Stocks & Equities

While the Japanese and Swiss central banks have turned themselves into hedge funds by loading up on equities, the US Fed has stuck to supporting the stock market indirectly, by buying bonds. It’s worked, obviously, with all major US indexes at record highs. But it won’t work going forward, thanks to two gathering trends.

First, the main way bond buying supports equities is by lowering interest rates which, among other things, allows corporations to borrow cheaply and use the proceeds to buy back their own stock. Companies avoid paying dividends on the repurchased stock and the government gets capital gains tax revenue from a bull market. From a short-sighted Keynesian perspective, it’s a win-win.

Alas, this New Age public/private partnership on running out of steam. Interest rates have fallen about as far as they can fall and corporations have borrowed about as much as they can borrow. So the buyback binge is topping:

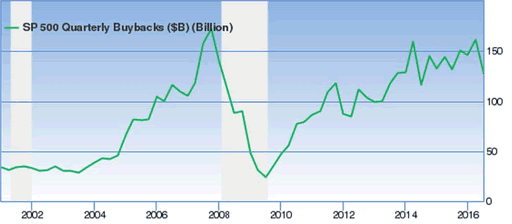

Share Buybacks Sink For Second Straight Year

(Forbes) – According to S&P Dow Jones Indices, companies of the S&P 500 index in the fourth quarter pulled back on their share repurchases by 7.2% from the fourth quarter 2015, although they accelerated 20.6% sequentially.

Companies spent $135.3 billion buying back their shares during the fourth quarter, compared to $112.2 billion from the third quarter and $145.9 billion in the fourth quarter 2015. For the full year, they spent $536.4 billion on buybacks, a decline from $546.4 billion in 2015 and $553.3 billion in 2014 – the first time the index saw two consecutive years of declines since the financial crisis era or 2008 and 2009.

A longer-term but potentially much bigger problem for equities can be found in the structure of US retirement savings accounts. At age 70, holders of IRAs are required to start cashing them out, and as the number of Boomer retirees soars the size of these required sales will rise commensurately. Here’s a snippet from a longer analysis by Economica’s Chirs Hamilton. The full article is here.

Simply put, investing for the long term had it’s time but that time is drawing to a close. The math is pretty easy…we’ll have too many sellers and too few buyers. Why? At age 70.5 years old, retirees are mandated by force of law to sell tax deferred assets accumulated over their lifetime and do so in a 15 year period. Conversely, buyers, incented by tax deferral (but not forced to buy by law), generally have a 35yr window of accumulation. Over the past 65 years (on a population basis), there were three new buyers for every new seller. Over the next 25 years (on a population basis), there will be three new sellers for every new buyer.

In the next downturn, corporations will stop buying — as they always do at bottoms — and retirees will be forced by both necessity and law to liquidate some of their nest eggs. Combined, these sales will put unacceptable downward pressure on stock prices, leading to the kinds of instability that over-leveraged systems can’t handle.

The Fed – and probably the ECB – will then join the BOJ and SNB in buying equities. Like QE and the other recent monetary experiments, this might be seen by mainstream economists as a good thing. But it’s not. For at least three reasons why it’s not, see We’re All Hedge Funds Now, Part 4: Central Banks Become World’s Biggest Stock Speculators for at least three reasons why it will make a bad situation infinitely worse.

Real estate is moving in many spots around the globe. You’ll never guess where the hottest European real estate market can be found. Where the money is headed. Is there still be an elimination of the tax exemption for a home office?

…also from Michael: The Key To Keystone’s Great Stock Market Success

While Washington is buried in bungled health care reform and Wall Street is vexed about possibly jinxed tax reform, both seem to have lost sight of the one, giant, intractable monster in the economy that virtually no one talks about any more: Debt.

While Washington is buried in bungled health care reform and Wall Street is vexed about possibly jinxed tax reform, both seem to have lost sight of the one, giant, intractable monster in the economy that virtually no one talks about any more: Debt.

They seem to forget that excess debt was the repeat offender behind the bank failures of the 1980s, the subprime mortgage disaster of 2007, the global market meltdowns of 2008, the Great Recession of 2009 and the multiple European debt crises of 2008-2015.

Worse, they seem to ignore the fact that the last 7.5 years of near-zero interest rates and unbridled money printing have only encouraged still more debt pile-ups. “Money is dirt cheap, so why not?” say officials in Congress, the White House, the Treasury Department, and government agencies.

“As long as the government’s debt burden is under 100% of GDP,” they tell you, “we can handle it. It’s only when it surpasses the 100% threshold that we’ll be in danger.”

True or false? Let’s look at the numbers …

- U.S. GDP is $18.6 trillion. And …

- U.S. Treasury debts outstanding are $16 trillion.

- So that means the debts are under the 100% danger threshold, right?

Wrong! That calculation conveniently excludes government debts that have piled up on the books of U.S. government agencies and U.S. government-sponsored enterprises, such as the Federal Home Loan Banks, Federal National Mortgage Association (Fannie Mae), Federal Home Loan Mortgage Corporation (Freddie Mac), Farm Credit System (FHS) and others.

How much? According to the Federal Reserve’s Flow of Funds, as of year-end 2016, they have a massive $8.5 trillion of additional debts.

These agencies were created by the U.S. government, are controlled by the U.S. government, and during the last debt crisis, were the biggest failures to be bailed out by the U.S. government. After that experience, how anyone in their right mind could continue to exclude their debts from the U.S. government’s books is beyond me. And yet that’s precisely what Washington has been doing all along, whether under Clinton, Bush, Obama or Trump.

Add those debts to the government’s total burden … and guess what! Instead of $16 trillion in U.S. government debts outstanding, the actual total comes to $24.5 trillion, or a whopping 132% of GDP!

How bad is that? Even with the recent growth in the U.S. economy, the government debt load today is significantly larger than it was during the Great Recession and the Debt Crisis.

And from a longer term perspective, it’s absolutely horrendous. Compare it to the 1980s, when banks and S&L went under by the thousands. In those days, government debt (even including government agencies) was close 40% of GDP. Today it’s more than three times bigger.

Or compare it to year-end 1970, about eight months before President Richard Nixon devalued the dollar and abandoned the gold standard. Then, the U.S. government debt burden was only 32.9% of GDP. Now, at 132%, it’s over four times larger — in a nation that’s far more difficult to govern or reform than it was in the 1970s. Moreover …

At 132% of GDP, the U.S. government now has roughly the same debt troubles as Italy. Worse, it now has a larger debt burden than Greece had before its collapse of years ago.

And this doesn’t even begin to include the U.S. government’s obligations for Medicare, Social Security, veterans’ benefits and more.

Will these shocking realities hinder private corporations in their quest for bigger profits, prevent investors from piling into the stock market, or stop the Dow from continuing its upward rampage? Probably not yet.

Will it return to haunt the Fed, the U.S. Treasury, Congress and Mr. Trump? Probably sooner than later.

Which market will be the first to feel the impacts? Government bond markets, of course. Expect long-term bond prices to begin a secular decline, culminating in collapse, as their yields begin a long-term rise, culminating in an explosive surge.

Good luck and God bless!

Martin

Collapsing oil prices are only the beginning as fossil fuels are turning into a historic relic, says Kenneth Ameduri, chief editor of Crush the Street. He discusses two commodities whose demand he expects to skyrocket as the world shifts to cleaner energy.

Elon Musk is at the forefront of this movement with his innovations that are turning fossil fuels into a historic relic. Some say oil’s true price per barrel with the “supply glut” that exists and the innovations in the battery space is $20 per barrel.

….also:

As Uranium Price Turns, Insiders Stock Up on Energy Fuels

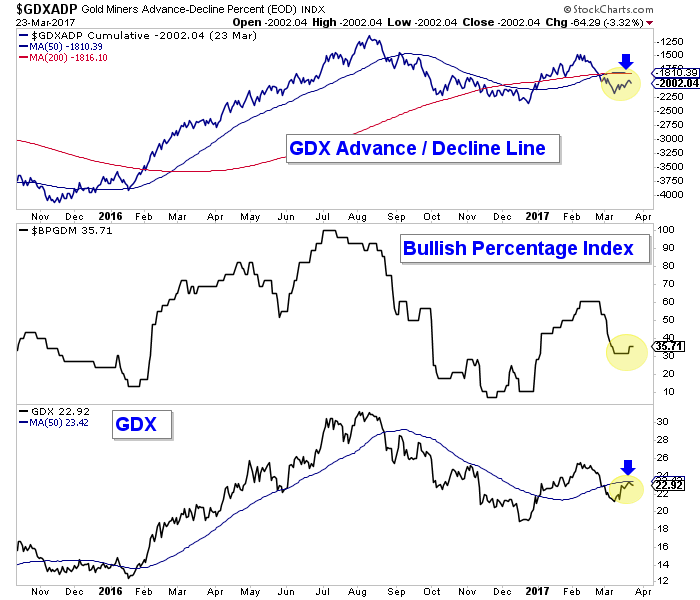

Last week we wrote that precious metals should see upside follow through but to be wary of the 200-day moving averages and February highs before becoming excited. The metals did follow through as Gold gained 1.5% and Silver gained 1.9% (for the week) but the miners disappointed. GDX gained only 1.1% while GDXJ finished in the red as did junior silver companies (SILJ). As spring beckons, the gold stocks are showing relative and internal weakness.

Two signs of weakness in the miners are visible in the weekly candle charts below. First, while Gold has already rallied back to its high the first week of February, GDX and GDXJ are down 11% and 15% respectively. The miners and the metals will not always be perfectly aligned but that is a rather stark divergence. Secondly, although Gold closed at the highs of the week in each of the past two weeks the miners failed to hold their gains. This is not exactly the type of price action that inspires more gains in the short term.

Gold, GDXJ, GDX Weekly Candles

Gold stocks are also showing some internal weakness. In the chart below we plot the advance/decline (A/D) line for GDX and its bullish percentage index (BPI). Both are breadth indicators. The A/D line is the holy grail of leading indicators while I have found the BPI to be more of a confirmation or overbought/oversold indicator. At present, the A/D line is below both its 50 and 200-day moving averages which are flattening and soon to slope lower. That is ominous if the A/D line can’t regain those moving averages. Meanwhile, the BPI is only at 36%. This means it has room to move up but it also shows weakness as it has barely changed despite gains in recent weeks.

x

xPart of the cause of weakness in the gold stocks (and relative strength in Gold) is the weakness in the stock market which is actually a welcome and positive development for precious metals. As we discussed in a recent video, precious metals are currently setup to benefit from weakness in the stock market as they were in the 1970s and early 2000s. Patience is needed though as stock market weakness is not necessarily an instant or immediate catalyst for the gold stocks.

The current weak technical action in the gold stocks is further evidence that precious metals are unlikely to see a blast off anytime soon. Gold could continue to rally on the back of stock market weakness but don’t expect that to pull miners much higher. I reiterate that at present it’s not wise to chase strength in the miners. Instead, traders and investors should be patient and wait for (presumably) lower prices and a better entry point. We continue to look for high quality juniors that we can buy on weakness and hold into 2018.

Jordan Roy-Byrne, CMT, MFTA

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair