Stocks & Equities

“Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.”

“Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.”

Given the media’s obsession with some of the President Trump’s communication challenges, it was utterly predictable that the President’s declaration that his trip to Europe and the Middle East should be considered a “home run” was met almost universally with ridicule. In truth, the President actually did accomplish a series of victories overseas, or at least laid important groundwork that should help advance American interests in ways that prior Administrations have failed to do. It’s a shame that these developments have been ignored among the din of partisanship.

From my perspective President Trump reasserted American leadership in the primary security challenge of our day, namely the defeat of radical Islamic terrorism. He also struck deals that could prove financial windfalls to U.S. industry. The President ran on security and prosperity and that was precisely the thrust of the trip.

Trump’s first stop was Saudi Arabia, the keeper of the most holy places in Islam, the most influential of the Sunni Arab states and the one with whom America has long enjoyed close relations. Over the previous eight years Sunni Arabs had been increasingly dismayed by the Obama Administration’s tilt towards friendship with Shiite Iran and her allies. (This change resulted in the Iran Nuclear Treaty which is widely despised among Sunnis.) Given that some had concluded that Trump had won the presidency on in part through anti-Islam rhetoric, his meetings in Saudi Arabia should do much to quell anxiety in America’s most important Islamic allies.

Possibly even of more significance was King Saud’s invitation to Trump to address the leaders of 50 Sunni Arab states, something never done before by a U.S. President. In his speech the President offered traditional American leadership, but in return demanded cooperation in the ideological battle with radical Islam. He exhorted Arab leaders to “Drive them out. Drive them out of your places of worship … your communities … your holy land … out of this earth.”

To achieve this he announced the opening of the new Global Center for Combatting Extremist Ideology to be located symbolically in Saudi Arabia. He assured his audience that while “America seeks peace-not war. … Our friends will never question our support and our enemies will never doubt out determination.” If any doubted Trump’s conviction, his ordering of a 59 Tomahawk Cruise missile strike into Syria on April 6th and the dropping of the CBU 43/B ‘Mother Of all Bombs’ in Afghanistan on April 14th, proved the determination of his words. All 50 national leaders signed an agreement designed to starve ISIS of international funds. This is an achievement that the mainstream press has bent over backwards to ignore.

But the biggest take away from Saudi Arabia may be financial. The Saudis agreed to a $100 billion arms purchase from the U.S. and a $400 billion joint investment in oil, gas, and high technology. Many have concluded that these deals could lead to the creation of hundreds of thousands of jobs in the U.S.

With positive accolades from the Saudis, Trump went to Israel for meetings with Prime Minister Netanyahu. While the President did not make any mention of a ‘two-state’ solution, the message was clear that Trump felt very positive that a long sought peace deal was possible between the Israelis and the Palestinians. Furthermore, in what appeared to be very friendly and positive meetings, he assured Israelis that America would “…never, ever allow Iran to possess a nuclear weapon.”

The most significant portion of the trip came when the President landed in Brussels for meetings with NATO leaders, who collectively represent America’s most vital allies. After a campaign in which candidate Trump famously asserted the obsolescence of the Post-war NATO alliance, the majority of the leaders in attendance were convinced that as President he would move past campaign rhetoric to adopt the pragmatism typical of American presidents. As such, it was expected that Trump would re-affirm the United States’ commitment to Article 5 of the NATO Treaty (that assures mutual defense if any single NATO member nation is subjected to outside attack).

To their dismay, Trump conspicuously failed to do so. This omission elicited palpitations on both sides of the Atlantic and caused many to conclude that the Western alliance had been permanently fractured and that the Russians had achieved their long awaited strategic triumph. This conclusion is laughably premature.

As an accomplished business negotiator, Trump knows that it is unwise to fold one’s cards while the hand is still in play. His real goal here is not to abandon Western Europe to the perils of Russian expansion but to compel wealthy European countries to finally pay for a commensurate portion of their own defense. For years many of these countries have spent far less than the 2% of GDP on defense as NATO membership requires. The neglect has been easy to make when these governments could be assured that a muscular Uncle Sam would always ride to the rescue regardless. As the old saying goes, “Why buy the cow when you get the milk for free?”

Undoubtedly Trump sought to create the ‘leverage of fear’ to force the cooperation of reluctant NATO leaders in meeting their defense spending targets. Following the initial shock, Trump’s attack appeared to have positive results. By the close of the NATO and subsequent G-7 meetings, many national leaders, including France’s new President Macron, who dined privately with Trump, appeared to agree that NATO must meet its defense spending commitments.

Trump also appears to have been successful in pushing the NATO allies in committing more resources in the fight against international Islamic terrorism. While ISIS has not yet been able to deploy weapons of mass destruction, it has instead been able to utilize a substitute: the weapon of mass immigration. It is likely that hundreds of ISIS cells live within NATO countries, where Muslims already have been given preferential treatment under local laws. The disgustingly barbaric ISIS attack in Manchester was mentioned repeatedly by Trump as a contemporary event in order to drive home the ever increasing, ever broadening global threat of ISIS. The Manchester attack may help stiffen the backs of NATO leaders in taking resolute anti-terrorist measures, including not merely watching but deporting known radical suspects. Again, it supported Trump’s long held stance on illegal immigration.

In the aftermath of the trip many have cited Chancellor Merkel’s remark that Europe must be more self-reliant as evidence of Trump’s failure as a world leader. But for those who have long believed the Translantic status-quo as both inequitable and inefficient, her admission may very well be a sign of his success.

The President’s trip can be viewed as the initial step of first isolating and then possibly forming a massive military U.S. led coalition of Sunni Arabs, Israel and NATO to defeat ISIS, while leaving Shite Iran and its nuclear treaty to be dealt with later. Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.

“This week I have good news and bad news for you” – John Mauldin

Centenarians Everywhere

The $400 Trillion Gap

A Wedding and the Virgin Islands

“I often joke that 100 years from now I hope people are saying, ‘Dang, she looks good for her age!’” – Dolly Parton

“Just because you live 20 years or 100 years doesn’t make it less meaningful. They’re both short amounts of time. So all we can do is just live in that time, whatever time we’re given.” – Ansel Elgort

“If I had more time, I would have written a shorter letter.” – Blaise Pascal, 1657 (and a few score other later attributions)

Welcome to the new, improved, faster-to-read, better yet still-free Thoughts from the Frontline. My team and I have been doing a lot of research on what my readers want. The reality is that my newsletter writing has experienced a sort of “mission creep” over the years. Bluntly, the letter is just a lot longer today than it was five or ten years ago. And when I’m out talking to readers and friends, especially those who give me their honest opinions, they tell me it’s just too much. There are some of you who love the length and wish it were even longer, but you are not the majority. Not even close. We all have time constraints, and I wish to honor those. So I am going to cut my letter back to its former size, which was about 50% of the length of more recent letters. (Note: this paragraph is going to open the letter for the next month or so, since not everybody clicks on every letter. Sigh. Surveys showed us it’s not because you don’t love me but because of demands on your time. I want you to understand that I get it.) Now to your letter…

This week I have good news and bad news for you. The good news is that you and your children will probably have much longer lives than you currently imagine. The bad news is that you’ll have to pay the bill for them.

I’ll explain what that means in a minute. First, let me thank everyone who helped produce this year’s Strategic Investment Conference, as well as all who attended. I know it sounds trite to say that this one was the best ever, but it really was. Every speaker brought a unique and valuable perspective, which the panels then mixed into new and even more interesting blends. Attendees asked probing and sometimes uncomfortable questions. I think everyone left Orlando bearing loads of new ideas.

If you missed SIC, you can still get our Virtual Pass. It gives you audio recordings of all sessions, all the slides that accompanied them, and written transcripts. It’s the next best thing to being there. Click here for more information and to place your order. We will close this offer in early June, so don’t wait too long.

I’m also pleased to announce that next year we’re taking SIC back to our old home at San Diego’s Manchester Hyatt. The dates are March 6–9, 2018. That’s just a little more than nine months away, so now is the time to start planning your trip. We’ll let you know when early bird registration opens in the fall.

Now, on to this week’s main course.

One of my team members pointed me to a World Economic Forum white paper called “We’ll Live to 100 – How Can We Afford It?” Regular readers know I’ve been saying we’ll live that long – and asking how we’ll pay for it – for several years now. It is good to see Davos Man finally catching up with me.

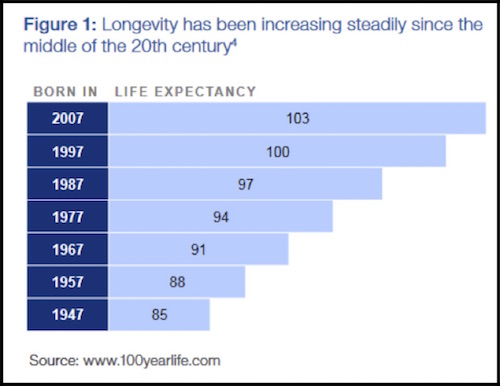

The WEF paper has some interesting data that I haven’t seen elsewhere. To begin, it breaks down life expectancy by birth year, showing a different picture than we see from simple averages. Here are the global numbers.

As far as I can tell, these estimates don’t consider the kind of major life-extending breakthroughs that Patrick Cox writes about for us and that he and I both expect to be realized in the next few years. Rather, the methodology of the WEF paper seems to depend on extending current trends. So I believe the numbers above are conservative.

Note also, these are median life expectancies, not simple averages. Half the people in each group will live longer than the median. Most of today’s young children will live to see the 2100s. Some (many?) of the younger Millennials will see their lives span three different centuries. That’s astonishing.

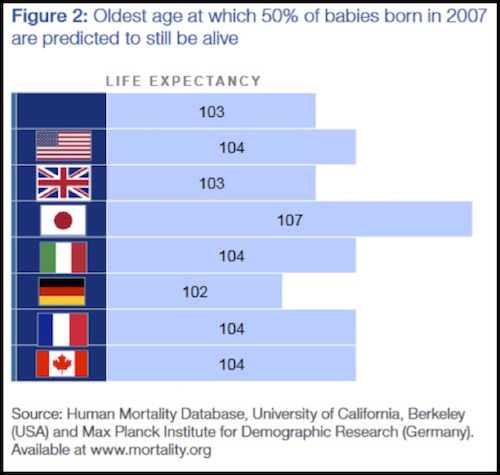

Here’s another table showing the differences among major countries for those born in the year 2007.

Again, this is astounding if correct. A Japanese child born in 2007, who is 10 years old today, has a 50% chance of living to 107. That will be the year 2114. Those in other developed countries are not far behind.

Better yet, the coming medical technologies will let us live to those ages or more without the decades of physical and mental decline that are now common. We’re not just increasing lifespans; we’re increasing “health spans,” too.

The good news is that many of those antiaging breakthroughs are going to be coming to a pharmacy near you in the near future – as in five to ten years. It is likely that you will live much longer and healthier than you are currently planning to. Most of us will be happy with that outcome. The bad news is that you will have to make your money last those extra years.

We had a panel at SIC with Patrick Cox and leaders of three of the biotechnology companies he follows. What they’re working on, from different angles, is almost unbelievable. It is entirely possible that we will see cancer wiped out in the next five years. Scientists are making huge strides with heart disease, dementia, spinal cord injuries, and the other great enemies of life and health. One by one, the dominoes are falling. Other companies we know about are working on the “Fountain of Middle Age,” whereby they intend to either delay or semi-reverse the aging process. It won’t take you back to your youth, but for many of us 50 years old sounds pretty good.

And there are groups like Mike West’s at BioTime, Inc., that are working on technologies like induced tissue regeneration (ITR), which will literally turn back your cellular clock. This was science fiction and a pipette dream 10 years ago. Today it is simply science, and it’s coming out of the theoretical stage and the petri dish and moving further up the experimental lab chain.

Some of you will object, “What will we do if everybody lives so long? Frankly, that’s a first-world problem. I see very few people who ask that question offering to die. If we live in a world that can figure out how to turn us young again, give us automated cars, and all sorts of abundant resources, you think we’ll have trouble figuring out how to feed everyone and keep them occupied? Malthus was so wrong in so many ways.

While this is wonderful news for humanity, it will bring some challenges, too. The world is not financially prepared to support as many retirement-age people as it will have to sustain in coming decades. We have some huge adjustments in store.

Specifically, we already have a huge retirement savings shortfall, both public and private. I discussed that problem at length recently in Part 4 and Part 5 of my “Angst in America” series. Adding millions more person-years to the equation will make the problem much worse.

The World Economic Forum’s white paper tries to quantify how much worse the personal retirement shortfall will be if current practices continue. The amounts presently earmarked for retirement income via government-provided pension systems (i.e., Social Security), employer plans, and individual savings fall far short of the mark.

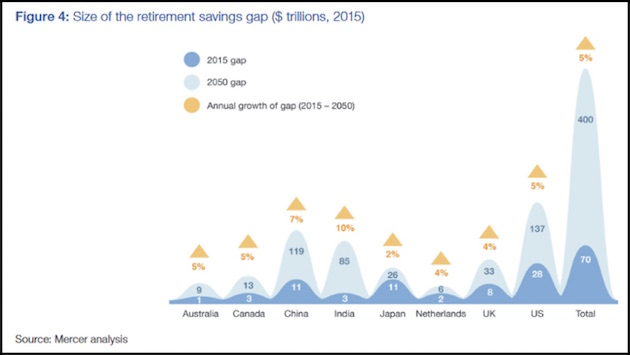

Here is the bad news in graphic form.

The bumps you see there are the difference between what is necessary to fulfill obligations (defined as 70% of pre-retirement income) and what has actually been saved or set aside to do so. The darker blue is the 2015 gap, and light blue is a 2050 estimate.

WEF shows these eight countries, which are obviously not the whole world, simply because the data was available. They also excluded assets held by the wealthiest 10% of the population, in order to show the situation of non-wealthy citizens. (Their full methodology is described on page 22 of this PDF file, for those of you who want to take a deeper dive.)

By 2050, the total shortfall in these eight countries alone will be $400 trillion. That number is so absurd that I feel very confident we will never have to face it. One way and another, some promises will be broken. The only questions are, whose and to what degree.

Remember, this is just the personal savings shortfall. This is not the government and unfunded liability shortfall. Globally, that runs into the multiple hundreds of trillions on top of the $400 trillion savings shortfall.

The present standard of retiring somewhere between ages 60 and 70 is not going to be sustainable when half the population lives to 80 or 90 – which is already realistic today – let alone 100 or more. It’s just not possible. If you’re like me, you don’t intend to retire at 70 or maybe not at all, but it’s nice to know we have the option. Future generations won’t.

According to WEF, the global dependency ratio under current policies will plummet from 8:1 today to 4:1 by 2050. That means just four active workers for each retiree. And that’s including developing and frontier markets. Developed markets will see a global dependency ratio of about 2:1. I see no way that can work. WEF doesn’t either. Here is their advice to political leaders.

Given the rise in longevity and the declining dependency ratio, policy-makers must immediately consider how to foster a functioning labour market for older workers to extend working careers as much as possible.

There you have it, straight from Davos. We must “extend working careers as much as possible.” Your dream of hanging up the work clothes at 65 and going on extended vacation will remain a dream until some later date. Early retirement will survive only for the kind of people who go to Davos.

Again, for me this is fine. I’m 67 and I love my work. I plan to keep at it for many years to come. But I understand many people don’t have that option. They have health problems, or their professions are being automated, or they spent their career doing physical work that is no longer possible. The medical advances I foresee will help, but they’ll take time to become affordable to everyone. Some people are going to fall through the cracks.

Moreover, simply saving more money probably isn’t an answer, either. Interest rates are a function of supply and demand. You can’t invest your savings in a high-yield bond unless someone out there can borrow at that same yield. When so many of us want to lend and no new borrowers appear, supply and demand will keep yields low. We already see this in today’s near-ZIRP conditions, and they may not improve much.

Part of the justification for ZIRP was that it would force capital into risk assets, thereby stimulating the economy. It now appears that the only thing stimulated was asset prices, and by and by the risk is going to catch up with those taking unwise amounts of it. That unhappy outcome will likely widen the retirement shortfall even further.

And so the expectation of longevity is going to motivate people to want to save more money, except they’ll have to have jobs that pay enough to enable them to save money to flesh out the retirement plan. This headline appeared a few weeks ago:

Oops. The Council of Economic Advisers now estimates that artificial intelligence will replace 83% of low-wage jobs. I’m not certain how they came up with that number – it seems high – but whatever is the figure turns out to be, it’s alarming. And the jobs we are creating today are not the high-paying manufacturing jobs that everybody wants to “bring back.” They’re not there to be brought back. There is actually a quite large “re-shoring” movement going on, but the companies that are coming back are doing so with automated technology and far fewer workers than before. The advantage of using inexpensive offshore labor has fallen before the advantage of being close to your markets and “employing” robots and artificial intelligence.

The McKinsey Global Institute published a report last December that said: “On a global scale, we calculated the adoption of currently demonstrated automation technologies could affect 50% of the world economy’s 1.2 billion employees and $14.6 trillion in wages.” That is an astonishing statistic.

By the way, one of the subheads in that screenshot above points out that 61% of financial services positions are at high risk of being replaced. If you are in the financial services industry, maybe you should be thinking about how you can keep from being automated out of a job.

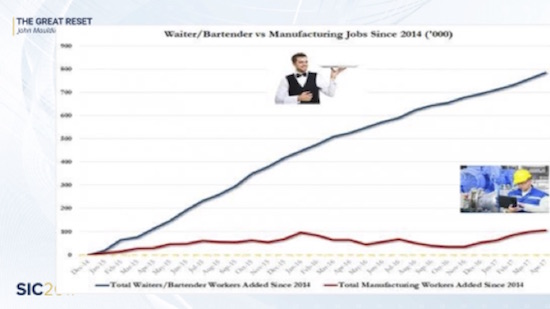

The jobs we are creating? Think 800,000 waiters and bartenders versus 100,000 manufacturing jobs. I have children who work in the food service industry, and I can tell you they are making barely enough to provide for themselves, let alone raise a family or save for retirement.

Officially, the US unemployment rate is 4.3%. There are 200,000+ manufacturing jobs that employers can’t find suitable, highly skilled candidates to fill. Last year, the labor force participation rate declined by another 0.2% to 62.7%. The employment-to-population ratio fell to 60%. Fewer of us are working and making enough to actually be able to save for retirement.

In other words, I don’t think we can invest our way out of this. The obvious answer – extend the retirement age – has the unwelcome side effect of reducing job opportunities for younger workers. At some point that might be okay if low birth rates create widespread worker shortages, but the adjustment will take time.

The solution may turn out to be something presently unimaginable. We don’t know where technology will take us and what opportunities it will create. We also don’t know what political alliances can create. What if the next time around we got not just President Bernie Sanders but a Bernie Sanders-compatible House and Senate? Could we see a wealth tax in addition to a whole slew of other taxes? Would our dear leaders be willing to tax your retirement plan so that people without adequate savings could enjoy a more pleasant retirement? Forget fairness to you as an individual, because they will be arguing about fairness to everyone in the country. Yet today the Republican majority refuses to consider instituting a value-added tax and lowering income taxes and corporate taxes to very low levels. They could do this, because they now have a majority. They are simply afraid of a VAT and are going to find themselves in far less sympathetic hands in a future crisis.

What we do know is this: An unsustainable situation will not be sustained. Retirement as we know it is unsustainable. It will give way to something else, and maybe soon. Frustration is building in America because of the problems I highlighted above, and we could well see an administration and Congress that will push through a much less friendly VAT plus income tax increases, not cuts.

Think it can’t happen? When your back is against the wall and you’re down to your last few bullets and the enemy just keeps coming, you start to very quickly consider all sorts of options. Within 10 years we are not only going to be thinking the unthinkable, we will be doing the unthinkable. And not just in the US but all over the world. The unthinkable will be coming to a country near you, along with unbelievable science-fiction-grade technology.

Count on it.

A Wedding and the Virgin Islands

I’m not doing much traveling this month until Shane and I go to the Virgin Islands the last week of June. On Monday, June 26, she celebrates her birthday. Since I asked her to marry me on her birthday last year, we are going to get married on her birthday this year. Just the two of us on the beach, and the rest of the week relaxing and thinking of the future together. While this approach does allow me to only have to remember one important day rather than two, I am informed by many friends that it does not relieve me of the responsibility to buy two presents.

Shane and I have lived together for four years now, and she has pretty much figured out how I operate. She has amazing forbearance and patience – she not only puts up with my peripatetic lifestyle; she even allows me to withdraw into my chair to read or to sit in front of my computer all day writing. Not exactly the most exciting of activities.

We will stay in the Virgin Islands for eight days and then come home to a full schedule. And I’m fully committed to begin to bring together the various chapters of my book, The Age of Transformation. That project will hopefully benefit from my new commitment to write fewer words per letter. Maybe I can do that for a chapter or two of the book as well. The reality is that each chapter could almost be a book of its own. I have to make sure I don’t get carried away. The book will not be a deep dive but rather a sweeping pass over the transformations that are coming to our world, not just technologically but also socially, demographically, politically, and especially geopolitically. The economic world will be turned upside down as we make decisions to do previously unthinkable things to get clear of the enormous debt burdens and bubbles we created.

And with that I must hit the send button. You have a great week.

Your determined to be more succinct analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

0:00 – 5:01: Michael Campbell’s Editorial: Protecting listeners from the fallout from the most dramatic historical change in generations that Michael sees coming. As JP Morgan said ” You can ignore economics and finance, the scary part is they won’t ignore you”.

5:35 – 12:22 – Michael Levy on the Top 3 Stories Smart People Are Talking About. One shocker, how low the Royal Bank sees the CDN Dollar dropping dramtically against the US Dollar by the end of the year!

13:14 – 17:45 – In this Week’s Big Fat Idea has a special interview with Eamon Percy and his book: The book is The 1% Solution – How Small Daily Improvement Produce Massive Long Term Results.

0:00 – 18:03 – Michael’s featured Guest: Joseph Schachter, Money Talks oil and gas expert who has been so accurate on the major Oil swings in the last 2 years. Michael’s asks Joseph how to time the energy market and the critical question of when we can expect the next bottom in Oil. Also which clues will tell us the trend has turned – and most important, which companies to consider adding to your portfolio at the turn. A must-listen too interview given the state of the oil market right now.

19:44 – 21:13 – Michael’s Shocking Stat: Whoa, taxpayers are going to foot the bill for this Government spending mystery! No explanation why a 26 Billion dollar expenditure exploded to 65 Billion since 2008!!

23:58 – 30:27 – Hot Properties: Ozzie on the change in Government in BC and what it might mean for real estate, not just in BC but also in Alberta.

30:54 – 34:02 – Live From The Trading Desk: Victor’s opinion on Joseph Schacther’s take on the oil market (hint, Victor thinks Joseph is brilliant). Also what to do with the stock markets of the world blasting to new all time highs, the US Dollar that just closed with a weekly key reversal down. Victor thinks the US Dollar is sitting on a knife edge and that its next move is going to effect a lot of markets.

34:25 – 35:36 – Michael’s Goofy: This week’s Goofy answers 3 questions, 1. What institution is the leader of the pro-life movement? 2. Who is the world leader of the Global pro-llfe movement?. 3. the answer to this question is the Goofy

Although frontier markets are a small subset of the emerging market universe, we think they represent an important constituency that offer some compelling potential opportunities. Here, I’ve invited my colleague Carlos Hardenberg, senior vice president and director of frontier markets strategies at Templeton Emerging Markets Group, to outline some of the opportunities he sees in these dynamic markets and debunk some of the urban myths.

Although frontier markets are a small subset of the emerging market universe, we think they represent an important constituency that offer some compelling potential opportunities. Here, I’ve invited my colleague Carlos Hardenberg, senior vice president and director of frontier markets strategies at Templeton Emerging Markets Group, to outline some of the opportunities he sees in these dynamic markets and debunk some of the urban myths.

There are a number of urban myths about frontier markets (the less-developed subset of the emerging-market universe). We think these myths may have caused investors to overlook them in favour of developed or traditional emerging-market alternatives.

We believe conditions are now ripe for a re-evaluation of this important niche. There are some very compelling reasons why many investors might want to take another look at frontier markets today. These can be summed up as the following, which I will delve into further.

- Expectations for robust economic growth

- Continued macro development

- Deep discounts in valuations

- Low correlations

Busting the Urban Myths

Recently, lots of news items have been discussing the run in the US equity markets and “how long can it go on like this?”. Our analysis of the markets shows us that many of these industry analysts are failing to consider one very important factor in much of their results. We wanted to share this with you through our own analysis so you have a clear picture in your head regarding the potential for US equities.

In our opinion, most of the industry leading analysts are developing conclusions based on Keynesian models that fail to adjust to recent disruptions in the global markets. Keynesian theory is focused on aggregate demand and the variations of this demand factor through normal and recession/depression economic events. In simple terms, as economies falter, Keynes suggested demand would suffer as a result of constrictions within the overall economy as a natural factor. His theories were radically opposed to those of the times (early 1900s) and proposed that government intervention to support demand would provide a more substantial economic recovery as savers would be converted into consumers and economic activity would inherently increase.

These theories have become entrenched in global economics and have been put to the test recently with the 2001 and 2009 market meltdowns. Yet, we believe something unprecedented has taken place recently and most of the industry analysis still fail to understand the affects and results of these clear indicators. First, Central Banks have backed this recovery with over $18T (globally) over the past 7+ years – a massive amount of capital investment. Second, M2 Money Velocity has decreased dramatically over the past 7+ years (to levels not seen in 50 years).

Interestingly, M2 attempted a slight recovery between 2003~2005 at levels much higher than statistically normal levels over the prior 40+ years. This move is very telling in the sense that capital supply post 9/11 was resulting in healthy M2 velocity acceleration – a sign of a healthy and organically growing economy. As M2 Velocity begins to increase, the economic engine is revving up on its own. After the 2009 market crisis, though, M2 Velocity has fallen dramatically and this tell-tale indicator is indicating that we have yet to see the economy begin to REV-UP. When it does, it could be a dramatic and explosive move.

In our opinion, the recent warnings from industry analysis of a potential “end to this run” or “end of the Trump Bump” are failing to understand the fundamental capital process that is taking place right now. In simple terms, the global Central Banks have injected nearly $18+T of capital into the markets that is searching for healthy returns. Much of this capital has been used to pay down corporate debt and to provide a recovery in the ailing housing markets. Additionally, much of this capital has been deployed into restoring financial order and capabilities within foreign governments and banking institutions. Therefore, we can assume that a portion of this capital has already been deployed into suitable fundamental support systems. Yet, a large portion of that capital is still searching for capital opportunity and will transition as the marketplace identifies healthy opportunities.

It is our opinion that we are about to enter a phase of a super-bull run that may last for an unknown period of time in certain markets. We believe the US, Canadian and UK markets are uniquely positioned to take advantage of this opportunity because they inherently support mature and structurally functional economic systems. We believe other, shorter-term, opportunities will present themselves in other foreign markets as dynamics shift that represent uniquely healthy economic investment. Just as quickly as these dynamics shift from one opportunity to another, the capital deployed into these opportunities will shift equally as fast.

We do expect market pullbacks and minor corrections to occur throughout this phase of the super-bull run. It would be foolish to think that this transitional shift in capital deployment would not be without some risk. We believe any positive rotation in the M2 Money Velocity indicator will be a strong sign that “capitulation of capital process” is beginning to take hold and become the turbo-charger of the mature markets (US, CAN, UK). Until this happens, our analysis is structurally sound and functional, yet it is missing the component that will create the “super-bull event”.

See for yourself how the market is reacting within these channels and try to understand that capital will always seek to find healthy economic environments that support adequate ROI. Given the amount and scope of capital that has recently been injected into the global markets, we believe the only locations this capital will find for adequate ROI will be the mature economic systems with the capabilities to innovate, lead and adapt to global market inconsistencies.

While I feel the equities market will run out of steam later this summer July/August, there is a case for the super bull-run, the ultimate wall or worry fueled by renewed M2 velocity and a recovery at some point. Take a look at the chart below because a bull market like this could be happening again and catch everyone off guard:

Do you want to learn how to profit from our detailed analysis of the markets? Visit ATP and learn how we can help you understand market dynamics, opportunities and develop clear objectives for success.

By Chris Vermeulen

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair