Stocks & Equities

With all the surprising and/or disturbing things going on – Brexit, China’s soaring debt, US/Russia/China saber rattling, the, um, unique US presidential race, the cyber attack that shut down big parts of the US Internet – you’d think that an unsettled world would be reflected in skittish financial markets.

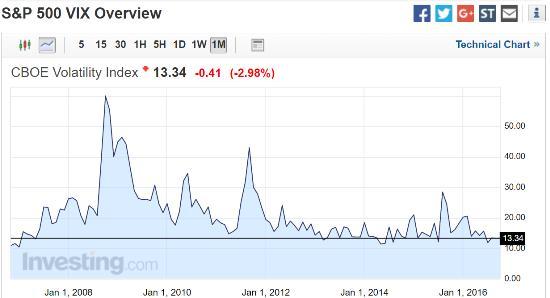

Instead we’re getting the opposite, with stock price movements becoming more and more placid as the year goes on. The following chart shows the volatility index (VIX) for the S&P 500 which, after some notable action in 2008 and 2011, has become ever-calmer, with recent readings comparable to the (in retrospect delusional) levels of 2006, just before the biggest financial crisis since the Great Depression.

What’s going on? First, during credit bubbles volatility normally contracts because enough new money is being created to provide pretty much everything with a bid. In other words, all the new liquidity being created by desperate governments has to go somewhere, so dips get bought before they can become dramatic and traders accept the placid present as the new normal.

Second, we’re in an election year and the people currently in charge badly want their chosen candidates to win. So government spending is rising dramatically. The federal deficit is up 17% so far this year, but jumped 67% in August. This burst of new borrowing has given the economy its current “all is well, stay the course” gloss. A bit more on this from MarketWatch:

U.S. runs $107 billion budget deficit in August, Treasury says

The federal government ran a budget deficit of $107 billion in August, the Treasury Department said Tuesday, $43 billion more than in August 2015.

The government spent $338 billion last month, up 23% from the same month a year ago. Spending rose notably for veterans’ programs and Medicare, Treasury said.

For the fiscal year so far, the budget deficit is up 17%. The government’s fiscal year runs from October through September. The Congressional Budget Office estimates the shortfall for fiscal 2016 will be $590 billion, or about $152 billion more than last year.

And what does it mean?

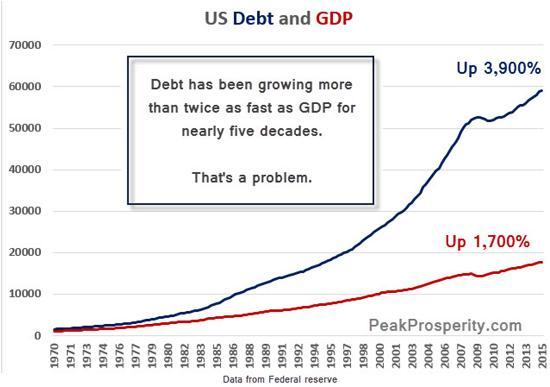

The current financial market insouciance is no more sustainable than that of 2006 because it’s caused by temporary factors that can’t continue without themselves causing turmoil. Debt, for instance, can’t grow relative to GDP forever…

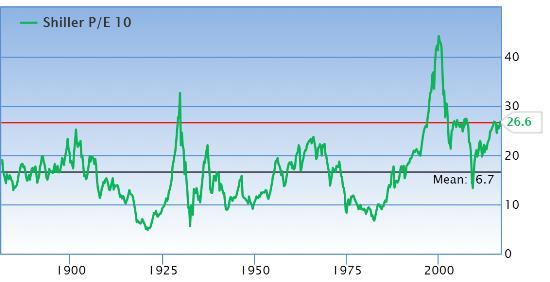

…and equity valuations have only exceeded their current levels thrice in the past century, each time with notable volatility following shortly.

So it’s a safe bet that 2017 will be in many ways a mirror image of 2016. US politics will be decided if not settled, government spending will stop spiking, and equities will return – possibly suddenly – to more historically normal valuations. And rising volatility will once again become the norm – as it should be in a world this dysfunctional.

How to play it? VXX is an ETF that tracks the VIX – but only for short periods of time. So it’s strictly a trading vehicle, not an investment. Shorting high P/E stocks is a longer-term way to bet on the coming mean-reversion of equities to lower valuations. Put options are a medium-term way to make the same bet with leverage. If we’re heading back to the exciting days of 2008 (which we are) then all of the above should provide both thrills and trading profits.

And precious metals, because they attract fearful capital, should benefit from the coming anxiety spike. Last time around – after an initial plunge – gold, silver and the shares of the companies that mine them embarked on a multi-year run that made them the best performing assets of the decade.

….also: Hot Properties: Government Blows Up Canada’s Hottest Industry

Money Talks listeners and readers have heard and read recent very clear expressions about pending equity market risks in the U.S. (from Martin Armstrong) and Canadian markets – especially in the Energy sector (from Josef Schacter). But what should you actually do? Should you seek shelter before the storm?

Money Talks listeners and readers have heard and read recent very clear expressions about pending equity market risks in the U.S. (from Martin Armstrong) and Canadian markets – especially in the Energy sector (from Josef Schacter). But what should you actually do? Should you seek shelter before the storm?

In 2008, many investors were either caught unaware of the systemic risks, or chose to ignore warnings of a major market crash. The financial pain from that (passive or active) decision to do nothing was profound; pain burns deep emotional scars that can be difficult to reverse. The theme of this article is simple: don’t make the same mistake again.

To be clear, our firm’s view is not an apocalyptic one. Our consistent investment thesis for the last 5 years has been (and still is) focused on over-weighting equities versus fixed income, U.S. equities versus Canadian and global equities, and tactical over-weights to stronger currencies like the $USD. Precious metals miners will eventually be very attractive as well. This thesis is the direct result of great work by our Portfolio Managers, including watching global capital flows (et al) via Martin Armstrong. This has resulted in our clients enjoying very solid risk-adjusted returns.

With the ongoing integration of Armstrong’s Socrates™ system into our managers’ processes, we remain optimistic about investment performance going forward. I’m certainly looking forward to attending the next WEC with Marty in Orlando on November 10th and 11th, and tapping into his models and systems to help enhance portfolio results going forward.

Given the downside risks (seasonality, U.S. election chaos, rising war-risk with Russia, stagnant global GDP, et al), each reader should carefully consider if it makes sense for them to lock in recent gains in stocks, bonds and currencies for a portion of one’s portfolio. This decision should be made BEFORE any major downturn begins, and should be made coolly and calmly in candid discussions with your trusted financial advisor – someone who really understands your goals, circumstances and “financial pain threshold.”

If your concerns are (even politely) dismissed as being irrational and you’re told to simply do nothing, then that in itself should be cause for a “mindful pause.” After all, it’s your money and dealing thoughtfully and respectfully with the emotions that surround your nest-egg is a critical part of the role that a great advisor plays in the journey toward achieving your Life Goals™. Tax consequences should also be part of the discussion, but remember the old age, “Don’t let the tax tail wage the investment dog.”

Minimizing the volatility during periods of market turmoil is something that most investors think is an implicit part of the investment management services that Canadians pay for. It should be, but the ability and willingness of large investment managers to be nimble within capital markets is shackled by three important limitations:

- The standard Prospectus (or equivalent) of most mutual and segregated funds typically requires each fund to be > 95% fully invested within their mandate;

- Mutual funds impose minimum holding periods and limit the frequency that an investor can make in-out-in tactical moves; and most importantly

- Canada’s investment management landscape is dominated by the major chartered banks, a few massive insurance companies, and several big mutual fund companies. Besides having an obvious bias toward riding through all short-term volatility, big money managers have a little-known practical problem: if they make major defensive moves by selling down a significant portion of their portfolios, they can actually cause turmoil by “spooking the market.” Translation: being too big limits their ability to be nimble. The result is that their size can actually work against your best interests.

There is a practical solution to this limitation, which you can find by clicking here: http://integratedwealthmanagement.ca/special-video/

Remember as well, that if you do decide with your advisor to partially “de-risk” your portfolio temporarily, that you need to be willing (and able) to buy back in again during a period of market panic. Don’t worry about timing this “perfectly,” because you’re improving your long-term returns as long as you get back in at a lower level than where you took money off the table.

Cheers,

Andrew H. Ruhland, CFP, CIM

Founder & President of Integrated Wealth Management Inc. in Calgary

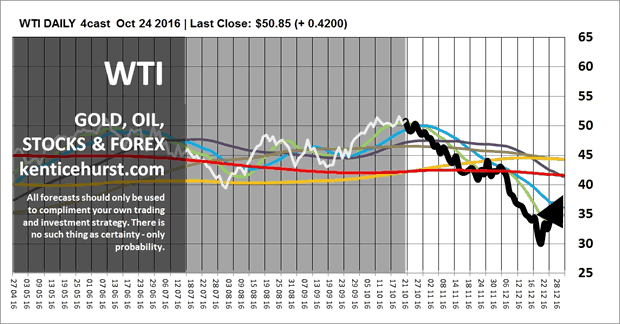

We should now begin to see a drop in WTI over the next couple of months and in to 2017, so far the consolidation that has occurred over the last few weeks has been as forecast and the next down phase we have been modeling for months is now due.

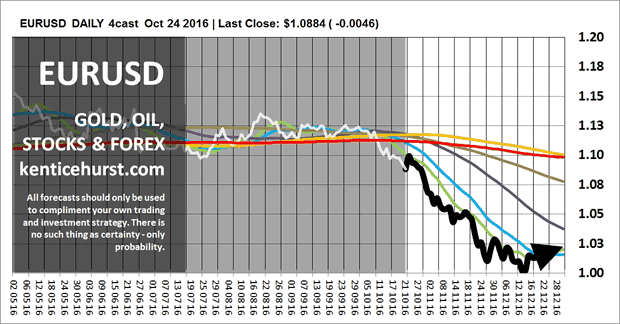

We have been forecasting for some time that the the Pound would be the weakest of the major currencies going forward and so far of all the major currencies it has been with the Euro not far behind.

Our forecast for a new down leg down in the Euro against the Dollar has remained on track for some time, we do now appear to beginning the next Dollar bull phase which could see parity within months. We expect this Dollar strength to be negative for many stock markets and other assets going forwards.

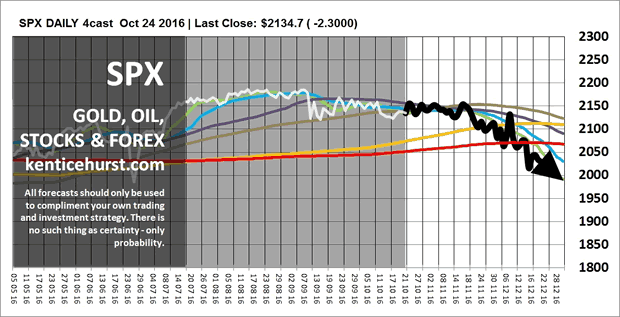

We are forecasting a correction in global stocks over the next six months, we think the SPX along with most of the major indices has put in a top, this fits in well with our commodity and forex forecasts. Our S&P500 forecast has remained on track for some time, it has been indicating that we are on the verge of a period of weakness it may take a few more weeks before we begin to see the market drop in earnest. We expect this weakness to extend well in to 2017.

We are still forecasting a new down leg in commodities, a stronger Dollar and an even stronger Yen during the fourth quarter of this year. We anticipate this Dollar strength will create the conditions for some key markets to sell off for a period which will relieve some over bought conditions necessary for a healthy market.

You can view live short term forecasts at our website, they are a representation of our medium and long term forecasts which always show the full picture, prices tend to be more random day to day than they are week to week or even month to month. Our short term forecasts are always anchored against these larger patterns that barley change from week to week, this is what allows us to be so confident with our shorter term forecasts in spite of the increase in volatility.

Taking patterns in nature that repeat over different time frames like fractals as the basis for the forecast methodology, our forecast patterns can last for months and years, we create a most probable long term fractal pattern and then continually test it and model it over multiple time frames to ensure the pattern remains a probable event.

Everything is so connected that a move in the US Dollar has broad implications. Believed to have made a low in May, the US Dollar has broken out of a chart formation and moved through a downtrend line. What comes next …..

….Don’t miss Martin Armstrong: The Worlds Top Forecaster, Reputation 2nd to None On The Markets & The US Electlon

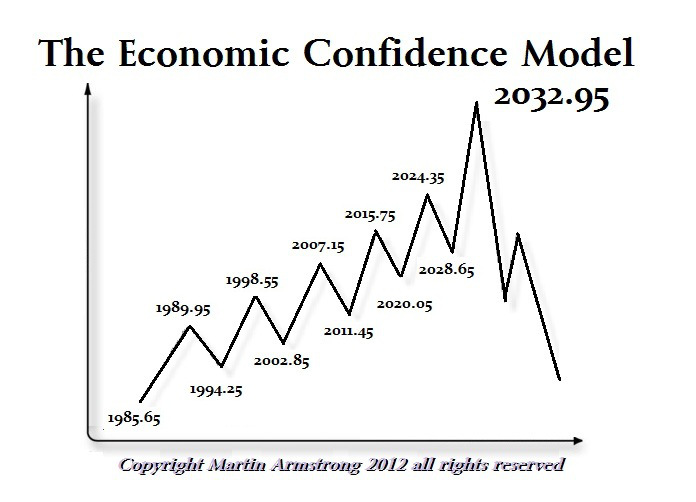

Martin Armstrong, whose reputation is second to none, on the moves he expects in the Stock, Bond, Gold and Currency markets. Martins model’s US election forecast, and when the nearby move up will begin from the current 5000 year interest rate lows. In this interview Martin explains why the Dollar has become the defacto world currency, why the US doesn’t like that, the steps they think they are going to take to correct. He thinks the US’s hands are tied and they can’t raise rates, nor can they avoid the pension crisis going critical. In short, Martin thinks that we are basically heading down into 2020, trust in government is at all-time lows and the 30 year bull market in bonds is over!

….Michael’s weekend editorial: Powerful Trends That Are Changing Everything

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair