Currency

Every central bank wants a weaker US$

Every central bank wants a weaker US$

Every central bank in the world, including the US Federal Reserve, now wants a weaker US$, which proves that central banks can be overwhelmed by market forces even when they are united in their goals.

Central banks outside the US want a weaker US$ due to the long-term consequences of the actions that they themselves took many years ago to strengthen the US$. To put it another way, they now want to strengthen their own currencies against the US$ because their economies are suffering from the inevitable ill-effects...

….related: James Dines on the US Federal Reserve:

The stock market has gone on quite a tear since the election of Donald Trump. In fact, the colloquial name for the recent surge in the market is the “Trump rally.”

One company has stood above the rest during this “Trump rally,” however.

As noted by market legend Art Cashin, the director of floor operations at UBS and long-time trading veteran, Goldman Sachs, one of the 30 stocks making up the Dow Jones Industrial Average index, has been responsible for a huge amount of the increase in that index. From Cashin’s daily commentary on Wednesday (emphasis added):

“The Dow closed up 35 points and almost 23 of those points came from Goldman Sachs (GS). In fact, our good friend and fellow trading veteran, Jim Brown, at Option Investor, points out that GS has rallied $57 since the election. That means that GS has provided 441 of the 1363 points that the Dow has rallied. In case your calculator batteries are dead, that’s about one third of the rally, all due to Goldman.”

In fact, the recent jump for Goldman has put the stock at an all-time high.

Investors seem to be betting that the deregulation of the financial industry – Trump and his new Treasury Secretary Steven Mnuchin have talked about rolling back the Dodd-Frank Act passed after the financial crisis – and rising interest rates in the bond market could be a boon for Goldman.

Trump was sometimes critical of the bank prior to the election, even featuring Goldman CEO Lloyd Blankfein in an ad highlighting people that the candidate claimed did not have America’s interests in mind. Blankfein came out after the ad in support of Hillary Clinton.

Trump has hired a number of Goldman Sachs alums in powerful administration positions, including Mnuchin, who was a Goldman banker for 17 years.

Back in 2013 interest rates in the US and elsewhere started to rise, and the results were scary to put it mildly. Here’s an excerpt from a column that appeared here in July of that year:

Back in 2013 interest rates in the US and elsewhere started to rise, and the results were scary to put it mildly. Here’s an excerpt from a column that appeared here in July of that year:

Interest rates soared again last week. This weekend a lot of people are running a lot of numbers and getting some terrifying results.

It seems that the past few years of falling interest rates have lulled a big part of the global economy into financing with variable-rate debt. So when interest rates go up, there’s a world-wide reset in interest costs that, best case, amounts to a tax increase on individuals and businesses and, worst-case, threatens to blow up the whole system.

The most familiar but least worrisome part of this story is the adjustable rate mortgage, or ARM, which is basically a teaser-rate home loan that rises over time towards the prevailing 30-year fixed rate. The latter rate jumped from 3.5% to 4.5% in just the past month, which means ARM resets are now aiming at a higher target. For ARM holders, the resulting higher monthly mortgage payment is exactly like a pay cut or tax increase, leaving less around at the end of the month for new cars, vacations, etc. So discretionary spending drops and, other things being equal, the economy slows down.

Another victim is the long-term bond. Retail investors poured about $1 trillion into bond funds between 2009 and 2012, in part because bonds had been going up pretty much forever, and in part because investors were scared and bonds were sold by credulous financial planners as safe.

For a while it worked. Bond prices soared as long-term rates kept falling, which helped both individuals and pension funds rebuild capital lost during 2009’s debacle. But since the beginning of this year US bond funds have seen $60 billion depart, while bonds themselves have fallen hard (though, okay, not nearly as hard as gold). The price of US 20-year Treasuries, for instance, is down by almost 15% since April.

In other words, the “safe” part of individual and institutional portfolios is tanking. Here again, this is like a big pay cut which makes the holders of these funds less rich and therefore less likely to spend money.

But the real systemic risk enters with sovereign debt. One of the many ways the US, Japanese and European governments hide the effects of their mounting debt is by doing most of their borrowing for short periods of time, a few months to one year, where rates are close to zero and money is effectively free. In some cases short-term rates have fallen faster than borrowing has risen, producing lower interest costs even while debt has been piling up. Now, with long-term rates rising, governments have a choice: either roll their maturing long-term debt into very short-term paper, which would keep interest costs down but make it necessary to roll over even more debt each year, or keep the maturity of their debt constant and see their interest costs rise dramatically. Or have their central banks buy even more debt and write off the interest, which might prolong the lie for a while, but at the risk of a tidal wave of newly-created currency wreaking various kinds of havoc.

Now for the big one: Hedge funds and money center banks have created hundreds of trillions of dollars of interest rate swaps, in which holders of a security that pays a fixed rate of interest exchange this income stream for a variable stream based on some benchmark interest rate. The players on the variable-rate side of the bet lose big if rates keep rising. And most money center banks and many, many hedge funds are in this position. All it will take is a few of them to be overwhelmed by these bets going sour to pull down the whole show — exactly as happened with credit default swaps in 2009.

The interesting (if that’s not too neutral a word) thing about all this is that the events mentioned here will happen simultaneously if rates keep rising. ARM and bond fund holders will have less money to spend, slowing economic growth; governments will see their interest costs spike, making borrowing more expensive and risking a flight from their now clearly-mismanaged currencies; and derivatives markets will see growing instability in interest rate swaps, which might threaten rest of the rat’s nest that is the global banking community.

All because interest rates return to historically normal levels.

Confronted with the above doomsday scenario, the major governments pushed interest rates back down – in many cases into negative territory. This granted the variable-rate world a temporary reprieve from the consequences of its mistakes — and allowed the worst offenders to ramp up their borrowing even further. Government debt soared, derivatives books expanded and mortgage and auto loans returned to pre-Great Recession levels.

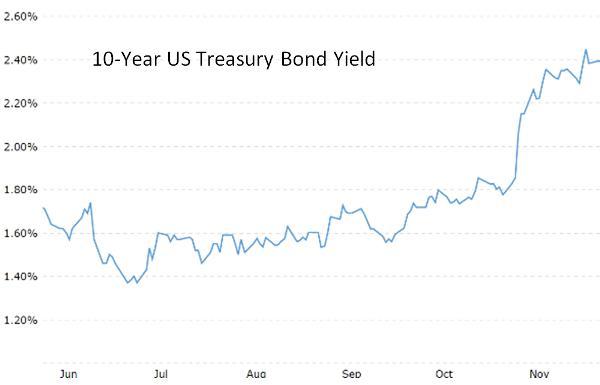

Now rates are rising again. Check out the near-parabolic arc of US Treasuries:

And the impact is, once again, being felt in the most rate-sensitive parts of the economy. Mortgage refinancing, for instance, is drying up:

Higher interest rates crush mortgage application volume

(CNBC) – The highest interest rates in well over a year are putting a dent in the mortgage business.

Total mortgage application volume fell 9.4 percent last week versus the previous week, on a seasonally adjusted basis. The Mortgage Bankers Association adjusted the weekly reading to account for the Thanksgiving holiday. Volume was 0.5 percent lower than the same week one year ago, the first annual drop in total volume since January.

“Mortgage lenders have been very thankful for a strong 2016 in terms of origination activity. However, mortgage application volume in the Thanksgiving week dropped sharply to the lowest level since early January, as mortgage rates increased to their highest point since July, 2015,” said Michael Fratantoni, chief economist for the MBA.

Refinance volume has been falling steadily as rates rise, but it took another sharp drop, down 16 percent for the week, seasonally adjusted. Refinances are most rate-sensitive and are now down 3 percent from a year ago, when rates were not much different than they are today.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.23 percent last week from 4.16 percent, with points increasing to 0.41 from 0.39 (including the origination fee) for 80 percent loan-to-value ratio loans.

And bond investors are losing their shirts:

‘Trump Thump’ whacks bond market for $1 trillion loss

(CNBC) – Donald Trump’s stunning victory for the White House may mark the long-awaited end to the more than 30-year-old bull run in bonds, as bets on faster U.S. growth and inflation lead investors to favor stocks over bonds.

A two-day thumping wiped out more than $1 trillion across global bond markets worldwide, the worst rout in nearly 1-1/2 years, on bets that plans under a Trump administration would boost business investments and spending while firing up inflation.

“We’ve had a sentiment shift in the bond market. People have already started reallocating out of bonds and into stocks, said Jeffrey Gundlach, chief executive officer of Los Angeles-based DoubleLine Capital, which has more than $106 billion in assets.

The stampede from bonds propelled longer-dated U.S. yields to their highest levels since January with the 30-year yield posting its biggest weekly increase since January 2009, Reuters data showed.

The 10-year German Bund yield rose to its highest level in eight months, while the 10-year British gilt yield climbed to its highest level prior to Britain’s decision to leave the European Union on June 23, known as Brexit.

Bank of America/Merrill Lynch’s Global Broad Market Index fell 1.18 percent this week, the steepest percentage drop since June 2015, which is equivalent to more than $1 trillion. Its U.S. Treasury index suffered a 1.91 percent decline on a total return basis, the biggest weekly drop since June 2009.

Auto loan rates, meanwhile, are spiking, especially for subprime borrowers. This couldn’t come at a worse time for a bubble that already seems to be popping:

6 million Americans have stopped paying their car loans, and it’s becoming a ‘significant concern’

(Business Insider) – There is a lot of talk out there about the auto-loan market right now.

Hedge fund manager Jim Chanos has said the auto-lending market should “scare the heck out of everybody,” while the auto-lending practices of some used-car dealerships has been given the John Oliver treatment on TV.

It’s a topic we’ve been paying attention to as well. In a presentation in September at the Barclays Financial Services Conference, Gordon Smith, the chief executive for consumer and community banking at JPMorgan, set out some eye-opening statistics on the market.

Now the New York Federal Reserve is taking a closer look at the market. In a blog published Wednesday on the New York Fed’s Liberty Street Economics site, researchers highlighted the deteriorating performance of subprime auto loans and set off the alarm.

“The worsening in the delinquency rate of subprime auto loans is pronounced, with a notable increase during the past few years,” the report said.

To be clear, the overall delinquency rate for auto loans is pretty stable, and the majority are performing well.

There are, however, signs of stress in the subprime market segment, which has seen rapid growth. Here are the key numbers from the report:

The subprime delinquency rate for the trailing four quarter period moved to 2% in the third quarter. The only other time it was 2% or more was in the aftermath of the financial crisis.

Subprime auto loan originations hit $31.3 billion in the third quarter, down from $33.6 billion in the second quarter. Outstanding subprime auto loan balances now stand at $280.2 billion, a record high. For perspective, the pre-crisis high was $249.5 billion, in the fourth quarter of 2007.

In other words, the subprime delinquency rate is creeping up, while the subprime market is ballooning in size. The Liberty Street Economics post, written by Andrew Haughwout, Donghoon Lee, Joelle Scally, and Wilbert van der Klaauw, said:

“The data suggest some notable deterioration in the performance of subprime auto loans. This translates into a large number of households, with roughly six million individuals at least ninety days late on their auto loan payments.”

Add it all up and a picture emerges of a system that can’t handle rising interest rates, but is nonetheless getting them. The result? At best a global slowdown and at worst an epic crisis. Wonder how the world’s governments will respond?

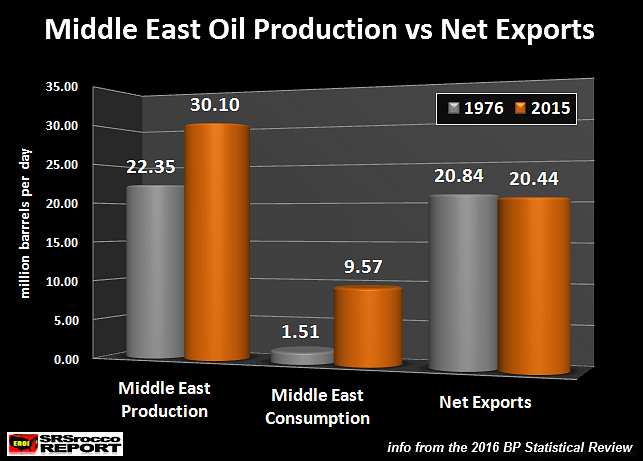

Yes, it’s true. Middle East net oil exports are less than they were 40 years ago. How could this be? Just yesterday, Zerohedge released a news story stating that OPEC oil production reached a new record high of 34.19 million barrels per day. To the typical working-class stiff, driving a huge four-wheel drive truck pulling a RV and a trailer behind it with three ATV’s on it, this sounds like great news.

Unfortunately for the Middle East, this isn’t something to celebrate. Why? Well, let’s just say, there’s more to the story than record oil production.

While the Middle East oil companies were busy working hard (spending money hand over fist) to produce this record oil production, their wonderful citizens were working even harder to consume as much oil as they could get their hands on.

In the past 40 years, Middle East domestic oil consumption surged more than six times from 1.5 million barrels per day (mbd) in 1976, to 9.6 mbd in 2015. This had a seriously negative impact on rising Middle East oil production:

…related:

Here’s Why The OPEC Cuts Won’t Hold

I have been watching the parade march by and after months of contemplation I have the following comments concerning the next 2 to 3 years.

I have been watching the parade march by and after months of contemplation I have the following comments concerning the next 2 to 3 years.

1.US Presidential election:

The election itself was not as important as the fact that a large percentage of the population has come to realize that we are on a course that cannot continue. Middle American decided that things must change. Dissatisfaction with the status quo is really what the 2016 election was all about. It was not republicans vs. democrats so much as it was globalist against nationalist.

2. The EU (European Union)

It appears that the euro was doomed from the start. Monetary policy was centralized but fiscal policy was not. Merkel’s immigration policy is just the last straw for many Europeans. Rules and regulations pouring out from Brussels are strangling the economies of all the EU countries. There are over 1,200 regulations on a “spoon”. There are over 1,000 regulations on “cabbages”. These regulations are coming from the central government from unelected bureaucrats that answer to no one. Many of the unelected ministers make over 300,000 euros / year along with their expenses. This new mandarin class of overseers can make regulations over the objections of the elected governments in the individual countries. The Italian banks have 18% of their loans in the non-performing category (US banks are about 2%). Italy cannot continue much longer without some sort of change. President Holland in France is on the way out and change is in the air for the coming election there. The EU will collapse as more countries pull out and quit paying for the central government. Wealth will flee Europe in the coming chaos and much of that wealth will find its way into the US markets. It will purchase blue chip stocks, high-end real estate, bonds and precious metals. This will cause the USD, precious metals, real estate and the stock market in the US to all go up together. Our balance of trade will become even more lopsided as our exports become more expensive.

3. Retirement and Life Insurance companies:

The ZIRP (the federal reserve’s zero interest rate policy) will cause retirements (both public and private) along with life insurance companies to blow up. The Dallas police and firefighters retirement fund is just the latest disaster. Watch for many more to follow. Many life insurance companies are spending down decades of accumulated capital because interest rates are so low. The math simply does not work anymore. Government defined benefit plans will not reduce payouts and will simply demand more tax revenue while private plans will default causing a great resentment against government retirees from retirees in the private sector. Eventually government retirements will be adjusted down but only after much bickering. Life Insurance companies will simply go bankrupt, as they just do not have enough yield to make the math work with bonds and mortgages. They will be forced further out on the risk curve, which will lead to failures one after the other.

4. BRICS (Brazil, Russia, India, China, South Africa)

The BRICS countries along with several other Asian countries will continue to pull away from the USD. Union Pay and the Asian “swift” equivalent will grow to over half of the world economy – outside of the USD and western banking system. If you haven’t yet noticed Union Pay it is the Chinese equivalent of VISA / Master Card. Many US merchants now accept it. Many MENA (Middle East & North African) countries are leaning east and away from the west. Some even predict that Germany may look east and hitch their economic wagon to Russia and China. The neo-cons in the US are fighting the BRICS and there is a lot of saber rattling going on with the “pivot to Asia” and baiting the Russian bear right on their European border. There has also been a recent declaration that “Russian” hacking on the internet is an act of war. (The very nature of hacking makes it near impossible to tell where it came from.) I pray to God that calmer heads will prevail and the neo-cons will fall out of power sooner rather than later.

5. Retail Trade:

Retail trade is changing and traditional retail stores such as Sears, JC Pennys, etc are continuing to get hurt by on-line sales. Young people are more comfortable with Amazon and other on-line purchases from the comfort of their own home. There is a larger selection available and popular sizes are rarely out of stock with on line stores. Commercial real estate for these companies will de-value greatly in the future. Office buildings are also changing since people can work from anywhere now. Few new high rise office buildings can cash flow now and most sell for much less than their replacement cost because current cash flow will not support new high rise construction costs in many markets. Many older office buildings are converting to condos and apartments. People still have to live somewhere even though they can shop (and in some cases work) on-line.

6. Health Care

Obama Care is coming apart at the seams with increases that are too large for most people to swallow. Health care is now mandated by law and the fine for not having it is also going up each year. The entire health care industry is around 12%+ (and growing) of the GDP. This is pretty outrageous and is squeezing the middle class more and more every year. I can remember having basic catastrophic “hospitalization insurance” when I entered the workforce many decades ago. Everything else was paid for out of pocket. You only insured the very expensive health issues such as a long hospital stay. You were required to pay your doctor and make arrangements with him privately. Third party payment has completely changed all that and now everyone thinks they should not pay over $5 for anything health related. Until we get rid of 3rd party billing and insurance except for only catastrophic illnesses we will never get heath care costs under control. Anytime “someone else” such as an insurance company pays the bill we are going to have a problem affording health care. Big pharma, big hospital corporations and big insurance companies are not the solution. Private contracting of services on a one to one basis is the only way to make health care affordable. The other direction only leads to a “free” government program with rationed care.

7. The War on Cash

Modi in India is the latest to declare war on cash by getting rid of the 500 & 1,000 rupee notes. Unfortunately that pulled about 85% of the circulating cash out of the economy and problems are legion. There is currently a $600 premium per oz on gold in India as people rush out of the local currency and into gold. Many countries are slowly trying to outlaw cash or at least discourage its use. The banker’s and the tax collector’s ultimate dream is to outlaw cash and run every last transaction through the banking system so that the bankers can charge a fee and the taxman can take his cut. People seem to forget that cash is freedom. Nothing good will come from this – unless you consider a yearly asset tax, even higher bank fees and a complete loss of financial privacy a good thing.

So where do these trends leave the average investor? Should we be careful investing in REITS specializing in shopping malls? Should we invest in UPS to capture the on-line delivery trade? Maybe, but asset allocation is probably the big picture that you need to consider. While I am not a fan of residential real estate millennial that do not want to purchase a home will have to live somewhere. Consider investing in real estate to house them. Possibly invest in apartment complexes, quads or even a garage apartment at your residence if allowed.

Stocks are overvalued but hot money from Europe and emerging markets will continue to pour into the US (the world’s last safe haven) and push them up for the next few years. Consider an S&P 500 index fund with low fees from Magellan since most of us are poor stock pickers.

Build cash and get out of debt. Spread cash around several different banks and keep a supply of cash (in small bills) on hand just in case. Up your precious metals allocation for long-term financial insurance.

Consider the following asset allocation:

20% real estate (income producing residential)

20% S&P 500 index stock fund (with low fees)

20% cash held in several local banks

(plus a few months living expenses in cash outside the banks)

20% gold & silver (buy the real thing and not an ETF)

20% short term corporate AAA bonds

(interest rates will probably go up so buy short-term bonds only)

If you don’t like this allocation then sit down and create your own mix. Decide on a plan and stick to it. Rebalance at least once a year in December. Of course you may want to make small adjustments and change up your allocations every few years but think through your allocations carefully and try not to make emotional decisions based on short-term news.

Larry LaBorde

Larry LaBorde sells precious metals through Silver Trading Company LLC. Please visit Silver Trading Company’s website at www.SilverTrading.net.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair