Currency

Transcript Below:

Transcript Below:

Mike Gleason: Well, to start out here Dr. Faber, before we get into some other stuff I wanted to hear your comments on the state of the U.S. economy. Now, it appears the Federal Reserve has finally gotten serious about moving rates higher at least modestly. U.S. equity markets seem to be discounting that fact, focusing instead on the so-called Trump trade. Markets are pricing in a huge infrastructure spending program and tax cuts stimulates that could overwhelm any modest tightening at the Fed. Now that efforts to reform healthcare seem to be failing we expected some of the optimism surrounding president Trump’s other initiatives would leak out of the stock market but so far that hasn’t happened.

Stocks remain near record highs and there isn’t a whole lot of interest in safe haven assets including precious metals. So, what are your thoughts here Marc? Is now a time to take some profits and move towards safety or is there still some good upside in equities?

Marc Faber: Well, I think that in terms of the economy I don’t think the economy is as strong as people believe or as the statistics would show and recent trends have rather been indicating some weakness is auto sales, not a particularly strong housing market and we have several problems as a result of excessive credit. So, I think that the economy is not going to do as well as people expect and concerning the huge infrastructure expenditure that Mr. Trump has been talking about, it is about a trillion dollars over ten years, maximum. In other words, a hundred billion a year.

In China in 2016 in the first ten months the infrastructure expenditures were 1.6 trillion, in other words 16 times higher than what Mr. Trump is proposing. So just to put this in a perspective. Now throughout Asia and the emerging world there will be a lot of infrastructural expenditures in the years to come. The question is will stocks go up because of that, maybe some stocks will go up and some will not. So, we have to be now increasing the selective in what we purchase in terms of equities. My sense is that the economy in the U.S. is weakening and not strengthening.

Mike Gleason: It is also possible markets aren’t responding to fundamentals and we ought to consider those ramifications. The advent of high frequency trading and massive intervention by central bankers could mean markets become more irrational than ever. It is possible for instance to see stock prices being bid higher despite slowing GDP growth, rising interest rates and congress failing to deliver fiscal stimulus here in the U.S. I mean, how artificial do you think markets are and to the extent today’s markets aren’t real, how much long will the central planners and bankers be able to maintain this illusion that they’ve created?

Marc Faber: Well, basically some people say that the central banks are out of bullets. This is not my impression. They can keep on printing money and boost asset prices where by not all asset prices will go up, some will go up and some will go down. But the point I want to make is the central banks are not really out of bullets. The economy, if it weakens some stocks will outperform others, in other words recently you’ve seen the weaker in automobile stocks, so there is still a selective process in the market. The stocks that have gone up the most recently are actually mostly companies with very little earnings, very high evaluations, Tesla, Amazon, Netflix and so forth and we’ll have to see.

All I can say is when I look around the world, I don’t see any particularly good values in the U.S. except in mining companies and I think some of the interest rate sensitive stocks are again relatively attractive because I expect the economy to disappoint, especially if the Fed continues to increase interest rates and so a short increase in interest rates could mean some further weakness in bond prices but eventually bond prices could rally again and this is my view that the U.S. by any standards compared to historical evaluations, compared to Europe, compared to Asia, compared to emerging markets the U.S. is very expensive. Now, can it go up another ten percent? Maybe 20 percent? Yes, between December 1999 and 2000 March 21 when the stock markets peaked out the Nasdaq was up more than 30 percent, but was it a good buy? No, everybody who bought at the time in the first three months of 2000 lost money.

So, my sense is that yeah people can buy stocks here but most of them are going lose money with the exception in my view, that mining stocks will perform reasonably well.

Mike Gleason: Let’s shift focus now and talk about what is happening elsewhere in the world, you’ve alluded to it in prior answers but you’re originally from Europe and now you live in Asia. Now, it’s easy for Americans to focus on domestic affairs such as the new president and lose track of important developments in other parts of the world. Can you update our listeners on developments you are watching in Asia? China in particular.

Marc Faber: Well, whether it’s sustainable or not the fact is that the Chinese economy has been improving recently, somewhat. Maybe it’s all driven by credit but for now they have stabilized the economy, it’s improving and it has had a huge impact on the prices on resources including copper and zinc and nickel and so forth and it has had a favorable impact on the Asian market. Earlier you asked me about the U.S… this whole euphoria about the performance of U.S. stocks, the fact is in Asia just about every market has outperformed the U.S. In Europe, just about every market has outperformed the U.S. measured in U.S. dollar terms. So, I think that the impact of an improving Chinese economy is being felt more in other emerging economies than say, in the United States.

Mike Gleason: How about Europe? The future of the European Union is in question with some important elections upcoming, banks there remain at risk and several if not most countries continue to struggle with slow growth and overwhelming debts. Give us your thoughts on Europe and how things might unfold there over the remainder of the year.

Marc Faber: Well, I’ve just written two reports recently highlighting that in Europe there are some companies, mostly utilities and infrastructure related companies that on a valuation screen appear relatively attractive. They have dividend yields of between four and six percent, the Euro is weak or has been weak and is at the low level and these yields of four to six percent are very attractive considering the bonds yield in Europe. And so, I think that this year European stocks and especially the stock I mentioned, infrastructure plays, utilities and also food (stocks) will way out perform the U.S. I also happen to think that there will be more and more American companies and foreign companies that will be interested to acquire European companies.

Mike Gleason: How about the geopolitical side, I know many of those nations over there the people are watching what happens with Brexit and have watched what’s taken place there. France, the Netherlands, some other nations have some important votes coming up. What do you make with everything that’s happened there with the state of the European union and how those votes might go as we go throughout the year and see some of these important elections come to fruition.

Marc Faber: Well, this is the big question and we all don’t know exactly what the answer is. My sense is that the Euro will stay and if some weak countries decide to leave the Eurozone, their currencies will be obviously punished. And if some weak countries decide to leave the Eurozone, I think the euro will strengthen. It’s just that if Italy decides to leave the Eurozone, the euro will strengthen but obviously, the new currency (of Italy) will weaken. And so, I think that this Is not a big concern for me.

Furthermore, with the euro having declined so much against the U.S. dollar, if there is further weakness in euro, European stocks will adjust on the upside and foreign companies from Asia… China, Japan and the U.S. will increasingly acquire European companies and European assets.

Mike Gleason: Gold is often referred to as the anti-dollar, if we see the euro strengthen and last as a currency, does that then weigh heavily on the U.S. dollar and might we see gold spike as a result of that because the dollar finally is starting to weaken a little bit?

Marc Faber: Yes, I mean the consensus was, at the beginning of the year that the only game in town are U.S. stocks and the U.S. dollar. I don’t believe that the U.S. dollar is structurally a strong currency. Now can it stay high as it’s rallied a lot against the euro but at this level, I don’t think that the U.S. is very competitive. So, my sense would be the U.S. dollar is vulnerable as well as asset prices in the U.S. both.

Mike Gleason: Dr. Faber, do you see the tide changing world wide when it comes to the importance of gold ownership? We know Asians are buying it relentlessly and so are folks in Europe, maybe that mindset hasn’t made its way to the U.S. yet, but do you sense that may be coming? And once it does do you foresee any problems with being able to get physical metal once the masses, especially in the western world, wake up to the idea that they ought to own some?

Marc Faber: Well, the gold market is very interesting because it consists of a very limited number of people who are “gold bugs” as they call them. And these are people that will accumulate gold, physical gold and gold shares and so forth, but this is the minority. And then there are the gold detractors. These are mostly fund managers and so-called central bankers. And central bankers are not particularly smart. And then there are people who simply haven’t heard about gold as an investment… and don’t forget that in the U.S. 50 percent of the people have no interest in investments for the simple reason that they have no money. You could show them any proposal for an investment, they wouldn’t be interested because they have not the money to invest in the first place.

But in general I think that people will gradually wake up to the fact that in absence of knowing how the world will look like in five or ten years, you need some diversification and in this environment, I think that some people will say “well, let’s own some gold.” Most people will only own five or ten percent but some people will own 20 percent and I think that if the whole world decides to own, just say three percent or five percent, and the fund managers who are very anti gold see gold prices running up again… the whole investment business has become a momentum game… so if they see that gold is moving up in a convincing way they’ll buy gold.

So, my sense is that you need some gold strength and then people will come in and buy gold simply because it moves up. I buy gold all the time, of course within my asset allocation… I also have shares and bonds and real estate… but I always buy some gold to maintain the proper weighting.

Mike Gleason: Well, as we begin to close here, what do you expect for the remainder of 2017 and what kind of second half of the year do you think it will be for hard assets like gold and silver specifically?

Marc Faber: Well, at the beginning of the year so many people have started to write reports about the surprise of 2017 and projections of 2017, so everybody has a view, nobody knows precisely and the lot will depend on central banks’ monetary policies. I don’t believe central banks can tighten meaningfully, maybe optically they do some, but in general I think they’ll keep money printing on the table as far as we can see, in other words, for the next few years. And eventually it will be friendly for precious metals and hard assets. Number two, hard assets such as precious metals are at the historical low point compared to financial assets, so I think that’s going forward there’s a huge discrepancy in the performance between financial assets which has been very good since 2009 and gold which has been more mixed… it’s also up but it’s been more mixed especially after 2011… that these hard assets will come back into favor.

So, if you’re asking what is my expectation for the rest of 2017, I think that gold shares are an attractive asset class. I think precious metals can easily move up another 20, 30 percent, possibly 100 percent or so. In general, I would say American investors should take the opportunity that the dollar is strong and that asset prices, in other words stocks and bonds in the U.S. has been strong to reduce their positions in the U.S. in terms of equities.

Mike Gleason: Yeah and certainly you hit the nail on the head earlier there with the whole momentum trade and it will be interesting to see what happens if we do start to see some positive upside momentum in the metals… more and more hedge fund managers getting into that space and it really feeding on itself and creating a snowball effect there, it could be interesting to see that play out. Well, Dr. Faber thanks very much for your time and your wonderful insights and we certainly appreciate you staying up late in Thailand to speak with us today. Now before we let you go, tell people how they can subscribe The Gloom, Boom and Doom Report and get your fantastic commentaries on a regular basis.

Marc Faber: It’s my pleasure, the best is to go on the website www.GloomBoomDoom.com – it’s all written in one word.

Mike Gleason: Well, excellent stuff. It’s been a real honor to speak with you Dr. Faber. I hope we can catch up with you again sometime soon, thanks very much for joining us.

Marc Faber: My pleasure, thank you. Have a nice day.

Mike Gleason: Well, that will do it for this week. Thanks again to Dr. Marc Faber, editor and publisher of The Gloom, Boom and Doom Report, again the website is GloomBoomDoom.com be sure to check that out.

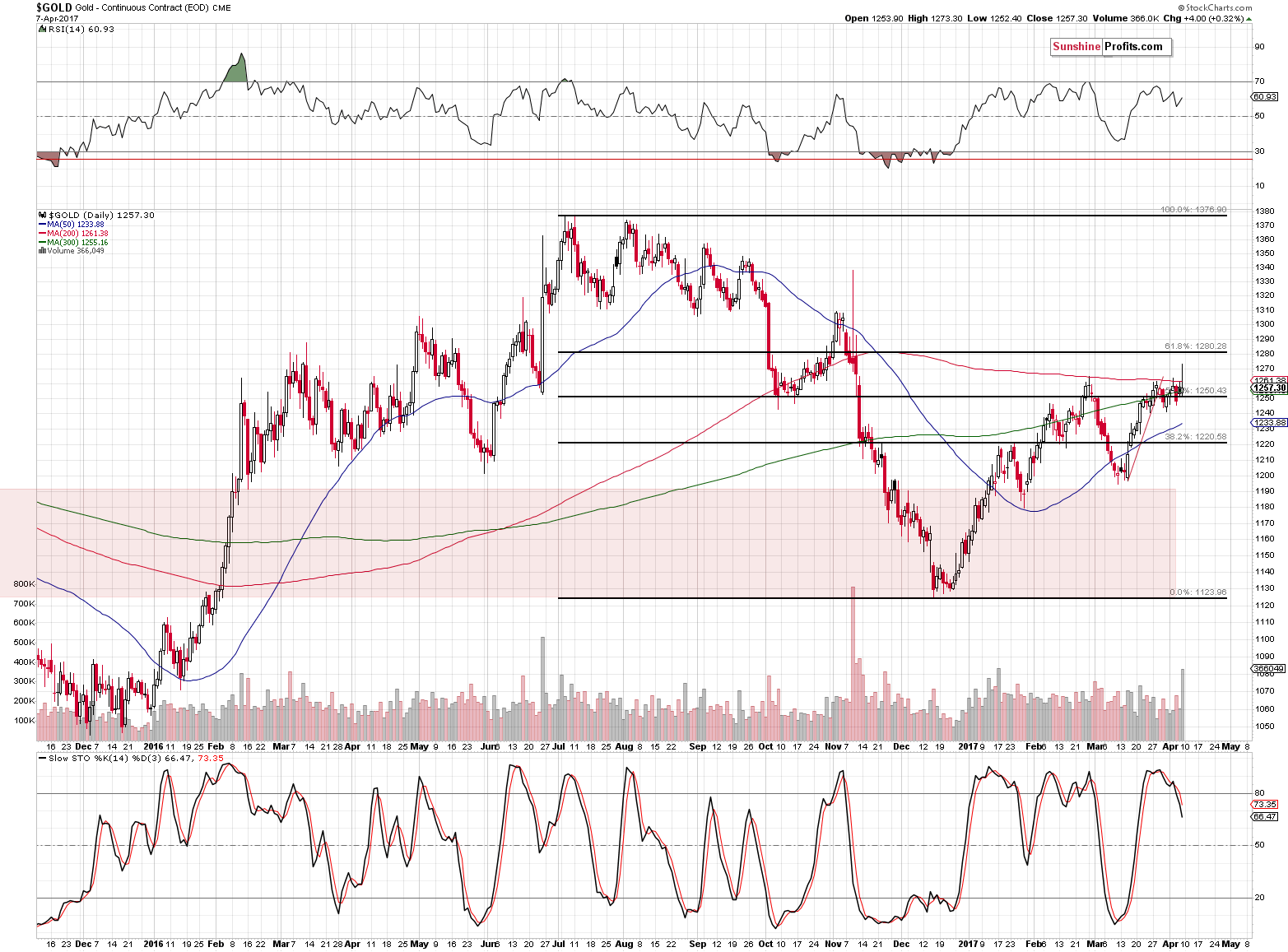

Several things happened on Friday and the markets reacted to them, so it’s not easy to interpret the final outcome. Was the reversal bearish or was the session bullish as gold didn’t decline substantially even though the USD rallied? Was gold’s reaction adequate, too small or too big?

Let’s start the discussion with a reminder of one of the reasons for Friday’s pre-market rally. In Friday’s Gold Trading Alert, we wrote the following:

The likely direct reason behind today’s overnight spike in the price of gold is a cruise missile strike at a Syrian airbase, most likely the one from which a deadly chemical weapons attack had been launched earlier this week. However, it’s not likely that 59 Tomahawk missiles was enough to ignite a rally alone. The strike had damaged ties between Washington and Moscow, as Russian spokesman Dmitry Peskov described the U.S. action as “aggression against a sovereign nation” on a “made-up pretext”.

We have already mentioned that news-based rallies are likely to be temporary – today let’s focus on the temporary impact that the above was likely to have – it was likely to boost prices of assets that are viewed as safe havens – gold and… the U.S. dollar. Both are being viewed as safe bets and thus it’s no wonder that we saw a temporary increase in prices of both assets. Consequently, the fact that gold didn’t decline is not a reflection of gold’s true strength vs. the US dollar and thus it shouldn’t be viewed as a bullish sign.

The important thing is that whereas the USD rallied further during the session, gold and silver reversed and erased (or more than erased in the case of silver) the entire daily rally before the end of the session. So, even though the initial safe-haven reaction was quite natural, it was also the case that the news-based rally was temporary – it didn’t even take one trading day for the move in precious metals to be reversed.

All in all, it appears that the reversals are the thing to keep in mind, while gold’s supposed strength vs. the USD is not. Let’s take a look at the gold chart (chart courtesy of http://stockcharts.com).

Gold’s reversal was not only sizable, it was also accompanied by huge volume – this is a classic, reliable reversal pattern. Needless to say, the implications are bearish. Moreover, please note that the sell signal from the Stochastic indicator remains in place.

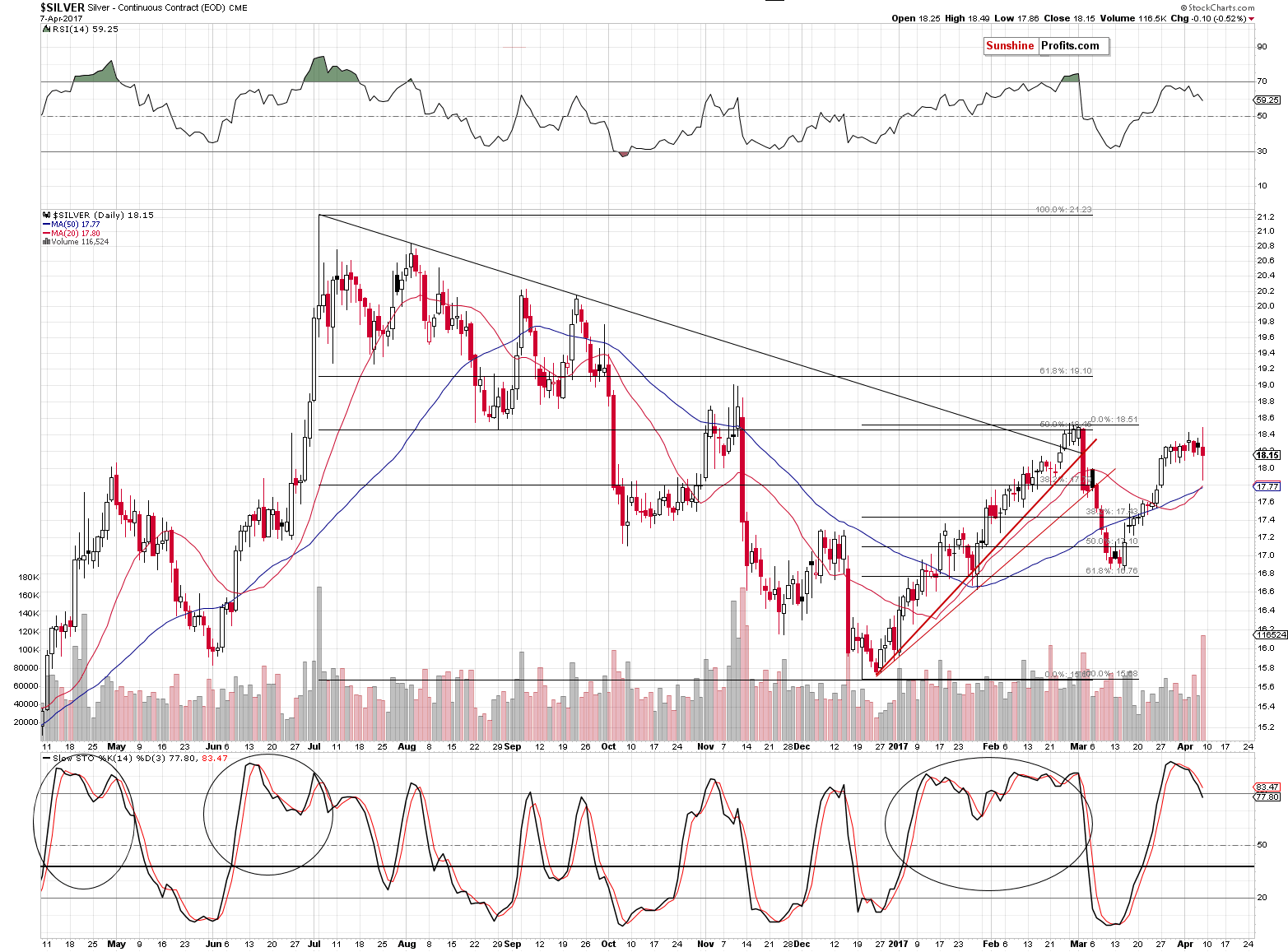

Not only is the reversal in gold significant by itself – it’s also confirmed by analogous action in silver. In fact, silver declined even more than gold (having closed below $18, which is not visible on the above chart) and it’s currently at $17.90. The implications are bearish.

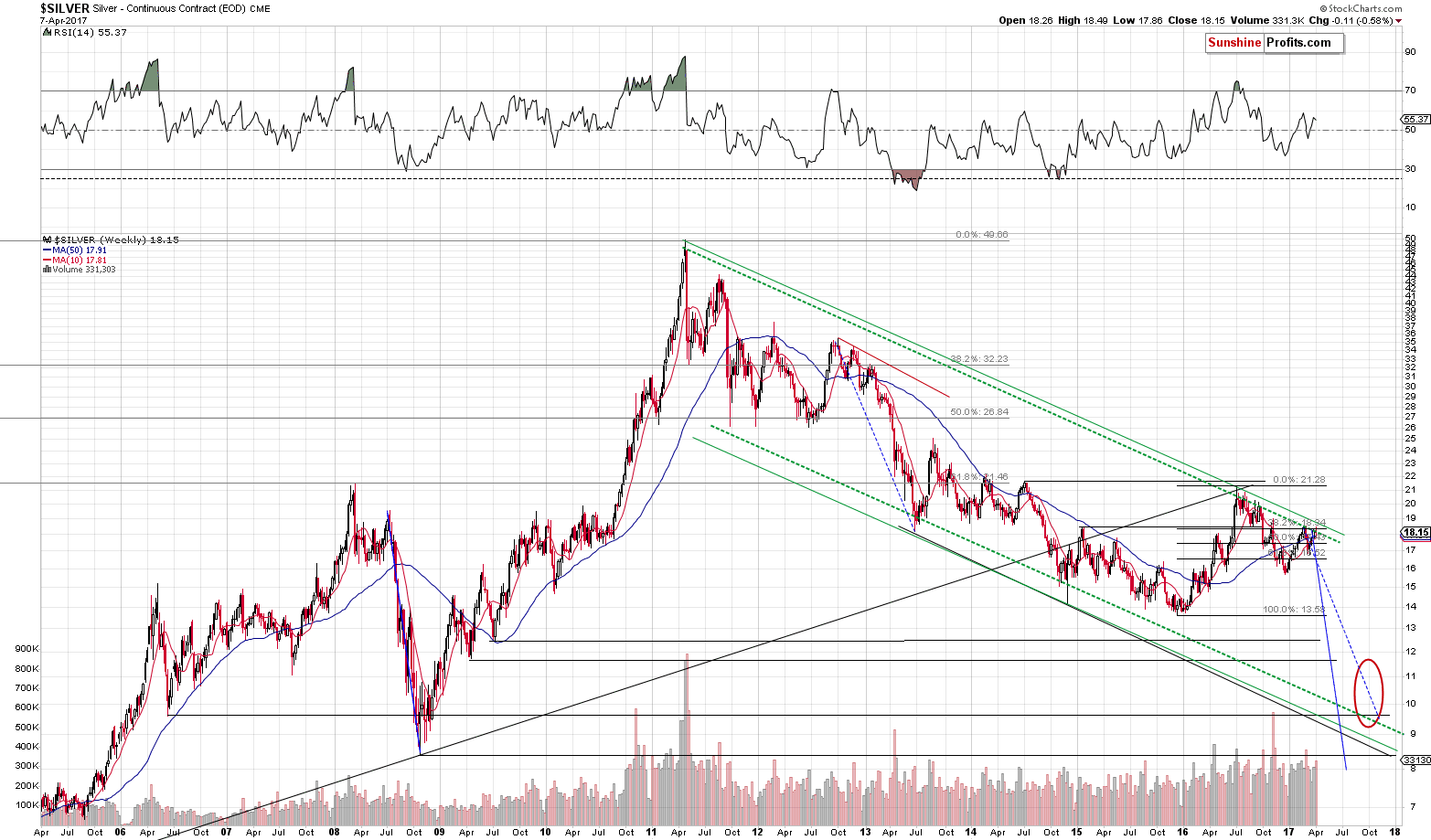

Last week, we wrote the following about the above long-term silver chart:

There are a few things that decide whether a resistance line is strong or not. The more important the tops that it’s based on, the more important the resistance line. The more tops create a given line, the more important the resistance is. Finally, for the line to be very important, the space between the tops that create it should be rather significant (for instance the red line based on 2 late-2012 tops didn’t result in anything in the following months and years).

Moreover, the way a given resistance line is likely to work is based on what created a given line. Therefore, a resistance line based on intra-day tops is likely to stop intra-day moves, a line based on daily closes is likely to stop the moves in terms of daily closing prices (so that the closing price doesn’t break the line even though intra-day moves might) and the line based on weekly closes is likely to stop the moves in terms of weekly closing prices (in analogy to daily closing prices).

After the rather lengthy introduction, let’s move to the point. Silver just moved to the line that is very important (green dashed line based on one extremely important top, one very important top and one less important top) and it did so in terms that were in tune with what the line was based on – silver closed the week at the line that was based on weekly closing prices.

The implications are naturally bearish for the following weeks and months as the above means that even if silver moves a bit higher temporarily, it’s unlikely to move higher substantially or for long. The above alone suggests that we are in the “pennies to the upside and dollars to the downside” territory without considering anything else (including the USD Index). The situation would be different if the silver had broken above this line and confirmed this breakout – but it didn’t, so the implications of moving to it are clearly bearish.

So, a reversal is very likely to occur shortly, if it didn’t occur on Friday.

Silver moved higher very temporarily, reversed before the end of the week and overall it declined last week. The mentioned long-term resistance line seems to have stopped the rally.

Summing up, Friday’s pre-market upswing in the precious metals sector appears to have been just a temporary news-based move that was already invalidated. The resulting reversals are very bearish developments especially that they were seen in both: gold and silver. Naturally, the above could change in the coming days and we’ll keep our subscribers informed, but that’s what appears likely based on the data that we have right now. If you enjoyed reading our analysis, we encourage you to subscribe to our daily Gold & Silver Trading Alerts.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief, Gold & Silver Fund Manager

The stock markets have enjoyed a “Trump bump.” Despite a recent “Trump fade,” North American stock markets are positive for the year and economic numbers have been fairly solid. Stock market volatility is low and recently the S&P 500® experienced a 110-day run without a 1% correction. Ev- erything just feels good. Enjoy it while it lasts.

It is not that there are ominous clouds on the horizon. There is nothing out there pointing to a sudden correction, but that does not mean that the stock market cannot correct. It can correct at any time. When everything seems just right, it is the surprises that can re-direct the stock market downwards. A healthy stock market tends to absorb the negative surprises well, with only a minor correction before heading higher once again. Or even, interpreting a typically negative event, with a positive spin. This is the type of market that we have been experiencing.

S&P 500 Technical Status

The S&P 500 is currently in a consolidation pattern with a “high” set at the beginning of March. Although the S&P 500 has had a series of lower highs, we have not established a pattern of lower lows. This pattern is neither bullish nor bearish, but it does show that the S&P 500 is looking to establish direction. A solid break above 2400 would show

that the stock market is decidedly bullish. A break below 2325 would be bearish.

Unfortunately, we are only weeks away from the period when the stock market often starts to fade as it enters into the six-month unfavorable period at the beginning of May. From a seasonal point of view, there is not a lot of time and the stock market may provide some muted gains, but the risk remains to the downside. Positive reaction from investors to strong earnings may provide some support to the market, but investors should start to become cautious at this point.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Strengths

- The best performing precious metal for the week was pretty much a tie between gold, platinum and palladium with roughly a 0.50 percent gain. Following the launch of a U.S. missile strike on Syria this week, gold rallied to its highest level in nearly five months, reports Bloomberg. Bullion was pushed back above its 200-day moving average, a level that analysts use to predict whether further gains will continue or stall.

- Earlier in the week, the minutes from the Federal Reserve’s March meeting “boosted gold prices with the mention of the shrinking of the balance sheet,” said Jingyi Pan, a Singapore-based market strategist, reports Bloomberg. “This agenda could potentially conflict with the pace of rate hikes, therefore placing pressure on the dollar.” In addition, gold advanced after automobile manufacturers reported worse-than-expected U.S. sales for March.

- BullionVault’s Gold Investor Index, measuring the balance of buyers against sellers, rose to 54.2 in March from 51.8 in February, reports Bloomberg. “Political risk continues to drive private investor demand for gold,” Adrian Ash, head of research at BullionVault, said in a report.

Weaknesses

- The worst performing precious metal for the week was silver, with a fall of 1.30 percent. Late Friday CFTC data showed that money managers actually increased their bullish opinion on silver to the highest level in more than eight months. Profit taking, post the morning surge in precious metals prices, late Friday pulled silver into a loss for the week. Gold reserves in China’s central bank remained unchanged for the month of March, coming in at 59.24 million ounces, reports Bloomberg. This is the fifth straight month that gold reserves have remained unchanged.

- Despite Goldman Sachs encouraging investors to have “patience” for the commodity market in the wake of a waning price rally, inflows into ETFs linked to raw materials have significantly plunged in recent weeks, reports Bloomberg. Goldman believes the pace of economic growth in China will drive raw-materials consumption. In a similar fashion, RBC Mining & Material Equity Team cut its precious metals recommendation to underweight from market weight for the second quarter, reports Bloomberg. It upgraded bulk commodities to overweight from market weight and fertilizers to market weight from underweight.

- In Canaccord Genuity’s Precious Metals Note this week, the group says we may see potential NAV multiple compression in the sector. It notes margin compression, rising management compensation, declining IRR hurdle rates and rising operational and geopolitical risks as potential headwinds that could temper enthusiasm for gold producers.

Opportunities

- In its U.S. Economics report this week, Macquarie Research says that demographic forces are intensifying, as the share of population 75+ begins to rise. Because of this, the group says the economy is confronting two headwinds, or “double trouble”: 1) a closing of the output gap and the end of slack and 2) unprecedented demographic change that has accumulated over the past seven years is now intensifying. They believe the Fed Funds may normalize at 1.5 to 1.75 percent and the 10-year Treasury yield at around 2.3 percent, well below consensus of 3 percent for Fed Funds and 3.5 percent for 10-year yields. With CPI running at 2.7 percent, it is likely we will continue to see flat to negative real rates, thus supportive of gold. And in a note from BMI Research, the team says gold can be supported as the Fed is likely to raise rates only once more in 2017.

- The technical team from Desjardins says that the gold price (COMEX) has substantial potential upside. The team notes that total known ETF holdings of gold have increased around 2 million ounces year-to-date, implying a gold price of $1,310 per ounce. Similarly, Comex paper claims to physical gold continue to soar to 45:1, while deliverable gold has contracted by 50 percent since the start of the year.

- Zacks Investment Research highlights Klondex Mines in an article this week, calling the company an “off-the-radar potential winner” and saying it looks well positioned for a solid gain, but has been overlooked by investors lately. Klondex has seen estimates rise over the past month for the current fiscal year by about 22.2 percent, although that is not yet reflected in its price, as the stock lost 21.7 percent over the same time frame, Zacks writes. The company carries a Zacks Rank #2, a strong buy, further underscoring the potential for its outperformance. Another company with positive coverage this week is Rye Patch Gold, initiating a buy recommendation from George Topping from Industrial Alliance Securities. Topping predicts that Rye Patch will trade at 75 cents within a year, implying a potential 124 percent gain.

Threats

- The Senate voted along party lines on Thursday to change the Supreme Court’s longstanding rules and effectively eliminate the filibuster for Supreme Court nominees, reports Bloomberg. Now it will only require 51 votes, not 60, to bring a nominee up for a confirmation vote. The Senate confirmed on Friday Judge Neil Gorsuch as the new Supreme Court Justice, restoring the generally conservative majority. Some commentators noted that this may embolden President Trump to now pick even more judges for the bench that are more divisive, since a simple majority will be all that is needed to confirm. Similarly, Adam Posen, president of the Peterson Institute for International Economics, says that Trump is likely to pick a Fed chairman who is “very responsive to him.”

- In its Global Precious Metals Comment this week, UBS points out that European diesel share decline accelerated in March, supporting its view on platinum group metals (PGMs). Diesel share in the top five European auto markets declined, bringing the share of diesel vehicles to a multi-year low of 40.6 percent. The UBS Global Autos team expects this trend to accelerate further out, resulting in falling platinum demand.

- Goldman Sachs writes this week, that after five years of operating cost deflation, we expect costs to start responding to the 40 percent rebound in metal prices witnessed since January 2016. Once earnings tailwinds, we believe these core cost drivers should now start putting upward pressure on the full spectrum of global cost curves, Goldman continues. Additionally, the group notes that not all costs can be controlled, explaining that around 85 percent of the copper industry’s opex improvement was driven by what it considers to be “uncontrollable costs.”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair