Wealth Building Strategies

– Dallas has blocked withdrawals from the police and firefighters pension fund.

– Dallas has blocked withdrawals from the police and firefighters pension fund.

– The Italian government is scrambling to prevent the world’s oldest bank – Monte Paschi – from going down.

– 446,000 people in the States joined the ranks of the permanently unemployed in November alone pushing the total number to an all time high 95.1 million.

– Meanwhile global stocks markets have added over $1 trillion dollars since Donald Trump’s election.

– Gold is off $250 since the post Brexit highs.

That’s not much of a way to say Merry Christmas, is it? But it’s a very good reminder as to how much things are changing. Of course we’ve been getting that message every day, week and month since the spring of 2008 when Bear Sterns went under.

Still, that collapse of an 85 year old Wall Street mainstay still wasn’t enough to wake up investors, regulators, financial institutions or politicians. So 5 months later the subprime mortgage crisis hit and the world hasn’t been the same since.

The question is – what aren’t we paying attention to today that will shake the financial world?

Is it the end of the 35 year decline in interest rates and the subsequent trillion dollar losses in the bond market since July? Maybe it’s the success of the 5-Star Movement in Italy, who want to stop using the euro and return to the lira.

It could be the escalating problems in the emerging market countries, led by the collapse of Venezuela, who are all in big trouble because they borrowed money denominated in US dollars and now their economies are tanking while the dollar goes up. As Canadian comedian Russell Peters says – “somebody’s gonna get hurt real bad.” Top of the list will be the people, banks and governments who lent them the money.

Maybe its Amazon’s new no check-out, no cashiers test store in Seattle, which reminds us of the job threat of technological substitution. My guess is that our political class is so clueless that they’ll be sitting in a self driving taxi on their way to an ATM machine in order to put money on their credit card to buy something online that will be delivered by drone – and still scratching their heads wondering if technological substitution is a problem.

The First Thing To Understand

We are living through the most intense rate of change in history – and that spells both danger and opportunity. Danger – as in the fall in gold from over $1900 US to the $1150 range or the drop in the euro from $1.60 to $1.06 or the loonie’s decline from over to par to the 68 cent low. There are no shortage of examples of the cost of missing the changes.

But it works both ways. (Warning: this is the promotion part) If you had taken the advice at the World Outlook Financial Conference (Jan 2013) / Moneytalks (Oct 2012) and bought US dollars you’d be up over 30% even if you put it under the mattress. Better still, if you bought our recommended quality US dividend paying stocks (starting Mar 2009 and ever since) or real estate in the Phoenix area (World Outlook 2012) you’d be up triple digits.

People ask me all the time how can I protect myself – well that’s my answer.

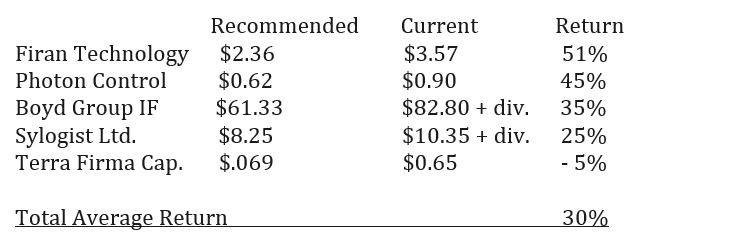

But it’s not just in the US. Look at the results of all the recommendations of the 2016 World Outlook Small Cap Portfolio (as of last week).

Of course past performance is not a guarantee of future results, but thanks to the research of Ryan Irvine and Keystone Financial, the World Outlook Small Cap portfolio has earned double digit returns every year since we first introduced it in 2009.

And I have to admit that I love when the recommendations pay for the price of a ticket many times over. And last year was no exception. John Johnson called the fall in the loonie from over 80 to under 70. Mark Liebovit called silver’s move from under $14 to $20. Josef Schachter oil stock recommendations were up over an average of 100%.

Of course I chose the keynote speakers for their track record so while it’s impressive, the great results are not a surprise.

Here’s the Problem For Some People

I looked at the Friday, February 3rd television schedule – you’d be missing Undercover Boss and Hollywood Game Night, and Saturday has the much anticipated recap of The Bachelorette. That’s tough to compete with, even with some of the top market analysts in the English-speaking world, including Martin Armstrong, subject of a critically acclaimed documentary and an upcoming Hollywood film. But then again we all have to make sacrifices to secure our financial future.

The bottom line is that we take your time and money seriously. With that in mind we have put together our best conference ever in the hope of making you a significant amount of money and just as importantly protecting you financially.

Sincerely,

Michael Campbell,

Host of Money Talks

2017 World Outlook Financial Conference Details

Where: Westin Bayshore, Vancouver BC

When: Friday afternoon and evening, February 3 and all day Saturday, February 4, 2017

For more information including speakers and the agenda: CLICK HERE

To reserve your seats: CLICK HERE

The optimism that has followed the election of Donald Trump has pushed the Dow Jones Industrial Average to the threshold of 20,000, a level that will be both a nominal record and a symbolic milestone. Although this is not the way most observers had predicted that 2016 would play out, most on Wall Street have become extremely reluctant to look a gift horse in the mouth…or to even look at him at all. The impulse is to jump on and ride, and only ask questions if it pulls up lame. But if this year has proven one thing, it is that predictions made by the consensus should not be trusted.

The optimism that has followed the election of Donald Trump has pushed the Dow Jones Industrial Average to the threshold of 20,000, a level that will be both a nominal record and a symbolic milestone. Although this is not the way most observers had predicted that 2016 would play out, most on Wall Street have become extremely reluctant to look a gift horse in the mouth…or to even look at him at all. The impulse is to jump on and ride, and only ask questions if it pulls up lame. But if this year has proven one thing, it is that predictions made by the consensus should not be trusted.

Back in the earlier part of 2016 the mood was decidedly darker. At that point most people believed that the Federal Reserve would be raising rates throughout the course of the year. While such hikes had been anticipated (and delayed) for years, most took comfort in the belief that the economy would be expanding nicely by the time the Fed actually pulled the trigger. But in late 2015, the already tepid GDP growth seen in the prior two years seemed to be decelerating. Investors also concluded that Hilary Clinton was a lock to win the election, thereby assuring that the anti-growth policies of the Obama years would continue. Many looked at these developments and concluded that the sins of the past decade, in which the Government and the Federal Reserve had used unprecedented levels of fiscal and monetary stimulus to prop up the economy and the stock market, had finally caught up with us. As a result, the Dow Jones shed more than seven per cent in the first two weeks of the year, its worst start on record.

But the year comes to an end amid a cloud of Trump-fueled bullishness. The markets fully embrace an unapologetic capitalist, and his team of billionaires, who promises to cut taxes, rewrite trade deals in America’s favor, take a machete to anti-growth regulations, repeal Obamacare, and return America to its former industrial might. Many are making parallels to the Reagan Revolution in which a maverick anti-establishment Republican took charge in Washington and ignited an economic boom, a stock market rally and a surge in the dollar. But to make this comparison, boosters must jump over a more telling comparison to the last Republican president elected, George W. Bush.

The parallels to W. are striking. Both lost the popular vote, and will have taken office following the tenure of a two-term Democrat who had presided over a furious stock market bubble and a surging dollar. In the 4 years prior to Bush’s election, the Dow Jones had surged approximately 60% and the dollar index had risen approximately 19% (1/2/97 to 12/29/2000). For Trump, the numbers are 48% and 24% (1/2/13 to 12/21/16). Then, as now, the U.S. was seen by investors as the only game in town. Clinton’s second term was rife with global crises that both created safe-haven flows into the dollar and caused the Fed to backstop U.S. financial markets with cheap money (at least cheap by the standard that existed at the time). Both will have come into office promising tax cuts and regulatory relief following eight years of Democratic reign. As a result, the market gains of the Clinton and Obama years were expected to continue under their Republican successors.

But the optimists did not anticipate that the big, fat, ugly bubble that inflated during Clinton’s second term, would burst early in Bush’s first term (although the air started coming out of that bubble while Clinton was still in office). Given the ensuing recession of 2001, it can be argued that the only reason Bush was reelected in 2004 was that the Fed was able to inflate an even bigger, fatter, and uglier bubble in housing that postponed the pain until the financial crisis of 2008. That is where the similarities will likely end, as Trump will likely not be that lucky.

One of the pillars of dollar strength under Clinton was eight straight years of deficit reductions, culminating with a massive $236 billion budget surplus in 2000 (Congressional Budget Office). While the surplus did require some accounting smoke and mirrors and a stock market bubble to create, it nonetheless marked a significant achievement. At that point, many economists had assumed that the U.S. debt problem had largely been solved and that the country would ride a wave of permanent surplus. The only problem most could envision was a shortage of Treasury bonds once the national debt was fully repaid. No one is to worried about that “problem” now.

Similarly, Trump is taking charge at a time when official budget deficits have fallen consistently since 2009 (albeit from astronomically high levels). But 2016 is projected to be the first year since 2009 in which the deficit will have risen, significantly, from the prior year. The Congressional Budget Office sees a return to perpetual $1 trillion plus annual deficits in the early part of the next decade (The Budget and Economic Outlook: 2016 to 2026 report, January 2016), even if we have no tax cuts, spending increases or recessions over that entire time. Under the Trump presidency, we are likely to get all three.

If a recession comes early in Trump’s presidency, it will be no more his fault than the 2001 recession can be blamed on Bush. A sharp pullback has been years in the making. Firstly, there is simply the issue of timing. On average, the U.S. has experienced a recession every 60 months or so since WW II (based on data from National Bureau of Economic Research and Bureau of Labor Statistics).The current expansion is already 90 months old, or 50% longer than average. Sooner, rather than later, it will have an end date. Recessions completely reshuffle the budgetary deck, causing government outlays to rise and revenues to fall simultaneously. The swings can be dramatic. The 1981-1982 recession resulted in a 61% increase in Federal red ink. The recession of 2001 turned a $236 billion surplus in 2000 into a $377 billion deficit in 2003 (then a record). The Great Recession of 2008-2009 caused the $458 billion deficit in 2008 to more than triple to $1.4 trillion in 2009. Rest assured, the next recession can cause a similar catastrophe to the government’s finances.

Trump’s election was predicated on his intention to buck traditional Republican policy of fiscal restraint. He has promised tax cuts for people and corporations and massive $1 trillion plus spending binges on infrastructure and the military. Of course the argument goes that these moves will stimulate growth thereby raising tax revenue to pay for both the cuts and the spending. The same arguments were made by George W. Bush in 2001 when he cut taxes, increased spending, and pushed through a temporary tax holiday to encourage corporations to repatriate money held overseas. Deficits soared anyway. The only real question is will the recession arrive before or after Trump’s fiscal policies kick in. If the events happen simultaneously, the budgetary implications will be hard to fathom.

Investors who are basking in the Trump victory should take a hard look at what happened to the markets during the Bush presidency. In mid-2008 (just a few months before the financial crisis sent stocks plummeting), the S&P 500 was just 17% above the level when Bush was elected nearly eight years earlier. The dollar, in particular, took a beating under Bush. In August 2008 (right before the dollar rallied temporarily as a result of the panic), the dollar index had fallen by 19% since his election. The opposite occurred in gold. In November of 2000, gold was at about $370 per ounce, close to a 20 plus year low. In August 2008, it was more than $920, down significantly from it’s high of almost $1,100 hit earlier that year.

Also, for all the optimism about the U.S. stock market and pessimism abroad, it was foreign markets that delivered for investors. From Bush’s election to mid-2008, just before the global financial crisis sent stocks reeling around the globe, developed foreign markets were up 80% (priced in U.S. dollars) while emerging markets were up a staggering 300% (priced in U.S. dollars). Even if you include the huge losses in the back half of 2008, by the time Obama was sworn in, developed markets were down less than 3% from the time of Bush’s election, and emerging markets were still up about 80%. (In contrast, the S&P 500 was down almost 27%).

The 2001 Recession, which was triggered by the bursting of the dotcom bubble and the September 11 attacks, came very early in Bush’s first term. Fortunately for W., the Federal Reserve was able to support the economy by bringing rates down from more than 6% to just 1% (Federal Reserve Bank of St. Louis) (which helps explain the swift collapse of the dollar). As a result, the 2001 recession was the shortest and mildest on record. In doing so, however, the Fed blew up an even bigger bubble in real estate, the bursting of which created a far bigger recession in 2008, propelling Obama into the White House.

But can the Fed ride to the rescue this time around? Given that rates are practically zero and the Fed is choking on trillions of dollars of assets that are permanently held on its balance sheet, the answer is clearly no. All the Fed will be able to do is launch the mother of all QE programs, perhaps in the form of a massive helicopter drop. But the bad news for Trump fans is that the result will not be a housing bubble like the one that bailed out Bush, but a wave of stagflation that will make Trump a one-termer. The nightmare scenario is that once again tax cuts and deregulation take the blame, allowing Bernie Sanders or a socialist candidate to ride another populist wave, only this one headed far left, into the White House of 2020.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube.

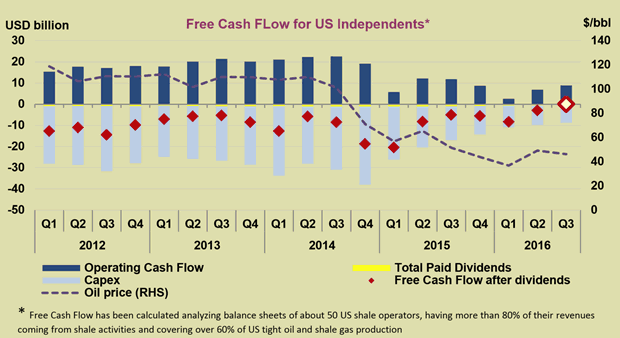

Oil prices are probably already high enough to spark a rebound in shale production.

The IEA says that in the third quarter of 2016, the U.S. shale industry became cash flow neutral for the first time ever. That isn’t a typo. For years, the drilling boom was done with a lot of debt, and the revenues earned from steadily higher levels of output were not enough to cover the cost of drilling, even when oil prices traded above $100 per barrel in the go-go drilling days between 2011 and 2014. Even when U.S. oil production hit a peak at 9.7 million barrels per day in the second quarter of 2015, the industry did not break even. Indeed, shale companies were coming off of one of their worst quarters in terms of cash flow in recent history.

That all changed around the middle of 2015 when the most indebted and high-cost producers went out of business and consolidation began to take hold. E&P companies began cutting costs, laying off workers, squeezing their suppliers and deferring projects that no longer made sense.

By 2016, oil companies large and small had shed a lot of that extra fat, running leaner than at any point in the last few years. By the third quarter, oil prices had climbed back to above $40 and traded at around $50 per barrel for some time, replenishing some lost revenue. That was enough to make the industry cash flow neutral for the first time in its history.

That suggests that moving forward, the shale industry could move into cash flow positive territory. Oil prices seem to be trading safely above $50 per barrel for the time being, and OPEC cuts could induce more price gains. The industry is now focusing on shale plays that have lower breakeven prices, namely, the Permian Basin and some parts of the Bakken. That has companies like Concho Resources, Murphy Oil, Devon Energy, Pioneer Natural Resources and EOG Resources all stepping up their spending levels heading into 2017.

Wood Mackenzie suggests that $55 per barrel is a sweet spot for the oil and gas industry to rebound, a level that is only slightly above today’s prices. At $55 per barrel, the shale industry is cash flow positive and will grow accordingly. “If we stay (at $55 a barrel), the world’s biggest oil companies start to make money again. If we go back down to $50 (or lower) in 2017…then those companies are in the negative territory and they go back into survival mode where they have been in the last two years,” Angus Rodger, WoodMac’s research director for upstream oil and gas, said in a report. He estimates that OPEC’s cuts could succeed in pushing oil prices sustainably up to $55 per barrel. Even taking into account some cheating, WoodMac concludes that a 75 percent compliance rate with the promised cuts would get the markets to that price level.

Still, the seeds of disappoint have already been sown – it is just a question of whether or not they will sprout. The U.S. dollar is at its strongest level in nearly a decade, which will weigh on global crude oil demand. Also, hedge funds and other money managers have staked out the most bullish positionon oil futures in more than two years. That has succeeded in running up prices this month, but it also sets up the market for downside risk. Should data emerge in the coming months that some OPEC members are cheating, the net-long positions could unwind. Those liquidations tend to happen quickly, so a sharp fall in oil prices is not out of the question.

“If confidence around the compliance with cuts wavers, the market will necessarily correct lower, considering that it also faces the twin headwinds of resilient U.S. production and a stronger dollar environment as the Fed begins to hike rates,” Harry Tchilinguirian, an analyst with BNP Paribas, told S&P Global Platts.

And while the financial markets present risk, the physical market is also up in the air. Of course, OPEC cheating is a possibility. But with U.S. shale producers already stepping up drilling, production could come back quicker than many expect. Weekly EIA data shows gains of nearly 300,000 bpd since the end of summer. On top of that, disrupted output from Libya and Nigeria – two countries not subjected to the OPEC cuts – could begin to come back. An oil tanker docked at Libya’s largest oil export terminal, Es Sider, this week, was the first tanker to load up Libyan oil from that terminal in more than two years. Libya hopes to add another 300,000 bpd in output in 2017 after adding as much in 2016.

Even with those negative risks in mind, the shale industry is getting back to work. If oil prices can stay roughly where they are right now, the industry could become cash flow positive for the first time ever next year.

Link to original article: http://oilprice.com/Energy/Energy-General/US-Shale-Is-Now-Cash-Flow-Neutral.html

By Nick Cunningham of Oilprice.com

Beware of all enterprises that require a new set of clothes.

Henry David Thoreau

Remember over a year ago when they first raised hikes-they huffed and puffed warning everyone that they would raise rates several times in 2016 and viola nothing happened until now. Now they are repeating the same thing all over again. To illustrate how bad this economy take into consideration that the Fed has raised rates only twice in the last decade; the economy was a lot stronger in 2006 and 2007 than it is today. Yellen’s statement below illustrates how the Fed is positioning itself so that it can pull another “oops we were wrong once again” moment.

Remember over a year ago when they first raised hikes-they huffed and puffed warning everyone that they would raise rates several times in 2016 and viola nothing happened until now. Now they are repeating the same thing all over again. To illustrate how bad this economy take into consideration that the Fed has raised rates only twice in the last decade; the economy was a lot stronger in 2006 and 2007 than it is today. Yellen’s statement below illustrates how the Fed is positioning itself so that it can pull another “oops we were wrong once again” moment.

“All the (Federal Open Market Committee) participants recognize that there is considerable uncertainty about how economic policies may change and what effect they may have on the economy,” Yellen said

Has anything changed since the last hike; is the economy stronger? The only thing that is getting stronger is the illusion that this economy is on the mend. If the economy was improving, then a rising rate environment could be seen through a bullish lens. In this instance, this economic recovery is a joke; it is all an illusion that is funded by debt. If the supply of hot money is cut, the markets will tank. The real estate sector is not stable yet, and most people already can’t afford a house, so raising rates is a recipe for disaster. Our take is that the Fed has raised rates to give them more room to manoeuvre while making it appear that they are loath to embrace negative rates. The Fed has to play a delicate balancing game; the US dollar has to look attractive to the world, as that is what gives the Fed the power to create unlimited money. The US dollar is the World’s reserve currency. If it were not, then the US would have followed Greece’s path long ago. It is our ability to rob the world by creating money out of thin air at other nation’s expense that gives the US capacity to hold onto the top dog position precariously. It is precarious because it is just a matter of time before China displaces the US. On a purchasing power parity basis, China has already replaced the US as the World’s largest economy. One day the world will realise that the emperor is naked, fat, old and ugly as sin. However, as there is still some time before this comes into play, we are not going to address this issue.

We believe that the Fed will have no option but to eventually embrace negative rates unless they are looking to trigger a crash. The Fed is famous for artificially creating every boom and bust cycle since the US went off the Gold standard. While it might appear that we are in a bubble like phase as far as the stock market is concerned, one needs to remember that the masses have not benefitted much from the current rally. History illustrates that the Fed usually pops the bubble after the masses have fully embraced the market. Additionally, the masses are not euphoric; however, they are turning more bullish, which suggests as we alluded in this article Stock Market Bulls-Stock Market fools-Market Crash next or is this just an Illusion, that it would not surprise us if the markets experienced a decent correction next year. In the interim, we think the Fed’s current move is just a trick to make it appear to the world that our economy is healthy. Now the Fed can lower rates twice before they move to zero, but it will force the rest of the world to lower their rates even more; effectively still making the US dollar the most attractive currency.

The bond market which many have given up for dead are looking for an excuse to rally sharply. We will look at this in more detail in a follow-up article. However, if you look at the long-term chart below, it is easy to spot that bonds have not crashed. They were pushed to extreme levels as individuals continued to embrace bonds for years despite the miserable returns they offered due to the safety factor. The masses, in general, were sceptical of this bull market and bought the hype that it was going to fall apart tomorrow for the past nine years. After Trump won money started moving out of bonds and into the market. What we have is a simple rotation; money is moving from one market into another. Now bonds are extremely oversold, and the markets are trading close to the extremely overbought ranges. When the markets start to pullback money will flow into bonds pushing rates lower. At that point, one will be able to tell if the rally in bonds is just a dead cats bounce or if the bull is ready to run again.

This is a weekly chart containing five years worth of data (each bar represents one week’s worth of data); it is easy to spot that Bond market is extremely oversold. Trump’s win has created a lot of enthusiasm, and a large number of individuals who were sitting on the sidelines moved out of bonds and into the market. As the move has been incredibly powerful, it is likely that bonds could experience a counter move that is equally strong.

For the first in time in roughly 24 months, bullish sentiment has soared to the 50% mark twice over a period of 6 weeks. Up until now, the masses were constantly negative, even though the markets continued to trend higher. Things are different right now; while the sentiment is not in the Euphoric, the percentage change is quite significant and signifies that some bloodletting is in order. Bond are attempting to find support in the 148.00 ranges; a weekly close below this level should result in a test of the 142.00-144.00 ranges, with a possible overshoot to the 140 ranges. The downside risk for bonds now is limited.

The markets have been resilient to sharp corrections for quite some time; a correction would be healthy for this market. It would scare the masses and sentiment would turn negative again, setting the bedrock for the markets to rally higher.

Conclusion

The illusion that the economy is doing well is supported because of the vibrant stock market. The stock market appears healthy because hot money is driving it. If the supply of hot money is cut, the markets tank and the illusion that all is well will come to screeching halt. If this economy were healthy, the Fed would have raised interest rates several times over the past ten years and not just twice. Moreover, Yellen’s statement that we posted at the onset of this article clearly indicates she is hedging her bets.

In the interim bullish sentiment has surged significantly on a percentage basis, and Bonds are trading in the extremely oversold ranges. The ingredients are in place for a decent correction. Don’t confuse the subsequent correction for a crash; the naysayers will do their best to have you believe that the world is going to end. We base our analysis on our Mass Sentiment indicators and the Trend indicator. When the trend turns negative, we will stop viewing substantial pullbacks as buying opportunities.

He that’s secure is not safe.

Benjamin Franklin

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair