Timing & trends

QUESTION: The bounce in the Euro is a fool’s’ game?

ANSWER: Absolutely. The Euro is doomed because especially if Le Pen loses, Brussels will be relieved and proceed as usual. The same problems will merely exist and no reform will come forward to save the day. A good wind will blow over the European banking system. You are expecting politicians to admit they were wrong and surrender power in Brussels. NOT GOING TO HAPPEN. As Einstein said, you will NEVER solve the problem of the Euro with the same thinking process.

A weekly closing above the 10860 level in the Euro will imply the rally will press higher to test the 112-114 level. Just look at the technical perspective on a monthly level. The Downtrend Line stands in May up at 12622. We are nowhere near reversing the trend in the Euro.

We have the French, British, and then German elections here in 2017. We do not expect total chaos before 2018. That seems to be the point of a major shift.

…also from Martin:

Market Talk – French Election Reaction

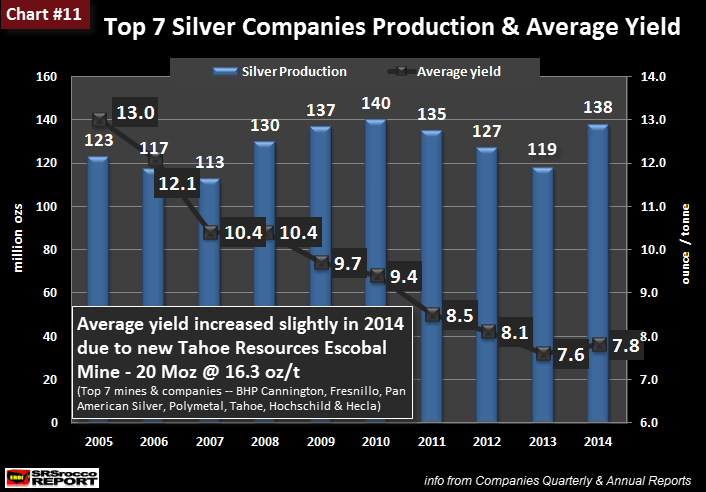

After the Primary Silver Mining Industry enjoyed a brief increase in productivity over the past two years, it fell to the lowest ever in 2016. The reason the primary silver mining industry’saverage yield increased in 2014 was due to the addition of Tahoe Resources high-grade Escobal Silver Mine.

Tahoe’s Escobal Silver Mine’s average yield in 2014 was an astonishing 16.3 ounce per ton (oz/t). Not only did Escobal Mine enjoy one the highest silver yields in the world, it produced over 20 million oz (Moz) in 2014. Thus, the addition of Tahoe to the Top Silver Miners pushed their average yield to 7.8 oz/t in 2014 versus 7.6 oz/t in 2013:

Now, what is very interesting about adding Tahoe’s Escobal super high-grade mine to the group, it didn’t move the average yield up that much…. only 0.2 0z/t to 7.8 oz/t.

I didn’t update this chart for 2015. However, I have now added the data for 2015 and 2016. As we can see in the updated chart below, the group’s silver production has increased over the past two years from 138 Moz in 2014 to 158 Moz last year. The majority of this increase was due to the ramp up of Fresnillo LLC’s Saucito Mine:

Even though the top 7 Primary Silver Mining Companies increased their production to 158 Moz in 2016, the amount of ore they processed also reached a record high. For example, these silver mining companies processed a record 21.3 million tons of ore in 2016 compared to 19.9 million tons in 2015. Furthermore, the top silver miners only processed 9.4 million tons of ore in 2005 to produce 123 Moz of silver… yielding 13 oz/t.

The falling average yield in the silver mining industry seems to be overlooked by the majority of analysts. As we can see in the chart above, the primary silver miner’s average yield has fallen from 13 oz/t in 2005 to 7.4 oz/t in 2016. This is a 43% decline in just 12 years.

Lastly, Tahoe Escobal Mine’s average silver yield will continue to fall over the next ten years. Thus, the global silver mining industry will continue to process more ore to produce the same or less silver in the future. While the cost of energy has declined over the past few years, falling ore grades will continue to put pressure on the silver mining industry going forward.

Check back for new articles and updates at the SRSrocco Report.

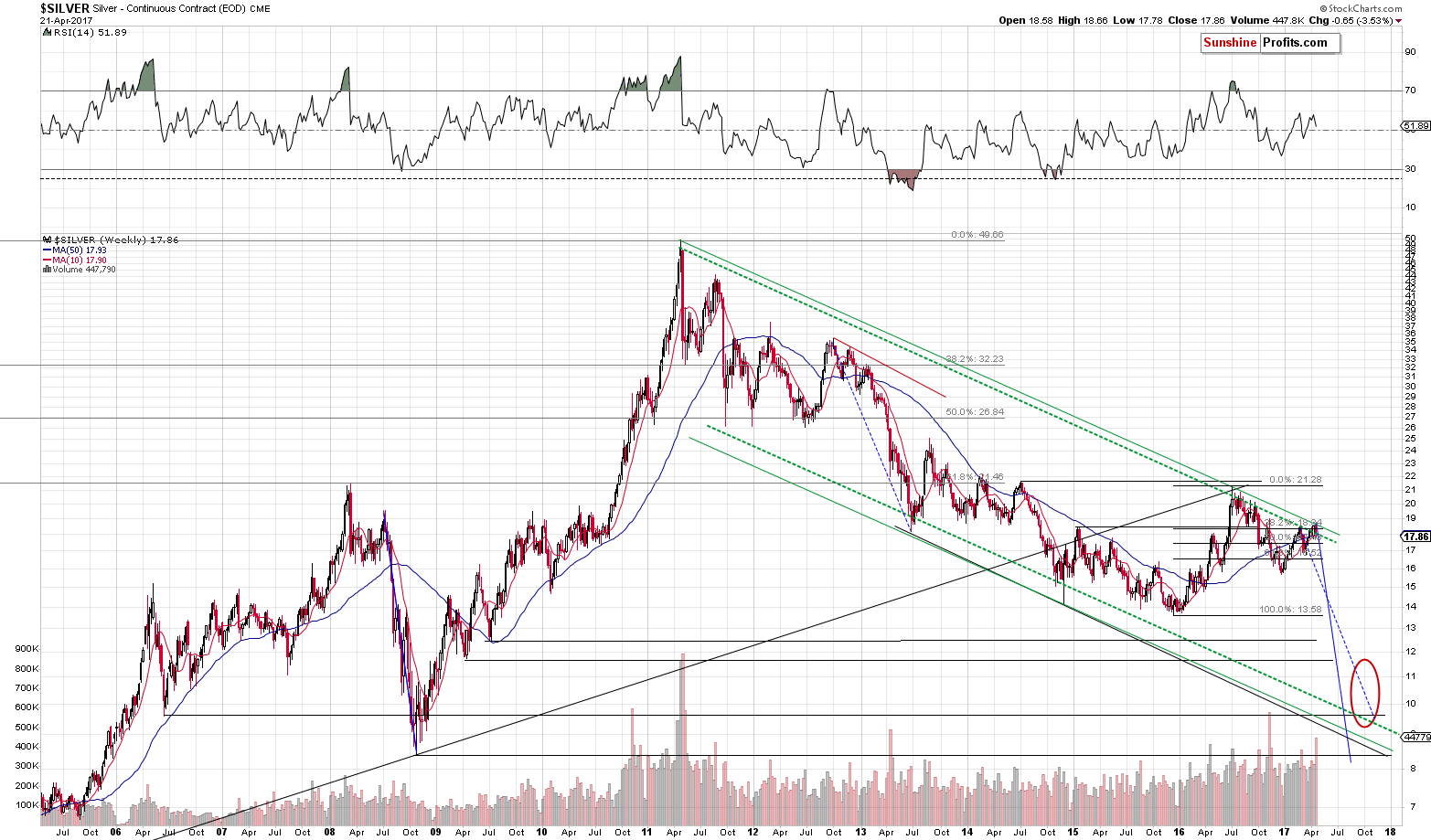

The most prominent action in the precious metals market that we saw last week, took place in silver – the white metal closed the week below the important long-term support/resistance line, thus invalidating the previous breakout. However, there’s more to the precious metals market than just the action in silver. In today’s free gold analysis, we discuss both the developments in silver and other factors.

Let’s start with silver itself (charts courtesy of http://stockcharts.com).

In Friday’s alert, we wrote the following:

(…) Still, if gold was to move higher (to $1,310 or so), then the above chart provides us with an analogous upside target – the upper, long-term green line (based on the same major tops as the lower line, but drawn through intra-day tops). It’s currently at about $18.70 – just 10 cents above this week’s high. So, the upside is quite limited.

Silver has indeed moved lower after it reached the upper of the declining, long-term, green resistance lines. The lower one (based on weekly closes) is currently at about $18, so if silver manages to close the week below it (which seems likely), the previous breakout will be invalidated and it would likely trigger another powerful decline. For now, the fact that the upper resistance line held, continues to have bearish implications – the upside is very limited and the downside is huge.

It didn’t take long for silver to slide below $18 – it did so a few hours after we posted the above and it’s been trading below it since that time. At the moment of writing these words, silver is at $17.92, so the odds are that it will indeed close the week below $18.

The volume on which silver declined was significant as well, so the implications are definitely bearish.

Naturally, if silver’s signals are not confirmed by other markets, one shouldn’t rely on them, but this time they are. In addition to multiple factors that we discussed in the previous alerts, we would like to emphasize that the breakdown in mining stocks was not invalidated yesterday.

The invalidation of the breakdown is now a clear fact. It’s no longer bearish, somewhat bearish, or a bit bearish – it’s very bearish. It’s been confirmed by the weekly closing price, and since the support/resistance line is based on the same kind of prices, the invalidation of the breakout is meaningful and clearly bearish.

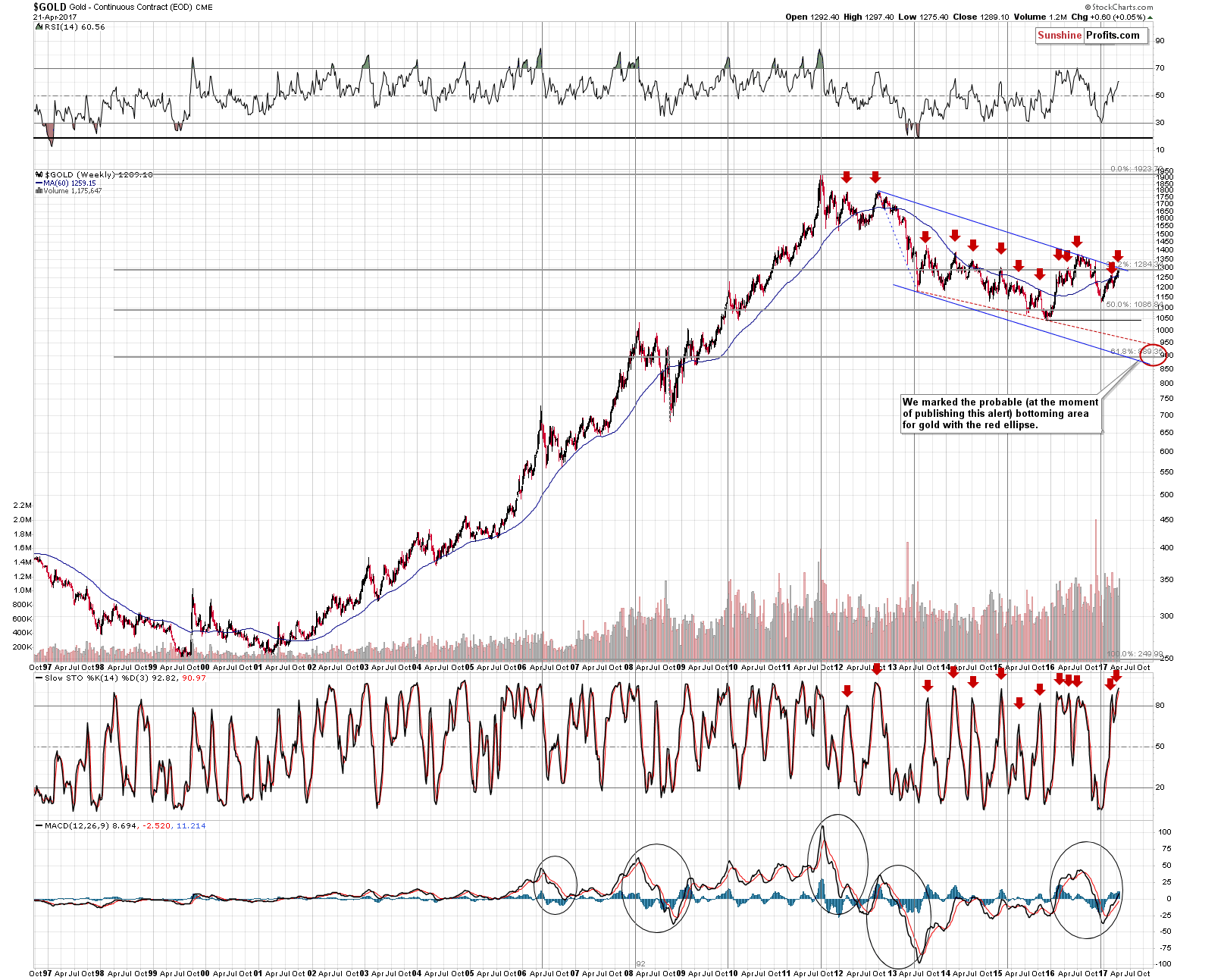

The long-term gold chart confirms the above bearish comments. The yellow metal moved to the declining long-term resistance line and then declined once again. There was no breakout, so the trend remains down.

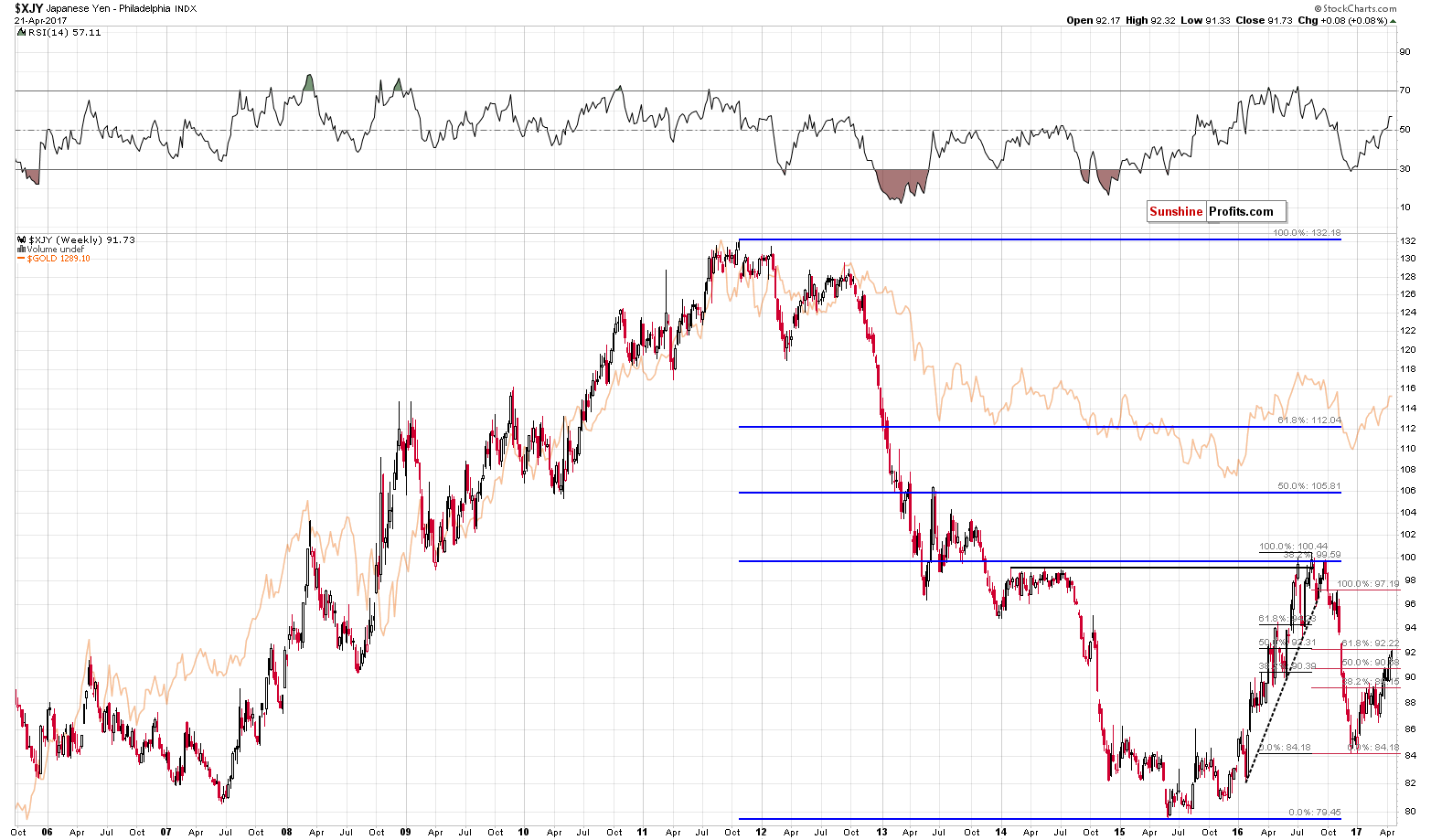

The Japanese yen which is closely linked to the price of gold, also moved to its critical resistance level (further supported by the zigzag corrective pattern) and thus it’s likely to have reversed its recent direction and decline in the coming days – and so is gold.

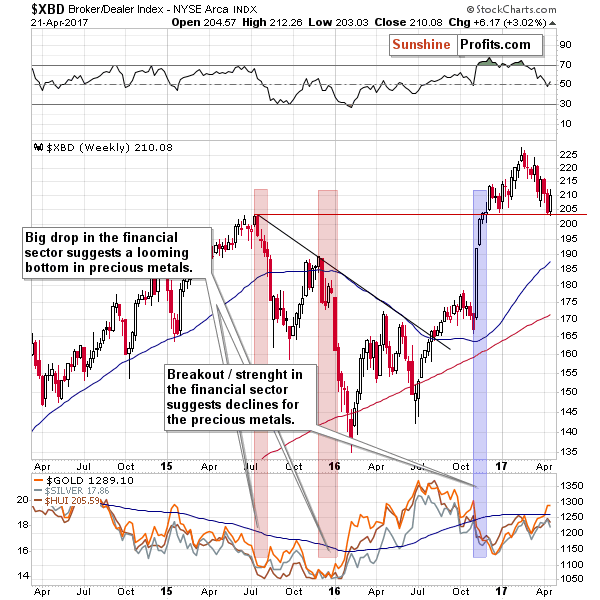

The financials were more clear as far as their signals are concerned. They too moved to an important level, but their bounce after reaching it was very visible. That’s a major medium-term development. This description is particularly important as the precious metals sector tends to react to major (!) moves in financial stocks (moving in the opposite way). Since the major move up is now (given the confirmation of the breakout above the 2015 high) likely for the financial stocks, a major move lower is likely for the precious metals sector.

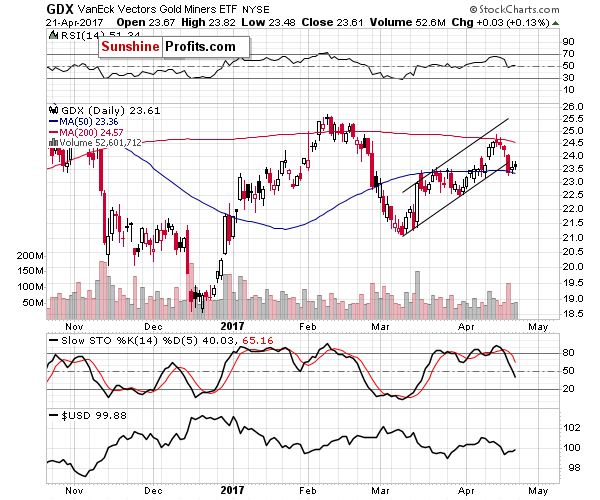

Let’s take a look at the short-term mining stock chart that appears to be leading gold once again (miners moved ahead of gold in the past months).

Gold and silver stocks confirmed the breakdown below the rising short-term support line by closing below it for 3 consecutive trading days, moving back to it without invaliding it and by closing the week below it. The volume on which Thursday’s and Friday’s upswing materialized was low, which also confirms that the move lower is the current true direction and the upswings should be treated as corrections.

Summing up, the precious metals market appears to be starting to decline even despite the lack of direct reasons to do so and that’s a particularly bearish situation. Precious metals had all the reasons to rally – tensions regarding North Korea, the unresolved situation regarding the U.S. airstrike in Syria and tensions before the elections in France… And it didn’t do anything substantial. Silver declined and miners have not only broken below the rising support line, but they also confirmed the aforementioned breakdown. This, plus other factors discussed previously support the expectation of lower precious metals prices in the coming weeks. Naturally, the above could change in the coming days and we’ll keep our subscribers informed, but that’s what appears likely based on the data that we have right now. If you enjoyed reading our analysis, we encourage you to subscribe to our daily Gold & Silver Trading Alerts.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief, Gold & Silver Fund Manager

Abstract

Abstract

America’s renewed desire to escalate military tensions is a front for America’s continual financial war, this time directed at North Korea, Syria and possibly Iran. This is likely to be the opinion of China’s strategic advisors. We analyse the geopolitics and economics behind America’s war strategy from China’s perspective, concluding that it is entering its final phase. China’s exit plan appears to be to tie the pricing of energy and then other major commodities to gold, returning to the pre-1971 status quo, when the dollar was just a settlement link between commodity prices and gold. Except this time, the dollar itself will be side-lined, so far as China is concerned, which will use the yuan instead for its empire, which will be far larger than that of the US in time, measured by GDP.

Introduction

The day President Trump assumed office, it appeared that at last there would be détente with Russia, leading to America’s withdrawal from unwinnable conflicts and towards a new peaceful agreement between these long-term enemies. However, within the traditional presidential bedding-down period of one hundred days, Trump has gone from his electoral platform of disengagement from foreign ventures to overt aggression in multiple locations.

Something major has changed his thinking. Trump has committed no less than five acts of foreign aggression in that short time, with a sixth pending….

….continue reading HERE (be sure to read the conclusion!)

Market Summary

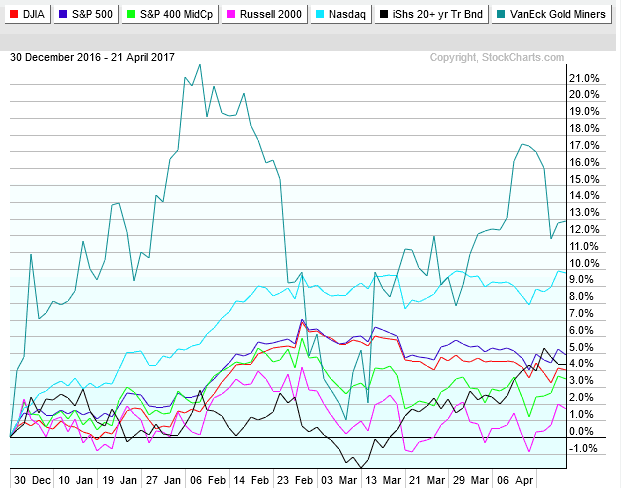

Last week, the benchmark S&P 500 index and the blue-chip DOW Jones Industrial Average advanced .9% and .5% respectively. The tech-heavy Nasdaq Composite Index logged a 1.8% weekly gain. The smaller cap Russell 2000 and MidCap 400 indexes are the biggest gainers ending up 2.57% and 2.18% respectively. In the chart below, gold is the biggest winner for the year as investors are hedging against nervousness about market uncertainty. Note that Nasdaq is edging higher which might signal the next bullish move for the overall market.

A standard chart that we use to help confirm the overall market trend is the Momentum Factor ETF (MTUM) chart. Momentum Factor ETF is an investment that seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks exhibiting relatively higher price momentum. This type of momentum fund is considered a reliable proxy for the overall stock market trend. We prefer to use the Heikin-Ashi format to display the Momentum Factor ETF. Heikin-Ashi candlestick charts are designed to filter out volatility in an effort to better capture the true trend. Last week’s comment “…the Momentum Factor ETF remains stuck in an almost two-month long trading range. Eventually there will be a breakout, but the question is will it be an upside or downside break…” The updated MTUM chart below is at an inflection point. You can see the current bullish trend is starting to pierce through the top of the current six-week trading range. Next week we should find out if the trend continues with a confirmed breakout or if it retrenches and stays range bound.

A tool to help confirm the overall market trend is the Bullish Percent Index (BPI). The Bullish Index is a popular market “breadth” indicator used to gauge the internal strength/weakness of the market. Like many of the technical market internal indicators, it is used both to confirm a move in the market and as a non-confirmation and therefore divergence indication. Nasdaq stocks have been leading the market direction for the past year. Last week we noted “…the Nasdaq Composite Bullish Index ($BPCOMPQ) continues to break down, until we get a confirmed recovery bounce the overall stock market will probably continue trending sideways…” As you can see in the updated chart the $BPCOMPQ is beginning a recovery bounce. We are looking to see the index moves above its 200-day moving average at approx. 62 to signal a break higher out its current trading range. There is a lot of overhead resistance, but as mentioned above the Nasdaq has been the market leader and if it breaks out the other major indexes can be expected follow.

The dollar rebounded a bit last week after Treasury Secretary Steven Mnuchin affirmed that there’s bipartisan support for raising the U.S. debt ceiling, and that an extension would likely be approved by the summer. Gold prices climbed Friday, erasing a loss for the week on the back of investor uncertainty ahead of first round of France’s presidential election this weekend. Gold prices have now posted gains for six weeks straight. Treasury prices fell Friday, pushing up yields, as investor appetite for riskier assets was boosted in response to U.S. President Donald Trump’s promise to unveil a tax plan next week, outweighing a flight to safety ahead of the first round of the French presidential election this weekend. Bond prices move in the opposite direction of yields; one basis point is one hundredth of a percentage point.

Market Outlook

As reported by Sue Chang, Markets Reporter for MarketWatch.com, just when it looked like the stock market was drowning in a sea of worry, President Donald Trump threw it a much-needed life line. Trump on Friday said he will reveal a massive tax package that will deliver cuts “bigger I believe than any tax cut ever.” The president plans to unveil the details on Wednesday, reiterated by a Saturday tweet. Some of the stock market’s sluggishness since the S&P 500 index hit a record on March 1 has been blamed on the absence of meaningful policy change since Trump took office. As a result, any hints that the president is committed to delivering on tax reform and deregulation will help to offset worries about soft economic data, most notably tepid auto and retail sales. But even that may be a boon for stocks as economic weakness could prompt the Federal Reserve to opt for gradual normalization of monetary policy, according to strategists at Yardeni Research. With the much-anticipated tax reform a step closer to reality, investors will be emboldened to return to the market to chase stocks higher. That the corporate-friendly measure comes on the back of an upbeat earnings season will give the market added upside momentum. Analysts are projecting one of the best quarterly earnings in more than five years on the back of a recovery in both the U.S. and global economies. You can see in the chart below how “risk-off” assets like gold, real estate and treasuries have been the stellar performers at the start of the second quarter.

The CBOE Volatility Index (VIX) is known as the market’s “fear gauge” because it tracks the expected volatility priced into short-term S&P 500 Index options. When stocks stumble, the uptick in volatility and the demand for index put options tends to drive up the price of options premiums and sends the VIX higher. The chart below indicates the market is at an inflection point. Last week the Volatility Index pulled back from six-month highs as the S&P 500 recovered higher. If the S&P continues crossing above the VIX line it might indicate the market is headed back to challenge its all-time highs.

The American Association of Individual Investors (AAII) Sentiment Survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market for the next six months; individuals are polled from the ranks of the AAII membership on a weekly basis. The current survey result is for the week ending 04/19/2017. Optimism among individual investors about the short-term direction of stock prices is at a new post-election low, according to the latest AAII Sentiment Survey. At the same time, neutral sentiment is at a two-month high and pessimism remains above its historical average. Bullish sentiment, expectations that stock prices will rise over the next six months, fell 3.3 percentage points to 25.7%. Optimism was last lower on November 2, 2016 (23.6%). The drop keeps bullish sentiment below its historical average of 38.5% for the 13th out of the last 14 weeks. This is the third consecutive week with a bullish sentiment reading below 30%. This week’s reading is unusually low, meaning more than one standard deviation below the historical average. (The breakpoint is 28.1 %.) Historically, unusually low levels of optimism have been followed by above-average gains in the stock market. The S&P 500 has realized a median six-month gain of 6.3% over the following six-month periods. Furthermore, the large-cap index has risen nearly 85% of the time following unusually low bullish sentiment readings versus nearly 72% for all six-month periods between September 1987 and November 2016. Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, rose 1.9 percentage points to 35.6%. Neutral sentiment was last higher on February 8, 2017 (36.5%). The rise keeps neutral sentiment above its historical average of 31% for the fifth consecutive week. Bearish sentiment, expectations that stock prices will fall over the next six months, rebounded by 1.3 percentage points to 38.7%. The rise keeps pessimism at or above its historical average of 30.5% for the 10th consecutive week and the 13th out of the last 14 weeks.

The National Association of Active Investment Managers (NAAIM) Exposure Indexrepresents the average exposure to US Equity markets reported by NAAIM members. The blue bars depict a two-week moving average of the NAAIM managers’ responses. As the name indicates, the NAAIM Exposure Index provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The current survey result is for the week ending 04/19/2017. First-quarter NAAIM exposure index averaged 92.85%. Last week the NAAIM exposure index was 86.70 %, and the current week’s exposure is 70.82%. Disappointing quarterly results from some big name companies made investors nervous last week. Instead of increasing equity exposure money managers sold some stocks and traded “risk-off” buying treasury bonds.

Trading Strategy

According to Jeff Hirsch in a recent issue of the Almanac Trader, the best six months for owning stocks can begin in October or early November and usually lasts until April or early May for DJIA and S&P 500. However, seasonal strength for technology stocks, measured by NASDAQ, tends to last until June. Due to its substantial weighting in technology, the S&P 500 also demonstrates a tendency to rally from late April until early June. This trade has been profitable 62.9% of the time over the longer-term however; its recent track record has been rough, declining seven times in the last eleven years. Going long the September futures contract on or about April 27 and holding until on or about June 7 has worked 23 times in 35 years. The key to this trade is overall market trend and proper trade management as numerous sizable losses and gains have occurred over trade’s history.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair