Wealth Building Strategies

A poorly performing company is in a state of constant and unmitigated chaos, where uncertainty abounds, communication is poor, and frustrations among employees, managers, and owners are high. Obstacles, both small and large, are throwing the company off kilter and there is no systematic approach to achieving order. Without intervention, long-term prospects are poor and its demise is inevitable.

A poorly performing company is in a state of constant and unmitigated chaos, where uncertainty abounds, communication is poor, and frustrations among employees, managers, and owners are high. Obstacles, both small and large, are throwing the company off kilter and there is no systematic approach to achieving order. Without intervention, long-term prospects are poor and its demise is inevitable.

There can be a number of reasons for this chaos. For instance, the company may be attempting to grow by expanding into new markets, but still using an old markets business model. Competitive threats could be driving industry changes but the company is in reactive mode, rather than leading those changes with innovation and new thinking. The company may have an insufficient focus on achieving sales, margins, and profit growth, and therefore be starved for capital and unable to make the necessary reinvestment in products, people, and infrastructure. Finally, the company may lack the resilience to withstand significant shocks, common in today’s economy, such as Brexit, abnormally low-interest rates, sluggish global growth, or technological change. Whatever the cause, this chaos must be acknowledged and dealt with.

The solution to taming this chaos, creating order and building a more resilient company, lies in implementing a systematic approach to building the business. In my more than 25 years of experience in transforming and building companies, as an executive, advisor, and board member, I have found that the best companies are built by leaders who work not only in the company but on the company. They have a clear sense of the difference between great products and a great company that produces great products.

For your benefit, I have summarized the six steps I believe are necessary to help reign in chaos and restore order, based on my real-life experience in running and advising companies. They are:

Buy-In

No company can achieve any meaningful change without first committing to change. Buy-in may be the result of a major crisis in the company (such as a big customer loss, cash crunch or other near death experience) which drives change, or it can be the result of an exceptionally powerful or visionary leader leading change. Either way, it is an absolutely and necessary first step in achieving growth and resiliency.

Assessment

A transparent, realistic, and objective understanding of exactly where the business is now is the next critical step. This is a thorough understanding of the company’s market, operational, financial, and execution strengths and weaknesses, validated by research and customer feedback. The assessment should also include a deep understanding of the talent in the organization, starting with the senior leadership through to all the roles of the company.

Plan

The plan encompasses the key findings of the assessment and lays out a clear, concrete, and well thought out roadmap which will create long-term value and market domination. The plan includes the necessary strategic initiatives that bolster your company’s position supported by actions and milestones. It should cover at least the next three year period, and include a 12-month perform cash flow and income statements. It should then be communicated to all employees and the necessary resources secured to ensure its successful execution.

Execute

The most successful companies I have worked with have an obsessive focus on execution. Research has consistently shown that the ability of a company to execute well is one of the strongest determinates of long-term success. Good execution includes building a culture of excellence, developing good systems, providing employees with the necessary skills and tools to succeed, and ultimately aligning the achievement of execution with long-term goals.

Measure

A small number of key metrics in the organization (less than six), should be tracked, reviewed, reported and acted upon on a regular basis. The goal of the measures are to ensure that the execution of the company’s action is in alignment with achieving the plan, and any significant deviation is highlighted and addressed.

Improve

Continuous and aggressive improvement is achieved by understanding the delta (gap or difference) between the plan performance and the actual performance, and then closing this gap. The best way for an organization to constantly improve is to build a culture of improvement and excellence, so the employees ultimately rise above the need for a methodical system and embrace the philosophy as their own.

Any company can be turned into a well-oiled machine and survive the turmoil that we are experiencing today by focusing on these six steps; buy-in, assessment, plan, execute, measure, and improve. Order can be achieved as the company grows through different stages of its maturity. There is no need to put your company at risk during difficult times, just follow these six steps and you will build a valuable, enduring, dominant, and resilient company.

By Eamonn Percy

We began writing on the War on Cash some time ago, when it was still just a theoretical ploy that we believed banks and governments were likely to employ as their economic adventurism continued to unravel.

We began writing on the War on Cash some time ago, when it was still just a theoretical ploy that we believed banks and governments were likely to employ as their economic adventurism continued to unravel.

But, in the last year, several countries have, as a part of the War on Cash, begun removing larger bank notes from circulation in order to force people to perform all economic transactions through the banking system, assuring that the banks would gain total control over the movement of money.

Of course, the banks could not admit their true goal to the public. They instead used the governments to claim that the measure was being undertaken to restrict crime (money laundering, drug deals, black marketing, terrorism, etc.)

Recently, without any fanfare, ATM’s in Mexico have ceased issuing the 500 peso note US$24). The largest note is now the 200 peso note (US$10).

At about the same time, Citibank in Australia declared that it will no longer accept coins or banknotes.

India has joined those countries that have done away with larger notes. They did so quite suddenly and the effects are already being felt by the Indian people. The elimination of the 500 rupee and 1000 rupee notes has, of course, not limited the level of spending in India, but it has caused a sudden demand for considerably more smaller notes through which to accomplish the same transactions.

A problem with the removal surfaced immediately when people using ATM’s were withdrawing far more notes than ever before in order to have enough cash to function normally. The ATM’s were quickly being emptied of the smaller denominations. The people of India cried foul, as 86% of all money in circulation had vanished from the system overnight. The limit for withdrawal per day is 2500 rupees (US$37) – which for some is sufficient to pay for daily expenses, but is most certainly not sufficient to carry on a business or facilitate larger transactions.

Although deliveries of notes to the ATM’s has increased, the banks simply cannot make up for the sudden loss of 86% of the nation’s money. Not only can the delivery trucks not meet the demand, the machines cannot store the volume of notes needed.

The result has been a partial breakdown of commerce. With millions of people beginning each day with insufficient funds to function, one bi-product of the money shortage is that over 9.3 million trucks have simply been abandoned by their drivers. (Nearly two thirds of all freight in India moves by road.)

In January of 2016, we published an article that made reference to the turning point of World War Two on the western front. Although the German war machine was collapsing, a major last-ditch effort was made at the Battle of the Bulge to reverse the tide of the war. German tanks raced to the battle and might well have made the Germans the victors, but they ran out of gasoline along the way .

The crews, understanding that the game was well and truly over, simply left the tanks and began to walk back to Germany. The great significance of this event is that, no matter how much bluster a political or military leadership presents, and no matter how obediently the soldiers respond to such posturing, once it’s clear that the game is up, the pretense amongst the soldiers evaporates.

The same is true in commerce. When those who make the decisions in banking and government try to game the system one time too many, dysfunction sets in and the “soldiers” – the countless minor participants in the system – simply walk away.

The lesson to be learned here is that, in all countries where a War on Cash is being destructively waged, the end will not be a positive one. The people of each country will increasingly become unable to function normally, as in Greece, where there have been riots due to the banking squeeze. Banks and governments have colluded to tie up wealth in order to have their hands on as much of it as possible, as they grow nearer to economic collapse. As the situation drags on, their intent is becoming ever-more transparent to those who have to suffer the difficulties caused by the squeeze.

But, as difficult as it may be to accept, these are “the good old days”. The direst events to come have not yet begun to surface.

As I’ve mentioned in past articles, the problem reaches its nadir when trucks that move the country’s food come to a halt. As long as sufficient food remains available to us, we treat it as just another commodity. But unlike clothing, hardware, vehicles, etc., when our source of food is cut off, even for a very short period, we become frightfully aware that its level of importance is far beyond that of any other commodity.

It’s been said that the average person abandons his moral inhibitions after three days without food. After this time, an otherwise morally responsible man is literally prepared to kill his neighbour for a loaf of bread.

To date, none of the countries that have declared a War on Cash has yet experienced a food panic. It would not be surprising if India becomes the first, as their trucking problem has them on the edge already.

However, it’s ironic that the War on Cash problem is most pronounced in what was called “the free world” only two generations ago. Many of those countries that we’ve come to regard as being both prosperous and “safe” are becoming less so with great rapidity.

Small wonder, then, that an increasing number of people are exiting these once-choice jurisdictions and seeking those that are not similarly in economic decline. Although we cannot predict how far the elimination of cash will spread, the further you are from the epicentre of the problem, the greater your chances of coming out with your skin on.

The trick, of course, is to say, “This is where I get off,” well before (as we are beginning to see in India) the driver himself has abandoned the bus.

…also:

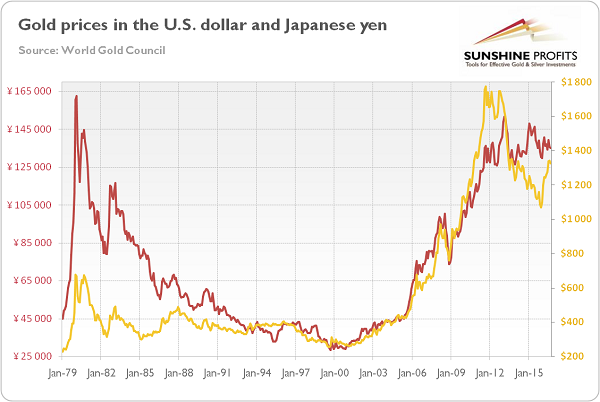

Our Market Overview would be incomplete without remarks about gold priced in the Japanese yen. Chart 1 shows nominal gold prices denominated both in the U.S. dollar and the Japanese currency, while Chart 2 plots the indices of gold prices in these two currencies.

Chart 1: The price of gold in U.S. dollars (yellow line, right axis) and in Japanese yen (red line, left axis) from January 1979 to September 2016.

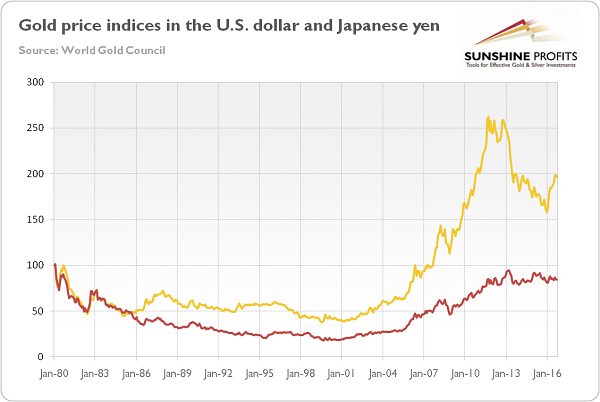

Chart 2: Indices of gold prices in the U.S. dollar (yellow line) and the Japanese yen (red line), January 1980=100.

As one can see, gold prices denominated in the greenback and the yen often move together. There were only two significant divergences in the relative performance of gold priced in the U.S. dollar versus gold prices in the yen. The first case occurred in the 1980s, when the yen strengthened against the greenback, leading to strong declines in yen-denominated gold prices. The second case started in mid-2014. In the second half of that year, gold priced in yen has outperformed its dollar cousin due to the strength of the greenback against the yen and the decline in Japanese real interest rates. However, in 2016 the U.S. dollar depreciated against the Japanese currency, which led to the underperformance of the yen-denominated gold prices. The reason may be the Fed being more-dovish-than-expected and the rising conviction that the Bank of Japan has been approaching the limits of monetary easing. Indeed, the introduction of negative interest rates in January and changes in the monetary policy framework in September have largely failed to weaken the yen, as investors judged that these actions implied that the BoJ had little scope to ease policy further. Such a belief diminished the perceived divergence in monetary policies between the Fed and the BoJ, which supported the gold market this year. Let’s analyze the chart below which plots gold prices against the balance sheets of the Fed and the BoJ, showing the divergence in the monetary pumping.

Chart 3: The price of gold (yellow line, right axis, P.M. London Fix), the Fed’s balance sheet (green line, left axis, in $ million) and the BoJ’s balance sheet (red line, left axis, in 100 ¥million), from January 2003 to August 2016.

As one can see, there is no clear correlation between gold prices and central banks’ total assets. However, the price of gold entered the bear market period at the end of 2012 when the BoJ adopted a more aggressive stance associated with Abenomics and the growth of its monetary base accelerated.

Looking forward, we expect that the divergence in monetary policy between the Fed and the BoJ will persist, supporting the U.S. dollar. The divergence has receded somewhat this year as the Fed has dialed back expectations for the pace of rising interest rates, however it may return to the spotlight in December when the Fed may hike interest rates, while the ECB and the BoJ would probably continue to loosen their monetary policies. Indeed, the BoJ left the possibility of more asset purchases and further interest rates cuts – at the press conference after its September meeting, Kuroda said:

“We won’t hesitate to adjust monetary policy with an eye on economic and price developments. “We will ease further when necessary. We can cut short-term rates, lower the long-term rate target, buy more assets or if conditions warrant, accelerate the pace of expansion in monetary base. There’s room to ease further with the three dimensions of quantity and quality of assets as well as interest rates.”

It goes without saying that a strong dovish statement from the BoJ could weaken the yen and strengthen the U.S. dollar, which would be negative for the price of gold. In a scenario of the broadening divergence in monetary policy between the major central banks, investing in gold priced in the yen (or the euro) would be a smarter choice than investing in gold priced in the U.S. dollar. Naturally, there is only one “gold” that can be purchased and the above simply means that those who hold the euro or yen and use it for purchasing gold, will likely benefit more (vs. the value of these currencies) than those, who hold the US dollars.

Thank you.

Arkadiusz Sieron Sunshine Profits

….related:

The Walt Disney Company is one of the largest media conglomerates in the world. To understand the company’s scale, we can look at the Media division, which alone represents approximately 40% of revenues.

The Walt Disney Company is one of the largest media conglomerates in the world. To understand the company’s scale, we can look at the Media division, which alone represents approximately 40% of revenues.

The Media division includes one of the four major television networks in the United States (ABC) and various other networks known as “Disney Channels”. The crown jewel of this division is the ESPN sports network and its affiliates (ESPN2, etc.).

Another division, the Disney brand products, has a huge library of movies among other assets. The latter continues to expand through the regular introduction of new products from various divisions, such as Pixar (Toy Story), Marvel Comics and its multiple superheroes and, more recently, the acquisition of Lucasfilm (Star Wars).

Obviously, these stories and characters are also marketed as amusement park attractions and other derivative products… CLICK HERE for Steve’s complete analysis

Last year, Richard Russell made one of his last and most shocking predictions ever. Below is what the Godfather of newsletter writers had to say. (Richard was 91 when he wrote his last article) A must Read in full M/T Ed:

Last year, Richard Russell made one of his last and most shocking predictions ever. Below is what the Godfather of newsletter writers had to say. (Richard was 91 when he wrote his last article) A must Read in full M/T Ed:

The Calls That Made Him A Legend

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late 1950s through the 1990s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Frightened, People Wouldn’t Pay $10,000 For A Building In New York City

I remember well during 1932, that real estate parcels in New York City were often for sale for $10,000 cash. Yet they didn’t sell because people were afraid to put down $10,000 cash on a New York City building. Anybody who had cash refused to part with it regardless of the huge possible return on their money. If you had cash, you thanked God that you had it and no investment was juicy enough to entice you to put down your money. Thus, New York real estate was selling at giveaway prices and it stayed that way until the Great Depression ended..

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair