Concrete steps you can take today to improve your cash flow tomorrow!

Concrete steps you can take today to improve your cash flow tomorrow!

Are you ready for what might become the most opportunistic setup we’ve seen in over a decade? Well, before we get to the guts of our incredible setup, let’s go over some other data to support our predictions – the global markets.

On May 3rd, 2017, we authored an article regarding Global Economic Shifts that were taking place as a result of Capital Migration and renewed risk factors throughout the global markets. Our hypothesis was that capital will always attempt to locate and migrate to financial environments where risk is mitigated and returns are sufficient. We consider this an active and intrinsic role of global capital – the hunt for the ability to thrive and develop success/profits.

Since this research was completed, a number of new and interesting facets have evolved. Two of the most interesting are the shifts within the Arabic nations with regards to Qatar and the almost total isolation recently enacted on this wealthy nation and the news from Europe that a number of smaller, regional banks are collapsing with broader, tangible relations to the EU banking system. This type of disruption within a financial environment (think globally) causes capital to migrate rather quickly to more stable locations for self-preservation.

China/Asian markets appear to be developing a level of “moderately healthy financial environment” in terms of global market capital migration. In the past, I would have warned that Asia/China could become a temporary safe-harbor for capital as it migrates out of riskier environments and I would still support that claim simple because China/Asia are less of a mature market compared to other. Thus, the likelihood that China/Asia could see dramatic asset revaluation or some type of unexpected market function issues is still near the top of my list. Yet, we can’t accurately predict when this will happen and until extended signs of weakness cause us to adopt a more concerned stance, we have to understand that capital will move to environments that seem suitable for success. At this time, we believe China/Asia are viewed as just that – moderately suitable for capital deployment and investment (till things change).

Asia Chart

You will see from our chart that a defined support channel is in place and resistance bands appears to be setting up near the end of June and throughout September 2017.

BRICs Chart

BRICS markets appear to have “rolled over”, as predicted, near resistance bands that indicate pricing levels may be setup for some level of correction. It is our opinion that an 8~18% correction may be near as capital will likely migrate away from perceived increased risk and towards healthier environments. This would put a downside target on this chart near $13k~$12.5k.

Europe Chart

The European markets appear to be at a critical juncture near a classic Fibonacci retracement pattern. Many people do not understand one of the basic concepts of Fibonacci theory that is; price will always attempt to develop new higher highs or lower lows. Keeping this in mind, any failure to develop higher highs in the European markets within the next 2~3 months will likely result in perceptions being that these markets are developing greater risk. Thus, capital may migrate away from the uncertainty and risk towards healthier alternatives.

The European markets chart shows clear price channels that originated near July 2016 – the date Theresa May assumed the Prime Minister role. It is interesting how the perception of an environment of strength, protection, leadership and opportunity can change the way capital migrates from different environments. In this case, the disruption in Europe with May’s election victory changed the way people saw the future opportunities in Europe.

Now, with recent elections, banking issues, further debt issues and uncertainty with leadership, we can only assume that perception will change, again, towards an environment that is more risky and unstable – prompting capital migration away from these markets.

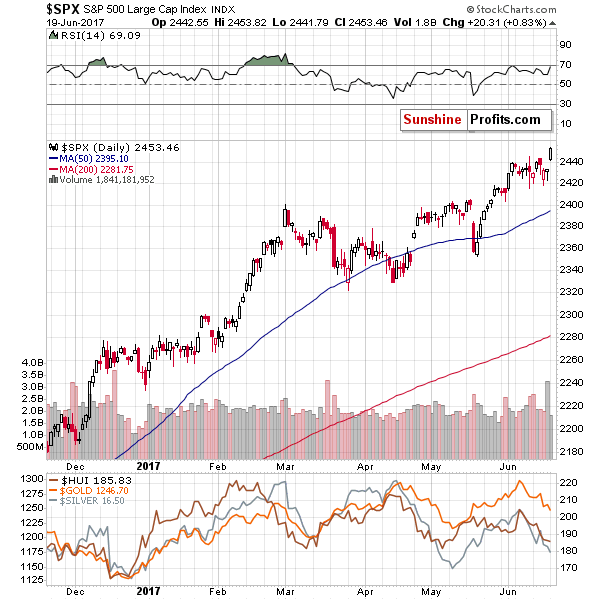

US charts

Meanwhile, on another continent… The US markets appear to be the “Garden of Eden” in terms of capital migration. It is true that the entire US/Canadian/Mexican conglomerate market is suitable and in perfect financial health, but it is also true that compared to many others, these market present the potential for the best and safest deployment of capital. The charts show that capital appreciation has been tremendous since the US Presidential Elections and may launch much higher if extended risk exists in other global markets.

Again, capital is always searching for a safe and suitable environment for deployment. Taken in global terms, there are really only two suitable locations for capital and the others are inherently more risky. These conditions may change over the next few months, but our analysis points to one critical factor that could disrupt many aspects of this global capital environment. One thing that could be related to a massively disruptive event.

768w,

768w,

We are now at the point that you have been waiting for. The incredibly disruptive and opportunistic setup that could change everything in the global markets (or so we hypothesize). Before we get to the details, we want to make certain that you understand this type of research if far from 100% guaranteed or set in stone. We develop our analysis based on a number of massively moving components within the global economy and are predicting price moves that may be weeks of month in advance. We advise you to consider this a learning experiment in the sense that there is absolutely no way we can state with 100% certainty our research/analysis or conclusions will play out exactly as we suggest. It is impossible for anyone to know what will or may happen, accurately, in the future. That is what trading is all about – making an educated guess and protecting your trade.

Well, here it is, folks.

The setup/opportunity that may turn into

the biggest move in the markets for the next century. METALS.

Think about this for just one minute. Given the knowledge that capital will migrate to sources of safety and investment return while avoiding environments that are risky. And, given that we’ve made fairly clear points that much of the global is setting up for some levels of disruption, uncertainty and greater risk – leaving only China/Asia and the US as the safe-harbor capital environments. We’ve also detailed how the China/Asia markets are setting up for disruption with technical resistance levels and exposure to other global environments. We’ve highlighted that Europe may enter a period of disruption and uncertainty with recent elections, debt, banking issues and more and illustrated that BRICs markets are rolling over as an early warning that emerging markets might contract as global capital migrates towards safer environments. This is not doom and gloom stuff, this is just what happens when markets are disrupted.

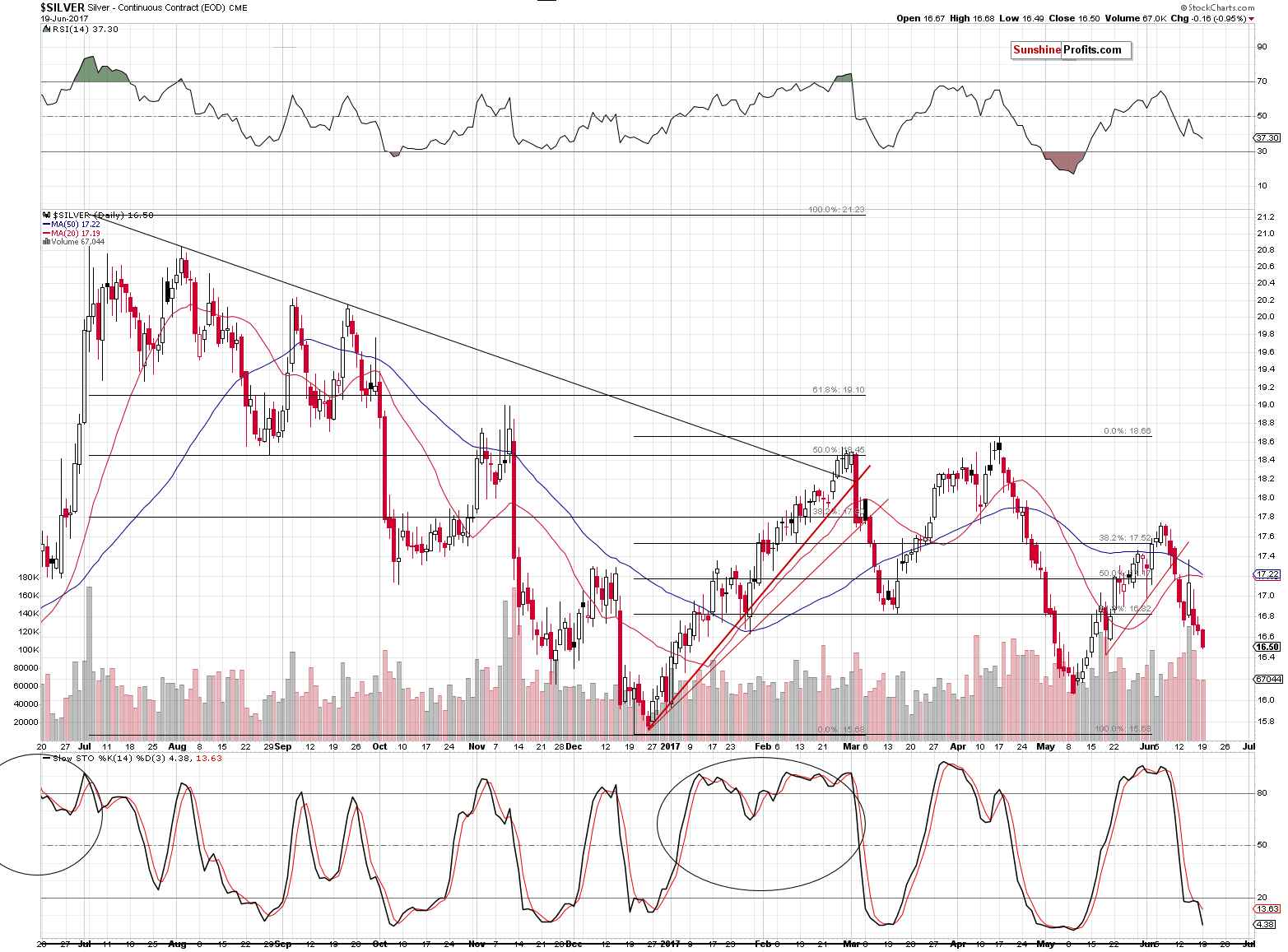

Now, look at the setup in these custom metals index charts. A clear Flag formation has setup near historical lows that is nearing the Pinnacle. My analysis of this pattern shows that we are setup for one more lower price rotation before the rally begins. One more attempt at buying near ultimate lows before we could see a massive, explosive rally capable of at least a 50%+ run. Long term, this run could be much bigger.. much, much bigger. Fibonacci theory shows the potential for 125% or 225% gains are easily possible.

Oddly enough, our research shows that this lower wave of metals prices should complete near or before June 29th. Remember that date from the beginning of this article? That’s right, this is the date that we predict would initiate a volatility spike (VIX Spike). Just how big will this VIX spike be? If our analysis is correct, the real VIX/volatility expansion won’t begin to happen till near the end of August or near the middle of September, 2017.

Our analysis shows that the Metals will begin to make a move near the end of June or early July 2017. Our analysis also shows that the US and global markets will begin to see increased volatility near Aug/Sept 2017. We also believe that any move in Metals will likely be the result of extended risk factors globally.

Chris Vermeulen

If you like receiving this type of analysis and want to continue to receive these advanced research reports, detailed trading signals and more, then visit www.ActiveTradingPartners.com and become a member.

{kind=link}

{kind=link}