Energy & Commodities

Surprising no one, President Donald Trump announced his decision to withdraw the U.S. from the Paris climate agreement last week, highlighting the depth of his commitment to keep “America First.” Also surprising no one, the media is making much of the fact that the U.S. now joins only Nicaragua and Syria in refusing to participate in the accord.

Trump was under intense pressure from business leaders, politicians on both sides of the aisle, environmental activists, members of his Cabinet—even his own daughter Ivanka, reportedly—to stay in the agreement, but he made his decision with the American worker in mind. The Paris accord, Trump said, “is simply the latest example of Washington entering into an agreement that disadvantages the United States,” leaving American workers and taxpayers “to absorb the cost in terms of lost jobs, lower wages, shuttered factories and vastly demised economic production.”

This is the assessment of Secretary of Commerce Wilbur Ross, who went on Fox News to defend the decision. “Any time that people are taking money out of your pocket and you make them put it back in, they’re not going to be happy,” Ross said, making a similar argument to the one that prompted the Brexit referendum last year.

Just as many Brits were tired of following rules passed down from unelected officials in Brussels, many Americans have feared the encroachment of global environmentalists’ socialist agenda, which they believe threatens to usurp their freedom.

A thought-provoking article from FiveThirtyEight outlines how climate science became a partisan issue over the last 30 years in the U.S. It was the fall of the Soviet Union in the early 1990s, the article argues, that brought on a significant partisan shift in attitude, with conservative thinkers beginning to see the regulations that went along with environmentalism as the new scourge.

No, the Sky Isn’t Falling

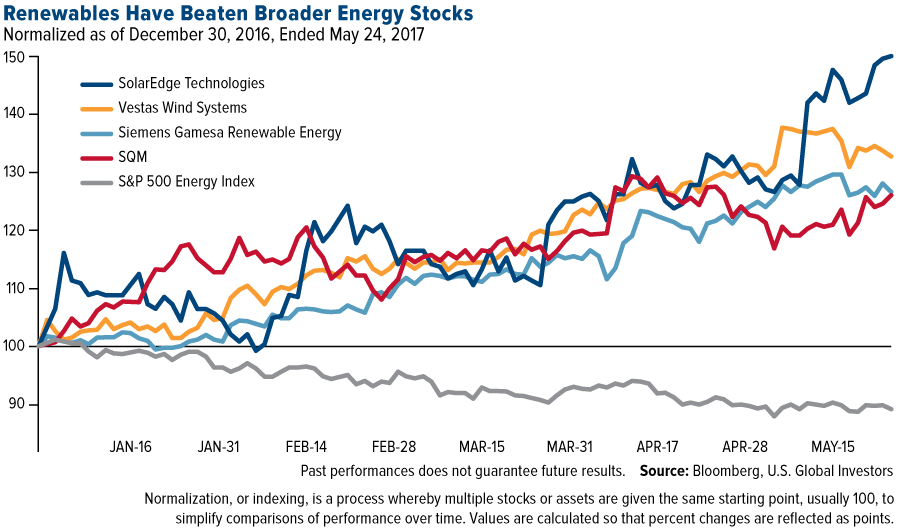

Despite the withdrawal, I believe that the U.S. will not stop innovating and being a world leader in renewable energy—even while oil and natural gas production continues to surge. As the president himself said, we will still “be the cleanest and most environmentally friendly country on Earth.”

Recently I shared with you that we’re seeing record renewable capacity growth here in the U.S., with solar ranking as the number one source of net new electric generating capacity in 2016. In the first quarter of 2017, wind capacity grew at an impressive 385 percent over the same period last year. The “clean electricity” sector now employs more people in the U.S. than fossil fuel electricity generation, according to the 2017 Energy and Employment Report.

This was all accomplished not because of an international agreement but because independent communities, markets and corporations demanded it. Solar and wind turbine manufacturers will likely continue to perform well in the long term as renewable energy costs decline and battery technology improves.

Clearly people’s attitudes toward climate change—and its impact on business operations—are changing. This week, Exxon Mobil shareholders voted to require the company to disclose more information about how climate change and environmental regulations might affect its global oil operations. The energy giant—along with its former CEO, Secretary of State Rex Tillerson—favored staying in the climate deal.

At the same time, markets reacted positively to the exit, with the S&P 500 Index, Dow Jones Industrial Average and NASDAQ Composite Index all closing at record highs on Thursday following Trump’s announcement.

So What Does This Mean?

The question now is what investment implications, if any, the withdrawal might trigger.

The short answer is no one knows exactly what happens now. There’s already speculation that some countries might act to raise “carbon tariffs” on U.S. exports, increasing the cost of American-made goods “to offset the fact that U.S. manufacturers could make products more cheaply because they would not have to abide by Paris climate goals,” according to Politico. German chancellor candidate Martin Schulz has said that, should he be elected in September, he would refuse to “engage with the U.S. in transatlantic trade talks.” Schulz’s comments are not that far removed from those of his political rival, incumbent Angela Merkel, who called Trump’s decision “extremely regrettable.”

This has the potential to widen the rift that’s been forming between the U.S. and Germany since Trump took office. Recall that Trump refused to shake Merkel’s hand during her Washington visit in March. More recently, the president reportedly called the Germans “bad, very bad,” adding that he would stop them from selling millions of cars in the U.S.

One of the biggest winners of the withdrawal could be China. Just as the Asian giant is poised to benefit from the U.S. distancing itself from multilateral free-trade agreements such as NAFTA and the Trans-Pacific Partnership (TPP), it’s also in a position to brand itself as the world’s leader in renewable energy. Last week, Chinese Premiere Li Keqiang met with European Union (EU) officials in Brussels to discuss trade between the two world superpowers, but they also took the time to condemn the U.S. president’s actions, with European Council president Donald Tusk saying that the Paris agreement’s mission would continue, “with or without the U.S.”

|

China might be the largest carbon emitter right now—it overtook the U.S. a decade ago—but it’s also the biggest investor in renewable energy generation, with $361 billion being spent between now and 2020. The country just fired up the world’s largest floating solar power plant in what used to be a coal mine, now flooded. The plant will provide as much as 40 megawatts (MW) of power to Huainan, China, home to more than 2.3 million people.

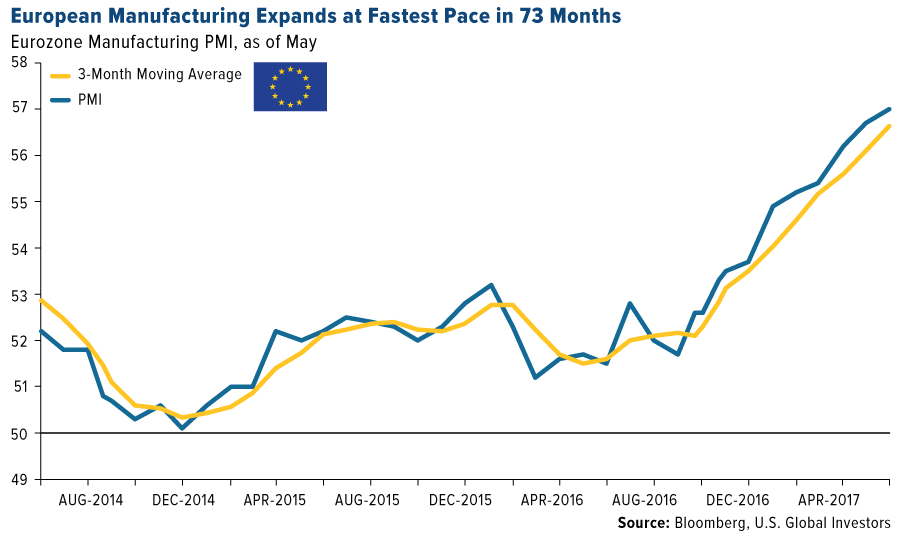

European Manufacturers Have Strongest Jobs Growth in 20 Years

On the same day President Trump shared his decision, new purchasing manager’s index (PMI) data was released, and just like last month, European manufacturers were the big surprise. The EU manufacturing sector strengthened its expansion for the ninth straight month in May, reaching a 73-month high of 57, right in line with expectations. Jobs growth grew to an incredible 20-year high.

Germany led the group with a PMI of 59.5. Of the eight EU countries that are monitored, only Greece fell short of expansion.

The U.S., meanwhile, slipped from 52.8 in April to 52.7 in May, posting the weakest improvement in business conditions in eight months, before the election. China fared even worse, falling from 50.3 to 49.6, signaling a slight deterioration in its manufacturing sector for the first time in almost a year.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every invest.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 03/31/2017: Exxon Mobil Corp., SolarEdge Technologies Inc., Vestas Wind Systems A/S, Gamesa Corp. Tecnologica SA, Sociedad Quimica y Minera de Chile.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Mike Gleason: It is my privilege now to welcome in Dr. Chris of PeakProsperity.com, and author of the book Prosper! How to Prepare for the Future and Create a World Worth Inheriting. Chris is a commentator on a range of important topics such as global politicals, financial markets, governmental policy, precious metals and the importance of preparedness among other things. And it’s always great to have him with us.

Mike Gleason: It is my privilege now to welcome in Dr. Chris of PeakProsperity.com, and author of the book Prosper! How to Prepare for the Future and Create a World Worth Inheriting. Chris is a commentator on a range of important topics such as global politicals, financial markets, governmental policy, precious metals and the importance of preparedness among other things. And it’s always great to have him with us.

Chris, welcome back and thanks so much for joining us again.

Chris Martenson: Thank you. It’s a real pleasure to be with you today, Mike, and all of your listeners.

Mike Gleason: Well, since this is actually the first time we’ve had you on in 2017, Chris, to get started here I’d like to have you set the stage for us because many of us continued to be confused and bewildered by the resilience of these markets. So, first off, give us your thoughts on the first 130 days or so of Trump’s presidency, and then how is it that the U.S. equities market continues to soar to new heights despite what appears to be massive overvaluation? Basically, assess for us what’s going on in the political and financial markets here during the first half of the year as we start off.

Chris Martenson: All right. Well, I love how you set that up, because they’re actually coincident in my mind. The first four months of 2017, we saw something that has never been seen in world history, and that was central banks across the globe creating a trillion dollars of new hot money. So, if you want to know anything I think about the markets, we have to start with 250 billion thin air hot money base currency units being created and tossed into the financial systems. That really is a large explanation factor. And of course, there was this idea that Trump was coming in and that this could put some sort of a fresh air, a theme here, but let’s be clear.

Trump was a surprise victory there, and at about 2:30 in the morning (on election night) with the Dow down 800 points, it rallied and got back to green by open, and no question in my mind, but that was official action, the Plunge Protection Team or somebody like that, and so I think that’s the world we’re in now, really. That’s my setup. The macro setup is the authorities are dumping huge amounts of money into markets to get them to go higher. They’re also making sure that markets can’t go down at any point. They do what they can. My view is they’ll do that until they can’t, and then it will break and it’d be very surprising for a lot of people.

Mike Gleason: Expanding the point here, Chris, lately we have been addressing the exhaustion that some bullion investors are feeling. They have spent the past decade watching as the growth in government data’s accelerated, something you’ve been following and documenting for years, all the way back to your amazing Crash Course presentation, which really opened my eyes when I first consumed that amazing material. The Fed and other central banks have abandoned all restraint, zero interest rates, monetizing treasury bonds, and mortgage securities, and other exotic programs. The federal government has been running massive deficits for even longer, for half a century at least, but none of this, to this point anyway, has seemed to matter.

The U.S. dollar appears to be holding up, the bond vigilantes have never shown up, stock prices are making all-time highs and no one on Wall Street seems to be interested in buying safe haven assets. Now, the upcoming webinar that you’re going to be doing here very soon, and we’ll get into those details later in the podcast, is titled, “The End of Money” and you will be making the case that these fundamentals do in fact matter. Talk for a minute about what you see developing and why you think safe haven investors just need to stay the course despite what appears to be a punishing environment.

Chris Martenson: Well, I’d love to. You have to have a macro view at a time like this. There’s no other way to explain, when you’re in the middle of the largest money printing experiment, and I use that word carefully, in all of human history. To try and think that what guided us in the past is going to be useful during the most extraordinary money printing of all time is, I think, misguided. What do we do with that? Well, I think we have to understand how much is being printed, what that actually means, what it really tells us about what the Fed is thinking, how scared they are. Listen, you’ve got your chips on one side of the table than the other.

Either they know exactly what they’re doing and they’ve got this all under control, or they really don’t. If you have all your chips on the “they’ve got this covered” side, I think it’s a bad debt at this stage. So that’s why we’re having this webinar, is to talk with people who have pretty good insights into who the Fed is, how they were founded, how they were organized, what they’re thinking currently, and really that means we’re in that speculative mode still. Because were trying to figure out, Mike, what’s the Fed going to do? It’s not very fundamental, but we do know that fundamentally, when we back up even further, there always has to be a balance between the money you create and the stuff you buy with it. In this story, the money we create is both currency and it’s debt.

They both operate like money, like if I take out a student loan for $50,000 and spend that money, that $50,000 that went out because of credit expansion. When we look at this story, the world has had the fastest period of credit expansion in the last eight years or so that it’s ever had. It has this extraordinary base money creation, largest in all of history by far. It’s driven up financial assets like stocks and bonds to ridiculous heights. Quite mysteriously, left commodities pretty much completely off of that particular run since 2011 and QE3. So, when we put all of that in one spot, all I see is that the claims no real wealth are increasing, and that’s both the debt and the currency.

With both of these increasing as fast as they are, I know there has to be a correction at some point, and things have gotten really extreme lately, all across the globe but particularly in equity markets, places like that. What can you do? This is a crazy bubble time, you have to sit back and watch, you have to understand where it comes from. In The Crash Course, I make the case, Mike, that we’re not dealing with the after effects of a housing bubble that burst in 2007. We’ve been growing our credit at twice the rate of our income in this story, so total credit market debt compared to GDP. The debt’s been growing twice as fast as our income in this story for 45 years. That’s what broke in 2008, and it hasn’t been able to be fixed because it’s just a dumb model.

“Hey, we’re going to grow our expenses and our expenditures at twice the rate of our income.” You know, you can’t do that as a person, so you can’t do it as a nation. That’s what we’ve been doing and that’s what I think has just gotten to extraordinary levels right here, with what the central banks are now trying to just keep this going a little longer. And we don’t have a lot of history to guide us here. We have seen currencies collapse in the past, we’ve seen economies really struggle. You see that in Venezuela, but there’s really nowhere to escape this one, truthfully, because the whole world is involved in this at this point. It’s not like you’re in Austria in 1918 and you could duck over the border and be in a safe country.

Where would you go, given that it’s really the dollar, the Yen, the Euro have all been principally on this train? China caught up really fast in this story. Where would you go? With that, I don’t have any great answers besides people need to understand the context and then begin to build resilience in their portfolio, financial resilience, but other forms of resilience around social capital, emotional capital, all of the other things that we talk about in Prosper!, because I personally don’t see a way to get out of this without experiencing a lot of pain, economically.

Mike Gleason: We certainly are in uncharted waters. Now, the Fed has had a bit lower profile since the November elections. Trump has decided to stick with Janet Yellen, at least for the time being, and the constant political drama in Washington seems to be dominating even when it comes to investing news. Frankly, the constant obsession over what the FOMC might do at their next meeting had become tedious beyond words, so we’ve been glad for the respite. However, there will be plenty of attention on this month’s meeting, where officials are expected to hike rates again.

Do you agree with the consensus that two to three more rate hikes are coming in 2017? If they keep hiking, it seems The Fed will eventually wind up at odds with Trump who would almost certainly like to avoid holding the bag during the next big economic slowdown. So, what are your thoughts about the Fed during Trump’s administration here, Chris, both in the short run and in the longer term?

Chris Martenson: Well, the Fed is really just running its own script at this point in time. It’s pretty independent of who’s in the White House, and Trump can try and lean on them a little bit, but he won’t lean on them in the way that you or I might think he should, which is to tighten things up would probably be a wise course of action. But something that I’ve written about and I’ve even produced a short video on recently, is that this dynamic you’re talking about of tightening is not actually happening in this cycle. Because in 2008, Congress gave the Federal Reserve the right to pay interest on excess reserves that are held by depository institutions at the Fed.

So, the Fed prints money and of course that creates lots of excess reserves in the banking system, then the banks put that back at the Fed, and the Fed pays interest on that. The last three hikes that we’ve seen, going from basically a range of between zero and a quarter percent, on up to the current 1% in quarter increments, what we saw is that each one of those moments on the same day that the Fed allegedly hiked interest rates, they also increased the amount they were going to pay on excess reserves. So, now the banks have a choice. Am I going to keep money risk-free at the Fed or am I going to lend it to bank B overnight? Of course, they increasingly just chose to take the safe, sure money from the Fed, and so this is what’s different about this particular story, is that now when the Fed raises rates, not only does it not remove money from the system, but it’s actually adding more money to the bank system because it pays interest.

Two trillion dollars held at the Federal Reserve right now will generate at current rates, 20 billion dollars of interest income to the big banks on a yearly basis. That’s adding money, that’s not subtracting. So, it’s totally different.

Mike Gleason: Now, you recently wrote a fascinating piece on your Peak Prosperity site about how the Fed, in your view, is destroying America. You’ve alluded to some of those reasons but talk about this, Chris. Why do you believe this to be the case?

Chris Martenson: Because what they’re doing, it’s not just printing money, but they’re social engineering. They have to pick winners and losers. I know it sounds like the Fed prints money and does these crazy sophisticated things, or buys treasury at an auction, or does a reverse repo, and all these fancy names, but really all they’re doing is they’re printing money and they’re handing it out to the market and taking pieces of debt in return for that. So, when you really look at that dynamic, the Fed has been the engineer of the largest wealth gap that we’ve ever seen in all of our history at this point in time. It’s engineered one of the most, if not soon to be the most punishing income gaps.

It’s also purposely driven up the prices of houses which if you think about it, isn’t actually good for anybody except the very few people who sell and downsize, and capture that gain. It’s not good for first time home buyers, it’s not good for existing home owners who have to pay higher property taxes and insurance bills and things like that. But the Fed drove this up and created huge income disparities and really drove up the actual true cost of inflation in all the areas, metropolitan areas particularly, where these new private equity firms like Blackstone came in and just scooped up lots of properties. So, when you look at all of this, what is The Fed really doing?

Well, they’ve locked out the millennial generation pretty handedly. They’ve enabled the federal government to go forward with even more aggressive indebtedness, in taking on more debt. They’ve really encouraged, if not almost forced corporations to engage in financial engineering, because hey, if you’re a CFO, you can borrow 1% and retire dividend yield in stock at 2%, do that all day long. Makes total sense, but companies have been doing financial engineering, not productivity engineering. So, all of these things you can lay at the feet of the Fed, and listen, if they wanted to run six months, maybe 12 months of emergency interest rate cuts, back in 2008, early in 2009, I would have said okay.

But how long are we into this now, right? Depending on how you count it, we’re at least eight years into this thing, maybe nine, and that’s a pretty long emergency don’t you think? And all that’s happening during this emergency is we’re watching those things I just described, just get wider and wider, and wider. More financialization, less investment. Harder starts for students and millennials and other young people coming in, not easier. Really low business formations, because a trillion dollars of interest income didn’t go to people who are the traditional savers, the moms, the pops, the dads, grandmas, who then take their interest income, that trillion missing dollars and use that to help their sons and daughters and granddaughters and grandsons start businesses.

So, we’re seeing all of these effects, and of course, just the big mystery is that really it’s not talked about all that much yet, but it should be.

Mike Gleason: In terms of the metals, Chris, it’s been a decent but unspectacular year, despite what appears to be the ongoing price manipulation schemes of these bullion banks. What are your thoughts on the gold and silver markets?

Chris Martenson: Well, I’m just going to deviate slightly into the Bitcoin market, and noticed today, I think it’s around $2,300 or so. It’s been gyrating a bit, and I know it was higher recently, but just watching how those prices are actually behaving, that to me looks something like a free and fair market, right? You can actually watch and make sense of the movements in those markets. As you and your listeners really well know, that once the leverage paper market gets wrapped around any market, it’s now open to the players who want to control those markets to do what they will.

So, in my mind, really important article for everybody to read, two weeks ago roughly in the Wall Street Journal, we had that article about how the quants, all these people who have the math skills who can come in and write the algorithms that now run Wall Street. Those algorithms have access to huge amounts of capital, most of them are really trading at millisecond, maybe microsecond speeds, and they’re running around doing things in various markets, including the precious metals markets. I think those have been under basically the direct control of the bullion banks for quite a while, and it’s been their own personal piggy bank, if you will. And hey, that all makes sense, right? But as you know and as I know, those gains can’t go on forever, and at this point, I think gold and silver have found what feels to me like a base here, hopefully.

I have a strong sense that when this next financial crisis or paralysis comes along, that people are going to want safe haven assets at that point, and the safer the better. That’s because I think there’s institutional risk, possibly even sovereign risk. Things could really get hammered. Once you understand how extraordinary the leverage is in the system, and where the debts are distributed, and who is, who what, it really doesn’t add up well. So, if that gets called into question, guess what? Having precious metals is going to be a really important thing to do, and as we’ve discussed before, you’re going to either have them before that moment comes, or you probably won’t have them after. That would be my guess, seeing how quickly those markets can dry up.

Mike Gleason: Your website Peak Prosperity focuses on preparedness and self-reliant living. You can find communities there with interests ranging from investing to living off the grid. Are there any particular topics that members there are focused on at the moment? What are people interested in these days? We assume it isn’t all Washington D.C. politics all the time, so what are people in your sphere concentrating on these days, Chris?

Chris Martenson: Oh, good question, but we’ve been talking about a variety of things, all across the spectrum, really. At this particular juncture, we’re not spending nearly as much time on politics as you might think. What we’re pretty interested in is where the market’s going, what’s really happening across certain geopolitical areas, not U.S. politics, and interestingly, a third and growing area on our website is talking about how would you simply be in this world today?

Like, how we conduct ourselves, how are we living into the stories that unfolds, because these are brand new times. Increasingly, Mike, I’m running into people who get it. They’re like, “Ah, something is off in this story. We know it.” Some people understand it, some just feel it, it doesn’t matter. That’s really what a lot of us are talking about at Peak Prosperity now, is how do we stay focused? How do we stay in the game? How do live in a way so that we’re really enjoying ourselves today? But we’re also prepared for tomorrow, and so increasingly, I think it makes sense. This has been a fairly long, slow, topping process that we’re in right now, and I think there’s a sense here that we don’t know how much this can continue, right? It’s just tiring to be on alert all the time. What we’re talking about is how not to be on alert all the time, yet be prepared at the same time, if that makes any sense.

Mike Gleason: Well, as we begin to wrap up here, and before we get into some more of those details on your upcoming webinar, give us your thoughts on this period of calm before the storm that we appear to be in right now. Many were calling for a tumultuous year in 2017, coming off of the chaotic year we had in 2016, with Brexit and the crazy U.S. election and so forth, but to this point it hasn’t really materialized. What is it going to be that throws us off course, derails this historic rise in equities, and changes the economic landscape and then ultimately gets precious metals back into the consciousness of the investing public, Chris?

Chris Martenson: Well Mike, a lot of things could do it, of course, but what will do it is hard to say. This is a complex system. After the fact, people will point back and say, “Oh, it was when the German Finance Minister said that” or something, right? We’ll try and identify, but we have giant bubbles at this point in time. Nobody knows when bubbles are going to burst, and they always do it in a surprising way. It’s part of their definition. I’ve been thinking that this can’t go on much longer for a while, and it has, so I’m adjusting accordingly, and understanding, “Yeah, they’ve really got a pretty good sense of control on the system, but look how much it cost us?” Again, rewind. I think the most important information people can have is a trillion dollars had to be put into the system to basically hold everything elevated.

Slight gains, but really honestly, mostly just bumping along. That’s a really astonishing situation. I like to follow what the central bankers are doing, not what they’re saying. They’re saying everything’s great, but they’re doing emergency measures in the highest amounts ever. So, given all of that, I think it just makes a lot of sense for individuals to take action based on that, to make themselves prepared, make themselves more resilient, and there’s lots of things people can do. By the way, almost all of these things that we would recommend, if not all of them, are going to make your life better today. People will not look back on getting ready in the way we suggest, and say, “Gosh, I shouldn’t have got in shape. I probably shouldn’t have saved so much money. It’s too bad I have this functioning house.”

Nobody’s going to say that. So, I think this calm before the storm is the time that we use as the gift that it is. It’s still very easy, relatively speaking, to take whatever steps you want to take, and becoming prepared while things are really unraveling is a bad strategy. It’s hard to be efficient, it’s hard to be calm, it’s hard to be rational if you’re in the middle of all that when it happens. That’s been our advice, it’s been our advice for a while. Hasn’t really changed and I honestly, I don’t know how much longer this can go on. It’s surprised me every month of the way so far.

Mike Gleason: Yeah, you’ve got to fight that complacent, and then also like you mentioned, when things are unraveling, that’s not when you want to be just now starting to think about what you’re going to do in those situations.

Well Chris, thanks so much for your time and your wonderful insights. Now, we’ve touched on it a bit already, but talk about this upcoming webinar. When it is, who’s involved, and then share a little bit more about what you’ll be discussing, and then of course how people can registered for that, because it will undoubtedly be very worthwhile and informative. Give us the info there, if you would.

Chris Martenson: Sure. So, the structure is it’s a webinar, it’s about two and a half hours long. We have three special guests on there. Each one of those guests is going to speak for a period of time, and also there will be an opportunity for live Q&A for the participants who’ve registered for this webinar. The cost is $50 and the three guests we have are G. Edward Griffin, he wrote the book on the Federal Reserve, so he’s the author of The Creature from Jekyll Island, which I’m sure many of your listeners have read. We’ve got David Stockman, former head of the Office of Management and Budget under Reagan. Was a U.S. representative and a pretty frequent commentator on the macro conditions in the markets. He’s going to be helping us understand those conditions. Also, what’s happening in Washington D.C. because the politics here are probably going to shape Fed policy as they have for a while. Will the Trump tax cuts go through? What’s the infrastructure plan looking like? We’re counting on David for that.

And then, Axel Merk he’s the person who knows more Federal Reserve officials than anyone else I know. Both current and former, he just came back from a whole two or three day event where I think there were 20 Fed officials at, so he got to talk with them, and read the tealeaves and read the body language, so hopefully he’ll be given us some insights into what comes next.

Again, so this is on June 7th, it’s at noon, and it’s going to be a live webinar. So people who signed up for that also will be able to download and watch that later.

Mike Gleason: We’ve got a link to the webinar registration page from this podcast page on our site, and we urge people to sign up for that. It’s a truly great lineup of participants and it should be fantastic.

Well, excellent stuff as always, Chris. It’s been great to talk with you again and thanks for being so generous with your time today. Much success with the upcoming webinar, continued success with the book, and I hope you enjoy your summer, and I look forward to catching up with you later this year. Thanks very much, Chris.

Chris Martenson: Thank you so much.

Mike Gleason: Well, that will do it for this week. Thanks again to Dr. Chris Martenson of PeakProsperity.com and co-author of the book Prosper! How To Prepare for the Future and Create a World Worth Inheriting. Check out the site for information on that, as well as next week’s webinar on the “End of Money,” which is June 7th at 12 noon, Eastern Time. Just go to PeakProsperity.com/webinar for more information.

Mike Gleason is a Director with Money Metals Exchange, a national precious metals dealer with over 50,000 customers. Gleason is a hard money advocate and a strong proponent of personal liberty, limited government and the Austrian School of Economics. A graduate of the University of Florida, Gleason has extensive experience in management, sales and logistics as well as precious metals investing. He also puts his longtime broadcasting background to good use, hosting a weekly precious metals podcast since 2011, a program listened to by tens of thousands each week.

We “went walkabout” over the past several years, largely deserting the Precious Metals sector for other greener pastures, because it has been performing so poorly, apart from a dramatic flurry during the 1st half of last year. However, the latest charts suggest that a major bullmarket is incubating in the sector and that it won’t be much longer before it starts. This being so it is time for us to return to take positions ahead of its commencement.

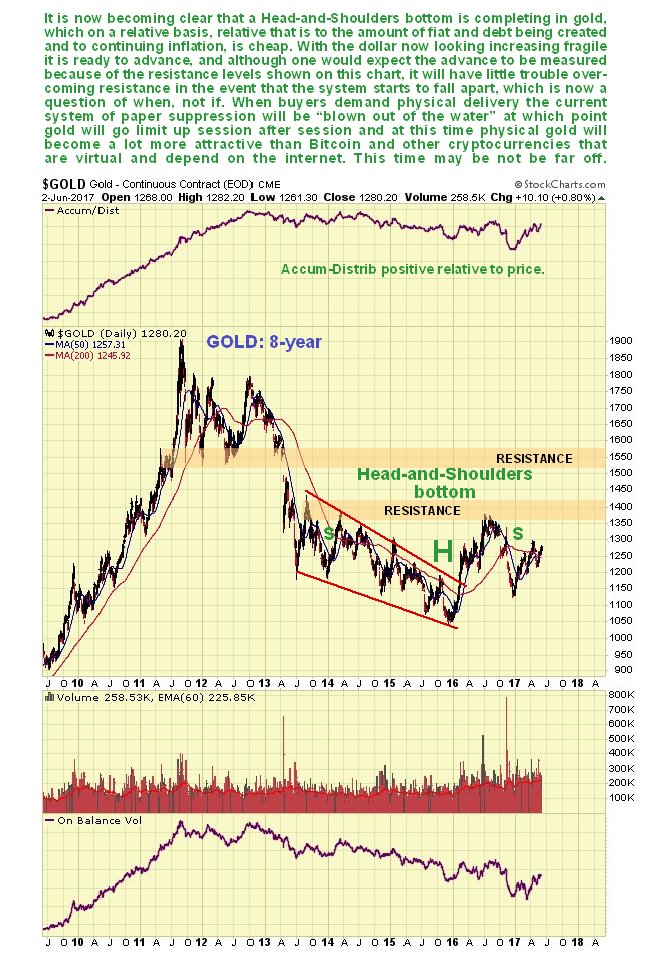

We will now proceed to look at the latest long-term charts for gold, silver, Precious Metals stocks and also the dollar to identify the signs of the impending major bullmarket in gold and silver. On the 8-year chart for gold it is now becoming apparent that a large Head-and-Shoulders bottom is completing, that started to form way back in 2013, so this is a big base pattern that should lead to a major bullmarket, and given what is set to go down in the debt and derivatives markets it should easily exceed earlier highs. With the benefit of this long-term chart we can also put the sizeable runup during the 1st half of last year into context – it was the advance to complete the “Head” of the Head-and-Shoulders bottom. This being so we can also readily understand why it then gave back about half of these gains – it dropped back to mark out the Right Shoulder of the pattern, and the good news is that with this late stage of the pattern now approaching completion, we can look forward to more serious gains soon. The new bullmarket will be inaugurated by the price rising above the 1st zone of resistance shown, although it will then have to contend with another major zone of resistance in the $1550 area. However, if the credit markets are coming apart at this time, this shouldn’t prove to be much of an obstacle.

The 8-year chart for silver is quite similar to that for gold, as one would expect, except that it is skewed downwards because silver tends to underperform gold during the late stages of sector bearmarkets and the early stages of bullmarkets, but it certainly looks like a good entry point for silver and silver related investments here, with it still only $4 off its lows.

The 8-year chart for the PM stocks index proxy, GDX, also looks very similar to that for gold, except that it is somewhat upwardly skewed, which reflects the wild excitement of speculators in this sector once they sense a turn. There was a really big percentage gain during the 1st half of last year as it came off a really low level, but as with gold what was happening was that GDX was rising up to complete the Head of the Head-and-Shoulders bottom pattern. Once it had done so a reaction set in which saw stocks lose about 50% of their gains before stabilizing, with this reaction serving to mark out the Right Shoulder of the pattern. Now it looks ready to advance up to the neckline of the pattern to complete it and set the stage for the nascent bullmarket to come, and just this part of the advance will result in big gains in many trampled down stocks, some of which we will be looking at in a separate article.

Despite the downsloping moving averages, there is evidence of coiling on the 6-month GDX chart, and this combined with the suspected bull Flag of the past couple of weeks could lead to a surprise strong rally soon…

Many are expecting the sector to weaken again, citing the falling 200-day moving average on the indices, poor seasonals until the end of June, and an expectation that the dollar will rally from oversold. With respect to these factors it is worth pointing out firstly as regards the falling 200-day moving average, that the high values at the peak around last August will soon drop out, causing it to flatten, especially if we see a rally. Secondly, the poor seasonals are a background influence, and didn’t stop the sector from advancing during June of last year. Thirdly, as we will now see, the dollar looks like it is tipping into a severe decline, oversold or not. On the 8-year chart for the dollar, we can see how the it broke out above resistance to new highs on euphoria over Donald Trump’s election victory, but it was subsequently unable to hold on to these gains, and has slumped back into the large trading range, a bearish development, particularly as the entire pattern from early 2015 now looks like a giant bearish Broadening Top. Having broken down back into the pattern and below its 200-day moving average, which is rolling over, it now looks like it will continue lower to the key support level at the bottom of the pattern, as a 1st stop, despite its already being significantly oversold. If it breaches this support there is some support lower down at the red trendline, which marks the lower boundary of the Broadening Top, but if it breaks below that things could quickly get a lot more serious.

On the 8-month chart for the dollar index we can see recent action in much more detail. This is an interesting chart for it shows that the dollar has been weakening beneath a parabolic trendline that is forcing it lower at an accelerating pace. There has been some talk about it forming a minor base here over the past week or two, and rallying from oversold, but it doesn’t look like that is going to happen. Instead the small tight pattern of the past week to 10 days looks like a bear Flag that will lead to another steep drop, and it started to fall quite hard again on Friday. Such a move can of course be expected to lead to gains in the Precious Metals sector.

Should we see the usual seasonal dip in the Precious Metals sector during this month and possibly into July, it won’t alter the Big Picture set out here and it should be seized upon as a buying opportunity, although what we are seeing in the dollar now suggests that the seasonal dip may not happen this year.

When the Central Banks finally lose control of propping up the markets, will the BIG MONEY be made in owning gold, silver or crypto-currencies? This is the question many investors who are focused on “alternative assets”, outside the typical mainstream stock, bond and real estate markets, are asking.

Most investors who have been concerned about the massively inflated Bubble Markets and the Greatest Financial Ponzi Scheme in history, have been investing in gold and silver. However, a new kid on the block, called Bitcoin and the other crypto-currencies, have gained a lot of attention due to the huge increase in their prices over the past few months.

So, now many investors are wondering what to make of these extremely volatile crypto-currencies and if they are nothing more than purely speculative and gambling vehicles. This is a logical assumption based on the massive spike in many of their crypto-currency values.

That being said, Charles Hugh Smith wrote the following in his article, Projecting The Price Of Bitcoin:

The wild card in cryptocurrencies is the role of Big Institutional Money.

I’ve taken the liberty of preparing a projection of bitcoin’s price action going forward:

You see the primary dynamic is continued skepticism from the mainstream, which owns essentially no cryptocurrency and conventionally views bitcoin and its peers as fads, scams and bubbles that will soon pop as price crashes back to near-zero.

Skepticism is always a wise default position to start one’s inquiry, but if no knowledge is being acquired, skepticism quickly morphs into stubborn ignorance.

Bitcoin et al. are not the equivalent of Beanie Babies.Cryptocurrencies have utility value. They facilitate international payments for goods and services.

This was very interesting analysis done by Charles Hugh Smith who is one of the more bright minds in the alternative media community. I have watched Bitcoin out of the corner of my eye over the past few years, but have not placed much attention on the leading crypto-currency. However, as the price of Bitcoin and crypto-currencies have surged over the past several months, I decided to take a closer look… to see what all the hubbub was about.

What I found out was quite interesting. Bitcoin’s price rise is not just based on mere speculative flows (as many assume), but rather it’s also rising due to the skyrocketing energy and capital costs to produce each coin. Yes, there is a lot more to this, but there is some METHOD TO THE MADNESS.

Charles Hugh Smith understands this and realizes that cyrpto-currencies will likely to continue to gain in price, interest and market cap going forward due to the way they were designed. Now, I am not saying I totally agree with Charles, but there is more behind crypto-currencies than just mere speculative flows into digital assets.

So, the question is…. where will the BIG MONEY be made when the Fed and Central Banks lose control of propping up the Markets? That’s a good question. Yes, the Central Banks will lose control because they are facing one force that they are unable to manipulate…. ENERGY.

While the Central banks can manipulate the oil price, than cannot manipulate the Falling EROI – Energy Returned On Investment that continues to decline. So, the more the EROI of oil falls, the more printing and propping up the markets the Central banks are forced to do. It is really that simple.

Thus, the END OF MARKET MANIPULATION has an expiration date…. and its not decades away. I wouldn’t be surprised that it takes place within the next 5-10 years… or even less.

To get an idea of the total current value of Gold, Silver and Bitcoin-Crypto-currencies, let’s take a look at the value of above ground gold and silver investment:

According to the data put out by the USGS – U.S. Geological Survey, GFMS, CPM Group and Kitco (market price), all the investment gold held in the world is worth $2.93 trillion versus $51.8 billion for silver. You will also notice that there isn’t much more above-ground investment silver in the world (2.59 billion oz) compared to gold (2.25 billion oz).

NOTE: The total global gold and silver value is based upon $1,300 for gold and $20 for silver

Now, if we bring in the total value of Bitcoin and all the other crypto-currencies, we have the following:

All the gold investment (including Central Bank and private investment) is approximately $2.93 trillion versus $89 billion for the total Bitcoin-Cryptos market cap and $52 billion for silver. So, the current market cap of Bitcoin-cryptos now surpasses the total global value of silver investment by $37 billion.

Of course, the Bitcoin-cyrpto market cap has increased significantly over the past few months. Common sense logic suggests the recent spike in Bitcoin and the other crypto-currencies will likely experience a large correction… thus a falling market cap. But, I agree with Charles Hugh Smith that these crypto-currencies will likely gain significantly over the next five years.

However, I also see the value of gold and silver rising considerably as well…. especially silver. The price of silver will likely increase in a much greater percentage because there isn’t much more physical silver in the world compared to gold, and its price is so low, that when large funds move into the silver market…. the huge pressure will be released by a much higher price.

There is a lot to understand about Gold, Silver and the Crypto-currencies going forward. Investors need to realize that while the crypto-currencies will likely see large gains in their values in the future, the BIG ENERGY PROBLEMS will are going to face may not be good for Cypto-currency network functionality. Again…. there is a lot of consider.

Which means… gold and silver will still be the some of the safest physical assets to own in the future.

Check back for new articles and updates at the SRSrocco Report.

As I was walking through the shopping district of Kingston-on-Thames yesterday, I was wondering whether the locals had gotten the memo that the country remained on “High Alert” in light of the Manchester bombings. Here I was in the middle of an historic “village,” walking across the Clattern Bridge (built in 1293) along with thousands of British shoppers, laughing and joking, sitting in pubs, talking about the rugby matches and generally going about their regular daily business as if nothing had happened. If I could have drawn little “thought balloons” above each and every person I observed, there would be one simple image of a raised middle finger everywhere. It was a wonderful, beautiful thing to witness.

It should come as no surprise to anyone that knows British history that, as my father used to refer to it, this “little peanut of an island” ruled the world under the British Empire for most of the 19th century, ceding superpower status only after WWII to the U.S. and Russia after ruling the waves from the mid-1700s. It was in 1939 that the British government designed a poster (shown above) intended to prepare the citizenry by “shaping morale” for the imminent arrival of WWII with an increasingly bellicose Germany. While the poster was rarely displayed publicly, it epitomizes the “stiff upper lip” mentality of nation and explains a great deal of the majestic history of the country. Of course, I am talking up my book as all four grandparents were from England and many of my partner’s first cousins are showing us around. For someone raised in a country barely 150 years old, to walk through churches built in the 1300s is awe-inspiring to say the least and intimidating at its best.

So as I attempt to make sense of today’s markets with rampant interventions and blatant manipulations all designed to “shape morale” and keep the citizenry at once both complacent and behaved, it is as if the global banking cartel, working hand-in-glove with governments, are preparing for a cataclysm of sorts—a financial tempest that will make the “Blitz” of 1940-41 over London pale by comparison.

By intervening in the gold and silver markets, they have been able to eliminate their usual “canary-in-the-coal-mine” predictive natures and by propping up stocks, bonds and real estate, the public is now juggling multiple bubbles in a manner not unlike the Roaring Twenties or the Late Nineties. One by one, I see the “Big Money” (Warren Buffett, Paul Tudor Jones, Ray Dallio) exiting the stock and bond markets, and hedge funds managers galore returning capital to investors as opportunities shrink and risk escalates. When you think about the fact the CNBC’s favorite ratings magnet, Warren Buffett, has now horded more then $100 BILLION “looking for better entry points,” you have to ask yourselves why Facebook shares at $150 with a 38 P/E or Amazon at $995 trading with a 187 P/E are not finding themselves in the portfolio of Berkshire Hathaway. Can all of these very seasoned players in global markets be wrong at the same time?

The days of traditional fundamental analysis may have metamorphosed but they are by no means “different” in terms of outcomes. Just as surely as quantitative analysis has altered the technical aspects of securities analysis, all it has actually achieved is a temporary Band-Aid over a cancerous lesion. That cancerous lesion is the inability of corporations listed on the public markets to actually deliver earnings that can be paid out in the form of dividends over time. Algorithms that use pattern-recognition software to trade markets are specialists in rearranging Band-Aids over thousands of these hideous lesions but the time is rapidly approaching when events such as government default, social insurrection, recession, geopolitical upheaval including war, and/or natural disaster will wash away those Band-Aids, leaving multiple exposures of the ill health of the body.

As Paul Singer said recently: “We think that the low-volatility levitation magic act of stocks and bonds will exist until the disenchanting moment when it does not. And then all hell will break loose.” That is precisely what I have been writing about through most of the last nine years dealing with serial intervention by central banks with checkered and sporadic periods of success and failure always finding solid FUNDAMENTAL reasons for trying to buy volatility (“VIX”/UVXY-US”) or to buy puts on the S&P 500. Many such efforts occurred as recently as last November when I took out pre-election hedges to protect against a Trump victory. By 10:30 p.m. on the night of the election, I was clinking champagne glasses with my partner and dancing around the room with Fido the Dog as my hedges, had they opened right then and there, would have been ahead over tenfold. I went to bed with a wondrous array of sugar plums dancing in my head only to awake to the horror of stocks opening unchanged. Since then, I have refrained from trying to trade against the Cretins because it has become a mug’s game of chronic head-banging and repeated rebukes.

That these interventions have cost us all a great deal of financial, intellectual, and emotional capital is in no way a sop to the significance of their criminality. However, the irony is that it has not affected the youngsters trained in the Millennial art of entitlement and self-indulgence. “Old people suffer bear markets; WE buy corrections” is the mantra of the day for tens of thousands of fuzzy-cheeked, selfie-obsessed traders and investors born during the first decade of the DotComs and the last decade of world-class mineral discoveries. The maddening part of it all is that the science of financial engineering studied and now-perfected by the dozens upon dozens of academics manning the halls of the global central banks have not only failed to experience the rapture of meeting payroll, they have never fully understood the delicate balance between the “real” economy and the “financial” economy.

Sadly, the latter has now overtaken the former in its significance not so much in its effect upon the bricks-and-mortar portion but more so in how it has grown to absolutely dominate policy, both fiscal and monetary. To wit, all simulative efforts enacted by the policy-makers, whether central bankers or elected officials, are now targeted toward bank collateral with the primary reflationary target being real estate.

Now that home prices in America are now approaching and in some cases surpassing the pre-GFC (2008) levels, the risk to the banking cartel has been mitigated by way of the reparation of the valuations of their collateral Achilles’ Heel. Now that the risk of balance sheet implosion has been transferred from the banks to the consumers and by natural progression, the government, stock and bond prices are able to levitate and remain at bubble-like plateaus. An interesting question might be how gold and silver might have reacted since 2008 had the major portion of bank collateral been gold versus debt.

So as we plough forward into the spring of 2017, the model portfolio I constructed in 2001 and one which I actually bought in 2002 has surprised everyone by actually outperforming the S&P 500 by almost twofold but it should be emphasized that physical gold has been the premier performer while gold stocks have not done nearly as well. The fact that gold continues to be acquired by the Asian and European central banks is testimonial to the fragility of the currencies they are empowered to protect. As I sit here in the middle of England typing in an inn built in 941 A.D., it is easy to be intimidated by the sheer history of the establishment, of the village, of the region, and of the country. It is also easy to be intimidated by the constant and consistent bid in global equities in light of the slowing macro picture and looming interest rate hikes.

It is disheartening to watch gold and silver holdings sitting in limbo while stocks and crypto-currencies like Bitcoin are recording new all-time highs. It is depressing to watch bubble after bubble inflate while new ETFs are launching every day that lever up existing leveraged ETFs. It is frustrating to read emails from many seasoned long-term followers that are in full liquidation mode having been rendered powerless to any longer stomach the smug cockiness of the CNBC crowd. To sit on the crypto-currency sidelines while witnessing the manic elation of the Bitcoin Battalion is for me the ultimate in aggravation. All of my haranguing and whining and raging about the demise of the global currencies over the years was actually taken to heart by the master code-writers of the tech world, but instead of those massive tech profits migrating to gold and silver, they wound up CREATING their own alternative currency that has actually sucked capital AWAY from the precious metals because it was and is insulated from the grappling hooks of the interventionalists.

However, as glum as it may appear, it is never, EVER, truly “different” this time or any other time and all of the time-tested reasons for owning gold and silver are not only intact, they are more powerfully relevant today than ever before. I do not say this lightly; it took a trip to the birthplace of my forefathers in order to fully understand where we are in the bigger scheme. One of my lifelong heroes, Sir Winston Churchill, said “‘Tact’ is the ability to tell someone to ‘Go to Hell’ such that they actually look forward to the trip.” He was a wonderful writer and was a published author long before he became a politician or a statesman. He had the uncanny ability to deliver scathing commentary upon foolishness. In an encounter with Lady Astor, she said to him: “Mr. Churchill, I think you are drunk!” to which he replied, “M’Lady, it is true that I am drunk but it is also true that you are UGLY. In the morning, I shall be sober BUT in the morning, you shall still be UGLY.” Yet again, Churchill is accused of being a chauvinist pig with the following recontre: Lady Astor: “Oh, if you were my husband, I’d put poison in your tea.” “Madame,” Winston responded, “if I were your husband, I’d drink it.”

I bring these nuances of human brilliance to the attention of my readers because I truly love “wit and intellect” with a passion. When you are forced to sit back and grind your back teeth as others around you are celebrating the ownership of stocks at valuation levels surpassing the highs of 2001 and 2007 and 1987, you must have a “Fall Back” position in order to maintain sanity. As we are not yet able to hold up a mirror and prove to the world that we have solved the puzzle surrounding the global debasement of currency purchasing power, it can in no way be seen as an analytical failure of the precious metals. Alternatively, we have to think in the same manner as Sir Winston. We have to think as independently and as reconstructively as he did when he told the British people what they should expect in the event that they could rebuff the German Luftwaffe in 1940-41. We as gold and silver investors have to think as adaptably as did Churchill when he told the British people that this would be “their finest hour.”

In this era of invasive central planning and congenital bubble-blowing, it isn’t easy to invest as a contrarian. It is even more painful to watch friends and colleagues dismiss overvaluation arguments because “it’s working.” And it is almost surreal to watch naive and unsophisticated Canadian “investors” sitting with $3 million in mortgage debt, five rented properties and plans to “buy more” while attending seminars and conferences with paid actors revving up overexuberant crowds.

Sanity can only be kept by remembering the mistakes of the past; focusing on time-tested methods; and by remaining vigilant. To do otherwise would be folly of great impact and consequence. When investing in today’s hyperventilating markets, I will vow to “Keep Calm and Carry On.”

Now it’s off to the Emerald Isle.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and images courtesy of Michael Ballanger.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair