Timing & trends

Danielle Park on making sense of the massive post election rally, the market forecasting a 100% chance of a Fed rate hike, what we can expect with the current minuscule yields in the bond market considering capital flows.

….also from Michael’s Saturday Editorial: They’re Still Blowing Your Money – Does Anyone Care

The oil market is overjoyed and back above $50 a barrel following this week’s OPEC deal to cut production by 1.2 million barrels per day (bpd). The deal is expected to rebalance global inventories, perhaps in the first half of 2017.

The oil market is overjoyed and back above $50 a barrel following this week’s OPEC deal to cut production by 1.2 million barrels per day (bpd). The deal is expected to rebalance global inventories, perhaps in the first half of 2017.

I’ve got one word for that: Malarkey!

The fact is, oil’s in a temporary upswing at best. My models have been predicting bearish action in oil for a while now and I’ve spared no breath telling you about it. (More on this in a moment.)

And they’re not alone. Here are the latest reasons that oil is going down … and going down hard.

Bearish Factor #1: OPEC has a lackluster history of compliance with these kinds of deals: Over the last 17 production cuts – from 1982 to 2009 – their cuts came in at just 60% of what they promised. That translates to a measly 720,000 bpd — a drop in the bucket compared to world petroleum and liquids production of 96.26 million bpd.

Bearish Factor #2: Will non-OPEC member nations follow through with a 600,000 bpd cut? That’s a tall order with Russia already watering down their ability to cut their allotted 300,000 bpd because of “technical issues”.

Bearish Factor #3: The November 9th non-OPEC member meeting is liable to nix the entire OPEC deal before it even begins. Mexico already said they won’t cut their allotted 150,000 bpd in 2017. And Norway, Kazakhstan and Oman are sending mixed messages.

Bearish Factor #4: Even if all parties (OPEC and non-OPEC members) comply with stated adjustments, there are still concerns over supply and demand not addressed by the cartel.

Bearish Factor #5: Oil demand uncertainties have been moved to the back burner with headlines of a deal — but they’ve not gone away: Higher U.S. interest rates and a surging dollar — just like I predicted — are going to slam oil demand.

Bearish Factor #6: Recent data from China shows oil imports falling to their lowest level of the year in October. Plus, oil demand could come under added pressure from the yuan devaluation.

Bearish Factor #7: Then there’s economic uncertainty in India after Prime Minister Modi’s demonetization maneuvering, which is a threat to their appetite for crude oil.

Bearish Factor #8: Higher oil prices encourages greater production, which exacerbates an already massive global oil glut. In fact, the latest weekly stats from the U.S. Energy Information Administration shows oil production up 250,000 bpd in the last two-months to 8.699 million bpd.

I expect this figure to ratchet sharply higher with oil prices above $50, especially as U.S. shale producers have become technologically efficient. And higher oil prices will only bring more U.S. supply online.

Bearish Factor #9: Prospects for President-elect Trump’s administration to ease regulations on U.S. oil producers is another factor that aims at greater output, not less.

Why is this important to You?

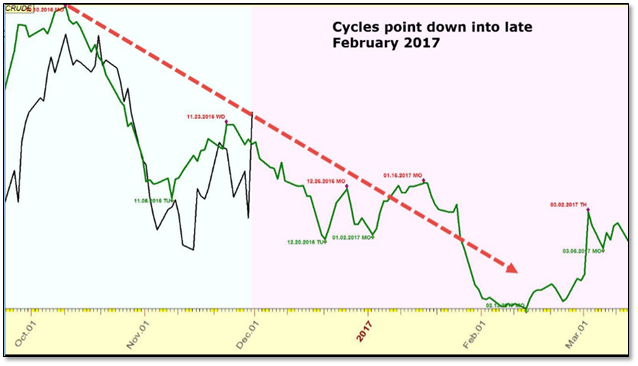

The initial excitement surrounding the OPEC deal means prices are bid up artificially. That creates an ideal selling — not buying — opportunity. And like I said, that’s right in line with what my models have been calling for all along: Lower oil prices into early February. Take a look:

I’ve advised my members to begin positioning for the next leg lower in oil prices. They stand to make a bundle as excitement over OPEC’s latest scheme fizzles and global market realities come home to roost.

Be proactive, guard your wealth and take advantage of these market anomalies by subscribing to the Real Wealth Report today.

Best wishes,

Larry

1. Something Big Is Happening….

1. Something Big Is Happening….

by Michael Campbell

No, Make That Something “Historical” Is Happening

– The 5000 year bottom in interest rates is in

– The 35 year bull market in bonds is over

– The Brexit vote & Donald Trump’s victory confirm the beginning of a major change in politics

– The Dow Jones has exploded to new highs since Nov 9th

– Gold has broken down

2. Is One Of Richard Russell’s Last And Most Shocking Predictions Now Unfolding?

Last year, Richard Russell made one of his last and most shocking predictions ever. Below is what the Godfather of newsletter writers had to say. (Richard was 91 when he wrote his last article) A must Read in full M/T Ed:

3. Marc Faber The Global Economy Is Entering An Epic Slump

Plus – Marc Faber: Current era of negative rates “a historic first”

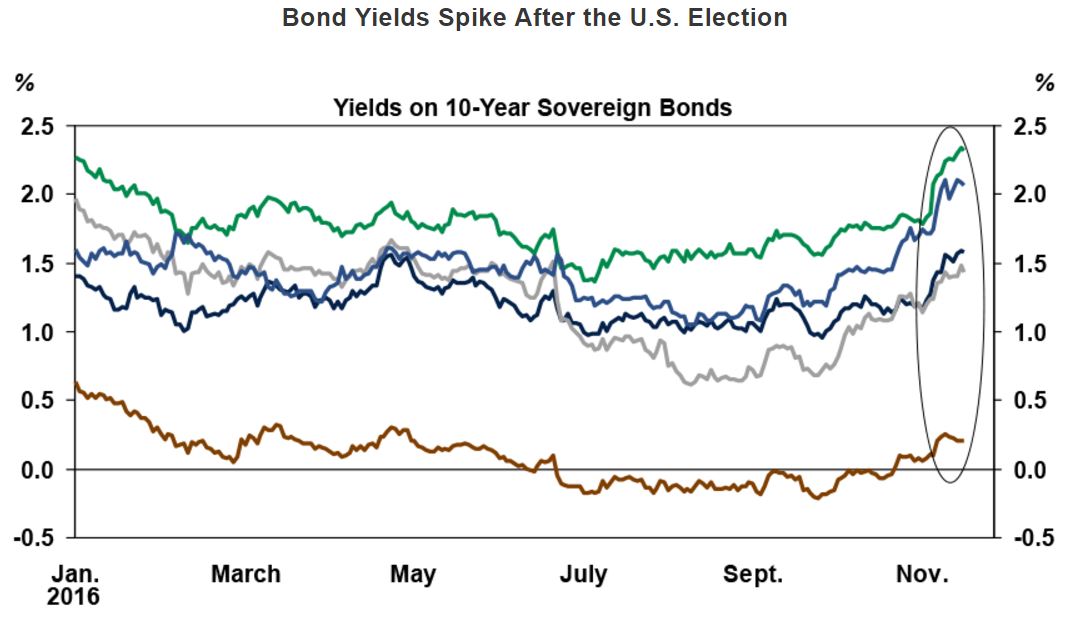

After the British backed the Brexit option at the start of the summer, U.S. voters in turn confounded forecasters by choosing Donald Trump as their next president in early November. Most observers initially expected that scenario to trigger a big surge in concern that would hurt risky assets. In the end, the surge in anxiety lasted just a few hours on the evening of the election, and investors quickly focused on the fact that the president-elect’s campaign promises could result in stronger growth and higher inflation in the United States. The outcome was a quick jump in stock markets, bond yields and the U.S. dollar. Investors must now ask themselves whether these moves are justified and if recent market trends will continue.

Although the dust has settled a bit after the election, we must first recognize that much uncertainty remains about what policies the future Trump administration will actually implement. The president-elect is still in the process of putting together his team and only takes power on January 20. He seems determined to quickly announce a series of measures, but it could take several months before they start to impact the economy. There is however some consensus among elected Republicans on…

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair