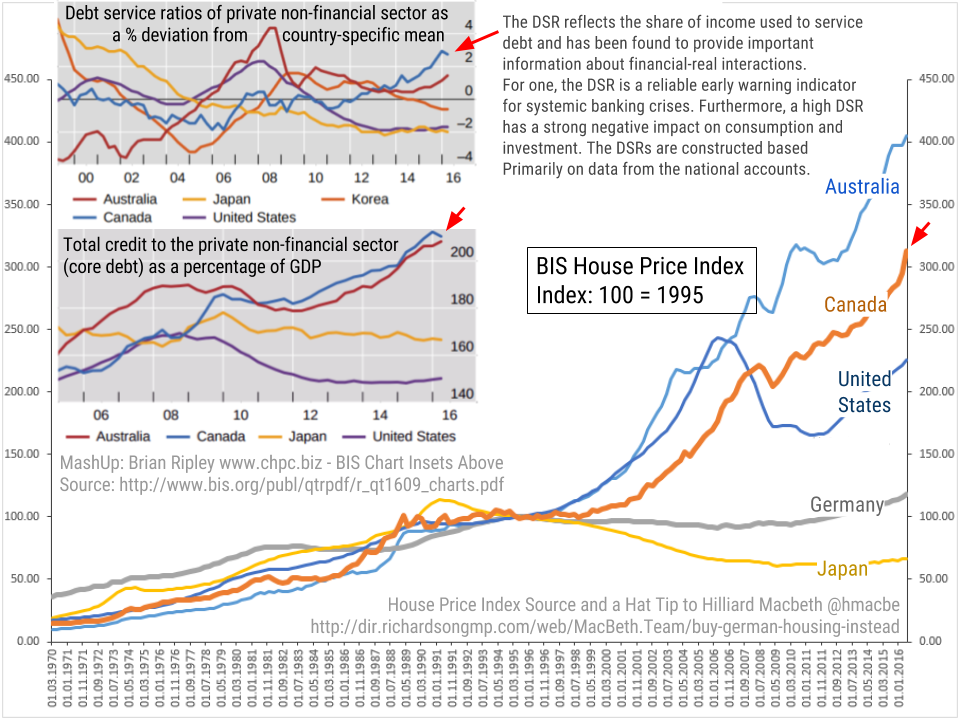

Real Estate

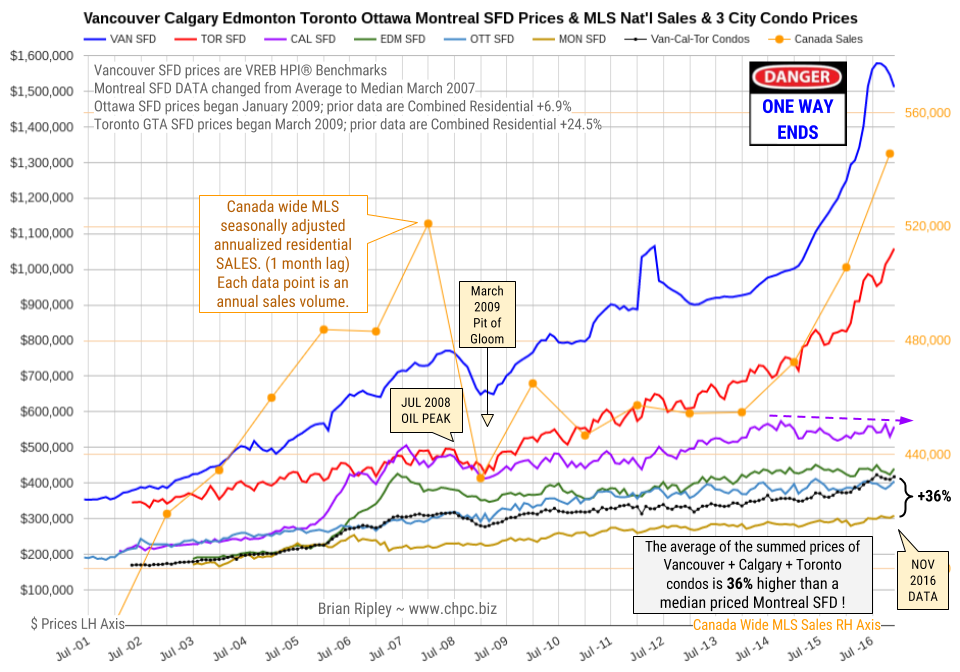

CANADA’s 6 BIGGEST METROS Vancouver, Calgary, Edmonton, Toronto, Ottawa and Montréal Single Family Detached Housing as well as the National MLS Residential Annualized Sales and the Average Price of Vancouver, Calgary and Toronto Condos. Rental Offerings via Craigslist, Kijiji, and Airbnb Chart…..BELOW

…also: Affordability or Bust

The world doesn’t realize it yet, but the implosion of the global markets has started and can’t be stopped. While the financial networks continue to focus on the rising U.S. stock market and Dollar, this represents a mindset that has totally gone insane.

The world doesn’t realize it yet, but the implosion of the global markets has started and can’t be stopped. While the financial networks continue to focus on the rising U.S. stock market and Dollar, this represents a mindset that has totally gone insane.

Why? Because the rapidly increasing Dollar and broader U.S. stock market do not represent a healthy economy, rather it reveals the swelling of the cancerous U.S. financial tumor. The faster and larger it grows, the more it will endanger the U.S. economy.

I am completely surprised by the lack of wisdom in the Mainstream and Alternative media analyst community. While many Mainstream analysts are probably paid to put out positive financial or economic propaganda, a good portion of the alternative media has no clue about the key factor that is driving the world straight over the cliff.

Furthermore, many precious metals investors are throwing in the towel and getting into the greatest overvalued stock market frenzy in history.

….also from Martin Armstrong:

The chart for Institutional Buying and Selling activity for last Friday’s close is now posted. If you look at the chart you will see that Institutional Buying had a an up tick and Institutional Selling showing an up tick.

Note the vacillation going on with the up and down Accumulation and Distribution movement.

While Institutional Investors were in Accumulation they were also selling, so be cautious.

also current market sentiment:

China’s economy and markets have been defying the laws of economics since 2009. Amid a worldwide financial crisis during that year, they managed to grow their economy by 8.7%. But that growth was fueled by a $586 billion dollar government stimulus package, which was followed by an additional $20 trillion dollars in new construction spending over the next seven years.

China’s economy became the envy of the world as the economy expanded through the edict of government to build massive cities that were mostly vacant. In fact, estimates are that 52 million homes in China are currently vacant and 90% of those empty units were purchased for investment purposes.

As investors sat on empty real estate, debt levels in the shadow banking system rose to troubling levels. A real estate bubble of this magnitude would bring most economies to the brink of destruction. But fear not; the megalomaniacs in Beijing had a solution: in 2015 they created a new bubble in the stock market to offset the fragile real estate bubble.

And to accomplish this, 40 online brokerage lenders helped arrange more than 7 billion yuan worth of loans for stock purchases.

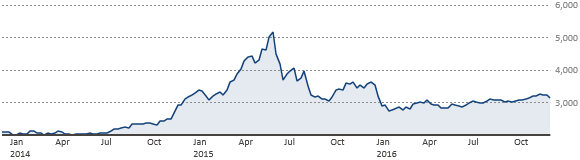

As you can imagine, China’s leverage problem quickly reached epic proportions. Fueled by margin debt the Shanghai Composite (SSE) started 2015 at 3,234 and hit 5,023 by June 4th; a 150% surge from the preceding 12 months, before plunging.

Shanghai Index:

With markets in free-fall, the totalitarian regime made daily policy modifications in a desperate attempt to stop the bleeding. Surprise interest rate cuts by the central bank, relaxations in margin trading and other “stability measures” did little to calm investors’ angst. But eventually, the central planners stepped in and stemmed the market’s decline.

However, the nation was far from out of the woods. Once a model of fiscal prudence, China became a country swimming in debt and asset bubbles. China’s corporate debt levels are now over 150% of its GDP, and estimates of total debt are as high as 280% of GDP.

Consumer credit has grown by over 300% in just the past six years. In October of 2015, debt levels for consumers hit 23.5 trillion yuan ($3.41 trillion). The expectations are that this will more than double by the end of 2020, reaching nearly 53 trillion yuan ($7.66 trillion).

The nation has now reached a 10-year high in delinquent corporate loans. Bloomberg reports that China has had nearly three times the number of defaults recorded in 2015.

Even the International Monetary Fund (IMF) is beginning to wave the warning flag that failing to act quickly to rein in corporate debt could prove detrimental to both China’s economy and the world as a whole.

Of course, supporting the rotating carousel of real estate, commodity, and stock bubbles, while also trying to stem bond defaults, comes at a cost. All of that debt and money creation usually results in a decimated currency. However, China uses its currency reserves (held mostly in dollar denominated Treasuries) to keep the value of the yuan from falling too quickly. But what had once been China’s get out of financial crisis free card–their immense foreign exchange reserves–is dwindling at an alarming rate.

November’s severe drop in reserves marked the fifth straight month of declines and are at the lowest level since March 2011. In fact, Japan just superseded China as the largest holder of U.S. sovereign debt.

IMF guidelines put $2.8 trillion as the minimum prudent level for China to hold in reserves–it is closing in on that level at the current pace. The yuan fell to an 8-1/2-year low in November and has dropped 6% against the dollar so far this year despite the government’s efforts.

Adding to pressure on the yuan is the newly elected U.S. president, Donald Trump, who has threatened to label China as a currency manipulator on his first day in office and impose huge tariffs on imports of Chinese goods. Pushing even further down on the yuan are the threatened three Fed rate hikes scheduled for 2017.

In January, Chinese citizens will get an even lower quote from Beijing for exchanging their local currency into foreign dollars. Yes, China’s government even tries to dictate the exact value of its currency. Many believe this will create a repeat of the market chaos that ensued at the start of 2016, as capital outflows surge.

Scotiabank Vice President of Economics, Derek Holt, believes these fears are warranted. He said in a recent article: “Why wouldn’t they convert like there is no tomorrow?” … “After another year of yuan depreciation, would you keep your life savings in a currency that is losing international purchasing power and within a banking and shadow finance system that gets all manner of negative headlines?”

Therein lies China’s dilemma: Allow the yuan to intractably fall, which will increase capital flight and destroy its asset-bubble economy. Or, raise interest rates to stabilize the currency and risk collapsing asset bubbles that will crumble under the weight of rising debt carrying costs.

China embodies a Keynesian dystopia that results from central planning gone mad. It’s mirage of prosperity should soon be coming to an unpleasant end. The misguided belief any government can print unlimited amounts of money and issue a massive amount of new credit; while providing the conditions that are the antitheses necessary for viable growth, has one significant Achilles heel: eventually, it will destroy your currency. Currency is always the pressure valve that explodes in an economy that has reached the apogee of dysfunction. The Red nation isn’t the only offender on this front, but is certainly one of the worst. Therefore, China and the yuan may have finally run out of time.

….also Live From The Trading Desk with Michael Campbell & Victor Adair: US Dollar Powers To a 14Yr High

It’s the same story every time: Imbalances build up during a recovery but most investors ignore them because good times have become the new normal and the uptrend seems bullet-proof. Then things fall apart and everyone wishes they’d paid attention to history.

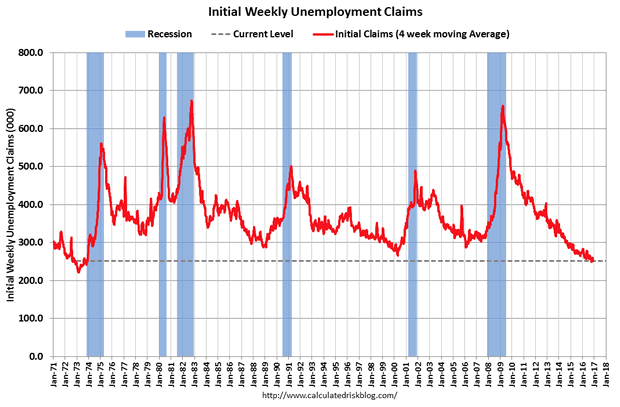

This series will cover a few of the more glaring examples of late-cycle myopia, beginning with jobless claims, i.e., the number of people joining the ranks of the unemployed.

In hard times when layoffs are widespread and new jobs scarce, this number spikes. In better times, when jobs are plentiful and employers are desperate to keep good people, the number falls.

But when it falls past a certain point wages start rising at a rate that leads (through market forces and/or Federal Reserve actions) to rising inflation and higher interest rates, which are destabilizing and generally cause a recession.

So let’s see what this stat says about our place in the current business cycle:

It certainly looks like we’re back in 1999 or 2007, with a tightening labor market at the tail end of a long recovery. If so, interest rates should be rising. And they are:

On the surface, at least, the US seems to be following the standard script: A few years of recovery, followed by a tightening labor market followed by rising interest rates. Followed by a recession that works off the imbalances built up during the expansion.

But the interesting part of the process is always the (many and seemingly quite reasonable) reasons why it’s different this time and the old rules no longer apply. The latest batch includes the following:

1) The terrible quality of the new jobs being created. Where in past recoveries people who were initially laid off tended to eventually regain their old jobs or something similar, in this recovery the new jobs are mostly in service industries (read bar-tending and waitressing) that are no one’s idea of career-track. So there’s room for a few more years of growth to get those people back into their old high-paying spots before wage inflation really gets going.

2) The incoming administration is proposing a big increase in government spending and tax cutting, paid for with borrowed money. This is stimulative and should turbocharge growth, which in turn should boost corporate profits, making stocks a lot more attractive.

3) The next stage of monetary policy experimentation seems to involve central banks buying equities more or less indiscriminately with newly created currency. The Bank of Japan, for instance, now owns about half of that country’s equity ETFs, thus providing a huge boost to the Japanese stock market. Let the Fed decide to join this party and it’s anyone’s guess how high blue chip stocks can climb.

When laid out this way, these do sound like compelling reasons for optimism. And maybe they are. But remember, every single expansion in the past century came with equally-strong arguments for ignoring traditional limits. And every one of them turned out to be illusory.

….also from Martin Armstrong: The Cycle of Assassination & War Bottomed in 2014

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair