Asset protection

Marc expects also markets to rally from present levels, advises to buy on near term dips, the markets will likely top out in July/August. Considers a further rebound in the Euro due to the extreme pessimisim.

One of the interesting things about the Great Recession was how Canada’s financial system sailed through it largely unscathed. Its banks were regulated wisely and behaved prudently, its citizens avoided the extreme stupidity of their credit-addicted neighbors to the south, and its government refrained from doubling its debt every eight years. It certainly looked like Canadians were smarter – or at least more emotionally mature – than we were.

But instead of Americans learning from Canada, Canadians appear to have concluded that we had it right after all. In the decade since the global financial system’s last near-death experience, Canadians have started to behave like turbo-charged Americans. A few recent examples:

Canadians Are Buying A Record Number Of New Cars, With A Record Amount Of Financing

(Better Dwelling) – Sales of new motor vehicles across Canada rose to an all-time record for February.

Average Sale Price For New Vehicles Rises

Consumers are purchasing more expensive vehicles too. Over $5 billion was spent on new vehicles for the month, bringing the average to $40,100 – up 3.4% from the same time last year.

Consumers Are Buying “More Car Than They Can Afford”

The uptick in average sale price is due to longer financing terms for buyers. According to the Financial Consumer Agency of Canada (FCAC), Canadians are “increasingly purchasing more car that they can afford,” due to longer financing becoming fashionable. The agency notes that average leases have crept up 2 months, every year since 2010. According to the Bank of Canada (BoC), the average loan was 74 months as of 2015. Longer terms bring down monthly payments, but increases the total cost of the loan.The Rise Of Non-Prime Lending In The Auto Industry

The right to debt seems to be a topic all Canadians are embracing, and the auto sector is no different. The BoC has estimated that 25% of borrowers are non-prime, which in case you didn’t know is Canadian-English for “sub-prime.” These buyers generally have a FICO score below 670, and face predatory loans with up to 25% interest. This makes it difficult to build positive equity on car loans.————————–

Over half of Canadians are $200 or less away from not being able to pay bills

(Global News) – More than half of Canadians are living within $200 per month of not being able to pay all their bills or meet their debt obligations, according to a recent Ipsos survey conducted on behalf of accounting firm MNP.

“With such a small amount of wiggle room, any kind of unanticipated hardship, such as a job loss or even a car repair, could send an already struggling family into financial despair,” said Grant Bazian, president of MNP’s personal insolvency practice, which is one of the largest in Canada.

For 10 per cent of Canadians, the margin of error when it comes to household finances is even thinner, at $100 or less.

But those with anything at all left at the end of the month were in better shape than many: A whopping 31 per cent of respondents said they already don’t make enough to meet all their financial obligations.

Many Canadians don’t understand how interest rates work

Another hair-raising finding from the survey: Roughly 60 per cent said they don’t have a firm grasp of how interest rates affect debt repayments.————————–

Toronto Real Estate Speed-Dating Event Helps Strangers Buy Houses Together

(Huffington Post) – The Toronto real estate scene is nothing short of nuts, as prospective homebuyers with jobs and tens of thousands of dollars in the bank are still getting shut out the red-hot market.

Many buyers are pooling their financial resources to enter the market, and co-ownership is becoming increasingly popular.

Toronto realtor Lesli Gaynor, who has a background in social work, has launched GoCo, a service dedicated to helping people find homes they can afford in Toronto through co-ownership.

“I sort of came to it through watching people be shut out of this market for all kinds of reasons — but mostly financial,” she told HuffPost Canada in an interview.

She primarily works on helping people find others to purchase property they actually want to share and live in, though not necessarily as roommates (i.e., not sharing a bathroom and kitchen).

To connect potential co-homebuyers, Gaynor held a “speed-dating” event called “C-Harmony: Creating Co-operative Connections” at a Toronto pub on Thursday. About two dozen people attended, according to the Toronto Star.

Matt Michaels, who attended the event, told Global News he would love to own a home in the High Park or Roncesvalles areas, and is “open to the idea of owning a home with like-minded people.”

“As a 35 year-old who doesn’t have $400,000 for a down payment right now, it’s increasingly unlikely I would be able to do that on my own,” he said.

Buying with strangers is a feasible idea, but it just “needs to be normalized,” says Gaynor. She pointed to Meridian Credit Union’s recent creation of a friends and family mortgage, and said many lawyers are adapting to write covenants that protect both parties.

“It’s going to catch on, it’s just a matter of normalizing it.”

Some thoughts

Yep, this is both crazy and familiar.

In one sense Canada is just the latest victim of global hot money flows. Rich people in unstable countries like China or Russia are always looking for safe places to stash what they’ve earned or stolen. And their wealth in the aggregate dwarfs the capacity of a Brazil or a Switzerland to absorb it. So when it really starts flowing it distorts the target market in ways that seem like fun for the recipients at first but eventually turn into a nightmare.

Now it’s Canada’s turn, as the fortunes created during China’s post-2008 credit binge flee in anticipation of the inevitable bust. Much of that cash is flowing into Vancouver and Toronto real estate, leading to the insanity chronicled above and much, much more.

Canadian homeowners find themselves becoming rich beyond their wildest dreams and spend accordingly while renters find themselves priced out of the market for shelter, devoting an ever-larger share of their income to rent and sinking deeper into financial insecurity. Those are the people who are one emergency away from bankruptcy.

This divergence between the haves and have-nots begets all kinds of societal ills, from financial speculation to political upheaval. And – so far at least – the targets of hot money flows have yet to figure out a solution. The money pours in, screws everything up, then pours out, causing a crisis.

If anyone deserves better, it’s our likable northern neighbors. But hot money, like the rest of life, is not fair.

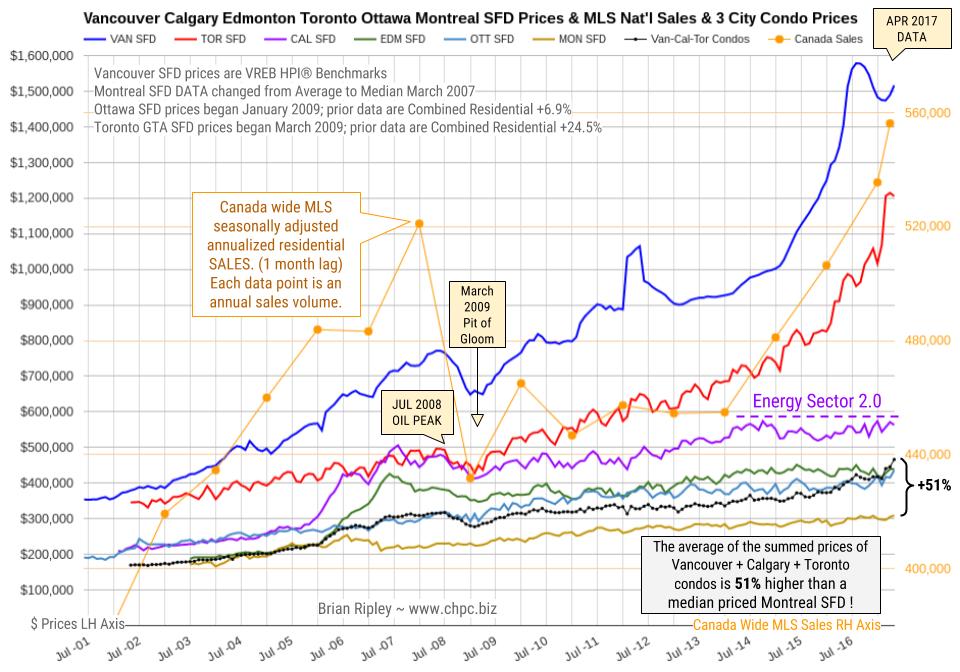

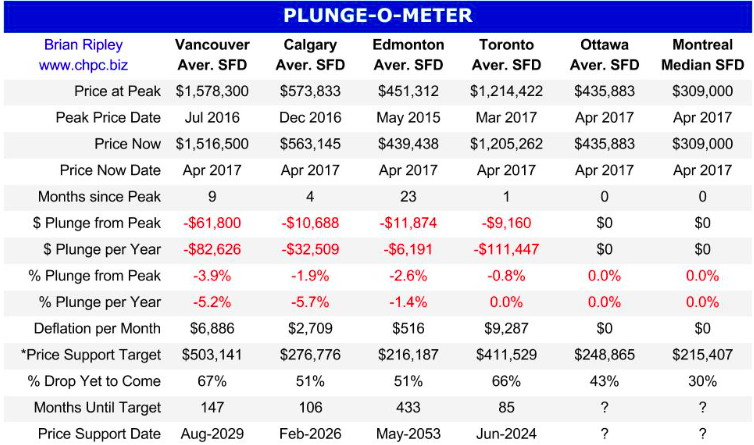

In April 2017 Canada’s big city metro SFD prices coiled about or slid off their near term highs except in Ottawa and Montreal where detached houses fetched new peak prices. Anyone owning a detached house in the scorching hot Toronto and Vancouver markets is sitting on an unredeemed lottery ticket.

In Calgary prices are labouring under the new Energy Sector 2.0 as the oil majors head for blacker fields; big money is fleeing Canada (and has been for nearly 20 years) and on the street, Calgary buyers are avoiding condo units in favour of townhouses and detached properties.

Many people don’t recognize the true value of an individual’s contribution to society until he or she is gone.

Many people don’t recognize the true value of an individual’s contribution to society until he or she is gone.

That’s not quite the case with our colleague, Larry Edelson. He did have a large, loyal following before he passed away. But it still applies to him in this sense: The Edelson Institute he founded now has an even larger group of devoted fans than he had.

I’m among them. And as I dig more deeply into his big-picture forecasts, I uncover even stronger evidence that supports them.

A classic example: Larry’s prediction of the coming sovereign debt crisis. Repeatedly and consistently, he told us how it would strike in three distinct phases — first hitting the European Union, then Japan, and finally the United States.

He explained how it would corrode society, corrupt politics, and raise the risk of war. Plus, he predicted what’s widely known today as the global money tsunami, the tidal wave of flight capital flowing into U.S. markets.

Now, the Edelson scenario is unfolding in aces and spades.

That’s why two weeks ago, I gave you the answers to five critical war questions, including the names of three defense giants that stand to benefit the most. It’s why last week, I showed you how the crisis is unfolding in the European Union (New, Bigger Shockwaves in Europe). Plus, it’s also why today’s the day to look ahead to the next big phase …

A Volcanic Sovereign Debt Crisis in Japan

Most people seem to have forgotten how massive Japan’s economy still is. Its GDP is double that of the United Kingdom, India and France. It’s three-times larger than Canada’s. Moreover, with nine of its banks among the 100 largest in the world (compared to ten in the United States), its banking sector remains among the most powerful in the world.

Yes, China’s economy has surpassed Japan’s in terms of sheer size. But compared to China, Japan is far more integrated into the global financial system and it will impact it more directly, especially during a sovereign debt crisis.

The big elephant in the room: Japan’s government debts are off the charts!

I witnessed this phenomenon firsthand. I was there in 1980 when the debt problem first emerged in a big way. I launched and edited Japan’s first newsletter on global bond markets. And I talked to virtually everyone who understood how serious the problem could become.

|

Even back in 1980, many feared that Japan’s giant government debts could strangle its economy, sink the stock market, or worse.

They didn’t want to talk about it publicly, themselves, but they implored me to write about it in the strongest possible terms.

“If we complain too loudly,” they said, “it could damage our relations with the Ministry of Finance and the Bank of Japan. But as a gaijin, you’re kind of expected to be more outspoken. So don’t pull any punches!”

Here’s the irony: In those days, Japan’s government debts were only 50% of GDP. Now, they’ve soared to 239% of GDP, or nearly FIVE times more. (See chart.)

That’s far bigger than the debt load weighing down on Greece (close to 160%) or Italy (about 130%). Plus, it’s nearly double the debt burden of the U.S. government and its agencies.

“Wait just a minute,” I said to Larry when he first made this argument years ago. “Japan and the United States are not directly comparable because Japan’s households save a huge portion of their income, which helps finance their deficit. America’s households save far less.”

True? When Larry and I first talked about it, yes. Now, absolutely not!

Over the years, Japan’s household savings rate has plunged from 20.4% of disposable income to a meager 2.4%. (See red line in chart.)

|

In contrast, the U.S. savings rate has declined gradually from 13.3% to 6.2% (blue line). In other words …

- Japan’s savings rate used to be close to double America’s.

- Now, in a radical reversal, it’s less than HALF of America’s.

Sound alarming? It should. Because if you multiply the risks illustrated in the two charts, you’ll see that the danger in Japan is far greater than most analysts think.

Risk #1 comes from the sheer size of the debt problem, which is 1.7-times worse than the United States (239% versus 138% of GDP).

Risk #2 comes from the scarcity of domestic savings to finance the deficit, which is over twice as bad as in the United States.

Result: All else being equal, their sovereign debt crisis could be about four-times worse! (And ours won’t be a piece of cake either; America’s government debt load is, itself, the worst of all time.)

How could that impact U.S. investors? For an answer, just remember that bond markets around the world are closely linked: When bond prices collapse in Japan, that crisis can easily spread like a contagion to U.S bonds as well.

Everywhere in the world, heavily indebted governments will have to …

- Pay a lot more to borrow money from the public, driving all interest rates higher, or …

- Raise taxes and cut spending dramatically, a big blow to their already-sagging economies, or …

- Some combination of both.

Bad for bonds. Bad for stocks. And bad for investors who are overcommitted to either.

Just don’t assume that this is going to happen all at once. The crisis could ramp up slowly at first and then erupt when least expected.

To make sure you’re prepared, stay tuned to the free updates provided by The Edelson Institute.

Good luck and God bless!

Martin

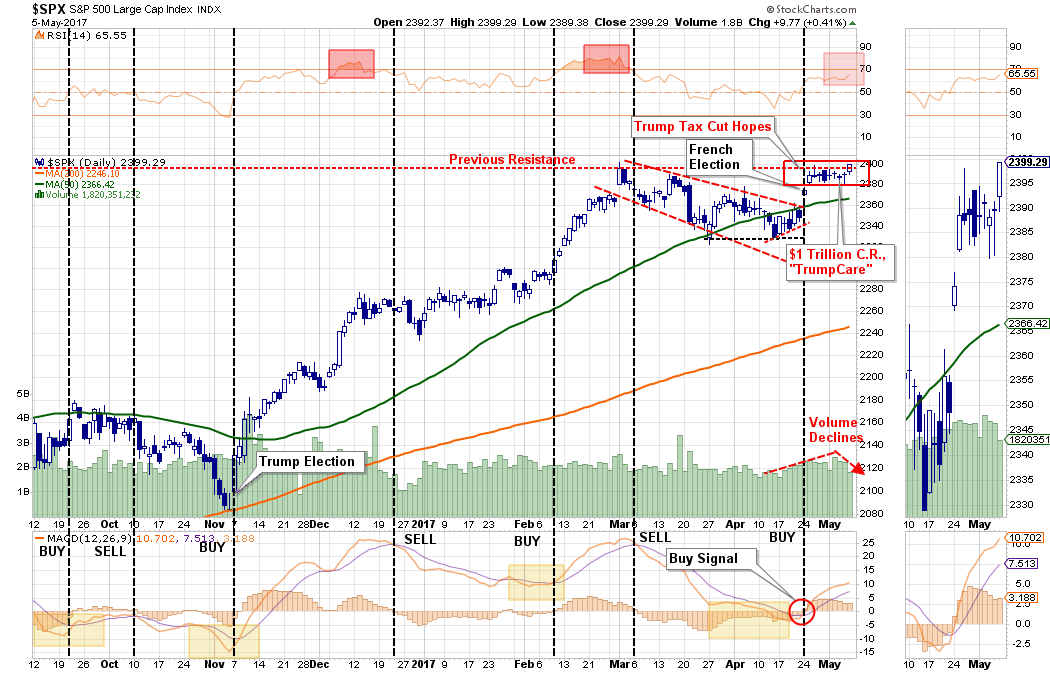

In this past weekend’s newsletter, I discussed the relatively “weak” breakout of the market to new record highs. To wit:

“Over the last few weeks, I have been discussing the ongoing consolidation process for the S&P 500 from the March highs. (For a review read: “Oversold Bounce Or Return Of The Bull,” and “Return Of The Bull…For Now.”) As the expected rally in stocks, and reversal in bonds, took shape as the S&P 500 was finally able to ratchet a record close at 2399.29. (Read: 10/2016 – “2400 Or Bust”)

“With the market on a short-term ‘buy signal,’ deference should be given to the probability of a further market advance heading into May. With earnings season in full swing, there is a very likely probability that stocks can sustain their bullish bias for now.

The market did do exactly that this past week, and while hitting a new high, as noted above, it was a ‘weak’ breakout as volume contracted.”

The question for the bulls, of course, is whether the current “breakout” is sustainable, or, is it a “fakeout” that reverses back into the previous trading range? As Steve Reitmeister from Zack’s Research suggested on Monday:

“I would say it all depends on investor confidence that tax breaks are on the way.”

It all hangs on just one issue.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair