Currency

If the road to hell is paved with good intentions, American’s exorbitant privilege might be at risk with broad implications for the U.S. dollar and investors’ portfolios. Let me explain.

The U.S. was the anchor of the Bretton Woods agreement that collapsed when former President Nixon ended the dollar’s convertibility into gold in 1971. Yet even when off the remnants of the gold standard, the U.S. has continued to be the currency in which many countries hold their foreign reserves. Why is that, what are the benefits and what are the implications if this were under threat?

Let me say at the outset that the explanation I most frequently hear as to why the U.S. dollar is the world’s reserve currency – “it is because of tradition” – which is in my opinion not a convincing argument. Tradition only gets you so far – it ought to be policies and their implementation that guide investors.

Wikipedia’s definition of exorbitant privilege includes:

“The term exorbitant privilege refers to the alleged benefit the United States has due to its own currency (i.e., the US dollar) being the international reserve currency.[..]

Academically, the exorbitant privilege literature analyzes [..] the income puzzle [which] consists of the fact that despite a deeply negative net international investment position [NIIP], the U.S. income balance is positive, i.e. despite having much more liabilities than assets, earned income is higher than interest expenses.”

In the context of today’s discussion, I would like to focus on what I believe may be the most under-appreciated yet possibly most important aspect of the so-called exorbitant privilege: what makes the U.S. so unique is that it is de facto acting as the world’s bank. A bank takes on (short-term) deposits and lends long-term, capturing the interest rate differential.

Applied to the U.S. as a country, investors borrow cheaply in the U.S., and seek higher returns by investing in the rest of the world. In the investment world, we also refer to this as carry, i.e. one might say the U.S. engages in an amazing carry trade. As long as this ‘carry trade’ works, it is quite a charm. That said, there are those who are concerned that the party cannot last forever. To quote from our own past writings, the former head of the European Central bank Wim Duisenberg said in 2003: ‘We hope and pray the global adjustment process will be slow and gradual.” — In fact, a reference to a “disorderly adjustment of global imbalances” was a risk cited by the ECB every month in its statement until about the time current head, Draghi, took over. This “adjustment process” is a thinly veiled reference to a potential dollar crash.’

So is there reason to believe the U.S. may no longer be serving as the world’s bank? At first blush, the answer would be no, as the U.S. has deep and mature financial markets. However, there are developments of concern:

-

The first has already happened. Due to a regulatory change, our analysis suggests it is less attractive to issue debt in U.S. dollars for anyone other than the U.S. government. The regulatory change might look arcane at first, but in our Merk Insight “The End of Dollar Dominance?”, we argued that a quirk in money market fund rules that could be interpreted as an implicit subsidy for issuers of debt has gone away. It’s more than a quirk because funding cost for just about everyone other than the U.S. government has gone up, as evidenced by elevated intra-bank borrowing rates (LIBOR rates) independent of the rise in Federal Funds rate. If our analysis is correct, it means that the U.S. dollar is a less attractive currency to raise money in than it had been. These days, issuers might as well issue debt in euros, a trend exacerbated by the extraordinarily low interest rates in the Eurozone.

Let me provide the link to U.S. Treasuries as reserve holdings: take an emerging market corporate issuer raising money in U.S. dollars because of what used to be a funding advantage: upon issuing debt (raising cash), they might sell dollars to buy the emerging market currency to fund their operations. In the meantime, their government buys U.S. dollars and subsequently U.S. Treasuries to sterilize the corporate issuer’s sale of the dollar. Due to regulatory changes in U.S. money market, it may now be no longer advantageous to issue debt in U.S. dollars, eliminating the downstream effects, including the holding of Treasuries as a reserve asset.

-

A second change is under consideration: the House GOP tax proposal would eliminate the deductibility of net interest expense. If passed, it could have profound implications on how issuers around the globe get their funding, as we shall explain below.

If corporate America can no longer deduct net interest expense, we believe it will make the use of debt less attractive. It would discourage the use of leverage. Banks use a lot of leverage. And, as we are pointing out, one can look at the U.S. as a whole as if it were a bank. A system with less leverage may well be more stable; however, a system that uses less leverage may also have less growth.

From the point of view of America’s exorbitant privilege, the key question in our view is how the world reacts. A plausible scenario to us is that American CFOs will move leverage to overseas entities where interest continues to be deductible. Similarly, to the extent that foreign issuers in the U.S. used U.S. legal entities to raise money, they would likely raise funds through foreign entities where interest expense would still be deductible. The question then becomes whether the money raised from these (newly minted) foreign entities would be in U.S. dollar or in foreign currency. If they raise money in foreign currency, the U.S. dollar would be cut out as the “middleman,” jeopardizing American exorbitant privilege.

If you take a U.S. firm, if they decide to use foreign subsidiaries to issue debt, they might want to also report more revenue overseas to make it worthwhile to deduct more. CFOs are highly paid, in part we believe, because of their ability to engineer where to recognize revenue and expenses. We would expect CFOs to rationally optimize shareholder value in the context of the regulatory and tax framework they are presented with. Once you take the step of recognizing more revenue abroad, it would only be prudent to match the liability, i.e. the interest expense, in the same currency.

But won’t the U.S. be a more attractive place to invest if the entire GOP tax plan gets passed? What about if the U.S. changes to a territorial tax system? What about the border adjustment tax (or a variant thereof)?

-

If the U.S. were to move to a territorial tax system, i.e. no longer tax corporations on their global income, it may provide a further disincentive to issue U.S. debt. In the current tax system, corporations issue U.S. debt to fund domestic operations while avoiding the repatriation of foreign earnings.

-

The concept of a border adjustment tax still needs to take shape before we can have a more definitive opinion about it. From what we see, it appears to foremost provide a one time shock to the system (possibly causing a one time inflationary impact as the cost of higher imports gets passed on to consumers); that said, corporate America might come up with a variety of tricks to mitigate the impact of such a tax (e.g. exporting fuel to their plant in Mexico, thus being able to deduct the cost of energy from imported goods).

-

Not much discussed, but a potential U.S. dollar positive would be if indeed investments could be fully expensed the first years rather than a requirement to amortize expenses over many years, as in the current tax code. That is, if the U.S. incentivized investments over spending. We’ll discuss this in more detail once we have more clarity on the actual tax reform.

There’s still one more component: a U.S. government that needs to issue a lot of debt to fund its budget deficits. To the extent that foreign governments have less of a need to hold U.S. dollar reserves, funding costs for the U.S. government might rise. While some may believe higher borrowing costs might be a positive for the dollar, the opposite may be true if the Federal Reserve has to keep rates artificially low to prop up an economy that would otherwise deflate; or because government deficits would otherwise be unsustainable. The point being here that the U.S. dollar might become more vulnerable should fiscal and monetary policy not be sound…

In summary, providing a disincentive for debt might make the world more stable, but lead to lower growth. It might encourage more issuance of debt in local currency, something that might also be healthy for global stability, but might leave the U.S. and the greenback behind.

To expand on the discussion, please register for our upcoming Webinar entitled ‘Trump or Dump Gold?’ on Thursday, February 16, to continue the discussion. Also make sure you subscribe to our free Merk Insights, if you haven’t already done so, and follow me at twitter.com/AxelMerk. If you believe this analysis might be of value to your friends, please share it with them.

Axel Merk

Merk Investments, Manager of the Merk Funds

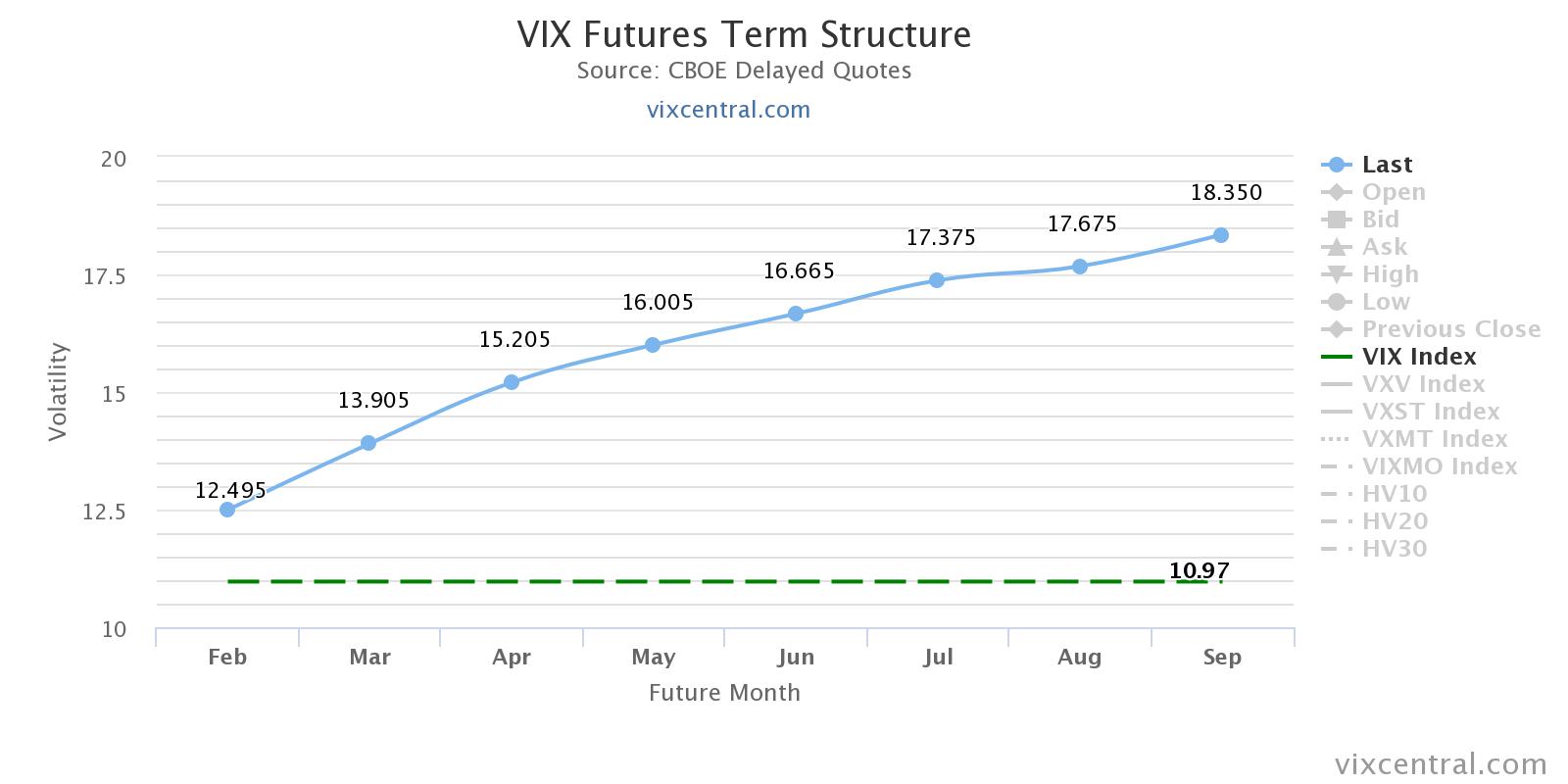

Summary

– Even after a small gain last week, the VIX is still near its lows.

– Long and short VIX strategies both have arguments in their favor.

– A Long VIX bias may be warranted, but active risk management is a must.

– Investors need to be nimble to take advantage of VIX spikes and switch to a short bias.

When the paper markets finally collapse, the silver market is set up for much higher price gains than gold. Why? Because the fundamentals show that precious metals investment demand has put a great deal more pressure on the silver supply than gold… and by a long shot.

There are three crucial reasons why the silver price will outperform the gold price when the highly inflated paper markets disintegrate under the weight of massive debt and derivatives. While many precious metals investors are frustrated by the ability of the Fed and Central Banks to continue to prop up the markets, the longer they postpone the day of reckoning, the worse the collapse.

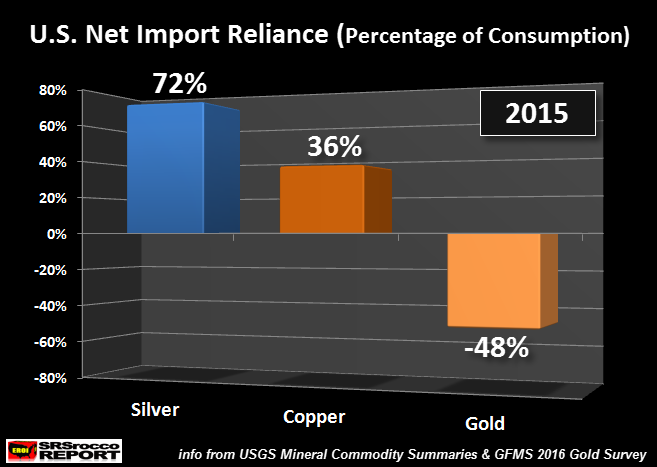

The first reason I wrote about in my article, Critically High U.S. Silver Supply Reliance In Jeopardy When Paper Markets Crack:

the United States silver net import reliance as a percentage of total consumption, was 72%, versus 36% for copper and a negative 48% for gold.

This chart shows that the U.S. relied upon 72% of its domestic silver demand from foreign sources in 2015. Thus, U.S. silver supply reliance (72%) is double that of copper (36%), while U.S. gold demand enjoyed a 48% surplus versus its domestic supply.

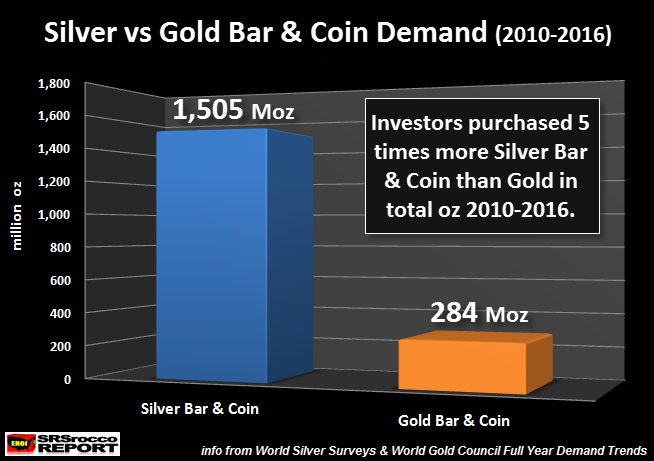

The second reason the silver price will surge higher than the gold price is due to the amount of physical silver, in total ounces, purchased by investors versus gold:

From 2010 to 2016, investors purchased a total of 1,505 million oz (Moz) of silver bar and coin compared to only 284 Moz of physical gold. Thus, precious metals investors purchased five times more silver ounces, than gold ounces during this seven year time period.

Of course, the total value of physical gold investment was much higher than silver during this time period, but this tremendous amount of silver bar and coin demand has impacted the silver market much greater than the gold market.

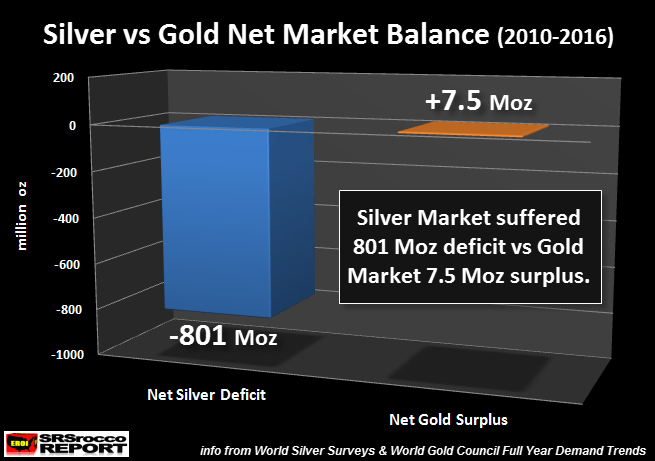

This brings me to the third reason. Due to the huge amount of silver bar and coin demand since 2010, the silver market suffered a net deficit of 801 Moz. However, the 284 Moz of gold bar and coin demand did not impact the gold market the same way. According to the World Gold Council, the gold market enjoyed a small 7.5 Moz net surplus during this time period:

While it is true that World Gold Council may be underestimating Chinese physical gold demand, and its impact on the annual surplus of deficit figures, a 7.5 Moz surplus is only 3% of the 284 Moz total gold bar and coin demand figure 2010-2016. However, the 801 Moz net silver deficit is more than 50% of total silver bar and coin demand during that same time period.

Which means, physical silver investment demand is causing much more stress on the silver market than it is on gold. While the silver market has been able to supplement the annual deficits with old silver coin stocks or large bars that were liquidated during the 1990’s, this is not an endless supply.

According to the data I obtained from the GFMS Team at Thompson Reuters, invested dumped a net 580 Moz of silver bar and coin on the market between 1995-1999. Now compare that to the past five years (2012-2016) as investors purchased a net 1,152 Moz (1.15 billion oz) of silver bar and coin.

And here is the CLINCHER. From 1985 to 2007, the total net silver bar and coin demand was a NEGATIVE 95 Moz. Which means investors sold a net 95 Moz of silver bar and coin in that 23 year period. However, investors purchased a net 1,785 Moz of silver bar and coin from 2008 to 2016. This is a huge TREND CHANGE.

After the U.S. financial and economic meltdown in 2007, investors continue to purchase a record amount of silver bar and coin. This has put severe stress on the silver market as the total net deficit since 2008 surpassed 1,155 Moz.

While the silver market will continue to supplement the ongoing annual deficits with old silver stocks, this supply is not endless. Furthermore, the days of the TRUMP STOCK MARKET RALLY are numbered. The last time the stock market crashed 2,000 points in the beginning of 2016, investors flocked into gold and silver in a BIG WAY.

In conclusion, the fundamentals in the silver market are setting up for a much higher price spike than gold due to the three reasons stated in the article. The timing of these event is hard to forecast as it is difficult to pinpoint when the Fed and Central Banks lose control of their massive market intervention. My work is not meant to provide a short term outlook on the precious metals, rather it offers fundamentals that will win out over the medium to longer term.

Precious metals investors need to look at buying and holding gold and silver the same way an individual puts money away each month in their 401K, pension plan or retirement account. The difference between the precious metals investor acquiring PHYSICAL METAL compared to individual acquiring PAPER ASSETS or DIGITS, is one is real wealth, while the other is an IOU.

Those who transition out of PAPER-DIGIT IOU’s and into physical gold and silver before the FAT LADY SINGS, will be rewarded with much better options.

To understand why the markets may be heading for big trouble, check out my article, A Large Crack Appeared In The Global Market… And No One Noticed.

Check back for new articles and updates at the SRSrocco Report.

Europe could become the site of a new global war in the East as tensions build there against refugees and the economic decline fosters old wounds. The EU is deeply divided over the refugee issue and thus it is fueling its own demise and has failed to be a stabilizing force. After five days of demonstrations, Romania’s month-old government backed down and withdrew a decree that had decriminalized some corruption offenses. They were still acting like typical politicians and looking to line their pockets. After one month, the people have been rising up saying “We can’t trust this new government.”

Europe could become the site of a new global war in the East as tensions build there against refugees and the economic decline fosters old wounds. The EU is deeply divided over the refugee issue and thus it is fueling its own demise and has failed to be a stabilizing force. After five days of demonstrations, Romania’s month-old government backed down and withdrew a decree that had decriminalized some corruption offenses. They were still acting like typical politicians and looking to line their pockets. After one month, the people have been rising up saying “We can’t trust this new government.”

….also from Martin:

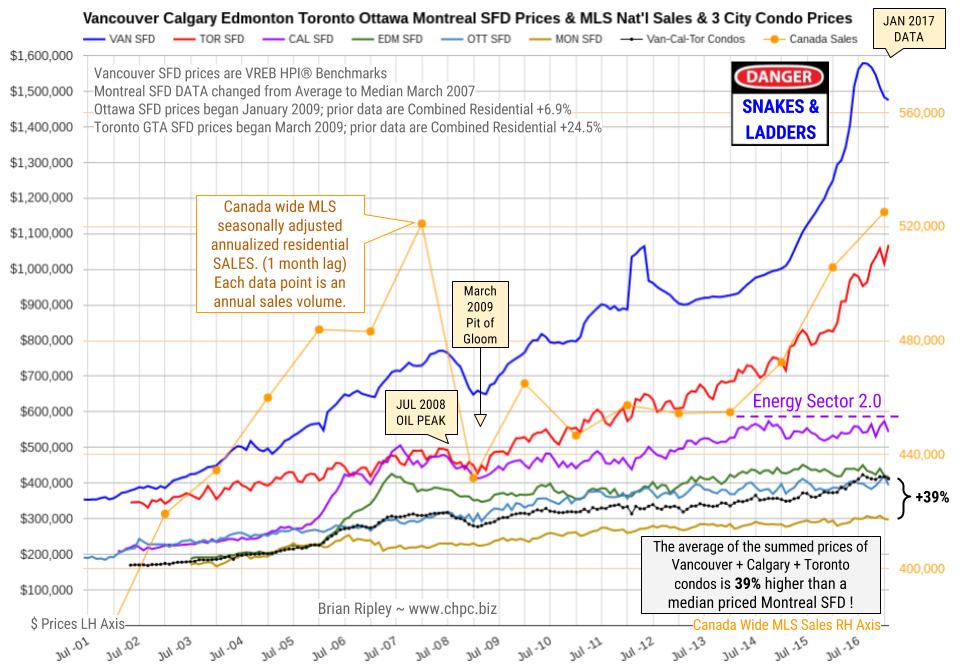

CLICK CHART TO ENLARGE

The chart above shows the average detached housing prices for Vancouver*, Calgary, Edmonton, Toronto*, Ottawa* and Montréal* (the six Canadian cities with over a million people each) as well as the average of the sum of Vancouver, Calgary and Toronto condo (apartment) prices on the left axis. On the right axis is the seasonally adjusted annualized rate (SAAR) of MLS® Residential Sales across Canada (one month lag).

In January 2017 Canada’s big city metro SFD prices coiled about or slid off their near term highs except in Toronto where detached houses and town houses fetched new peak prices. Anyone owning a house in the scorching hot Toronto market is sitting on an unredeemed lottery ticket. In Vancouver scorched earth ruins are beginning to appear. Notice Calgary prices are labouring under the new Energy Sector 2.0 which could be anticipating the Trumpster’s U.S. energy independence.

….related: The Canadian Real Estate Plunge-O-Meter (The Plunge-O-Meter tracks the dollar and percentage losses from the peak and projects when prices might find support.)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair