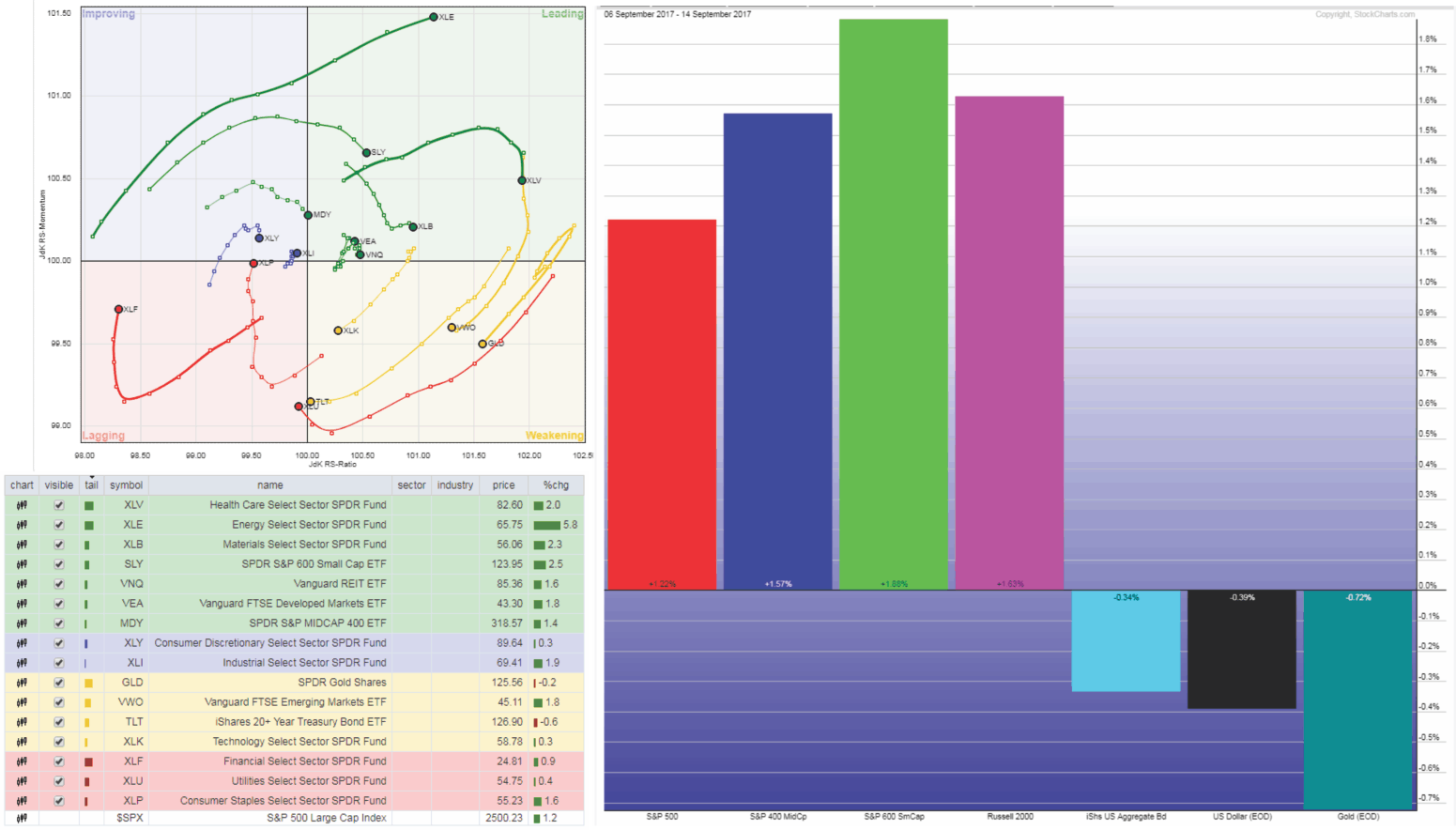

With that, and a lot of Central Bank intervention, the world breathed a sigh of relief as the previous “risk off” trade converted into a “rush for risk.” This rotation over the last 7-10 trading days out of bonds and gold back into equities can be seen in the chart below.

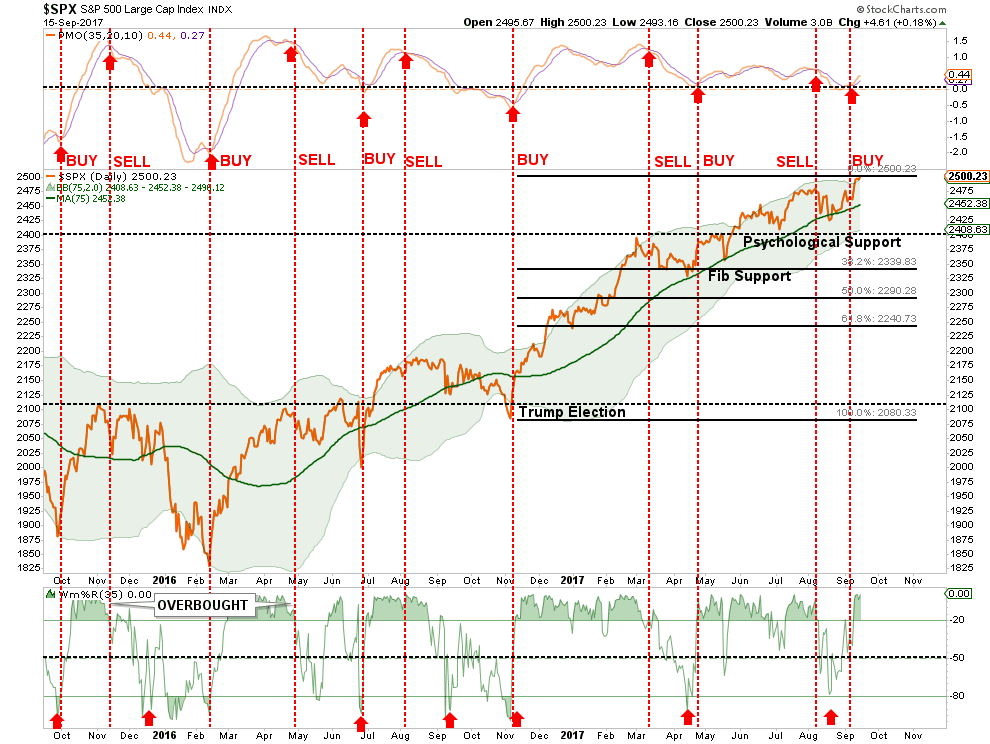

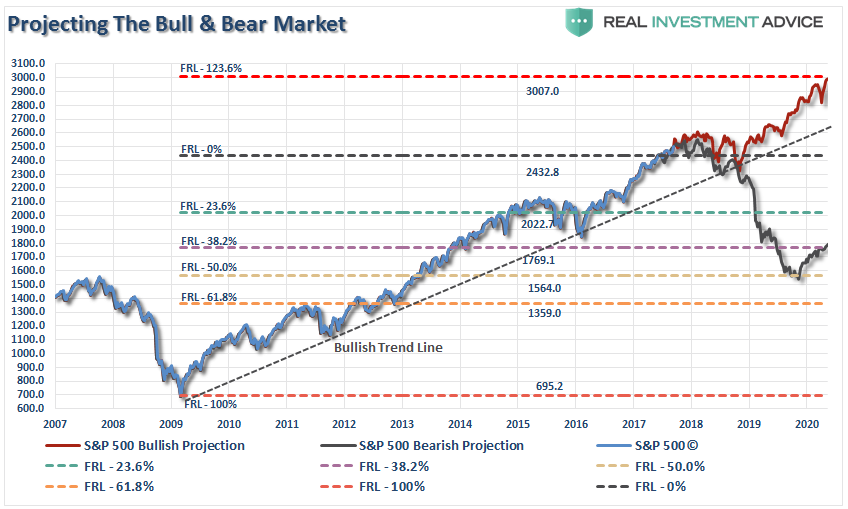

2500 or Bust!

Not surprisingly, and as I noted yesterday, the market very slightly breached 2500:

“Since the election, there has been a concerted effort to push stocks higher on the hopes of tax reform, ACA repeal, and infrastructure building which would lead to strongly improving earnings for U.S. companies. Now, eleven months later, stocks have been breaching the psychologically important levels of 2200 in December, 2300 in February and finally 2400 in May. 2500 is the next target.”

As shown below, the market is pushing a short-term “buy” signal. However, now at 2-standard deviations above the 75-dma, as seen previously, the market likely has limited upside from here. Look

Let me remind you this move is not unexpected. As I addressed back on June, 9th:

“Let me state this VERY clearly. The bullish bias is alive and well and a move to 2500 t0 3000 on the S&P 500 is viable. All that will be needed is a push through of some piece of legislative agenda from the current administration which provides a positive surprise. However, without a sharp improvement in the underlying fundamental and economic backdrop soon, the risk of something going ‘wrong’ is rising markedly. The chart below shows the Fibonacci run to 3000 if ‘everything goes right.’”

Despite the complete lack of legislative agenda, the markets did achieve its first milestone since that missive.

However, just remember, the bull-run is a one-way trip.

For now, the “bullish trend” remains intact which keeps portfolios allocated towards equities for now. BUT, and that is a “Kardashian” sized one, we do so with a “clear and present” understanding of the risk that we are undertaking. Stops have been moved up to recent support levels on all positions.

While there is some psychological support at 2400, the first level of Fibonacci support, post-election, is at 2340-ish. However, on a longer-term retracement, we are looking at a correction closer to 2000, and ultimately back to 1800ish.

The biggest concern currently is the massively elevated level of complacency. Regardless of threats of nuclear war, legislative agenda failure, missiles being launched over Japan, weak economics, and downwardly revised earnings estimates, the market has pushed higher on “hope.”

I have seen this environment before. We are in one of the longest periods on record without a 5% correction not to mention one of 10%. Volatility remains historically suppressed, and as noted on Thursday, investors are “all in the pool.”

The bulls have become completely desensitized to market risk.

I don’t know when.

Nor, do I know what will trigger it.

But a correction is coming and the following three charts are my biggest concern.

Chart 1) The current bull market cycle is already pushing one of the longest in history. With the support of global Central Banks, it could indeed become the longest. Regardless, it will end, and like all previously over-valued, over-extended, over-leveraged and overly-complacent bull cycle in history, it ends badly.

Chart 2) One of the hallmarks of a late-stage bull market cycle is the acceleration in price as investors capitulate by “jumping in” as prices accelerate. While the long-term moving averages currently suggest the bull cycle is intact, we will watch for the crossover to give us an indication of when to leave.

Chart 3) It is also not surprising to see earnings hit a “rough patch” before moving higher into the final phase of exuberance. The second downturn in earnings, particularly when sales are stagnating as they are now, tends to be the demarcation point of a repricing phase.

The ramp up in earnings in late 2016 and the first half of 2017 were a function of the rise in oil prices from the mid-30’s to the $50/bbl range. This led to a massive surge of 400% profit growth in the energy sector which boosted earnings higher for the index.

With oil prices stagnant over the last two-quarters, estimates are now being ratcheted lower as noted by FactSet recently.

If tax legislation fails to be passed this year, it is likely we will see a much more aggressive repricing of expectations in the near future.

As I stated previously:

“The question you have to ask yourself is simply this.

‘From current levels, IF everything goes right there is roughly 600 points of upside. If something goes wrong there are 900 points of downside. Are those odds I am willing to take?’

It’s easy to get wrapped up in the bullish advance, however, it is worth remembering that making up a loss of capital is not only hard to do, but the ‘time’ lost can’t be.”

At this juncture, there is a large, and inevitable, loss of capital forthcoming.

As a “Game Of Thrones Fan” would say…

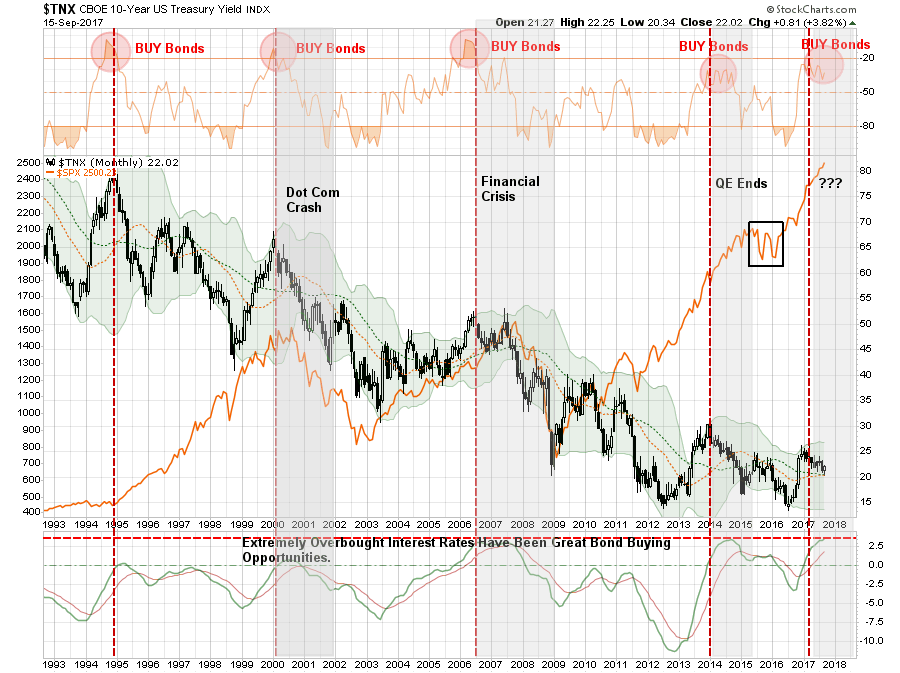

Bonds Send A Signal

Last week, I discussed the various economic indicators suggesting the “Trump Trade” has likely come to its conclusion.

Interest rates are also currently sending a signal that investors should heed.

As you know, I have been, and remain, a rampant bond bull. Since 2013, as the vast majority of mainstream analysts were touting the end of the “bond bull market,” I was aggressively buying bonds.

While we have recently pared back some of our bond holdings and took profits around 2.1% on the 10-year treasury, we remain optimistically long corporate, GNMA and municipal bonds and are looking for the next opportunity to buy more bonds. (When you headlines about the “death of the bond market,” that is your signal to buy.)

When the next recession hits the U.S. economy, rates will fall below 1% as money flows to the relative safety of bonds as equity prices lose 30-50% of their value.

More importantly, and as shown below, interest rates on a monthly basis are at levels that have been associated with significant tops in both rates and stocks.

Whether or not you agree, there is a high degree of complacency in the financial markets. The realization of “risk,” when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.

In other words, I get paid to hedge risk, lower portfolio volatility and protect capital.

Bonds aren’t dead, in fact, they are likely going to be your best investment in the not too distant future.

“I don’t know what the seven wonders of the world are, but the eighth is compound interest.” – Baron Rothschild

For what seems like decades, other countries have been tiptoeing away from their dependence on the US dollar. China, Russia, and India have cut deals in which they agree to accept each others’ currencies for bi-lateral trade while Europe, obviously, designed the euro to be a reserve asset and international medium of exchange.

For what seems like decades, other countries have been tiptoeing away from their dependence on the US dollar. China, Russia, and India have cut deals in which they agree to accept each others’ currencies for bi-lateral trade while Europe, obviously, designed the euro to be a reserve asset and international medium of exchange.

These were challenges to the dollar’s dominance, but they weren’t mortal threats.

What’s happening lately, however, is a lot more serious. It even has an ominous-sounding name: de-dollarization. Here’s an excerpt from a much longer article by “strategic risk consultant” F. William Engdahl:

Gold, Oil and De-Dollarization? Russia and China’s Extensive Gold Reserves, China Yuan Oil Market

(Global Research) – China, increasingly backed by Russia—the two great Eurasian nations—are taking decisive steps to create a very viable alternative to the tyranny of the US dollar over world trade and finance. Wall Street and Washington are not amused, but they are powerless to stop it.

So long as Washington dirty tricks and Wall Street machinations were able to create a crisis such as they did in the Eurozone in 2010 through Greece, world trading surplus countries like China, Japan and then Russia, had no practical alternative but to buy more US Government debt—Treasury securities—with the bulk of their surplus trade dollars. Washington and Wall Street could print endless volumes of dollars backed by nothing more valuable than F-16s and Abrams tanks. China, Russia and other dollar bond holders in truth financed the US wars that were aimed at them, by buying US debt. Then they had few viable alternative options.

Viable Alternative Emerges

Now, ironically, two of the foreign economies that allowed the dollar an artificial life extension beyond 1989—Russia and China—are carefully unveiling that most feared alternative, a viable, gold-backed international currency and potentially, several similar currencies that can displace the unjust hegemonic role of the dollar today.For several years both the Russian Federation and the Peoples’ Republic of China have been buying huge volumes of gold, largely to add to their central bank currency reserves which otherwise are typically in dollars or euro currencies. Until recently it was not clear quite why.

For several years it’s been known in gold markets that the largest buyers of physical gold were the central banks of China and of Russia. What was not so clear was how deep a strategy they had beyond simply creating trust in the currencies amid increasing economic sanctions and bellicose words of trade war out of Washington.

Now it’s clear why.

China and Russia, joined most likely by their major trading partner countries in the BRICS (Brazil, Russia, India, China, South Africa), as well as by their Eurasian partner countries of the Shanghai Cooperation Organization (SCO) are about to complete the working architecture of a new monetary alternative to a dollar world.

Currently, in addition to founding members China and Russia, the SCO full members include Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan, and most recently India and Pakistan. This is a population of well over 3 billion people, some 42% of the entire world population, coming together in a coherent, planned, peaceful economic and political cooperation.

Gold-Backed Silk Road

It’s clear that the economic diplomacy of China, as of Russia and her Eurasian Economic Union group of countries, is very much about realization of advanced high-speed rail, ports, energy infrastructure weaving together a vast new market that, within less than a decade at present pace, will overshadow any economic potentials in the debt-bloated economically stagnant OECD countries of the EU and North America.What until now was vitally needed, but not clear, was a strategy to get the nations of Eurasia free from the dollar and from their vulnerability to further US Treasury sanctions and financial warfare based on their dollar dependence. This is now about to happen.

At the September 5 annual BRICS Summit in Xiamen, China, Russian President Putin made a simple and very clear statement of the Russian view of the present economic world. He stated,

“Russia shares the BRICS countries’ concerns over the unfairness of the global financial and economic architecture, which does not give due regard to the growing weight of the emerging economies. We are ready to work together with our partners to promote international financial regulation reforms and to overcome the excessive domination of the limited number of reserve currencies.”

To my knowledge he has never been so explicit about currencies. Put this in context of the latest financial architecture unveiled by Beijing, and it becomes clear the world is about to enjoy new degrees of economic freedom.

China Yuan Oil Futures

According to a report in the Japan Nikkei Asian Review, China is about to launch a crude oil futures contract denominated in Chinese yuan that will be convertible into gold. This, when coupled with other moves over the past two years by China to become a viable alternative to London and New York to Shanghai, becomes really interesting.China is the world’s largest importer of oil, the vast majority of it still paid in US dollars. If the new Yuan oil futures contract gains wide acceptance, it could become the most important Asia-based crude oil benchmark, given that China is the world’s biggest oil importer. That would challenge the two Wall Street-dominated oil benchmark contracts in North Sea Brent and West Texas Intermediate oil futures that until now has given Wall Street huge hidden advantages.

That would be one more huge manipulation lever eliminated by China and its oil partners, including very specially Russia. Introduction of an oil futures contract traded in Shanghai in Yuan, which recently gained membership in the select IMF SDR group of currencies, oil futures especially when convertible into gold, could change the geopolitical balance of power dramatically away from the Atlantic world to Eurasia.

In April 2016 China made a major move to become the new center for gold exchange and the world center of gold trade, physical gold. China today is the world’s largest gold producer, far ahead of fellow BRICS member South Africa, with Russia number two.

Now to add the new oil futures contract traded in China in Yuan with the gold backing will lead to a dramatic shift by key OPEC members, even in the Middle East, to prefer gold-backed Yuan for their oil over inflated US dollars that carry a geopolitical risk as Qatar experienced following the Trump visit to Riyadh some months ago. Notably, Russian state oil giant, Rosneft just announced that Chinese state oil company, CEFC China Energy Company Ltd. Just bought a 14% share of Rosneft from Qatar. It’s all beginning to fit together into a very coherent strategy.

Meanwhile, in Latin America:

De-Dollarization Spikes – Venezuela Stops Accepting Dollars For Oil Payments

(Zero Hedge) – Did the doomsday clock on the petrodollar (and implicitly US hegemony) just tick one more minute closer to midnight?

Apparently confirming what President Maduro had warned following the recent US sanctions, The Wall Street Journal reports that Venezuela has officially stopped accepting US Dollars as payment for its crude oil exports.

As we previously noted, Venezuelan President Nicolas Maduro said last Thursday that Venezuela will be looking to “free” itself from the U.S. dollar next week. According to Reuters,

“Venezuela is going to implement a new system of international payments and will create a basket of currencies to free us from the dollar,” Maduro said in a multi-hour address to a new legislative “superbody.” He reportedly did not provide details of this new proposal.

Maduro hinted further that the South American country would look to using the yuan instead, among other currencies.

“If they pursue us with the dollar, we’ll use the Russian ruble, the yuan, yen, the Indian rupee, the euro,” Maduro also said.

The state oil company Petróleos de Venezuela SA, known as PdVSA, has told its private joint venture partners to open accounts in euros and to convert existing cash holdings into Europe’s main currency, said one project partner.

This first step towards one or more gold-backed Eurasian currencies certainly looks like a viable and — for a lot of big players out there — welcome addition to the global money stock.

Venezuela, meanwhile illustrates the growing perception of US weakness. It used to be that a small country refusing to take dollars could expect regime change in short order. Now, maybe not so much.

Combine the above with the emergence of bitcoin and its kin as the preferred monetary asset of techies and libertarians, and the monetary world suddenly looks downright multi-polar.

Storms from Nowhere

Blood from Turnips

Promises from Air

Chicago, Lisbon, Denver, Lugano, and Hong Kong

This time is different are the four most dangerous words any economist or money manager can utter. We learn new things and invent new technologies. Players come and go. But in the big picture, this time is usually not fundamentally different, because fallible humans are still in charge. (Ken Rogoff and Carmen Reinhart wrote an important book called This Time Is Different on the 260-odd times that governments have defaulted on their debts; and on each occasion, up until the moment of collapse, investors kept telling themselves “This time is different.” It never was.)

Nevertheless, I uttered those four words in last week’s letter. I stand by them, too. In the next 20 years, we’re going to see changes that humanity has never seen before, and in some cases never even imagined, and we’re going to have to change. I truly believe this. We have unleashed economic and technological forces we can observe but not entirely control.

I will defend this bold claim at greater length in my forthcoming book, The Age of Transformation.

Today we will zero in on one of those forces, which last week I called “the bubble in government promises,” which I think is arguably the biggest bubble in human history. Elected officials at all levels have promised workers they will receive pension benefits without taking the hard steps necessary to deliver on those promises. This situation will end badly and hurt many people. Unfortunately, massive snafus like this rarely hurt the politicians who made those overly optimistic promises, often years ago.

Earlier this year I called the pension mess “The Crisis We Can’t Muddle Through.” Reflecting since then, I think I was too optimistic. Simply waiting for the floodwaters to drop down to muddle-through depth won’t be enough. We face an entire new ocean, deeper and wider than we can ever cross unaided.

This year marks the first time on record that two Category 4 hurricanes have struck the US mainland in the same year. Worse, Harvey and Irma landed directly on some of our most valuable and vulnerable coastal areas. So now, in addition to all the problems that existed a month ago, the US economy has to absorb cleanup and rebuilding costs for large parts of Texas and Florida, as well as our Puerto Rico and US Virgin Islands territories.

Now then, people who live in coastal areas know full well that hurricanes happen – they know the risk, just not which hurricane season might launch a devastating storm in their direction. In a note to me about Harvey, fellow Rice University graduate Gary Haubold (1980) noted just how flawed the city’s assumptions actually were regarding what constitutes adequate preparedness. He cited this excerpt from a recent Los Angeles Times article:

The storm was unprecedented, but the city has been deceiving itself for decades about its vulnerability to flooding, said Robert Bea, a member of the National Academy of Engineering and UC Berkeley emeritus civil engineering professor who has studied hurricane risks along the Gulf Coast.

The city’s flood system is supposed to protect the public from a 100-year storm, but Bea calls that “a 100-year lie” because it is based on a rainfall total of 13 inches in 24 hours.

“That has happened more than eight times in the last 27 years,” Bea said. “It is wrong on two counts. It isn’t accurate about the past risk and it doesn’t reflect what will happen in the next 100 years.” (Source)

Anybody who lives in Houston can tell you that 13 inches in 24 hours is not all that unusual. But how do Robert Bea’s points apply to today’s topic, public pensions? Both pension plan shortfalls and hurricanes are known risks for which state and local governments must prepare. And in both instances, too much optimism and too little preparation ultimately have devastating results.

Admittedly, public pension liabilities don’t come out of nowhere the way hurricanes seem to – we know exactly where they will strike. In many cases, we know approximately when they’ll strike, too. Yet we still let our elected officials make impossible-to-fulfill promises on our behalf. The rest of us are not so different from those who built beach homes and didn’t buy hurricane or storm surge insurance. We just face a different kind of storm.

Worse, we let our government officials use predictions about future returns that are every bit as unrealistic as calling a 13-inch rain in Houston a 100-year event. And while some of us have called pension officials out, they just keep telling lies – and probably will until we reach the breaking point.

Puerto Rico is a good example. The Commonwealth was already in deep debt before Irma blew in – $123 billion worth of it. There’s simply no way the island can repay such a massive debt. Creditors can fight in the courts, but in the end you can’t squeeze money out of plantains or pineapples. Not enough money, anyway. Now add Irma damages, and the creditors have even less hope of recovering their principal, let alone interest.

Puerto Rico is presently in a new form of bankruptcy that Congress authorized last year. Court proceedings will probably drag on for years, but the final outcome isn’t in doubt. Creditors will get some scraps – at best perhaps $0.30 on the dollar, my sources say – and then move on. We’re going to find out how strong those credit insurance guarantees really are.

“That’s just Puerto Rico,” you may say if you’re a US citizen in one of the 50 states. Be very careful. Your state is probably not so much better off. In 10 years, your state may well be in the same place where Puerto Rico is now. I’d say the odds are better than even.

Are your elected leaders doing anything about this huge issue, or even talking about it? Probably not.

As it stands now, states can’t declare bankruptcy in federal courts. Letting them do so would raises thorny constitutional issues. So maybe we’ll have to call it something else, but it’s going to end the same way. Your state’s public-sector retirees will not get what they were promised, and they won’t take the outcome kindly.

Public sector bankruptcy, up to and including state-level bankruptcy, is fundamentally different from corporate bankruptcy in ways that many people haven’t considered. The pension crisis will likely expose those differences as deadly to creditors and retirees.

Say a corporation goes bankrupt. A court will take all its assets and decide how to divvy them up. The assets are easy to identify: buildings, land, intellectual property, cash, etc. The parties may argue over their value, but everyone knows what the assets are. They won’t walk away.

Not so in a public bankruptcy. The primary asset of a city, county, or state is future tax revenue from households and businesses within its boundaries. The taxpayers can walk away. Even without moving, they can bypass sales taxes by shopping elsewhere. If property taxes are too high, they can sell and move. When they take a loss on the sale, the new owner will have established a property value that yields the city far less revenue than it used to receive.

Cities and states don’t have the ability to shed their pension liabilities. They are stuck with them, even as population and property values change.

We may soon see an example of this in Houston. Here in Texas, our property taxes are very high because we have no income tax. Your tax is a percentage of your home’s taxable value. So people argue to appraisal boards that their homes are falling apart and not worth anything like the appraised value. (Then they argue the opposite when it’s time to sell the home.)

About 200 entities in Harris County can charge taxes. That includes governments from Houston to Baytown to Hedwig Village, plus 20 independent school districts.

There’s a hospital district, port authority, several college districts, the flood control district, a multitude of utility districts, and the Harris County Department of Education. Some homes may fall within 10 or more jurisdictions.

What about those thousands of flooded homes in and around Houston; how much are they worth? Right now, I’d say their value is zero in many cases. Maybe they will have some value if it’s possible to rebuild, but at the very least they ought to receive a sharp discount from the tax collector this year.

Considering how many destroyed or unlivable properties there are all over South Texas, I suspect cities and counties will lose billions in revenue even as their expenses rise. That’s a small version of what I expect as city and state pension systems all over the US finally face reality.

Here in Dallas I pay about 2.7% in property taxes. When I bought my home over four years ago, I checked our local pension and was told we were 100% funded. I even mentioned in my letter that I was rather surprised. Turns out they lied. Now, realistic assessments suggest they will have to double the municipal tax rate (yes, I said double) to be able to fund fire and police pension funds. Not a terribly popular thing to do. At some point, look for taxpayers to desert the most-indebted cities and states. Then what? I don’t know. Every solution I can imagine is ugly.

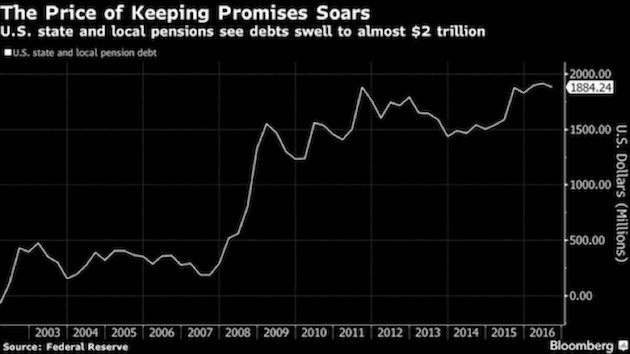

Most public pension plans are not fully funded. Earlier this year in “Disappearing Pensions” I shared this chart from my good friend Danielle DiMartino Booth:

Total unfunded liabilities in state and local pensions have roughly quintupled in the last decade. You read that right – not doubled, tripled or quadrupled: quintupled. That’s nice when it happens on a slot machine, not so nice when it’s money you owe.

You will also notice in the chart that much of that change happened in 2008. Why was that? That’s when the Fed took interest rates down to nearly zero, meaning it suddenly took more cash to fund future payments. Also, some strapped localities conserved cash by promising public workers more generous pension benefits in lieu of pay raises.

According to a 2014 Pew study, only 15 states follow policies that have funded at least 100% of their pension needs. And that estimate is based on the aggressive assumptions of pension funds that they will get their predicted rate of returns (the “discount rate”).

Kentucky, for instance, has unfunded pension liabilities of $40 billion or more. This month the state budget director notified local governments that pension costs could jump 50-60% next year. That’s due to a proposed reduction in the system’s assumed rate of return from 7.5% to 6.25% – a step in the right direction but not nearly enough.

Think about this as an investor. Do you know a way to guarantee yourself even 6.25% average annual returns for the next 10–20 years? Of you don’t. Yes, some strategies have a good shot at doing it, but there’s no guarantee.

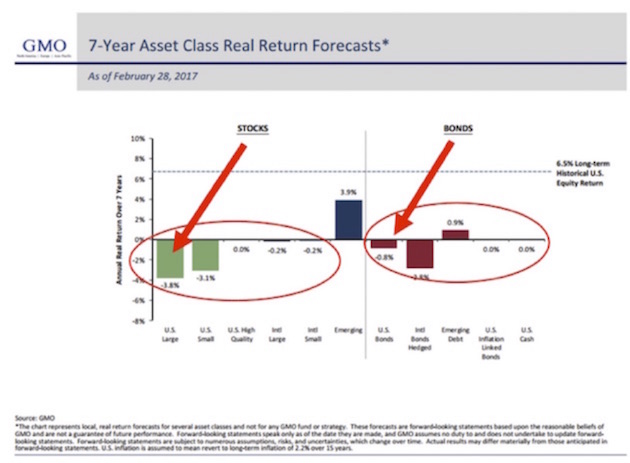

And if you believe Jeremy Grantham’s seven-year forecasts (I do: His 2009 growth forecast was spot on), then those pension funds have very little hope of getting their average 7% predicted rate of return, at least for the next seven years.

Now, here is the truth about pension liabilities. Let’s assume you have $1 billion in funding today. If you assume a 7% compound return – about the average for most pension funds – then that means in 30 years that $1 million will have grown to $8 billion (approximately). Now, what if it’s a 4% return? Using the Rule of 72, the $1 billion grows to around $3.5 billion, or less than half the future assets in 30 years if you assume 7%.

Remember that every dollar that is not funded today means that somewhere between four dollars and eight dollars will not be there in 30 years when somebody who is on a pension is expecting to get it. Worse, without proper funding, as the fund starts going negative, the funding ratio actually gets worse, sending it into a death spiral. The only way to bring it out of the spiral is with huge cuts to other needed services or with massive tax cuts to pension benefits.

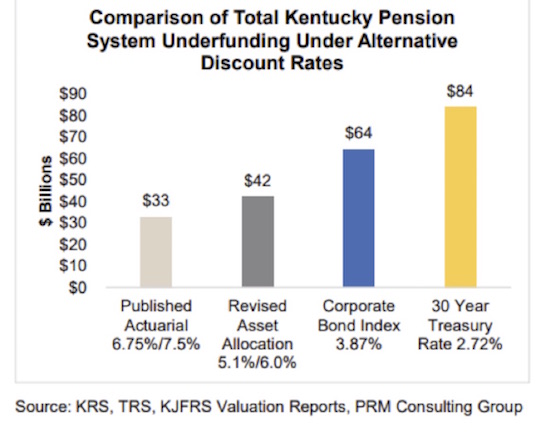

The State of Kentucky’s unusually frank report regarding the state’s public pension liability sums up that state’s plight in one chart:

The news for Kentucky retirees is quite dire, especially considering what returns on investments are realistically likely to be. But there’s a make or break point somewhere. What if pension plans must either hit that 6% average annual return for 2018–2028 or declare bankruptcy and lose it all?

That’s a much greater problem, and it’s a rough equivalent of what state pension trustees have to do. Failing to generate the target returns doesn’t reduce the liability. It just means taxpayers must make up the difference.

But wait, it gets worse. The graph we showed earlier stated that unfunded pension liabilities for state and local governments was $2 trillion. But that assumes an average 7% compound return. What if we assume 4% compound returns? Now the admitted unfunded pension liability is $4 trillion. But what if we have a recession and the stock market goes down by the past average of more than 40%? Now you have an unfunded liability in the range of $7–8 trillion.

We throw the words a trillion dollars around, not realizing how much that actually is. Combined state and local revenues for the US total around $2.6 trillion. Following the next recession (whenever that is), the unfunded pension liabilities for state and local governments will be roughly three times the revenue they are collecting today, and that’s before a recession reduces their revenues. Can you see the taxpayer stuck between a rock and a hard place? Two immovable objects meeting? The math just doesn’t work.

Pension trustees don’t face personal liability. They’re literally playing with someone else’s money. Some try very hard to be realistic and cautious. Others don’t. But even the most diligent can’t control when the next recession comes, or when the stock market will crash, leaving a gaping hole in their assets while liabilities keep right on rising.

I have had meetings with trustees of various government pensions. Many of them want to assume a more realistic discount rate, but the politicians in their state literally refuse to allow them to assume a reasonable discount rate, because owning up to reality would require them to increase their current pension funding dramatically. So they kick the can down the road.

Intentionally or not, state and local officials all over the US made pension promises that future officials can’t possibly keep. Many will be out of office when the bill comes due, protected from liability by sovereign immunity.

We are starting to see cities filing for bankruptcy. That small ripple will be a tsunami within 7–10 years.

But wait, it gets still worse. (Do you see a trend here?) Many state and local governments have actually 100% funded their pension plans. Some states and local governments have even overfunded them – assuming they get their projected returns. What that really means is that the unfunded liabilities are more concentrated, and they show up in unlikely places. You think Texas is doing well? Look at some of our cities and weep. Look, too, at other seemingly semi-prosperous cities all over the country. Do you think the suburbs of Dallas will want to see their taxes increased to help out the city? If you do, I may have a bridge to sell you – unless you would rather have oceanfront properties in Arizona.

This issue is going to set neighbor against neighbor and retirees against taxpayers. It will become one of the most heated battles of my lifetime. It will make the Trump-Clinton campaigns look like a school kids’ tiddlywinks smackdown.

I was heavily involved in politics at both the national and local levels in the 80s and 90s and much of the 2000s. Trust me, local politics is far nastier and more vicious. And there is nothing more local than police and firefighters and teachers seeing their pensions cut because the money isn’t there. Tax increases of up to 100% are going to become commonplace. But even these new revenues won’t be enough… because we will be acting with too little, too late.

This is the core problem. Our political system gives some people incentives to make unrealistic promises while also absolving them of liability for doing so. It also places the costs of those must-break promises on innocent parties, i.e. the retirees who did their jobs and rightly expect the compensation they were told they would receive.

So at its heart the pension crisis is really not a financial problem. It’s a moral and ethical problem of making and breaking promises that profoundly impact people’s lives. Our culture puts a high value on integrity: doing what you said you would do.

We take a job because the compensation package includes x, y and z. Then someone says no, we can’t give you z, so quit and go elsewhere.

The pension problem is going to get worse as more and more retirees get stuck with broken promises, and as taxpayers get handed higher and higher bills. These are irreconcilable demands in many cases. It’s not possible to keep contradictory promises.

What’s the endgame? I think much of the US will end up like Puerto Rico. But the hardship map will be more random than you can possibly imagine. Some sort of authority – whether bankruptcy courts or something else – will have to seize pension assets and figure out who gets hurt and how much. Some courts in some states will require taxes to go up. But courts don’t have taxing authority, so they can only require cities to pay, but with what money and from whom?

In many states we literally don’t have the laws and courts in place with authority to deal with this. And just try passing a law that allows for states or cities to file bankruptcy in order to get out of their pension obligations.

The struggle will get ugly, and innocent people on both sides will be hurt. We hear stories about retired police chiefs and teachers with lifetime six-digit pensions and so on. Those aberrations (if you look at the national salary picture) are a problem, but the more distressing cases are the firefighters, teachers, police officers, or humble civil servants who served the public for decades, never making much money but looking forward to a somewhat comfortable retirement. How do you tell these people that they can’t have a livable pension? We will see many human tragedies.

On the other side will be homeowners and small business owners, already struggling in a changing economy and then being told their taxes will double. This may actually happen in Dallas; and if it does, we won’t be alone for long.

The website Pension Tsunami posts scores of articles, written all across America, about pension problems. We find out today that in places like New York and Chicago and Cook County, pension funds have more retirees collecting than workers paying into the fund. There are more retired cops in New York and Chicago than there are working cops. And the numbers of retirees just keep growing. On an individual basis, it is smart for the Chicago police officer to retire as early possible, locking in benefits, go on to another job that offers more retirement benefits, and round out a career by working at least three years at a private job that qualifies the officer for Social Security. Many police and fire pensions are based on the last three years of income; so in the last three years before they retire, these diligent public servants work enormous amounts of overtime, increasing their annual pay and thus their final pension payouts.

As I’ve said, this is the crisis we can’t muddle through. While the federal government (and I realize this is economic heresy) can print money if it has to, state and local governments can’t print. They actually have to tax to pay their bills. It’s the law. It’s also an arrangement with real potential to cause political and social upheaval that Americans have not seen in decades. The storm is only beginning. Think Hurricane Harvey on steroids, but all over America. Of all the intractable economic problems I see in the future (and I have a vivid imagination), this is the most daunting.

Chicago, Lisbon, Denver, Lugano, and Hong Kong

I will be in Chicago the afternoon of August 26, meeting with clients and friends, and then I’ll speak at the Wisconsin Real Estate Alumni conference the morning of the 28th, before returning to Dallas that afternoon and flying with Shane to Lisbon the next day. My hosts are graciously giving me a few extra days to explore Lisbon, and Portugal is one of the last two Western European countries I have never been to. After this, only Luxembourg is left, so the next time I’m in Brussels or Amsterdam on a Sunday, I’m going to get on a train and go have lunch in Luxembourg.

On Wednesday morning the 27th I will be on CNBC with my friend Rick Santelli. As usual, we’ll talk about whatever’s on the top of Rick’s mind at the moment. It makes for a hellaciously fun discussion.

I return to Dallas to speak at the Dallas Money Show on October 5–6. You can click on the link for details. I will speak at an alternative investments conference in Denver on October 23–24 (details in future letters) and return to Denver on November 6 and 7, speaking for the CFA Society and holding meetings. After a lot of small back-and-forth flights in November, I’ll end up in Lugano, Switzerland, right before Thanksgiving. Busy month! Then there will be a (currently) lightly scheduled December, followed by an early trip to Hong Kong in January. It looks like Lacy Hunt and his wife, JK, will join Shane and me there. Lacy and I will come back home exhausted from trying to keep up with the bundles of indefatigable energy that JK and Shane are.

Boston was a very intriguing two full days of meetings. There is the potential to expand the services that my firms can offer readers and investors into areas that I never knew might be possible. It is truly exciting, and I hope we can pull it off.

I am off to meet with a close friend from out of town and compare notes on the world, one of my favorite things to do. I know we all have times when we wish we were being more productive, when we wondering why are we here and not moving the ball forward. But when I get to spend time with good friends, old or new, I somehow never feel that way. And while our pension systems may be going to hell in a handbasket, friendships will remain forever. You have a great week.

Your wishing I could see a better path forward analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair