Gold & Precious Metals

Strengths

- The best performing precious metal for the week was palladium, up 5.10 percent. Grant Sporre, an analyst at Deutsche Bank, noted there is a genuine physical tightness in the market, but the spike had all the hallmarks of someone being caught short and being squeezed. Bullionvault’s Gold Investor Index, which measures the balance of client buyers against sellers, rose the most in two years reaching a high of 55.3 in May versus 52.1 in April, reports Bloomberg. In India, gold imports jumped fourfold in May to 126 metric tons from 31.5 metric tons in the same month last year. In a report by the World Gold Council, consumption in India could climb dramatically this year as a “simple” nationwide Goods Services Tax will boost the economy, making the gold industry more transparent to benefit buyers, reports Bloomberg.

- Amid unease over a congressional hearing on possible links between Russia and the Trump campaign, holdings in SPDR Gold Shares (the world’s largest gold-backed ETF) climbed to the highest this year on the back of safe-haven demand, reports Bloomberg. In the two weeks through the end of May, hedge funds and other large speculators boosted their bullish bets on the precious metal by 37 percent, notes another Bloomberg article, the most since 2007 according to government data.

- Japanese investors sold a record amount of U.S. debt in April, reports Bloomberg. “Political turmoil in Washington and uncertainty about French elections pushed down Treasury yields, diminishing their attractiveness,” the article continues. Japanese investors cut holdings of U.S. debt by $33.2 billion in April, the most in data going back to 2005, according to a Ministry of Finance balance-of-payments report.

Weaknesses

- The worst performing precious metal for the week was silver, off 1.90 percent and largely in sync with the fall in gold. Data from the People’s Bank of China show that the Asian nation kept its gold reserves unchanged for the fifth straight month. Holdings stand at 59.24 million ounces for the end of May, the same level since the end of October. UBS commented on the moves in a report this week. “We maintain our base case that purchases should resume up ahead as overall official reserves stabilize, given that the diversification argument remains intact,” writes Joni Teves at UBS. “Nevertheless, we acknowledge growing risks to this view considering that the pause in buying has gone on longer than we initially expected.”

- According to an emailed statement from the Athens-based Energy Ministry, the Greek government will seek arbitration against Hellas Gold to “ensure contractual obligations of the company,” reports Bloomberg. The compliance measures are in reference to Kassandra mines in northern Greece. On the flip side of things, Eldorado Gold says is hasn’t been notified of the Greek arbitration, and says it operates in accordance with all applicable laws and regulations in jurisdictions where it conducts business.

- Employees at Freeport McMoRan’s Grasberg mine in Indonesia who stopped showing up for work in mid-April (totaling 4,000 employees and contractors), are in the process of being replaced, reports Bloomberg. Freeport CFO Kathleen Quirk said in a presentation in Chicago that all 4,000 are deemed to have resigned. The company’s top priority for the remainder of 2017 is getting a long-term extension to operating rights in Indonesia.

Opportunities

- A rush to haven assets has led to two firms saying they plan to open vaults in Europe capable of holding more than 100 million euros in gold, reports Bloomberg. This would offer customers lower costs that ETPs as well as protection from rising prices. “Inflation is a key concern for many of our clients,” said Ross Norman, CEO of Sharps Pixley. In a related note, China (the world’s biggest gold market) could boost its imports through Hong Kong by about half this year, as investors seek to protect their wealth from currency risks, reports Bloomberg. In fact, China’s gold imports are already heading higher in 2017. A slowing property market and volatile stocks also add to the safe-haven allure, according to the Chinese Gold & Silver Exchange Society.

- In its Global Precious Metals Comment this week, UBS writes that gold’s strength is justified by macro forces. “In particular, lower rates, weaker dollar and broader uncertainty provide good foundation for the market to continue its journey higher,” the report reads. The group adds that gold’s use as a portfolio diversifier has become increasingly relevant in the current environment and that despite the rally from May lows, UBS believes gold positioning is not crowded overall and there should still be room for the move to extend.

- Sean Casey, contributing analyst with Bloomberg, writes “Commodities’ negative correlation to the dollar has never been more stressed in the Bloomberg Dollar Spot Index’s 13-year history.” The note continues by stating that commodities could rally 20 percent just by catching up to the declining dollar. Over the past 26 weeks the dollar is down 6.1 percent and the Bloomberg Commodity Index is down 2.2 percent. “This unusual disparity has never happened since the dollar index’s start in 2004,” the article continues. “In the 73 weeks where the dollar ended down 5 percent or more on a 26-week basis, commodities have increased 20 percent on average.”

Threats

- Mexico’s tax agency owes Canadian mining companies over $360 million in tax rebates, reports Reuters and Bloomberg. The sum includes $230 million owed to Goldcorp and $66.5 million to Torex Gold Resources, just to name a few. “It’s damaging the ability to reinvest the dollars in assets that actually pay real tax,” said Torex chief executive Fred Stanford. The situation proves even more difficult for smaller, cash-strapped miners and explorers.

- A note from Global Mining Research this week states that wholesale electricity prices have nearly tripled over the last 18 months in Australia, primarily driven by capacity closures and higher gas costs, according to Energy Australia. Although short-term fluctuations are nothing new, “these price increases look here to stay with new generation capacity needed.” The mining industry in South Africa is also facing cost pressure. Its new mining charter will be gazetted and become law next week, Mineral Resource Minister Mosebenzi Zwane said Tuesday. The mining industry doesn’t think it has been consulted enough on these changes and is thus losing investment. Similarly, Tanzania plans to introduce a 1 percent clearing fee on the value of mineral exports in 2017/18, according to its finance minister, part of government measures aimed at getting a bigger share of revenues from tis natural resources.

- Mitsubishi Materials Corp. processed 20 percent of all electronic waste gathered globally last year to recover gold, silver and copper, reports Bloomberg. The “urban miner” plans to expand processing capacity by 14 percent to 160,000 tons next year, according to senior managing executive officer Yasunobu Suzuki. The company plans to open a facility in the Netherlands in November to collect waste in Europe for processing at its Japanese facilities and should be additive to recycled gold supply.

………Find out what’s driving gold!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001).

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Mega-Risks Loom in the Next very few months and most will be realized. But for Investors properly positioned, they Provide Very Substantial Profit and Wealth Protection Opportunities. First let’s examine the Risks, then the Profit Opportunities.

MEGA-RISKS

China

Perhaps the Main One will be the slowdown in growth in China, the world’s second largest economy. This Slowdown will be Caused mainly by China’s serious drive to restrain unsustainable credit growth.

Indeed, credit outstanding (including to “Wealth Management” entities outside the formal banking system) is a Real Threat to China’s Economy and was recently estimated to be 260% of GDP. Indeed, China’s Credit has been rising twice as fast as China’s GDP. But China’s restraints on Credit Growth will lead to the slowing of China’s economy.

Consequences of China’s Slowing:

¾ Dramatically reduced demand for many commodities Worldwide

¾ Chinese GDP growth plunging by up to 50% by 2020

¾ Diminished liquidity in China and thus Worldwide

¾ A fall in Chinese Equities, the beginning of which is already evident in the Shanghai Exchange

¾ Greatly diminished Credit Availability

¾ And because China is the 2nd largest Economy, these Negatives will adversely affect other Economies and Markets

USA

Almost surely this coming Fall’s Budget Deal will require an increase in the Debt Ceiling. There will be several consequences of which the most important are:

¾ Weakening of the $US

¾ A great deal of Conflict and Consequent Uncertainly

¾ Strong leg up for Real Money, i.e., Gold and Silver (but only in certain Forms see Deepcaster’s recent Letter and Alerts), and Spike UP and then the beginning of the Great, probably multi-year, Bear Market for Key Sector Equities

¾ The beginning of a deeper and widely acknowledged U.S. Recession

¾ Consider the Real Numbers courtesy of shadowstats.com compared with the Bogus Official Ones (Note 1)

Internationally

¾ An intensification of the Currency Wars among Central Banks, with one eventual Result being the $US loss of World Reserve Currency Status and either the Gold-backed Chinese Yuan or the IMF SDRs ascending to that Status.

Result: an even worse recession in the USA and China, and spreading Worldwide.

Political-especially in the USA, Eurozone and Mideast

Political Factors will continue to have an inordinate influence on the Markets going forward. Indeed, if the Deep State Neo-Con Globalist’s and Cultural Marxist’s Attempts (see Carrying Capacity Network’s February 2010 article re Cultural Marxism) to destroy the Trump Administration continue to gain momentum, The Great Crash we forecast to begin in September/October could start sooner than even we have forecast it to begin (see our most recent Alert for likely Triggers).

But it could also be delayed, but not avoided by a successful Repeal and Replace Healthcare Bill and/or Corporate Tax Cut which might still cause a significant Market Bounce lasting for days or a few weeks, ifother Political Events do not continue to dominate.

Indeed, Equities Markets around the world have topped, or, in the case of the USA, are Topping, and the USA is almost done Topping!

Overview: the Markets have shot up since the U.S. Election (Dow has hit a record 21,000+) on the hope/sentiment that President Trump’s Optimistic speeches and Policies will usher in a New Era of a Booming Economy and Markets.

Unfortunately, as much as we would like to believe in that vision, the Economic and Geopolitical Realities/Headwinds which Trump inheritedare simply too great for that hope to be entirely fulfilled, at least in the short-term.

Consider:

The $20 Trillion-plus U.S. Debt and $100 Trillion+ downstream Unfunded Liabilities are one problem which has not been dealt with! Indeed, those debts are unpayable absent currency devaluation. And China’s unpayable Debt to GDP is 260%! So China can not be the Savior of the International Economy. How are substantial Tax Cuts Possible without substantially raising the Debt Ceiling?

And we reiterate that, in addition, Due to the private for-profit U.S. Federal Reserve Bank’s low interest rate Policies, Many Companies and Countries are highly overleveraged (and Many Retirees devastated due to hyper-low rates on CDs etc). EXCESS DEBT IS THE GREAT TRAP and likely The Primary Cause (among several) of the expected Crash. (See our Buy Recommendation aimed at profiting from this.)

Moreover, until recently, the Markets have been pricing in Massive Trump Tax cuts. We expect there will be cuts, but not as substantial or as soon as the Markets expect, want, or are pricing in. And other Trump Initiatives are meeting strong resistance. And the RyanCare debacle has been disastrous. Therefore, Earnings Improvement (though Good for Q! 2017) Expectations will eventually be dashed. Result: More Impetus to the downside. See our most recent Alert for Timing.

Thus, The Fed will eventually have to print “Money from Helicopters” and that will be very inflationary.

Great Volatility is coming!

Bank Failures and likely consequent Asset Confiscation

If the Coming Crash is as severe as we have forecast, Banks will Fail. If the U.S. or other Entity fails to bail them out, then Assets in a bank in excess of $25,000 are subject to confiscation.

Specifically, under the “Adequacy of Loss-Absorbing Capacity” Mandate, approved by the G20, the failed bank can take Depositors’ money and convert it in to Equity in that (failed!) Bank!

Also, CDs, Money Markets, Annuities, IRAs and Savings Accounts are apparently at risk, as well!

Note that, Banks are already Failing in Greece, Puerto Rico, Argentina and Venezuela and are threatened in various Eurozone Countries. This will likely cause an increasing Ripple Effect since Credit Markets are interrelated.

The Bitcoin (and related Blockchain) Delusion/s

That Investors treat Bitcoin as anything other than a Rank Speculation amazes us.

Surely it is not a reliable Store of Value, nor a convenient Medium of Exchange—two Characteristics of Real Money.

Consider:

1) One major Electro-Magnetic Pulse (e.g., from Satellites which North Korea already has circling the Globe) could take the Internet down for weeks or Months. And Bitcoin’s Fate?

2) And the Monetary and Law Enforcement authorities are surely Monitoring it to get a lead on crooks. Indeed, allowing Bitcoin to continue even though it is arguably illegal Money, is very convenient for law enforcement. The claim that it cannot be traced or hacked is nonsense.

3) And any government can make Bitcoin Transactions illegal at any time. It is after all a Competitor to their Fiat Currencies. Therefore, we fully expect the Coming Crash would be a Trigger for a Bitcoin Meltdown.

Mega-Bankers Ongoing Move to Eliminate Cash

Very serious and a Great threat to our Freedom as well as our Assets. See our Article “Profit and Protection from Threats to Our Freedoms” for more analysis and detail.

Profit and Protect

Deepcaster has Recently recommended several positions which should do well, or very well, in the event of Key Sector Crashes and/or Deeper Recession, for both Profit and Wealth Protection. See our Recent Alerts.

Gold and Silver

But there is one Asset class we expect to do very well—Real Money, i.e., Gold and Silver provided they are owned in a Non-Fraudulent, Not-merely-or-allegedly-Representative Forms. To see what Form/s we recommend for both Profit and Protection see our recent Letters and Alerts.

And there is one additional Impediment to owning and profiting from Gold and Silver.

A Fed-led Cartel of Mega-Banks has for years conspired and continues to conspire to Suppress their Prices. Of course they do this to push investors into their Fiat Currencies and Treasury Securities to enhance The Cartel’s Power, Wealth, and Control.

This Cartel is and can be beaten but the forms of an Investor’s of Gold and Silver Holding is here crucial as is Timing of Purchases. (See Deepcaster’s Letters and Alerts.)

We encourage those who doubt the scope and power of Overt and Covert Interventions by a Fed-led Cartel of Key Central Bankers and Favored Financial Institutions to read Deepcaster’s February, 2017 Letter entitled “Profit, Protection, Despite Cartel Intervention” in the ‘Latest Letter’ Cache at www.deepcaster.com. Also consider the substantial evidence collected by the Gold AntiTrust Action Committee at www.gata.org, including testimony before the CFTC, for information on precious metals price manipulation, and manipulation in other Markets. Virtually all of the evidence for Intervention has been gleaned from publicly available records. Deepcaster’s profitable recommendations displayed at www.deepcaster.com have been facilitated by Deepcaster’s attention to these “Interventionals.” Attention to The Interventionals facilitated Deepcaster’s recommending five short positions prior to the Fall, 2008 Market Crash all of which were subsequently liquidated profitably.

Best regards,

Deepcaster

June 9, 2017

Note 1: Bogus Official Numbers vs. Real Numbers (per Shadowstats.com)

Annual U.S. Consumer Price Inflation reported May 12, 2017

2.20% / 9.95%

U.S. Unemployment reported June 2, 2017

4.29% / 22.0%

U.S. GDP Annual Growth/Decline reported May 26, 2017

2.04% / -1.86%

U.S. M3 reported June 4, 2017 (Month of April, Y.O.Y.)

No Official Report / 3.514%(e) (i.e., total M3 Now at $17.988 Trillion!)

[See also our other recent Letters, Alerts and Buy Recommendations at Deepcaster LLC for further Analysis and Forecasts.]

DEEPCASTER LLC

www.deepcaster.com

DEEPCASTER FORTRESS ASSETS, HIGH POTENTIAL

SPECULATOR & HIGH YIELD PORTFOLIOS

Wealth Preservation Wealth Enhancement

Investment and Geopolitical Intelligence

Why are these billionaires buying precious metals?

Their cited reasons can basically be summed up with six categories: wealth preservation, store of value, inflation hedge, portfolio diversification, future upside, and investment fundamentals.

What Billionaire Investors are Doing

1. Lord Jacob Rothschild

In late summer 2016, Rothschild announced changes to the RIT Partners portfolio because he was worried about very low interest rates, negative yields, and quantitative easing, saying they are part of the “greatest monetary experiment in monetary policy in the history of the world”.

His solution? Buy gold to help preserve wealth, and as a store of value for the future.

2. David Einhorn

Einhorn has a similar assessment. He believes that monetary policy is becoming increasingly adventurous, and that this – along with the policies of the Trump administration – will eventually lead to large amounts of inflation.

In February 2017, he shorted sovereigns, and bought gold.

3. Ray Dalio

Ray Dalio is the founder of the world’s top hedge fund, Bridgewater Associates, but he’s also no stranger to gold.

If you don’t own gold, you know neither history nor economics.

– Ray Dalio, Bridgewater Associates

More recently, in 2016, Dalio is quoted as telling investors to own a well-diversified portfolio that is 5-10% gold.

4. Stanley Druckenmiller

Druckenmiller, some people argue, is the best money manager of all time.

Lately, he’s placed his bets on gold as well, but for different reasons than the above managers. Druckenmiller has always placed big trades with lots of conviction, and in February 2017 he put his money in gold because “no country wants its currency to strengthen”.

Marc Faber points out the financial system, the Federal Reserve and other Central Banks in the world are being run by academics, most of who haven’t worked outside of academia for their entire lives, that interest rates have never been lower in 5000 years and that this unprecedented monetary experiment will one day react negatively.

….related by Michael Campbell: Voters Love Hearing It’s Going To Be Free

Sell to Whom?

Sell to Whom?

(Almost) Everything Is Awesome

Bending the Yield Curve

The Dangers of Passive Investing

Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

“Forget the past. The future will give you plenty to worry about.”

– George Allen, Sr.

“I try not to worry about the future, so I take each day just one anxiety attack at a time.”

– Tom Wilson

The middle ground can be uncomfortable. As someone now widely known as the “muddle-through guy,” I have learned this the hard way. My bullish friends call me a worrywart, and the bearish ones think I am Pollyanna incarnate.

The irony here is that I’ve never claimed to be a great trader or a short-term forecaster. I think I have a pretty good record of calling major turning points. Next week or next month is another matter. Anything can happen, and it probably will.

That said, the fact that my forecast may be wrong doesn’t prevent me from making one. So, with all the usual disclaimers, today I will review some recent analysis from my reliable sources and let you take a peek into my worry closet.

One point we all agree on: We live in unusual times.

Last week Doug Kass sent around an e-mail comparing today’s markets to Queen’s classic “Bohemian Rhapsody.” I know that seems odd, but it was actually a good fit. I shared Doug’s full message with my Over My Shoulder subscribers. For everyone else, the point is that, like the song says, “Nothing really matters” to whoever is buying stocks these days. They just keep buying and pushing prices higher. As Jared Dillian says, “It’s a bull market, dude!” Stock prices do go higher in a bull market; and sometimes, as the end approaches, they make value investors very uncomfortable.

Neither Doug nor I quite understand the “Nothing really matters” attitude, though we have some theories. Doug is probably more bearish than I am. He has a long list of open questions. I zeroed in on the last one, which is critical: “When ETFs sell, who will buy?”

The stratospheric ascent of passive indexing is having side effects that I suspect will make markets sick at some point. Passive investing is perverting the financial markets’ core economic function, i.e., efficient capital allocation. In terms of stimulating buying interest, a company’s fundamental business prospects are now much less important than its presence in (or absence from) popular indexes.

We’ve created this environment in which badly managed companies can still see their stock prices rise along with those of well-managed companies. The actual facts about a company don’t mean all that much in a passive-investing world. Capitalization-weighted indexes aggravate this already problematic phenomenon. Money is pouring into stocks like Apple (AAPL) and Amazon (AMZN) simply because they are big. The resulting higher prices make them bigger still, and they pull in yet more capital. Here’s a look at the five largest stocks in the S&P 500.

What about the QQQ or the NDX? The five stocks above represent 42% of the NDX and 13% of the S&P 500. That means every time you buy an index based on the NASDAQ, 42% of your money goes into just five stocks, leaving 58% for the remaining 95. By the time you get past the largest 25, you are under 1% per stock. Apple alone is 12% of the NASDAQ 100 Index and 4% of the S&P 500. That explains, in part, why the NASDAQ has outperformed the S&P 500.

For the record, Goldman Sachs researchers recently released a paper with a strong fundamental forecast for those stocks. That is, they expect them to continue to go up, absent a recession or something else that triggers a bear market. I keep scanning the horizons in every direction, and I just can’t see anything that would trigger more than a minor correction today. Of course, a minor correction could deliver outsized impacts, given the heavy weighting of a few stocks and passive index investing. Be careful out there.

Doug asks, “When ETFs sell, who will buy?” The ETFs of the world may quickly begin trading below their actual net asset values (NAV). This is called price discovery, and the arbitrageurs will not be slow to take advantage of that difference. This means the indexes will drop much faster than they have gone up. I am neither a fortuneteller nor the son of a fortuneteller, but there are a few things I’ve picked up along the way. One of them is that, next time, stocks are going to go down breathtakingly fast once they begin to roll over.

This bull can’t end well, but it will end. At that point, Doug’s question becomes critical: Who will buy? I don’t know, but someone will. Prices for good and bad stocks will drop to whatever levels attract buyers. The indexes will eventually fall lower than any of us think likely right now. Whether that will happen next month, next year, or next decade is anyone’s guess.

Sidebar: You should think of cash as an option on your ability to buy the stocks that will lose 50% of their value and suddenly become the value stocks of the future. The option value on your cash today is not that much. You don’t make much on it, but you don’t lose much holding it. The time is going to come when you will be glad you have a little cash to put to work. Think March 2009.

(Almost) Everything Is Awesome

While Doug was musing about Queen, Louis Gave was thinking about rugby. Should one go where the ball is now, or try to figure out where the ball will be?

Louis asks that question while noting that it has been extremely difficult to lose money this year. Almost every tradable asset class has been climbing. You are probably making good returns this year unless you have been:

Overweight energy and materials, and/or

Overweight financials.

Those have been the primary weak spots. Investors in everything from technology to emerging markets, to Europe and even utilities have done well. All you had to do was avoid energy, materials, and financials.

The reasons for this are pretty simple. Inflation remains low to nonexistent in most places, which hurts commodity prices along with companies in the energy and materials sectors. The widespread belief that inflation will stay low is keeping long-term bond yields low, which reduces the net interest margin for lenders, particularly banks. Hence, we see underperformance in financial services stocks, too. Further complicating the energy story is the continued expansion of unconventional shale oil production in the United States. Eventually the technology will spread to the rest of the world. Countries that depend on high oil prices are hurting. (And not just Saudi Arabia and Russia but a whole host of Middle Eastern countries).

The conditions that will change this pattern aren’t complicated: higher inflation expectations and rising long-term bond yields. That combination would push energy and metals prices up and steepen the yield curve. But the problem there is that the Federal Reserve remains intent on raising short-term rates. If they tighten another notch next week, as everyone expects, the current trends seem likely to continue. Here’s Louis’s conclusion:

In sum, it is hard to foresee what will disturb the current Goldilocks scenario. So, investors who liken themselves to Rugby forwards (aka “piggies”) [an actual rugby term that is a double-play pun on investors getting greedy and hungry – JM] will want to continue dining at the trough of the current bull market. Meanwhile, investors who like to get their hair blow-dried before games (backs, or princesses), and prefer to run where the ball is going to be rather than where it is, may want to look at reducing their underweights in financials. After all, at current global fixed income valuations, it wouldn’t take much – central bank hawkishness, upside surprises to core CPI – to trigger a mild fixed income sell-off. And any steepening of the yield curve would lead to a very different investment environment.

The shape of the yield curve is clearly critical in assessing markets right now. I agree with Louis that any steepening would lead to big changes. I wonder if we might get a steepening the other way: An inverted yield curve – when short-term rates are higher than long-term rates – is a classic recession indicator. It’s something the US hasn’t seen lately but can’t avoid forever.

How can we get an inverted yield curve with short-term rates so low? The Federal Reserve just slowly and surely raises rates; the weight of debt begins to slow economic growth even more; and long-term rates drop. Voilà, inverted yield curve. That is at least classically what is supposed to happen. So let’s think about that for a few paragraphs.

The other much-anticipated news from next week’s FOMC meeting is how/when the Fed intends to start reducing the massive bond portfolio it accumulated during the QE years. The initial move may be simply to stop reinvesting the proceeds when bonds mature. That is still billions of dollars each month – enough for even the very deep Treasury bond market to notice. (Then again, maybe they just let their mortgage bonds roll off and keep buying the Treasuries. They have so many options, and they haven’t bothered to tell us which ones they are seriously considering.)

A little-discussed aspect of this situation is, who will buy the Treasury bonds once the Fed backs out? That part is beyond the Fed’s control. The federal government won’t stop borrowing just because the Fed stops “lending.” The Treasury will have to find other buyers for its paper and will likely pay higher rates to attract them. Maybe. That is what is supposed to happen. In a world where the unthinkable keeps happening, we’ll just have to wait and see.

Brevan Howard’s chief US economist, my friend Jason Cummins (a past SIC speaker, I should note) wrote a fascinating guest column in the Financial Times on this topic. He points out something quite obvious that hasn’t occurred to many. The Treasury Department must borrow enough cash to pay the government’s bills, but it has huge discretion as to how it structures federal debt.

That means Treasury Secretary Steve Mnuchin can choose to replace the Fed’s purchases by issuing new debt at any point on the yield curve. It doesn’t have to be of the same term as the maturing paper it replaces. He can issue thirty-year bonds, three-month bills, or anything in between, in whatever combinations he thinks best.

The implication, as Jason gently explains, is that Steve Mnuchin can essentially rebuild the yield curve into whatever shape he wishes – presuming he can find buyers. He always will, of course, at some price.

The Treasury is such a massive borrower that its entry at any given maturity level can crowd out other borrowers and force rates higher. I am sure the Treasury people who manage this process try to reduce interest expense as much as possible, but they can only do so much. The government has bills to pay.

If Mnuchin decides to concentrate new borrowing at the long end, it will drive up those yields and steepen the yield curve. That’s exactly what banks would like to see. That would enhance their profit margins – but with the possible outcome of raising mortgage and other long-term rates. Not good for the housing sector.

Or, Mnuchin could do more borrowing at the short-term end. That would be a bit of a gamble because there’s no way to know what rates will be when the debt matures in the relatively near future. The strategy would also flatten and possibly even invert the yield curve.

Just to make all this more suspenseful, the government is also bumping up against its statutory debt ceiling. Congress might have to approve an increase as soon as August, and some in the House want to use the opportunity to exact spending cuts. The odds are low, but we can’t rule out the possibility of another government shutdown scenario, as we saw in 2011 and 2013.

As Cummins noted, “As the clock ticks down and investors get increasingly skittish, the last thing the Treasury needs is to have to find more private sector buyers of its debt.” Agreed. That is why I expect the Fed to delay implementing its balance sheet reductions until after the debt ceiling is raised – or maybe longer, if employment growth and/or inflation weaken over the summer and fall.

The Dangers of Passive Investing

Before we end, I want to come back to a few charts that illustrate some of the problems that are building up in the passive index world. It is not just ETFs, but also index mutual funds and the enormous amount of pension and insurance funds, along with many trust funds, that are passively invested directly in stocks. They simply duplicate indexes.

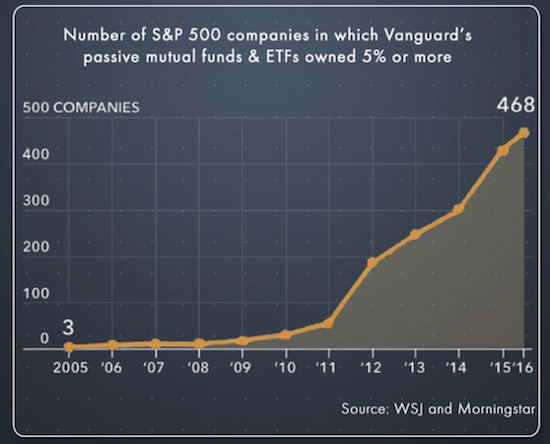

First, let’s note that Vanguard now owns more than 5% of 468 stocks in the S&P 500. That’s one fund company.

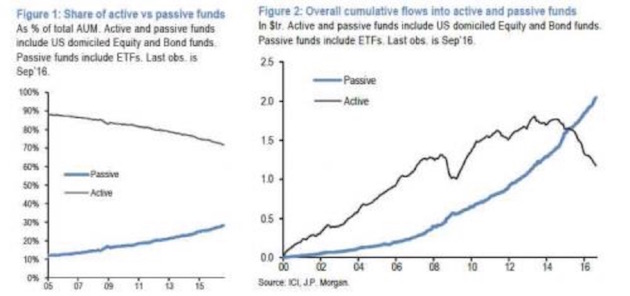

Here’s the picture for fund flows last year:

The number of hedge funds is at its lowest level since 2000. Passive funds are eating away at the assets under management by active funds:

This trend goes back to a point I made a few weeks ago but that needs to be repeated again and again. When the market obscures distinctions between good stocks and bad stocks because it buys all of them at the same time, there is no way for an active manager to take advantage of his skill in determining value. That ability to look at a company’s balance sheet and determine something close to true value is what gives active managers their edge. If you don’t have the chance to do this, you cannot add any alpha, and you are going to underperform the simple passive indexes – even though you charge higher fees. Money will leave you for the seemingly more plentiful pastures of passive indexing. One day you will be vindicated, and the money will come back (think Jeremy Grantham); but because investors will lose a great deal of their money in a bear market, you won’t get as much back in the short term as left you over the past few years. If you are an active manager, this just sucks.

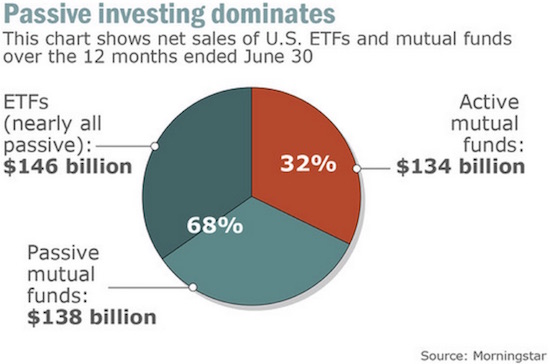

The next two charts show the difference between active and passive investing in the retail fund space. It’s a huge contrast:

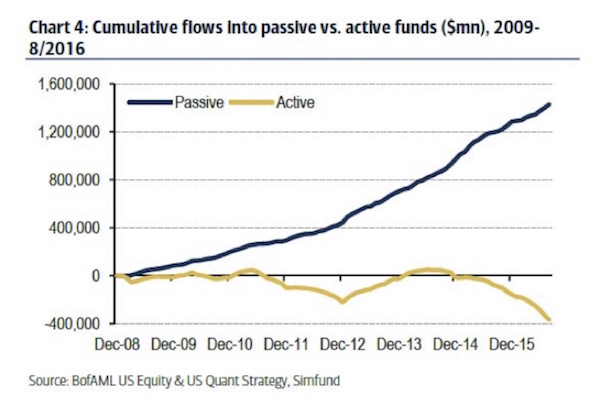

The chart below traces the widening imbalance since 2008.

As I stated above, this imbalance will eventually be corrected. But the correction will not be pretty, though it may be swift.

If I’m going to keep my pledge to be shorter, more thoughtful, and faster, then I’d better close on that note.

Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

Shane and I will be leaving for St. Thomas on 24 June, and we will be married on some beautiful beach on June 26, her birthday. Then I actually intend to relax for a week, enjoying time with my new bride and reading books with no redeeming social value (also known as science fiction/fantasy). I will begin final writing on my new book when I come back. I am finally really ready to attack the topic of what the world will look like in 20 years.

I have a quick trip to Omaha in the middle of June, then I’ll head directly on to San Francisco and Palo Alto for speaking engagements, come home to Dallas, recover for a few days, and then leave with Shane to go to Las Vegas for the Freedom Fest. It has become one of the largest libertarian gatherings, and I have so many good friends who go that it’s really a lot of fun for me. And while I am not much of a gambler (as in I suck at it and hate losing money to people who are much richer that I am), I really do like the shows. And dinners with friends.

That covers July, and August is, of course, the annual Maine fishing trip, but right now the rest of August looks to be pretty wide open. If I can figure it out, I may go somewhere that has a much cooler climate than Texas does in August and relax and write.

I will be cooking a chili dinner along with some prime this week for a dozen or so investment advisors who will be coming to Dallas to learn about my new Mauldin Solutions Smart Core investment program. For those of you have not yet gone to www.mauldinsolutions.com and given me a little bit of information about you, we have a white paper we would like to send to you, and there is other information on the website that will give you an idea as to how I think core portfolios should be structured in today’s world. Whether you are an individual or a professional or an institution, the principles are the same.

And with that I will hit the send button. You have a great week.

Your not going passively into the next bear market analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

|

Get a Bird’s-Eye View of the Economy with |

|

Share this letter using the buttons below |

|

Share Your Thoughts on This Article![]()

http://www.mauldineconomics.com/members

Thoughts From the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com.

Any full reproduction of Thoughts from the Frontline is prohibited without express written permission. If you would like to quote brief portions only, please reference www.MauldinEconomics.com, keep all links within the portion being used fully active and intact, and include a link to www.mauldineconomics.com/important-disclosures. You can contact affiliates@mauldineconomics.com for more information about our content use policy.

http://www.mauldineconomics.com/subscribe

Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin’s other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available, President and registered representative of Mauldin Securities, LLC, (MS) member FINRAand SIPC, through which securities may be o ffered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Mauldin Securities. It is intended solely for investors who have registered with Mauldin Securities and its partners at www.MauldinCircle.com(formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available. John Mauldin is a registered representative of Mauldin Securities, LLC, (MS), an FINRA registered broker-deale r. Mauldin Securities cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with w hich they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account manager s have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair