Stocks & Equities

Quick take: At the end of April the inflation-adjusted S&P 500 index price was 97% above its long-term trend, unchanged from the previous month.

About the only certainty in the stock market is that, over the long haul, over performance turns into under performance and vice versa. Is there a pattern to this movement? Let’s apply some simple regression analysis (see footnote below) to the question.

…also from Advisor Perspectives:

May 2, 2017

- Gold and silver currently have a bit of a fundamentally and technically oriented “hangover”.

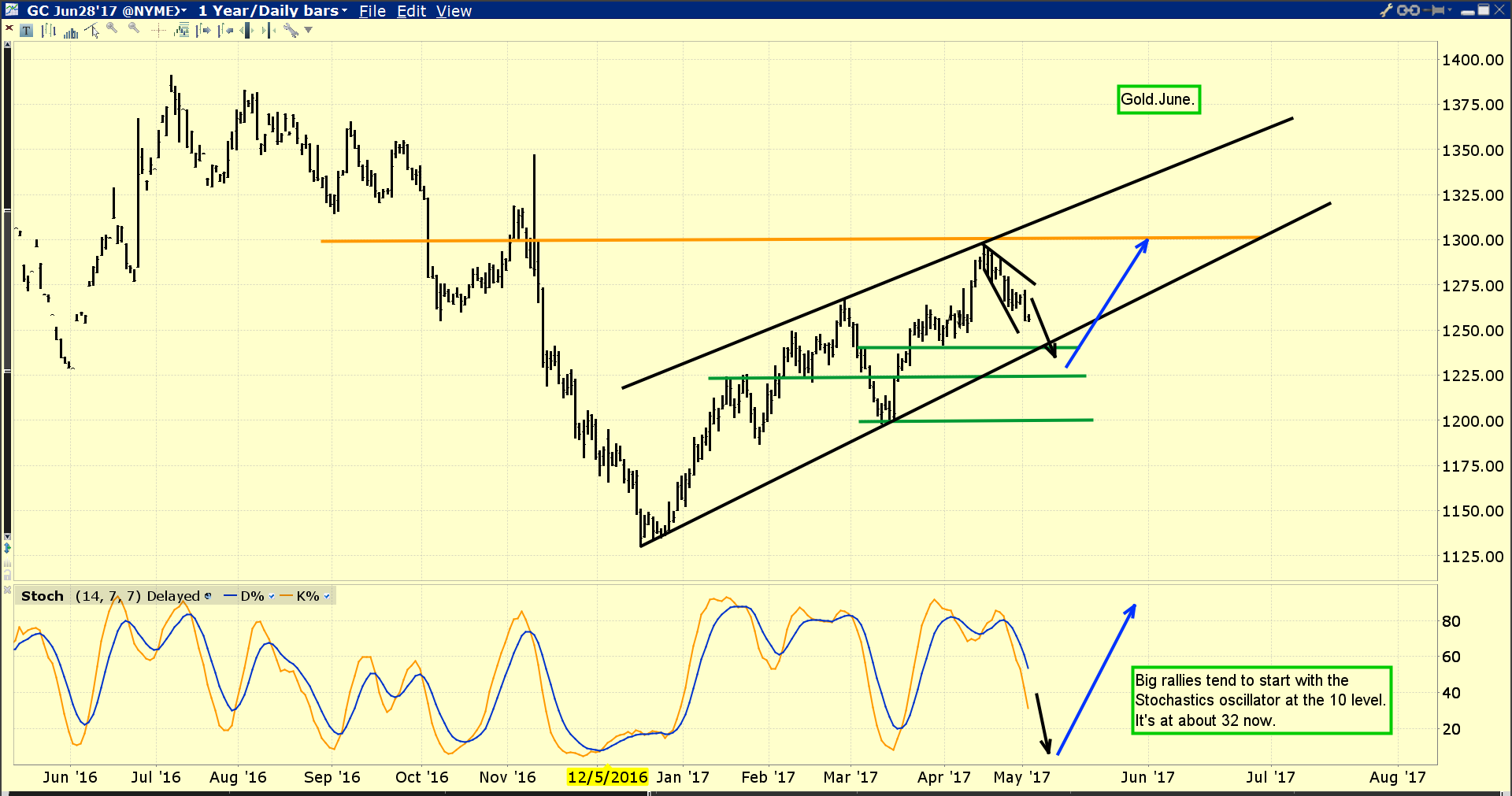

- Please Double-click to enlarge image below. From a technical perspective, gold is recoiling from the weekly chart downtrend line and a daily chart overbought condition.

- The Stochastics oscillator I use for the daily gold chart is the 14,7,7 series. It’s now at about 32, and decent rallies tend to begin after it’s declined to about 10.

- From a fundamental perspective, gold is in between rate hikes in America. It tends to rally after a rate hike, and be soft before the hike. That’s the case right now.

- The next FOMC meeting is on Wednesday. I expect Janet Yellen will hint that the June rate hike is not a sure thing, and that will do nothing to alleviate the current price softness.

- Also, the next jobs report is due to be released on Friday. Gold has a rough general tendency to decline ahead of the jobs report, and then rally after it is released.

- So far, gold is reacting with “textbook” price softness ahead of this jobs report. All members of the world gold community should cheer that it rallies with textbook strength once this report is released!

- The end of Indian dealer stocking for the Akha Teej festival is probably the biggest reason for the current “wet noodle” gold price action.

- Dealer stocking in preparation for the festival was incredibly strong and created the gold price rally to the $1300 area.

- Unfortunately, while Indian citizens bought decent amounts of gold for the festival, it doesn’t appear to be as much as the dealers bought.That’s created a lull in the market.

- Please click here now. Double-click to enlarge. That’s a shorter term look at the gold chart.

- Note the broadening pattern that has been in play since gold recoiled from the $1300 area high. These types of patterns tend to be resolved in quite a violent fashion.

- I carry short positions in gold that will only be covered if gold trades under $1000 an ounce. I hope I never cover these positions, but no analyst “knows” where gold is going for 100% sure, including myself.

- The wise investor carries some market positions that are essentially bets against their own outlook, and that’s what my short positions are!

- Regardless, the current price weakness is a great buying opportunity for gold stock investors. Please click here now. Double-click to enlarge this GDX chart. I’m an accumulator of GDX in the $23 to $18 area, buying every ten cents decline in that price zone.

- The big banks buy in the same manner, and that’s because it’s impossible to consistently buy at points where the price is bottoming or breaking out to the upside.

- The entire world gold community should be keen gold stock accumulators at the current time. Put options can be used to manage downside risk during the accumulation process.

- Please click here now. The US central bank uses the PCE index as their main measure of inflation.

- It’s been rallying nicely, but has stalled at the same time as gold has stalled. More rate hikes are required to push the PCE index higher. The rally began around the time that Janet did her first rate hike in late 2015.

- In my professional opinion, American GDP growth will surprise on the upside in the coming months, and Janet will commit to a June hike. That will provide further incentive to banks to make more loans, and it will increase the profit margin for those loans.

- That’s inflationary, and the PCE index should turn higher once the next rate hike has occurred. GDX and most gold stocks should turn higher in advance of the PCE upturn.

- Please click here now. Double-click to enlarge. Silver is now trading in a rectangular formation. The bottom of the rectangle is a great buying area for accumulators, and that’s exactly where the price is now.

- Please click here now. International FCStone has essentially the same gold market outlook that I have for the month of May, which is that the current price softness is not quite over.

- When the softness ends (with an ending point that is likely this Friday) a very violent upside rally will occur, perhaps pushing gold up towards the $1300 area highs! All precious metal investors should be in accumulation mode now, so they can enjoy the imminent upside action!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Thanks!

Cheers

st

May 2, 2017

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

Total SA’s chief energy economist, Joel Couse, forecasted that EVs will make up 15 to 30 percent of global new vehicle sales by 2030.

Total SA’s chief energy economist, Joel Couse, forecasted that EVs will make up 15 to 30 percent of global new vehicle sales by 2030.

Oil demand for transportation fuel see its “demand will flatten out,” after 2030, “Maybe even decline.” Couse said speaking this week at the Bloomberg New Energy Finance conference in New York.

Colin McKerracher, head of advanced transport analysis at Bloomberg New Energy Finance, sees Couse’s forecast as the highest EV sales margin yet to be forecasted by a major company in the oil sector.

“That’s big,” McKerracher said. “That’s by far the most aggressive we’ve seen by any of the majors.”

Royal Dutch Shell Plc sees a similar trend with oil demand in transportation flattening out in the near future. Chief Executive Officer Ben van Beurden said in March that oil demand may peak in the late 2020s. In November during an interview, Shell CFO Simon Henry said that demand is expected to peak in about five years.

Shell and Total SA have been looking to diversify their energy assets through hydrogen as a transport fuel. In January, both companies joined a global hydrogen council that included Toyota, Liquide SA, and Linde AG. The companies will be investing about $10.7 billion in hydrogen products over the next five years.

Like hydrogen fuel cell vehicles, electric vehicles have major walls to climb to find mass adoption in vehicle sales and infrastructure. One barrier is the cost of owning an electric vehicle versus a cheaper, comparable gasoline-engine vehicle. The battery pack in an EV can be quite expensive, making up half the cost of the car, according to BNEF.

Backers of EVs point to two trends fast approaching the market; with one being the longer range, 200-plus-miles per charge EVs coming to market like the Chevy Bolt and Tesla Model 3. The higher-priced versions of the Tesla Model S and Model X are thought to be a sign of it, with consumers willing to finance or lease one of these EVs to gain access to more power and longer range.

Automaker are feeling pressed by strict emissions reduction rules in Europe and China, with other markets like the U.S., Japan, and South Korea having similar standards.

Auto Shanghai has been a showcase for existing and startup automakers launching several EVs to the China market, with some of them ending up overseas.

It’s helping that lithium ion battery prices are dropping about 20 percent year, as automakers spend billions on electrifying their vehicle lineups. Volkswagen wants to see at least 25 percent of its vehicles sold in 2025 to be EVs. Toyota is moving toward selling zero fossil-fuel powered vehicles by 2050.

Another sign that the Total SA report carries some weight is the diverse and broad portfolio of EVs that automakers till be rolling out on the market soon.

“By 2020 there will be over 120 different models of EV across the spectrum,” said Michael Liebreich, founder of Bloomberg New Energy Finance. “These are great cars. They will make the internal combustion equivalent look old fashioned.”

Electric cars only make up about 1 percent of global vehicle sales, so making it to 30 percent in the short-term future would be a huge leap. Analysts point to a few market forces that need to be addressed before that technology takes off in sales. Among those issues are pre-incentive prices coming down, distance per charge going up beyond 300 miles, and the fast charging infrastructure becoming pervasive and cost competitive to gas pumps.

Erik Townsend and Patrick Ceresna welcomes Martin Armstrong to MacroVoices. They discuss Martin’s views on the U.S. Dollar and the future of the European Union. Martin offer his bullish case for U.S. stocks and considerations for international money flows. They discuss future interest rate trends, government debt, the geopolitics of North Korea and Syria and considerations on China and the debt crisis.

N.B. Patrick will be offering two workshops (free to MoneyTalks readers) on How To Trade Options in Calgary and Burnaby on Saturday May 6th and Sunday May 7th respectively. CLICK HERE to register

After two years of recurring warnings (both on this website and elsewhere) that Canada’s largest alternative (i.e., non-bank) mortgage lender is fundamentally insolvent, kept alive only courtesy of the Canadian housing bubble which until last week had managed to lift all boats, Home Capital Group suffered a spectacular spectacular implosion last week when its stock price crashed by the most on record after HCG revealed that it had taken out an emergency $2 billion line of credit from an unnamed counterparty with an effective rate as high as 22.5%, indicative of a business model on the verge of collapse .

Or, as we put it, Canada just experienced its very own “New Century” moment.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair