Bonds & Interest Rates

Across asset classes, investors are worried about a bond market crash, according to a survey of fund managers around the world conducted by Bank of America Merrill Lynch.

Across asset classes, investors are worried about a bond market crash, according to a survey of fund managers around the world conducted by Bank of America Merrill Lynch.

They think that bond prices are frothy, showing signs of being in a bubble — meaning that prices are much higher than what bonds are actually worth.

Bond prices rose and pushed yields lower as investor demand grew and central banks, in Europe for example, bought bonds to lift inflation and fire up their economies.

…related:

Central bankers are able to put off the day of reckoning for years

Oct 25, 2016

- The US election is now only about two weeks away. The winner of this election is likely to be… gold. Here’s why:

- Both candidates are eager to increase infrastructure spending, and that’s likely going to open the door to congressional discussion of the issuance of perpetual bonds (aka “perps”).

- That’s inflationary. It is also going to lead to a significant drop in central bank credibility, because central banks will be reluctant to increase the cost of borrowing for governments at a time when governments want to borrow more for their infrastructure spending schemes.

- Please click here now. The longer that central banks wait to increase interest rates more consistently and substantially, the more dangerous the credit bubble becomes.

- Also, bank loan profits have been in a twenty-year bear cycle. That has caused a vicious deflationary bear cycle in money velocity.

- Central banks are prolonging that bear cycle by promoting unprecedented growth of government debt and unfunded social programs.

- The longer that central banks wait before moving interest rates noticeably higher, the more violent the liquidity flows from the government bond markets will be when the rates are finally hiked.

- In my professional opinion, I think most career politicians really believe the world is in a “new era”, where governments can take on unlimited amounts of debt without any real consequences.

- Central bankers are supporting this fantasy world view by pretending that the economic upcycle now in play from 2009 was created by them.

- They created nothing except more danger for pension funds and government bond investors. Central banks effectively engineered a massive flow of bank assets into the stock market, real estate, and government bonds.

- They did it with the biggest attack on Main street citizens in the history of America. Main street workers and pensioners have really been under constant attack since 2009, via QE and low rates.

- The one rate hike that Janet deployed in December of 2015 has been the only real central bank help for Main street in the past seven years.

- That help is just a drop in a bucket. Much more needs to be done in 2017. Main street needs four rate hikes over the next twelve months. I’m predicting they get two, which is better than one or none.

- Western governments need twenty rate hikes from the US central bank. That’s the only way to force them to clean up their disgusting debt-obsessed acts. Sadly, in 2017 I expect most American politicians will cry like babies over just two rate hikes.

- Paul Volker had no problem raising rates to 14% to reign in inflation. Janet Yellen should have even less issue with hiking rates to reign in government lunatics who act more like dictators than politicians. Government size is the disease. Aggressive rate hikes are the cure!

- Gold is very well supported at this point in time. Please click here now. Double-click to enlarge. After bursting upside from a small symmetrical triangle pattern, gold is coiling nicely in a drifting rectangle pattern. My next short term target is $1285.

- Please click here now. Double-click to enlarge this daily bars silver chart. I look for key non-confirmation events between gold and silver, and there’s a great one in play right now.

- On this pullback, gold is trading near the key February highs, and has even traded below them, while silver has held well above its February highs.

- That tells me that inflation is becoming a potential issue, and silver’s relative strength during this pullback is a very positive indication that 2017 will see inflationary pressures strengthen more than they already have in 2016. Two rate hikes in 2017 plus one in December of this year should be enough to reverse the bank loan profits and money velocity bear cycles.

- I’ve predicted a revival in the Chinese gold jewellery market will commence by early 2017, if not sooner. Please click here now. Top Goldman economists are also very excited about the Chinese gold market.

- The bottom line is that gold is well supported by both the Western fear trade and the Eastern love trade.

- Please click here now. Double-click to enlarge. The risk-on dollar is drifting sideways against the safe-haven yen, and is technically overbought. If it starts to decline, I expect gold to race straight to my $1285 short term target zone.

- Please click here now. Double-click to enlarge. The US T-bond has swooned since the Brexit vote occurred, and that’s been a headwind for gold. In 2017, I expect the T-bond to swoon more, but against a background of falling real interest rates and rising nominal rates. That’s good news for gold.

- Gold stocks, like silver, are doing a bit better than gold itself is, compared to the February highs. Please click here now. Double-click to enlarge this daily bars GDX chart. I suggested the $22 area needed to be bought, and the pullback from the $32 area did halt in my target zone. GDX is now trading in a tight range between $22 – $25. I suggested traders could book light profits at $25, and that’s worked out well. Now, I think GDX is getting ready for a rally to $27, and pullbacks to $22 – $23 should be bought again, and sold between $25 – $27 for healthy profits!

Thanks!

Cheers

st

Oct 25, 2016

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

“A champion is afraid of losing. Everyone else is afraid of winning.” ~ Billie Jean King

The financial crisis of 2008 scarred many individuals and scared away even more; add in the Great Recession, and one can see that the average can come up with many reasons to avoid the stock market. To make matters worse, the unemployment rate remains stubbornly high, and wages in most instances are dropping instead of rising which means that many Americans have little to no disposable income left after expenses. Don’t for one second believe the twisted statistics issued by the BLS (Bureau of labour department); those statistics are on par with toilet paper.

Individuals making $30,000 or less per year are more likely to avoid the stock market, citing insufficient funds as one of the main reasons. There appears to be a misconception in thinking that one needs a lot of money to invest in the markets. Nothing could be further from the truth. One can start off with small amounts and slowly add to this base over the years.; the power of compounding is amazing. If you start young enough even putting away $50-$100 a month can add up to a sizable bundle by the time you retire.

Another misconception is that investing in the markets is risky especially after the crisis of 2008. If one is investing for the long haul and in quality stocks, then investing is one of the surest ways of making money and building a sustainable nest egg. However, one needs to understand what one is getting into and not pluge into the markets blindly as is the case with most individuals.

Lack of education

We are referring to financial education and not higher education from institutes such as colleges or universities. We would even go as far as to suggest what these institutes teach regarding the stock market is useless. If you want to learn something, you need to allocate some time to it and then put that knowledge into practise. Regarding the stock markets it would be wise to look at the history of the markets; study past stock market crashes; the events that lead to the crash and events that set the foundation for the next bull run. Then paper trade before deploying your hard earned cash?

If you are going to rely on a financial advisor; how are you going to know if he is not selling you sack of sawdust if you know next to nothing. In most cases people set themselves up to lose in the markets or to be taken advantage of; it takes two to tango. Surveys done by bank rate shows that Millennials were twice as likely as any other group to cite lack of financial knowledge as their main reason for avoiding the markets. If this trend persists, they are going to ten times more likely to ask the government for handouts when they retire.

Distrust of the Financial Markets

Yes, one could say there is a valid reason to fear the markets as many Millennials have grown up in an era of financial disasters; two of the most painful ones were the dot.com bubble and the Financial Crisis of 2008, which later came to be known as the Great Recession. However, again, lack of financial knowledge and the wrong perspective is what provides the foundation for this fear. Fear is a useless emotion when it comes to the stock markets; the best time to buy is when blood is flowing freely; translation, so-called disasters always provide opportunities for the astute investor. Additionally, one could have easily sidestepped both disasters by paying attention to market sentiment; in both instances the masses were euphoric, and they thought the bull market could last forever. Nothing lasts forever and when the masses are ecstatic it is time to leave the party.

Disaster can be viewed as an opportunity or as a tragedy; it all comes down to one’s perspective. Alter the angle of observance and the perspective changes.

Concept of retirement planning is nonexistent for many

Bankrate states that only 25% of Americans check their investments and retirement accounts more than once a month. These same individuals can spend countless of hours on their phones texting each other or on Facebook or otherwise known as Face Crack. One does not need to look at one’s investments every day, however, spending time on finding out what’s trending or where the crowd is leaning could make the difference between banking your profits or trying to catch a falling dagger.

Ideally, individuals should have a rough idea of how much they would like to have by the time they retire and then come out with a feasible plan. Otherwise, they are bound to come up with some harebrained scheme that is fuelled by fear when they suddenly realise that the years have passed away, but the account is looking as miserable as it did on the day of its inception.

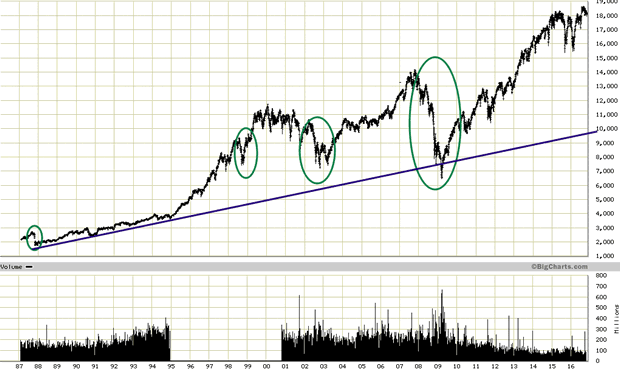

Disaster is usually opportunity knocking in disguise; take a look at the chart below

The financial world often refers to black Monday (the crash of 1987) when they want to ratchet up the fear factor; on a long-term chart, it is just another blip that more aptly represents an opportunity rather than a disaster. In every instance before the market pulled back firmly, the sentiment was extremely bullish; in other words, the crowd was euphoric. If you used just followed the emotion you would have managed to avoid almost every disaster and this dates back to the tulip bubble. We are not talking about timing the exact top; those that try to time the exact top usually have plenty of time on their hand and an enormous appetite for pain.

For the masses, sharp pullbacks feel like a crash because they have the uncanny ability to buy exactly at the wrong time; they buy high and sell low. We will examine the concept of opportunity being masked as a disaster in a future article.

Conclusion

The word disaster represents an opportunity for the astute investor. It is only the uneducated investor that views a market pullback through a negative lens, and this is usually done because they have not taken the time to study the markets. One would be well served if one spent some time in examining the history of stock market crashes and what was taking place before the markets crashed. In every instance, one will find out that the crowd was bullish and every Tom, Dick and Harry was busy giving out financial advice. When the crowd is happy, you should leave the party.

Spending a little time on history and market psychology could prove to be priceless. If you take the time to do this, you will have a better understanding of the markets than most so-called financial experts. The phrase “knowledge is power” was not coined for no reason, but there is a difference between knowledge and rubbish. When it comes to the stock markets, most of the stuff that is marketed as valuable is nothing but garbage and in many cases what the experts make fun of is what you should be paying attention to.

For instance, market sentiment is far from bullish even though the stock market is trading close to its highs. Hence, all sharp pullbacks have to be viewed as buying opportunities. When the crowd embraces this bull market, it will be time to leave the party.

“A man’s doubts and fears are his worst enemies.” ~ William Wrigley Jr.

Back in September we looked at a possible morphing Diamond on the GDXJ in which the dashed trendlines were showing the original Diamond. When it started to morph into the bigger Diamond I added the two red circles that showed the false breakouts from the original dashed Diamond. As you can see the last two weeks produced a rally that so far has failed below the apex of the morphing Diamond. From a Chartology perspective the Diamond is a reversal pattern as it has five reversal points.

Below is a longer term daily line chart for the GDXJ which shows how it is situated at the top of the big impulse move up out of the January low. The brown shaded support and resistance zone comes in between 29.75 and 32.50. It may be possible that the Diamond could be the reversal pattern at the first reversal point in a much bigger consolidation pattern.

In the very big picture the neckline symmetry line comes in around the 33.75 area on the long term monthly chart, which would be in the ball park of the brown shaded support and resistance zone. Symmetry suggests the right shoulder still needs a lot more work compared to the left shoulder.

Below is a daily chart for the GOEX, which is the old GLDX gold explores etf, which shows a Diamond reversal pattern in place with a small expanding rising wedge forming as a possible halfway pattern. The price objective for the expanding rising wedge comes in around the 29.56 area. The 50% retrace of the first impulse leg is at 30.15.

As you can see the indicators below the chart all have a positive cross. If the expanding falling wedge plays out to the downside it would be nice to see a positive divergence on the RSI at the top of the chart.

The breakout below the bottom rail of the Diamond consolidation pattern only took about four days or so to reach the low. If we see a similar move down to the price objective, that will shake many PM investors to the core. This looks like a good time to raise a little cash if one is a shorter term trader. For the intermediate to longer term investors sitting tight still looks like the best approach. Once we get the first reversal point in place, at the bottom of the new trading range, that will suggest the low for the rest of the bull market is in place. Surviving this first reaction low will test your mental fortitude if it plays out.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

We say no to pipelines, no exceptions. as C02 levels trump economic growth, job losses, growing energy needs. Meanwhile the world it not that simple. Especially when it comes to immigration, which the same people support without question.

….related from Michael: Venezuela : Reality Intrudes on Fiction

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair