Gold & Precious Metals

Jan 17, 2017

- Rate hikes tend to be good for gold, and even better for gold stocks. On that note, please click here or on the above image now. Double-click to enlarge this hourly bars gold chart.

- Since Janet Yellen hiked rates in December, gold has rallied almost $90. That’s good news, but the great news is that the US central bank plans more rate hikes this year.

- Gold has a rough historical tendency to decline ahead of rate hikes, and rally strongly after they happen.

- Please click here now. Double-click to enlarge this daily bars gold chart.

- The 14,7,7 Stochastics oscillator is beginning to show signs of “flat lining” in the overbought position. That tends to happen during very strong rallies.

- Britain’s prime minister Theresa May is about to make a key speech on the Brexit. That could push gold into my next profit booking target zone at $1245.

- Both gold and gold stocks have been chewing through overhead resistance zones with ease this year, and $1245 is the next one. Gold price enthusiasts should be light sellers if gold goes near that $1245 target zone.

- Please click here now. Double-click to enlarge. The dollar continues to weaken against the safe-haven yen, with smart money bank traders long the yen, and short the dollar.

- Gold’s rally began when the dollar began falling against the yen in December.

- Please click here now. Donald Trump is good for gold in a number of ways.

- Uncertainty is one of them, but he’s also poised to ramp up infrastructure spending (inflationary).

- Also, for the past 50 years, gold sports a good track record of rising during US presidential transition years. 2017 is a transition year.

- Trump endorses a lower dollar and higher interest rates. If he’s able to do that, inflationary pressures would increase quite dramatically.

- Higher rates incentivize banks to make loans, and a lower dollar itself pushes gold higher.

- As good as gold looks now, gold stocks look even better. Please click here now. Influential analysts at Credit Suisse bank are very positive about gold stocks, regardless of whether gold rises or falls, but they see gold at $1300+ in 2017.

- Mining companies that have cut costs are well-prepared to handle lower gold prices, and they will have great profits at even slightly higher prices.

- Please click here now. Double-click to enlarge this fabulous GDX chart.

- GDX is breaking out of a drifting rectangle, and beginning to surge towards the $25 target zone. Gamblers can buy the breakout with a tight stop-loss order, targeting that $25 area.

- Longer term investors who bought in the $20 – $18.50 area can lighten up a bit in the $25 area too, if GDX makes it there.

- Please click here now. Double-click to enlarge.

- T-bonds are rallying nicely along with gold, and Ben Bernanke just added some “punch” to the price action, with his latest statement that the decline in the T-bond was likely a bit overdone.

- Please click here now. Double-click to enlarge this silver chart.

- Silver is moving higher in a “steady as she goes” manner. This type of price action is indicative of a rally that may be in the early stages, rather than near an end.

- For another look at the silver chart, please click here now. The $17.30 area is quite important. I think the Trump inauguration should be the catalyst that moves silver above $17.30, and ushers in the kind of “meat and potatoes” rally that most of the world’s silver bugs are waiting for!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Thanks!

Cheers

st

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am. The newsletter is attractively priced and the format is a unique numbered point form; giving clarity to each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualifed investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Several years ago, New York Times Wealth Matters columnist Paul Sullivan opened up his finances to a group of high-powered, high-net worth investors known as Tiger 21.

Several years ago, New York Times Wealth Matters columnist Paul Sullivan opened up his finances to a group of high-powered, high-net worth investors known as Tiger 21.

Members gather regularly to discuss investing strategies and at one meeting, Sullivan asked them to critique his own — relatively meager by their standards — financial life.

“Given what I do, I thought [my wife and I] had a handle on it, but what I learned from that meeting is that we hadn’t thought enough about the risks in life,” Sullivan says.

Those risks include declining incomes and the unexpected death or disability of a household wage earner. As a result of that meeting, Sullivan and his wife took out life and disability insurance policies and sold off a condo in Florida that had been a vacation home for the family.

“They were so direct and harsh about that being a possible drain, if we weren’t able to sell it if something bad happened. That was a wake-up call,” Sullivan says.

The lessons he absorbed from that wealthy, exclusive group of over 300 members across the U.S. and Canada led Sullivan to write his new book, “The Thin Green Line: The Money Secrets of the Super Wealthy.” The title refers to the security that can come from knowing you’re prepared for a negative event, like a layoff, no matter how much money you have or earn. “The people in the book who I call wealthy, whether they’re a teacher or a hedge fund manager, are wealthy because they have security. They have behaviors around money that let them be in control of their lives when something bad happens,” he says.

Those behaviors, Sullivan says, can be learned or even adopted later in life. As someone who grew up without much money, he says it took him a long time to have a healthy relationship with it. He would avoid credit card debt and overspending so assiduously that he often wore threadbare clothing and skipped even affordable purchases he would have enjoyed. “You should be able to spend money on things you enjoy. If you love $4 Starbucks lattes, then buy it,” he says.

If you’re looking to adopt some secrets of the wealthy, Sullivan suggests the following strategies:

…related:

Why do we do this? Because a small number of people will get through – and we want you to be one of them.

2017 World Outlook Financial Conference – Feb 3rd & 4th, 2017 at the Westin Bayshore Hotel in Vancouver

CLICK HERE to order your ticket

CAN’T ATTEND? CLICK HERE to get your online video subscription

Predicting, especially the future, is very difficult. Still, let’s try to figure out what investors should expect from the gold market next year. For sure, in the long run, the price of gold will mainly depend on the U.S. dollar, the real interest rates, and the market uncertainty. How will these factors develop and affect the gold market?

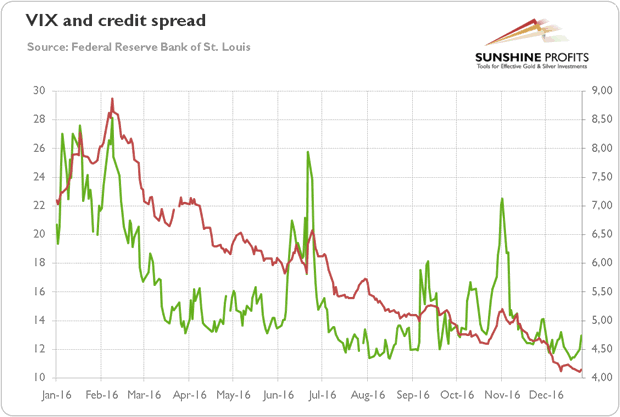

Well, as one can see in the chart below, the level of investors’ confidence has strengthened recently, as both the market volatility (represented by the CBOE Volatility Index) and credit spreads (illustrated by the BofA Merrill Lynch US High Yield Option-Adjusted Spread) have diminished after the U.S. presidential election. Hence, the risk aversion should be low for a while, and so the safe-haven demand for gold. Surely, if such risks as China’s hard landing, the banking crisis in the Eurozone or the turmoil in the U.S. bond markets materialize, gold may again shine as a safe-haven asset. However, investors should remember that gold failed to rally on negative news in 2016, while stock markets flourished.

Chart 1: The CBOE Volatility Index (green line, left axis) and BofA Merrill Lynch US High Yield Option-Adjusted Spread (red line, right axis) in 2016.

And what about the U.S. dollar and real interest rates? As the next chart shows, both indices have been rising since October, which corresponded to the plunge in gold prices.

Chart 2: The U.S. dollar index (green line, left scale, Trade Weighted Major U.S. Dollar Index) and the U.S. real interest rates (green line, left scale, yields on 5-year Treasury Inflation-Indexed Security) in 2016.

Will this trend continue in 2017? Well, it depends mainly on three things: 1) the expected pace of the Fed’s tightening; 2) divergence in the monetary policies among major central banks in the world; 3) the market sentiment toward the Trump’s policies. Let’s analyze them now.

The Fed’s hiking will be gradual, for sure. However, it would be difficult to be more gradual than in 2016, when the U.S. central bank managed to lift interest rates only once, exactly one year after the previous hike. With the labor market near the full employment and rising inflation and inflationary expectations, two or three hikes in 2017 are not impossible, unless we witness recession, of course. Therefore, the U.S. dollar and real interest rates may be under upward pressure next year, which would not support the price of gold.

The divergence in the Fed’ stance compared to the rest of world should also strengthen the U.S. currency and real interest rates. The American economy will grow faster than other developed economies which would translate into more hawkish monetary policy. Just as a reminder, the ECB just extended its monthly asset purchase program by nine months and relaxed its rules, while the FOMC members revised its projections for the federal funds rate in 2017. Given the fact that the interest rates are not going up in the Eurozone any time soon and a whole bunch of economic problems the Europe faces, including the upcoming important elections in several countries, we believe that the U.S. dollar will strengthen against the Euro in 2017. The same applies also to the USD/JPY exchange rate, especially given the yield curve management introduced by the Bank of Japan in September 2016. As the BoJ tries to maintain the Japanese 10-year rate around zero percent, the spread between U.S. and Japanese real interest rates should widened further, which would strengthen the greenback and soften the price of gold.

The market sentiment toward gold will be shaped also by the expected effects of the new administration’s policies. Donald Trump will take office on January 20, 2017 and we will probably see important changes from the very beginning of the presidency. Investors now await the “great rotation” out of bonds and into stocks, as the heavy government spending and higher fiscal deficits under the new president are believed to lead to higher bond yields. If Trump fulfills such hopes, the price of gold will take a hit. On the other hand, if the “Trump rally” turns out to be only a mirage, there will be a relief in the gold market.

Summing up, the major fundamental forces affecting the gold market in 2017, they will be the strength of the U.S. dollar, the dynamics of the real interest rates and the level of fear in the markets. The political and market uncertainty diminished after China’s turmoil, the Brexit vote and the U.S. presidential election. The world is full of risks, but the sad fact for the gold market is that financial markets showed great resilience to them in 2016, shrugging of practically all bad news, or even rising on them. Therefore, although investors should not downplay the potential threats to the global economy, they should focus on the relationship between gold and the greenback with real interest rates instead of the safe-haven appeal of the yellow metal. We believe that the fundamental outlook for the gold market is rather bearish in the near future, until markets lose their faith in the pro-growth policies of Trump or financial turmoil will force the Fed to adopt a more dovish stance.

Thank you.

If you enjoyed the above analysis and would you like to know more about the most important factors influencing the price of gold, we invite you to read the January Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It’s free and you can unsubscribe anytime.

“The problem with police officers and firefighters isn’t a public-sector problem; it isn’t a problem with government; it’s a problem with the entire society. It’s what happened on Wall Street in the run-up to the subprime crisis. It’s a problem of people taking what they can, just because they can, without regard to the larger social consequences. It’s not just a coincidence that the debts of cities and states spun out of control at the same time as the debts of individual Americans. Alone in a dark room with a pile of money, Americans knew exactly what they wanted to do, from the top of the society to the bottom. They’d been conditioned to grab as much as they could, without thinking about the long-term consequences.”

― Michael Lewis, Boomerang: Travels in the New Third World

Though it may not be instantly clear, in the above quote Michael Lewis is talking about public sector pensions and how over the course of several decades, mayors and governors across the US have colluded with police, firefighter and teachers unions to promise outrageously-generous benefits and then failed to put aside enough money to pay for them.

As a consequence two things are happening. In dozens if not hundreds of cities and towns, services are being cut to the bone to pay for ballooning pension benefits, and – when even these cuts prove inadequate – pensions are being drastically reduced.

Which in turn means two other things. First, life isn’t nearly as easy or pleasant as it used to be in a lot of places, as library hours are cut, trash piles up and police response times lengthen. And second, hundreds of thousands of public sector workers who expected to retire comfortably are staring at major lifestyle shrinkage.

To which a reasonable person might yawn and say, sure the numbers look grim. But they’ve looked that way for a long time and outside of Chicago, American life is still pretty good by Greek, Venezuelan or Russian standards. So go away until something tangible actually happens.

Point taken. But this might be that time. Beginning with Dallas, where the city is actually taking money back from plan recipients…

Dallas Police and Fire pension members may have to pay back funds

The city has agreed to put in an additional billion dollars over 30 years, but they’re proposing a series of bitter pills to make up the rest of the nearly $4 billion shortfall.

The bitterest pill: A proposal to take back all of the interest police and firefighters earned on Deferred Option Retirement accounts, or DROP. That would amount to an additional billion dollars saved. The city is calling it an “equity adjustment.” Retirees call it an illegal “claw back.”

The city is also seeking to “equity adjustment” on cost of living increases. The city says that pension checks are about 20 percent higher than they would have been if increases had been tied to inflation.

The city’s proposing to freeze cost of living increases until it catches up to the inflation index.

…and moving on to Kentucky, where if a funding level of 16% for the state employees fund isn’t an imminent crisis, then nothing is:

Things are if anything even bleaker in the private sector:

Multiemployer Pension Plans In Crisis: Troubled Plans Need Public Resources To Survive

(Forbes) – There is an emerging financial crisis among multiemployer pension plans in America. These plans are a subset of private sector defined benefit pensions covering 10 million workers and retirees. Most critical are the projected bankruptcies of the Teamsters Central States and the United Mineworkers of America plans, making front page news for the last several months.

Multiemployer plans are insured by the US Federal Government’s Pension Benefit Guaranty Corporation (PBGC). But PBGC is itself in danger of going broke. Set up in 1974 to “encourage the continuation and maintenance of voluntary private defined benefit pension plans [and] provide timely and uninterrupted payment of pension benefits,” the plan uses the ultimate backstop to provide those guarantees: the U.S. taxpayer.

In the fiscal year 2015, PBGC paid out nearly $6 billion in benefits to participants of failed pension plans, increasing the agency’s deficit to $76 billion. The PBGC now has $164 billion in obligations and just $88 billion in assets.

When this was reported to Congress, it passed the Kline-Miller Multiemployer Pension Reform Act of 2014, allowing pension plans to ask permission to cut benefits to its plan participants. Prior to 2014 those plans weren’t allowed to do so. But actuaries looking into the PBGC reported that unless something was done, the PBFC itself would be broke in less than a decade.

The door is now open for other pension plans facing similar shortfalls to apply for permission to cut benefits to their participants. The ripple effect could be enormous: PBGC is the ultimate backstop for some 22,000 single-employer pension plans and another 1,400 multi-employer pension plans covering 40 million participants.

Some other relevant headlines:

CalPERS Cuts Pension Benefits For First Time

Ohio workers face precedent-setting pension and retiree health cuts

Teamsters’ Pension Plans Seek Massive Cuts to Retirees to Stay Solvent

Chicago’s massive unfunded pension deficit could swallow the city

And this, remember, is happening at the tail end of a 30-year bull market in bonds and a 7-year bull market in stocks, which took the main asset classes held by pension funds to record valuation levels. So the rubber truly meets the road during the next recession when stocks will, if history is a reliable guide, drop by 20% or more. The current gaps in thousands of pension funds will become gaping holes, and the experience of Teamsters and Dallas cops will be replicated across the country.

Click here for the previous posts in this series

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair