Current Affairs

Canadian military leaders saw the pandemic as a unique opportunity to test out propaganda techniques on an unsuspecting public, a newly released Canadian Forces report concludes.

The federal government never asked for the so-called information operations campaign, nor did cabinet authorize the initiative developed during the COVID-19 pandemic by the Canadian Joint Operations Command, then headed by Lt.-Gen. Mike Rouleau.

But military commanders believed they didn’t need to get approval from higher authorities to develop and proceed with their plan, retired Maj.-Gen. Daniel Gosselin, who was brought in to investigate the scheme, concluded in his report.

The propaganda plan was developed and put in place in April 2020 even though the Canadian Forces had already acknowledged that “information operations and targeting policies and doctrines are aimed at adversaries and have a limited application in a domestic concept.”…read more.

The price of natural gas has soared to a 13-year high, as fears over scarcity ahead of the winter months intensifies.

October futures for natural gas jumped by more than 10% on Monday to close at US$5.86 per million Btu, marking the sharpest increase since February. November futures were also up on Monday, hitting a fresh high of nearly US$6 per million Btu— the highest since November 2008. Energy prices have been on a steep rise over the past several weeks, particularly as low reserves in Europe and China ignite fears over widespread shortages ahead of the cold season.

The steep rise in natural gas prices has been unprecedented across Europe, and is expected to be even worse than the US oil price shock of the 1970s, according to estimates from Rabobank. European natural gas prices have soared to above $25 per million Btu, which is a staggering 400% more than the average of the past decade, and significantly higher than the commodity’s price in the US…read more.

For the past several years, the strain of financial stress has left Safiya Mayers with depression, anxiety, fatigue, aching muscles, weight fluctuations and chest pains.

The 25-year-old facilities coordinator in Toronto said she experienced considerable stress paying for tuition and rent as a university student in her early 20s, while also taking on student debt. She’s no longer in school, but a significant portion of her income goes towards paying rent, leaving it difficult to repay loans or build sizable savings.

“I have to move in December and I’m mostly likely going to have to sacrifice either a social life or renting my own place. When I think about my future, I have a lot of anxiety because I don’t have a cushion. I don’t have that proper foundation to know that I’m OK if the ground were to shake,” she said.

“I feel like my early 20s have been taken from me because I was always worried about my finances, which in turn has affected my health.”

Mayers isn’t alone. According to FP Canada’s Financial Stress Index, published in June 2021, 39 per cent of Canadians polled under 35 say that financial stress has led to health issues and 11 per cent of respondents under 35 say that financial stress has led to mental health challenges or substance abuse. Comparatively, 28 per cent of those over 35 say financial stress has impacted their health and 5 per cent say it’s led to mental health challenges and substance abuse…read more.

Canada’s housing agency said the country is now at high risk of a sharp correction in home valuations as the continued appreciation in prices becomes unmoored from economic fundamentals.

The Canada Mortgage and Housing Corp. raised its market risk assessment to high from moderate on Tuesday, in a report showing both activity and prices remain near record levels reached earlier this year amid rock-bottom mortgage rates and a frenzy for bigger living spaces driven by the COVID-19 pandemic.

Though Canada has seen a rising vaccination rate and an improving economy since then, the strength in the housing market is still far beyond what’s warranted by these developments, with prices further detached from labor incomes, the agency said.

“We’re seeing price acceleration, over-valuation, and it’s increasing the vulnerabilities for Canada,” Bob Dugan, CMHC’s chief economist, said on a conference call with reporters. “Hopefully we don’t see a large fall in house prices.”

On top of the shift in the national outlook, the agency raised its risk assessment of Montreal’s housing market to high from moderate, bringing the number of Canada’s major cities deemed most at risk to six. Vancouver was a notable exception, seeing its risk assessment fall to low from moderate on an increase of homes on the market that’s caused price growth to settle down…read more.

Evergrande Monday

The Dow Jones futures contract dropped >1,300 points from last Friday’s highs to Monday’s lows and then rallied back > 1,300 points to Thursday’s highs – a ~2,600 point round trip in five trading sessions.

Here’s my take: The leading stock indices had rallied >100% from the March 2020 lows without so much as a 5% correction since October 2020. Monetary and fiscal stimulus had been the principal drivers of the rally; the rally was showing many signs of speculative excess, and any “catalyst” could trigger a correction. Looking ahead, the market could see that the Fed was going to start “taking away the punch bowl” (even if only a spoonful at a time), and the increasingly dysfunctional environment in Washington meant that fiscal stimulus was going to be scaled back. (Fiscal fatigue, as my friend Kevin Muir, calls it.)

In August, I wondered if developments in China would be contagious, but North American markets seemed “complacent,” with stock indices inching higher and higher while volatility metrics were near multi-year lows.

Last week I wrote: “The answer (to the contagious question) appeared to be “No,” in August, but now that the “stress” of September has arrived, the answer might be, “Yes, but with a delay.”

It was easy to imagine contagion within the over-levered Chinese real estate market, especially considering the recent “anti-capitalist” bend of the CCP (“homes are for living in – not for speculation”). It was also not difficult to imaging that contagion within China could trigger corrections in other markets.

The critical question seems to be, “What will the CCP do?” They are reshaping Chinese society (“common prosperity for all”) and seem more concerned with policy compliance than short-term market reactions. I expect more companies will “fail” with executives arrested, but I do not expect the CCP will allow chaos.

The market seems to have drawn the same conclusion (as Evergrande moved from a page 16 story in August to a front-page feature on Monday) and has bounced back from the lows.

What’s next?

The stock indices have historically been weak in September (especially the 2nd half), and then they rally into year-end. That may happen, but I can also imagine that the decline from the early September All-Time highs is only the first leg of a more significant correction.

An alternative view to the seasonal norm would be that this week’s rally has been a “reflexive” bounce from a market that is “used to” going up and that if it rolls over without making new highs and takes out this week’s lows, a deeper correction may develop.

Interest rates

As the S+P futures plunged ~180 points from last Friday’s highs to this Monday’s lows, Treasury bonds barely moved – they stayed inside the relatively narrow range they’ve been in since mid-July. I thought that was curious. Where was the “haven” bid for bonds when the stock market was in free fall? Even the Japanese Yen was getting a little “haven” bid.

Then the bonds rallied on Wednesday following what seemed to be a hawkish tilt from the Fed. I was genuinely perplexed. But bonds sold off hard on Thursday and Friday.

Not only were nominal yields rising, but real yields were also rising.

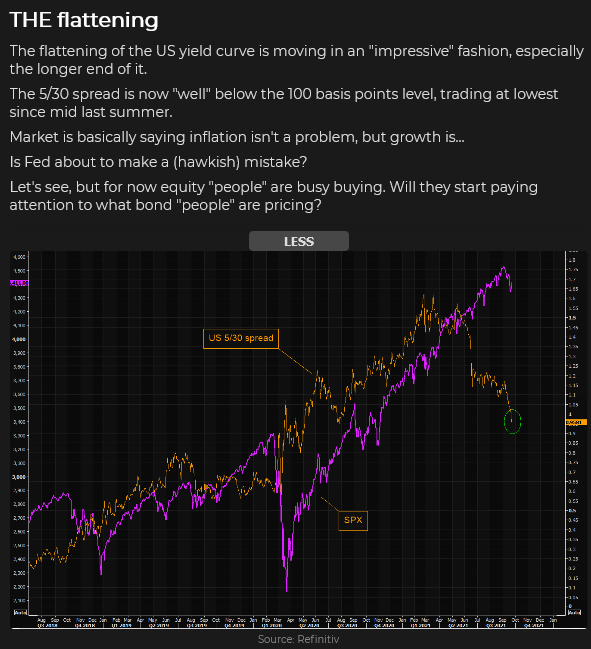

The yield curve has been flattening (don’t worry about inflation, the economy is slowing?)

volatility spike

I think of the S+P futures market as the best barometer for market risk on/off sentiment, but I also watch several different volatility metrics. S+P Vol gapped higher as markets got “back to work” after Labor day, then jumped to a 4-month high on Evergrande Monday, only to quickly retreat as the stock market rallied Tuesday through Friday.

Energy

Uranium prices have corrected after their sharp rally, New York Nat Gas has backed off from its highs, but crude oil and gasoline are aggressively bid.

Currencies

The US Dollar has sustained its rally from early September – especially against European currencies and the Yen.

The Canadian Dollar: strength/weakness in the S+P often impacts the CAD – this week, the CAD traded almost tick-for-tick with S+P futures. The relative strength/weakness of the USD Vs. other currencies also affects the CAD – but this week, as the USD was steady, the CAD rallied against most other currencies, perhaps because the commodity indices rallied to fresh 7-year highs – with a big boost coming from energy prices.

The Commitments of Traders report issued by the CFTC on Friday after the close (based on Tuesday, Sept 21 data ) shows the net long USD position to be the largest since Q1 2020. Large speculators were the shortest CAD they have been in over a year (remember they were hugely long in mid-June just after the CAD hit a 6-year high.) The AUD has a record net short position.

My short term trading

I started the week with a net short CAD position (short futures and short OTM puts.) I had been unable to bring myself to sell S+P futures in the hole the previous Friday but thought that the CAD would drop if the S+P kept falling.

The CAD tumbled with the S+P on Monday, and I wrote deeper OTM puts against my futures position. That was the high point of the week as far as my unrealized gains were concerned.

Monday evening (Pacific Time), I realized that I had a risk management problem. There was “no market” for my options. I had lowered the stop on my short futures position, but if the stop was hit, I would be net long the CAD (due to the short options) – with no way to cover them.

Sometime after midnight (as the European markets opened), bids and offers appeared in the CAD options – but the bid/offer spreads were WIDE and implied Vol had jumped – sharply increasing the prices of the options I was short. Mama Mia!

I covered all my CAD positions Tuesday and made a little money on the trade. By then, I had the idea that the panic that had caused the sharp sell-off on Monday had run its course, and I started buying Dow and S+P futures. I had my stops too tight and took small losses.

As much as I was right on my idea that the panic was over, I lost money buying the indices because the intra-day price swings were so much bigger and faster than they had been before the panic – and I couldn’t adjust how wide I needed to place my stops.

At the end of the week, my net P+L on realized trades was flat. I had come into the week bearish; the market had dropped, I had changed to bullish, the market had rallied, and, net, I didn’t make any money. Have I ever told you that trading is not a game of perfect? I ended the week flat.

On my radar

I think there has been a change in market psychology. As noted above, this week’s rally from Monday’s lows might have been reflexive. If the market rolls over and, especially if it takes out this week’s lows, I would be looking for opportunities to short stock indices, buy the USD, and I might even buy bonds!

Thoughts on trading

My trading time horizon got too short this week. My sweet spot is more of a swing trading time frame – a few days to a few weeks. I had experimented with shorter-term time frames where I would enter a market close to the point where I would stop myself out – using only price action to make trading decisions. (No supply/demand analysis etc.) I thought this would likely generate lots of small losses with occasional big wins. It probably works well for some people, but it doesn’t seem to suit me.

Finding the right time frame (that suits you) is one of the most important things for a trader. I don’t think all of my trading has to happen within the same time frame – the market doesn’t always move at the same speed – but I think there has to be a “pace” to my trading that allows for reflection – not just intuition.

I’ll wrap up this week’s Notes with a quote from Denise Shull’s recent interview on RTV. She runs the ReThink Group, providing performance coaching for traders and professional athletes. She said, “People think they make decisions based upon their analysis – but actually, they make decisions based upon how they “feel” about their analysis.”

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair