Currency

Strengths

- The best performing precious metal for the week was silver, climbing 2.36 percent and just beating out gold’s price performance as softer economic data emerged.

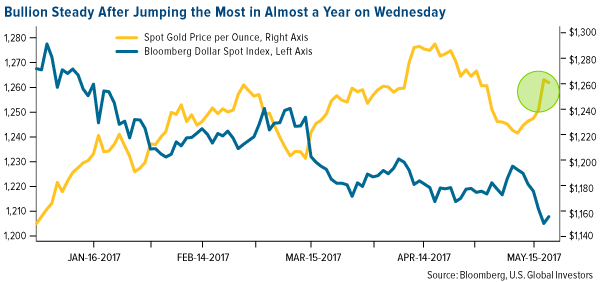

- Gold traders and analysts are split on their outlook for gold, reports Bloomberg, with 12 bearish, three bullish and four neutral this week. On May 16 the yellow metal advanced for a fourth day, with Kotak Commodities Services saying gold is supported by “mixed U.S. economic data, weakness in the U.S. dollar, geopolitical tensions and uncertainty about Trump’s policy actions.” On the prior Friday, consumer prices (excluding food and energy) rose 1.9 percent year-over-year for April, the least since 2015, while retail sales were also weaker, reports Bloomberg.

- Eldorado Gold will “gain an operating foothold in its own country with a deal to take full control of Integra Gold Corp,” reports Bloomberg, offering the equivalent of C$1.2125 for each Integra share. That is a 52 percent premium to Integra’s closing price on May 12, according to a statement on Monday from Eldorado. The proposed acquisition provides Eldorado with its first operating mine in Canada, offering G&A and income tax benefits, along with exposure to a lower political risk project, notes a Viii Capital report.

Weaknesses

- The worst performing metal for the week was palladium, down 5.87 percent. UBS noted that electric cars will be brought to the market sooner than consensus expectations and that platinum group metals are expected to lose market demand on this technology adoption.

- Barrick Gold reached an agreement with the Dominican Republic government (where it operates its Pueblo Viejo mine), outlining new financial terms and tax rates, reports Bloomberg. The new terms show the government is projected to receive an additional $181 million from Barrick between 2017 and 2019, according to a statement from the Dominican President’s office. The new terms are based on a gold price of $1,275 per ounce.

- Sibanye Gold Ltd. announced it will sell around $1 billion of shares at a 60-percent discount to partly fund its purchase of Stillwater Mining. The statement soon sent the stock plummeting the most in five months before rebounding after, reports Bloomberg. “The South African miner dropped as much as 11 percent in Johannesburg, the most since December 9, before paring losses to trade 2.4 percent lower,” the article continues.

- Frankfurt-based Commerzbank AG is exiting its physical precious-metals trading and services business, reports Bloomberg. The bank’s physical services include trading of physical precious metals, refining services, vaulting and transportation. Commerzbank does plan to continue its other bullion banking operations.

Opportunities

- Author and investor Mark Faber says that for the first time in a long time he is more heavily weighted in Europe than in the U.S. Faber cites “good opportunities in European stocks” at the present time along with his belief that the euro will continue to strengthen against the dollar. In a Bloomberg phone interview, he continues by stating, “In my opinion in the U.S. they will launch QE4 at the end of the year. The economy in the U.S. is weakening.” He also noted that gold mining shares are “inexpensive” and Amazon is “expensive.”

- Since President Trump’s comments about the dollar being “too strong” back in April, the greenback has since dropped – the Bloomberg Dollar Spot Index has fallen 3.1 percent, reports Bloomberg. Citigroup, the world’s biggest currency trading firm, believes continued erosions for policy changes in D.C. will only lead to further weakening of the currency, the article continues. Even Westpac Banking Corp., the second most-accurate currency forecaster in Bloomberg’s recent rankings, is advising clients to sell the dollar, with Macquarie Bank expecting the greenback to decline as well. Gold traded near a two-week high this week, with equities in retreat “and in

- Bullion markets are staging a tentative recovery, reports Bloomberg, with the number of holes drilled at gold deposits steadily rising for more than a year, according to S&P Global Market Intelligence. For example, exploration has jumped around 50 percent in parts of Argentina for lithium mainly, but also for gold. “When prices fell, exploration budgets were slashed, which means the industry had limited scope to grow,” said Goldcorp CEO David Garofalo. In a similar note from Bloomberg, mining companies lured back to Ecuador after a ban on large projects was overturned, “will welcome news that the incumbent mining minister is set to continue in the role under President-elect Lenin Moreno.”

Threats

- Despite the world’s largest gold-mining companies posting their best profit margins in four years, the biggest ETF linked to producers (the VanEck Vectors Gold Miners ETF) has seen net withdrawals this month of $617 million, reports Bloomberg. During 2016, investors poured record amounts into the ETF, but now it seems the gold rally has faded, with prices lower by 10 percent from 2016 highs. “Some companies are finding it more difficult to tighten their belts further, diminishing prospects for increased cash flow,” the article continues.

- Staff was evacuated and production was suspended at one of the two Banro Corp. gold mines in eastern Democratic Republic of Congo on Thursday, reports Bloomberg. A gunman left three people dead, making this the fourth assault on the company’s operations in eight months. Namoya is the company’s second mine in eastern Congo, beginning production back in January of 2016.

- Acacia Mining will start its three-year process of closing down its Buzwagi mine in Tanzania, reports Bloomberg. According to an emailed statement from the company’s communication manager, the mine will be shut down by 2020, leading to as many as 100 job cuts. At current gold prices, Acacia is not able to increase the life of the mine past the year 2020. Back in March, the Tanzanian government issued a ban on concentrate exports that Acacia said cost the company over $1M a day.

Last Friday’s CoT for the Comex Metals was rather interesting from a historical perspective. Because of this…and because we know that not everyone listened to Friday’s podcast…it seemed appropriate to type up this written summary today.

Before we begin, it is VERY important to note the restrictions that have been deliberately placed on this info by the CFTC. Even though the Commitment of Traders reports are surveyed at the Comex close each Tuesday, the CFTC purposefully waits 74 hours before releasing the data to the general public. As you consider the degree to which the “regulators” at the CFTC are complicit in the ongoing price management and manipulation, ask yourself why it takes a handful of dedicated public servants 3 days to crank out these spreadsheets: http://www.cftc.gov/dea/futures/other_lf.htm

Also, we are going to assume that this data is accurate. There have been occasions in the past where the CFTC has put out some numbers that seemed odd and inconsistent to those of us who follow the reports weekly….only to have the CFTC come back the following week and correct their “mistakes”.

And lastly, never assume that this data is sacrosanct and honestly reported by The Banks. Over just the past three years, JPMorgan has been fined on several occasions for knowingly submitting false data:

- https://www.bloomberg.com/news/articles/2016-03-23/jpmorgan-fined-by-cftc-for-failure-to-submit-accurate-reports

- http://www.cftc.gov/PressRoom/PressReleases/pr6968-14

OK, now that we have that behind us, let’s take a look at last Friday’s report and point out a few of the important points.

Let’s start with Comex Digital Gold (or as we call it here, “CDG”). As you assess where price may go from here, please consider the following:

- Over the past three reporting weeks, price has fallen by $35 or nearly 3%.

- During this time period, the Large Speculators in CDG have reduced their NET long position by over 71,000 contracts or about 37%.

- As of last Tuesday, when this latest CoT was surveyed, the Large Spec NET long position was just 126,724 contracts and the Commercial NET short position was just 142,859 contracts. These are the lowest NET positions since the CoT survey of February 21, 2017.

- At 142,859 contracts NET short, the Commercial NET short position has been trimmed by more than 1/3 in just the past three weeks.

- Perhaps most importantly from a historical perspective, at the recent price highs of July 5, 2016, the NET long position of the Large Specs was 316,037 contracts and the NET short position of the Commercials was 340,207. Ask yourself how high might price rise if these 200,000 Spec longs return to the Comex over the next few months?

Finally, for CDG, consider this chart:

Now let’s turn our attention to Comex Digital Silver or “CDS” for it’s here that the changes are rather eye-opening. Let’s lay some of them out as we did above for CDG:

- Over the past five weeks, price has fallen by $1.58 or about 8.6%.

- During this same time period, the Large Specs have reduced their NET long position by over 62,000 contracts or about 59%.

- As of last Tuesday, the Large Spec NET long position was just 43,004 contracts and the Commercial NET short position was just 57,337 contracts. These are the lowest NET positions since February 2, 2016.

- At 57,337 contracts, the NET short position of the Commercials has been cut almost exactly in half over the past five weeks from an alltime high total of 114,4141 contracts on April 11.

As you can see, just as in Comex Digital Gold, the recent CoT changes in Comex Digital Silver are significant. But, there are a few more remarkable datapoints you need to know. Again, these are from the report surveyed last Tuesday and released late last Friday:

- Here at TFMR, we like to look at what we call “The Large Spec Net Long Ratio” when we consider the “bullishness” or “bearishness” of the survey. All we do is take the summary positions from the silver report and divide Spec longs by Spec shorts. The lowest ratio we’ve ever recorded came from the CoT surveyed July 21, 2015. On that report, the Large Specs in silver were long 66,576 contracts and short 62,331. This produced a ratio of just 1.07:1.

- On February 28, 2017, we observed the highest ratio we’ve ever seen at 6.04:1. This ratio was still 4.99:1 five weeks ago with the CoT surveyed April 11. As of last Tuesday, the ratio is all the way down to just 1.75:1 and this is the lowest Large Spec Net Long Ratio we’ve seen since January 19, 2016.

- At 112,949 contracts, the GROSS short position of the silver Commercials is the smallest since the CoT of April 5, 2016.

- The GROSS short position of the Large Specs stood last week at 57,138 contracts, up from 26,454 contracts five weeks ago. But that’s not the interesting part. Consider this: At 57,138 contracts, this is the largest Large Spec GROSS short position in silver since the CoT Survey of August 4, 2015.

As in CDG, let’s put this data onto charts. See below:

In the end, what does all this mean?

Well, I suppose you could make the case that these most recent selloffs have washed out any “excess Speculator bullishness” that might have been present a few weeks ago. The CoT could also imply that upside potential now outweighs downside risk. However, for the reasons listed back at the beginning of this post, no one should ever make a trading or physical purchase decision based upon CoT info alone.

That said, given the similarities the current CoT structure has to the CoTs of late 2015 and early 2016, it seems safe to conclude that the prices of CDG and CDS are very close to…or have made…new bottoms. History suggests that the turnaround may not be immediate but the next price move from these lows could once again be substantial.

TF

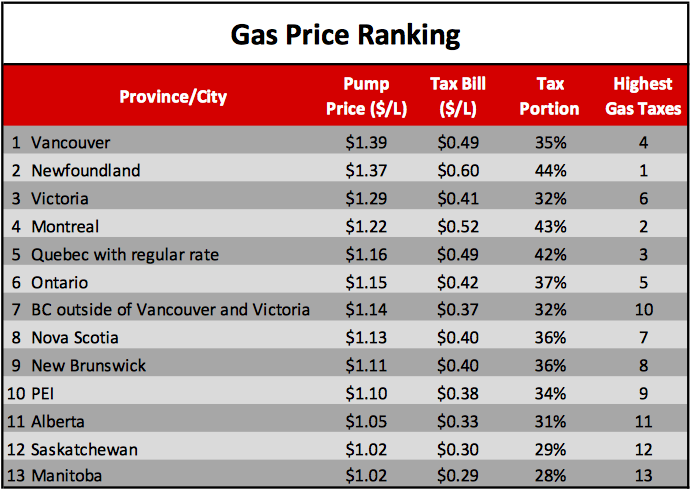

Everyone loves to talk about gasoline prices, usually incorrectly assumng that the biggest gasoline cost factor is the price of oil. That’s why when oil prices fall they demand to know why gas prices didn’t fall proportionately. The go to answer is to blame greedy businesses, but the truth is that taxation is the biggest gasoline cost factor in most markets.

Both provincial and federal taxes on gasoline make-up about 36% of the at the pump cost. One of my favorite add-ons is paying GST on top of the other gasoline taxes. According to an illuminating new study by the Canadian Taxpayer Federation, the federal and provincial tax-on gas tax adds an extra 3 cents per litre on average. All told governments take in an extra $1.4 billion in revenue thanks to paying GST on the taxes.

Okay, maybe that’s not my favourite – as the Taxpayer’s Federation reminds us we still pay the temporary 15 cent per litre deficit reduction levy that was implemented in 1995. Temporary my ass, so far that little beauty has brought in $13.3 billion since inception. This year alone it will bring in $638 million.

The grand total of fuel taxes is a whopping $23.5 billion in 2017.

If you are wondering how much you pay in gas taxes check out the table below compiled by the Canadian Taxpayers Federation:

source: The Canadian Taxpyer’s Federation’s 19th Annual Gas Tax Honesty Report May 18th, 2017

Michael Campbell

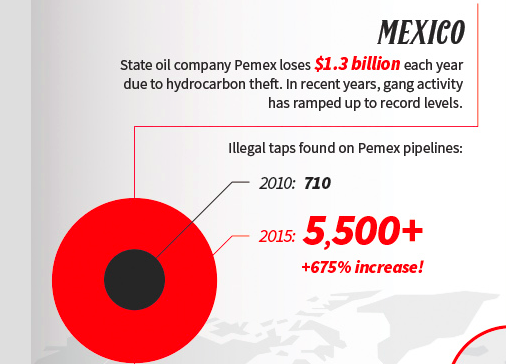

1. Crude Awakening: The Global Black Market for Oil

1. Crude Awakening: The Global Black Market for Oil

The value of the crude oil production alone is worth a staggering $1.7 trillion each year. Eventually, everybody wants a piece of the pie, includng politicians, military personnel, and police who are complicit in the outright theft of oil. Tapping pipelines….

2. An Impending Economic And Financial Disaster

An extremely low VIX level, like the current one, is signaling an eventual sell-off that I believe will be quite extreme.This event always generates a lot of press, and this year’s event was no exception. Here are a few of what I think are the most-interesting takeaways from Berkshire meeting.

3. An Unexpected Change In Gold’s Seasonal Trading Pattern

One of the interesting things about the Great Recession was how Canada’s financial system sailed through it largely unscathed. Its banks were regulated wisely and behaved prudently, its citizens avoided the extreme stupidity of their credit-addicted neighbors to the south, and its government refrained from doubling its debt every eight years.

But instead of Americans learning from Canada, Canadians appear to have concluded that we had it right after all.

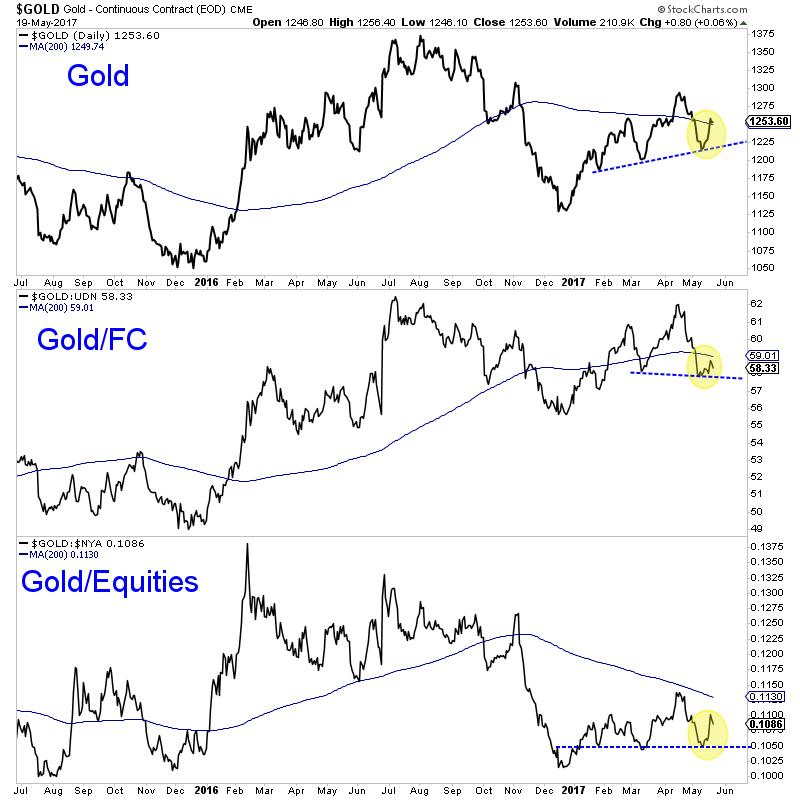

The precious metals complex rebounded as expected after becoming very oversold just a few weeks ago. The rebound has been aided by weakness in the US Dollar, which plunged roughly 2% over several days. However, upon further inspection Gold’s rebound has been entirely dollar-centric. Gold has remained weak in real terms and strength in the gold stocks and Silver has been rather muted. In short, the lack of much stronger performance in the face of US Dollar weakness bodes for increasing downside risk over the near term.

Gold’s recent strength has been driven entirely by Euro strength and not due to falling real interest rates, its primary fundamental driver. Macron’s win in France coupled with recent strength in European markets has supported what was an oversold and depressed Euro. This has supported Gold in US Dollar terms but only in those terms. As the chart below shows, Gold has been weak when measured against foreign currencies and equities.

The above chart shows that Gold remains well below its spring high near $1300 despite the US Dollar breaking its spring lows to the downside. In addition, Gold remains rather weak relative to foreign currencies and equities. The one hope for Gold would be a falling stock market and sustained strength in the Gold/equities ratio. While I expect that eventually, I do not think it is in the cards yet.

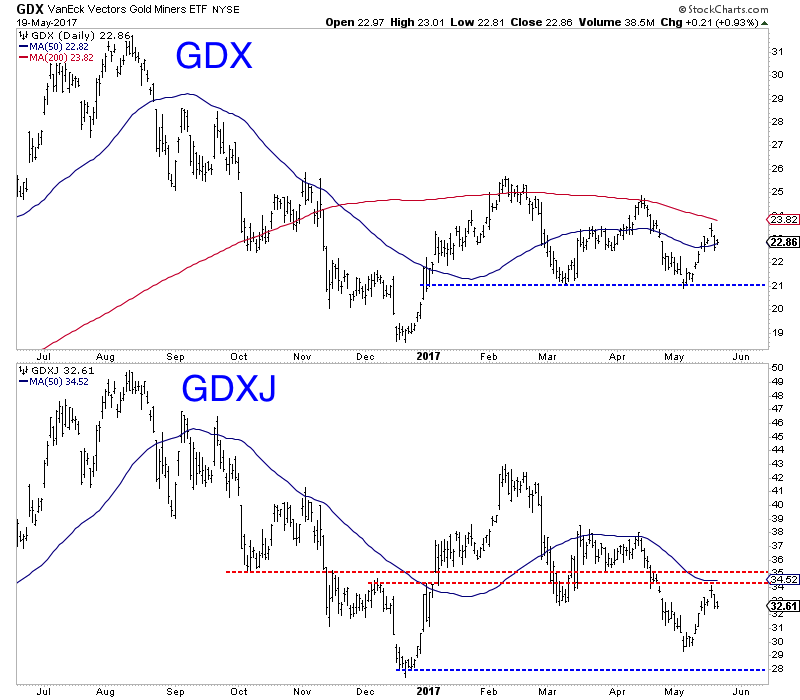

Turning to the gold mining stocks, we see immediate downside risk as the miners appear to have completed their oversold bounce.

Over the past few weeks GDX and GDXJ rallied 13% and 17% respectively and retraced a good chunk of their April decline. However, they now appear ready to decline into June and the upcoming Fed meeting. For the first time in months, GDX was unable to touch its 200-day moving average, which is already sloping down. Support for GDX is at $21 and $18-$19. Meanwhile, GDXJ peaked at its 50-day moving average and strong resistance at $34-$35. Its next strong support level is the December 2016 low.

If precious metals were about to blast off due to US Dollar weakness it would have already happened or precious metals would at least be showing much more strength. The greenback fell to a 6-month low yet the entire complex (ex Gold) is nowhere close to 6-month highs and remains well below 200-day moving averages. (Gold is trading right around its 200-dma). This is a warning sign as the sector could be quite vulnerable to a rebound in the US Dollar. We continue to wait as we expect lower prices and a good buying opportunity in select juniors at somepoint this summer.

Jordan Roy-Byrne CMT, MFTA

Learn more about our premium service including our current favorite junior exploration companies.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair