There probably only is a remote possibility that the S&P 500 (NYSE:SPX) topped out as 2,395 on the 1st of March last week as equities, in my opinion, will remain elevated until the FOMC meeting.

Following President Trump’s speech the Dow Jones Industrial Average (Dow) easily broke 21,000, and closed at another all-time high – 21,115.

Following President Trump’s speech the Dow Jones Industrial Average (Dow) easily broke 21,000, and closed at another all-time high – 21,115.

The Dow closed up for the 12th consecutive day on Monday February 27, another three decade record.

Excel calculated the Dow’s daily Relative Strength Index (RSI – 14 period), a technical timing oscillator. It reached 97.75 (maximum = 100.00) on March 1, an exceptionally “over-bought” reading that has occurred nine times since 1950.

The weekly RSI also reached a very high “over-bought” reading as of March 3, the end of last week.

Margin debt recently registered an all-time high on the NY exchange. Price to earnings ratios have risen into “nosebleed” territory, and the last 1% correction in the S&P was in November – a long time ago. Many other market extremes and highs in confidence indexes are evident.

The Dow reached new highs the normal way – levitated through the creation of massive unpayable debt and the expectation of huge profits (for traders). Daily sentiment has reached a peak and indicates we are at or near a top. Read Bob Moriarty.

Official national debt is nearly $20 trillion. Regardless, President Trump promised something for everyone:

The Dow likes more debt, until reality strikes.

Previous Peaks in the Dow: (National debt in $ billions.)

Date Dow Official National Debt Ratio Dow to Debt

Jan. 1973 1,067 450 2.37

Aug. 1987 2,746 2,330 1.18

Jan. 2000 11,750 5,776 2.03

Oct. 2007 14,198 9,055 1.57

Mar. 2017 21,115 19,960 1.06

But it takes more debt to buy each Dow point than it did several decades ago. How much debt will be needed to levitate the Dow to 30,000? Will it require $40 trillion in debt? And what are the consequences of massively more debt? Stagflation is on the horizon.

Consequences of the spending problem according to Ron Paul:

“That leaves only one solution: printing money out of thin air.” [But] “printing money out of thin air destroys the currency, hastening a US economic collapse and placing a very cruel tax on the working and middle classes as well.”

His solution for US government policy:

“… end the US military empire overseas, cut taxes and regulations at home, end the welfare magnet for illegal immigration, and end the drug war. And then get out of the way.”

These ideas will encounter fierce resistance, so much that his plan is clearly “dead on arrival.”

More debt is guaranteed by a century of fiat currency devaluations, a borrow-and-spend congress, the executive branch, central banks that love debt, and an economy that runs on debt and credit. Expect continued dollar devaluation and more Dow highs after a nasty correction/crash.

While the Dow corrects and the U. S. economy struggles in a fiat currency induced coma, gold and silver prices will rise.

CONCLUSIONS:

Gary Christenson

The Deviant Investor

Donald Trump’s election and subsequent comportment stirred emotions and provided entertainment.

Donald Trump’s election and subsequent comportment stirred emotions and provided entertainment.

But the critical question was always simple: does this administration represent a break with the pattern of the last 40 years… or a continuation of it?

Reagan, Bush, Clinton, Bush II, Obama – all of them have taken our political economy in essentially the same direction. More debt. More Deep State control. More consolidation of power in the executive branch (including the military).

A new president always has some influence. Typically, he can rearrange the furniture and hand out some choice sinecures.

But not since John F. Kennedy has any president dared to change the direction the government is going or challenge the real power of those who run it.

And today, it would take an almost superhuman leader to do so.

Mr. Trump sounded, at times, as if he posed a threat to the elite. Liberals acted as though he were a devilish scourge sent by evil gods.

Conservatives allowed themselves to believe he was the long-awaited messiah.

And now we see that “The Donald” – for all his late-night tweets and bull-in-a-china-shop bluster – is all too human, prone to sin and error… just like the rest of us.

Most likely, the important trends of the last four decades will intensify as the insiders use the chaos and distraction of the Trump team as cover to take even more power and wealth from the American people.

In short, our guess is that there will be plenty of little surprises coming from this administration, but no big ones.

President Trump has already proposed to shuffle more cash to the generals and to the jailers. Soon, we will see more money grabs… from the insiders in finance.

Among the coming non-surprises will be the feds’ reaction to a crash on Wall Street… or a recession on Main Street.

Here’s a shorthand for how it will probably go down: crash and/or recession = QE4, direct asset purchasing by Fed, and helicopter money = more wealth for the cronies.

The U.S. economic expansion – albeit weak by historic standards – has gone on for 93 months. That makes it the third longest in history.

If it goes on another 27 months, it will set a new record: the longest expansion on record uninterrupted by a recession.

Although that sounds like an achievement, it is like setting a new record for eating jalapeno peppers: you know you’re going to be sick soon.

Economies make mistakes; corrections clean them up. Typically, the interest rate serves as a “hurdle.” If your project can’t produce enough money to pay for the cost of the capital that went into it, it gets eliminated.

But if you reduce the cost of capital to almost nothing by way of ultra-low interest rates, you never have to reckon with your mistakes. Today, the hurdle is so low, you can’t even trip over it.

The errors stay in place – misallocating more precious savings and consuming more real wealth.

Meanwhile, the stock market is at record levels.

On a CAPE ratio basis – which looks at stock prices relative to the average of the last 10 years of earnings – only three times since 1929 has the S&P 500 been so pricey, all of them in the last 18 years: first in 1999, then in 2007, and again now.

And like the business expansion, this bull market must contain trillions of dollars of uncorrected errors.

And for the same reason: when capital is almost free, it’s hard for businesses to stumble. They don’t go out of business… They just refinance… merge… acquire a competitor… and buy more of their own shares.

But wait… CBC News reports:

Federal Reserve chair Janet Yellen gave investors a pretty clear sign on Friday that the U.S. central bank is likely to raise its benchmark interest rate later this month – and more hikes to follow later this year.

In a speech on the central bank’s economic outlook at the Executives’ Club of Chicago on Friday, the Fed chair told the gathered audience that a slight increase to the federal funds rate would be “appropriate” when the bank next meets for a two-day policy meeting on March 14 and 15.

And here we can be clear about what the Fed won’t do…

There will be no big surprise coming from that quarter either: the Fed will only raise rates to the extent that it is irrelevant.

In its meeting, the members of the Fed’s policy setting committee, the FOMC, will vote on whether to raise rates one-quarter of a percentage point.

We don’t know which way that will go. But we know it won’t matter. Because if it did matter, they wouldn’t do it.

That’s really what Ms. Yellen means by “appropriate.” It will only be appropriate if it doesn’t cause or exacerbate a correction; that is, they will only raise rates as long as it doesn’t interfere with the debt bubble.

If the Fed’s “data” appear weak… and even a tiny increase might prick the bubble… there’ll be no rate increase.

The deeper meaning of this is that the Fed, Wall Street, the Pentagon, and Team Trump are all in sync.

None wants to upset this apple cart. It would reveal too many rotten pieces of fruit in the pile. All now collude with the media to keep the public distracted and off-balance, while the whole shebang keeps rolling along.

The Trump administration picks unnecessary fights with unimportant adversaries… pretending to be defending the common man. The media is confused… and confuses the public even further.

The Pentagon goes about its business… happily scaring the public in order to transfer money and power to itself and its crony pals.

Wall Street provides the illusion of prosperity… bidding up stock prices as though they were made more valuable by the administration’s dumb-head policies.

And the Fed provides as much fake money as necessary to keep the scam alive.

But the first big test can’t be long in coming. The feds are running up against their debt ceiling.

There again, the sound and fury will sell newspapers. Democrats will fume. Republicans will fret. But it will be essentially meaningless agitprop.

All of the main players are firmly committed to more spending. They won’t let prudent legislation or a $20 trillion deficit stand in their way.

Here’s pseudonymous blogger Tyler Durden at Zero Hedge:

While in recent weeks there has been a material increase in Fed balance sheet normalization chatter, according to a new report from Deutsche Bank analysts, it may all be for nothing for one simple reason: should the U.S. encounter a recession in the next several years, the most likely reaction by the Fed would be another $1 trillion in QE, delaying indefinitely any expectations for a return to a “normal” balance sheet.

No return to “normal.” Not voluntarily. Empires don’t back up. And bubbles don’t prick themselves.

Regards,

Bill

BY CHRIS LOWE, EDITOR AT LARGE, BONNER & PARTNERS

What’s the best-performing global stock market since President Trump’s inauguration?

The answer may surprise you…

Because it’s also the worst-performing global stock market since Trump’s win over Hillary Clinton on Election Day.

The answer to this riddle: Mexico.

Today’s chart is of the iShares MSCI Mexico Capped ETF (EWW). It tracks the performance of a broad range of Mexican stocks.

And as you can see, EWW is down 9% since Election Day – making it the WORST-performing country stock market over this period.

But it’s up 12.5% since Inauguration Day – making it the BEST-performing country stock market over the following period.

Why such a roller-coaster ride?

One explanation is that investors panicked and dumped Mexican stocks based on candidate Trump’s fiery rhetoric on trade south of the border.

They then started to re-evaluate this bearish stance based on what they’ve since learned of President Trump.

Further evidence, as Bill says, that never before has politics been so important for markets.

– Chris Lowe

– I am expecting the market to drop into an intermediate low sometime soon.

– The robo ratio is slowly demonstrating that retail investors are becoming more bullish.

– Investors must only buy quality (or stay in cash) with the market trading at all-time highs.

There probably only is a remote possibility that the S&P 500 (NYSE:SPX) topped out as 2,395 on the 1st of March last week as equities, in my opinion, will remain elevated until the FOMC meeting.

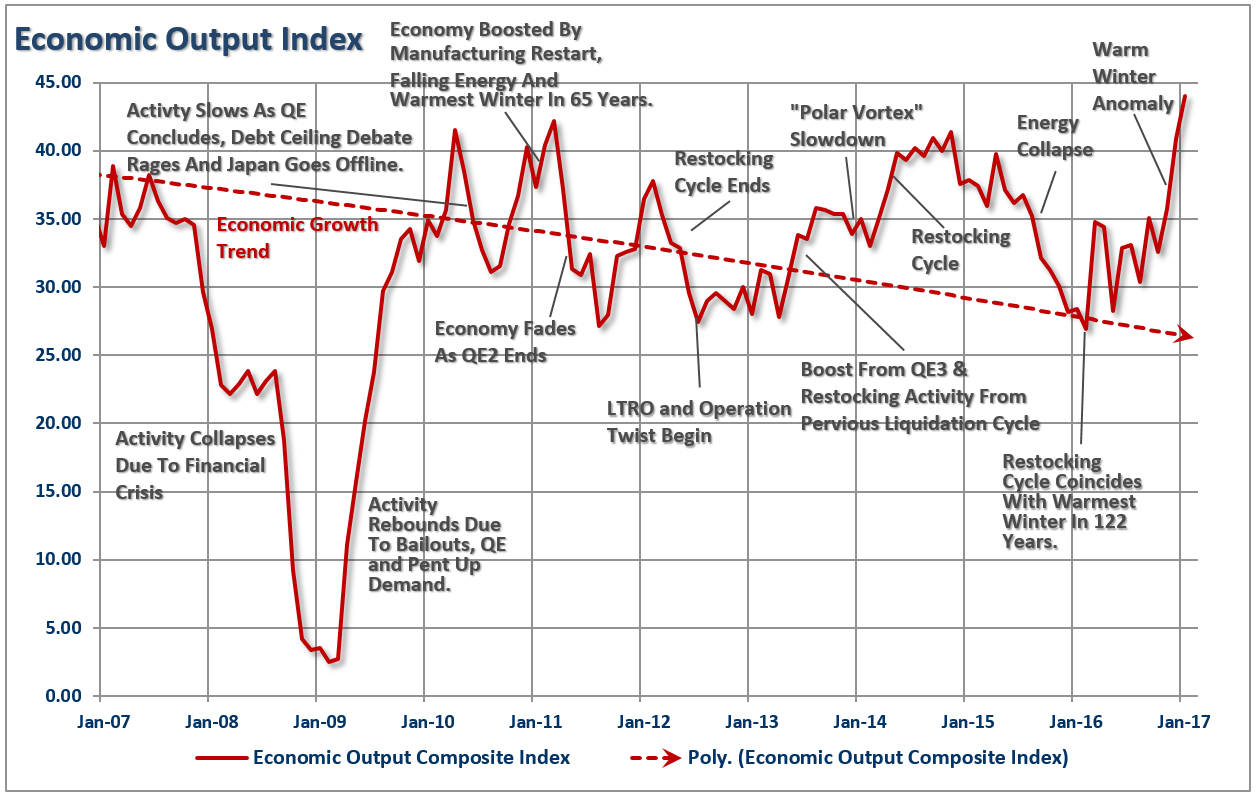

The month of March typically marks the beginning of Spring. This weekend will also mark the loss of an hour of sleep as we set our clocks forward an hour in observance of daylight savings time.

As we will discuss momentarily, the month of March begins following an unseasonably warm winter period that allowed for manufacturing activity to occur during a period where inclement weather normally abounds. This is an interesting point because two years ago, the BEA adjusted the “seasonal adjustment”factors to compensate for the cold winter weather over the previous couple of years which had suppressed first quarter economic growth rates. (The irony here is that they adjusted adjustments for cold weather that generally occurs during winter.) However, the problem with “tinkering” with the numbers comes when you have an exceptionally warm winter. The new adjustment factors, which boosted Q1 economic growth during the last two years now creates a large over-estimation of activity during the first quarter of a year where winter weather is unseasonably warm.

This anomaly has boosted “bullish hope” as the fear of an economic slowdown has been postponed. At least temporarily until the over-estimations are revised away over the course of the coming months. Of course, with the spread between “hope” and “reality” currently at some of the highest levels ever, it is worth paying attention to what happens.

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

A sane voice in a scrambled investment world.

~ Ed R.

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}