Gold & Precious Metals

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

It is finally going to be a make or break earnings season for stocks. This is because the justification for record high stock prices that have been perched atop extremely stretched valuation metrics has been the following false assumptions: the hope that the Federal Reserve will not resume its interest rate hiking cycle, the U.S. dollar stops rising, the price of oil enters a sustainable bull market and long-term interest rates continue to fall.

It is finally going to be a make or break earnings season for stocks. This is because the justification for record high stock prices that have been perched atop extremely stretched valuation metrics has been the following false assumptions: the hope that the Federal Reserve will not resume its interest rate hiking cycle, the U.S. dollar stops rising, the price of oil enters a sustainable bull market and long-term interest rates continue to fall.

If all those conditions were in place investors could continue to believe a turnaround in the anemic 2% GDP growth rate endured since 2010 was imminent. And, most importantly, that a reversal in the 5 straight quarters of negative earnings on the S&P 500 was just around the corner. But even if they were perpetually disappointed in growth and earnings that didn’t materialize, they could always afford to wait until the next quarterly earnings report because there just wasn’t any alternative to owning stocks.

However, if earnings come in weak for the current quarter—which would be the 6th quarter in a row—that disappointment would occur in the context of a rising U.S. dollar, falling commodity prices, spiking long-term interest rates and a Federal Reserve that will most likely resume its hiking cycle in December. In other words, it would be game over for the equity bubble.

After all, market pundits have placed nearly all of the blame for the negative earnings string on a crashing oil price and a spiking U.S. dollar. However, during the 3rd quarter the WTI Crude price and the dollar were both very stable. And the price of crude was trading in the mid $40 a barrel range for both Q3 2015 and 2016. Therefore, if earnings don’t bounce back now how can they be expected to improve in Q4 and beyond, especially while the Fed re-commences its hiking cycle, which should cause the dollar to rise and commodity prices to fall once again?

So how does the earnings season look so far? Industrial and Metals giants such as Honywell, Dover Corporation, PPG Industries, Alcoa and United Technologies have all missed and/or warned on earnings for the third quarter. In the case of worldwide lightweight metals producer Alcoa, (down 11.4% on its earnings report) not only missed bottom line expectations but revenue fell by 6% year over year, which indicates the lack of global growth and demand for industrial metals. Multinational industrial giant Honeywell’s CEO Dave Cote said last week that Jet engine service orders, scanners, and logistic and shipping services simply failed to materialize in September. His warning and comments sent the shares down 7.5% last Friday. The company further sited worsening growth in the Middle East, Russia and China.

The free pass on overhyped stock valuations is now over. And with the S&P 500 trading at 25x reported earnings, this market needs a huge revenue and earnings rebound in Q3 or the gravitational forces of rising interest rates will send stock prices significantly lower.

The low on Treasury yields is most likely behind us. In fact, the Ten-year Note yield has risen from 1.36% in July, to 1.8% recently. Indeed, interest rates are rising across the globe as central bankers now believe higher long-term rates and a steeper yield curve are necessary for a healthy banking system. And the Fed has similarly duped itself into believing asset prices are not in a bubble and that borrowing costs can normalize without hurting equity prices and economic growth. However, both assumptions are extremely far removed from reality.

The truth is this protracted economic and earnings malaise—that shows no sign of turning around–coupled with record high stock prices and the reversal of a nearly decade-long zero interest policy on the part of the Fed is clear: a collapse in equity, bond and commodity prices concurrently. The reversal of the central bank’s trickle down wealth effect should cause a recession to hit the economy hard by the middle of 2017.

But this next bear market and recession may once again lead to a change in monetary policy on the part of the Fed. Collapsing equity prices and rising bond yields should cause the monetary megalomaniacs on the FOMC to follow up on Ms. Yellen’s recent threat to use fiat credit to purchase corporate securities in an attempt to reflate the bubble once again. That is when Pento Portfolio Strategies will close out our current short hedges, aggressively repurchase precious metals and use our substantial amount of spare capital to pick up internationally diversified high-dividend yielding stocks at a steep discount from today’s unreasonable prices.

Last December, the Fed’s liftoff from ZIRP sent stock prices tumbling over 10%–for their worst start of a year in its history. Investors still have time avoid a similar outcome. But since that correction in equity and bond prices should be enough to tilt this anemic economy into a recession, the cumulative collapse could end up being much worse.

The 2016 US presidential election between leading candidates Republican Donald Trump and Democrat Hillary Clinton has been unusual in that allegations of rape have cropped up during the campaign with Bill Clinton accused of rape, Hillary Clinton accused as an accessory, and Donald Trump accused of groping women without their consent. However, the core issue of the campaign — indeed the reason the Trump campaign exists — is citizen anger at a growing sense that their country itself has been abused at the hands of a financial elite. And this core campaign issue is lost as the back and forth sexual recriminations between the campaigns deflects attention from a critical issue.1

Something’s Wrong — And It’s Big

But citizens increasingly know something is wrong – and that realization is despite soaring stock markets and bond markets since the Great Financial Crisis of 2008.

The current US administration promotes an unemployment rate of 5% (down from 10% in 2009) as a sign that the economy has recovered from the Great Financial Crisis.

Flying in the face of this promotion is the fact that the number of adults not in the US labor force is 94 million people in September 2016 up from 80 million not in the labor force in October 2008. Excluding 14 million people from the US labor force so that they are not counted as unemployed helps to statistically reduce the unemployment rate.

And 41 million Americans now remain on food stamps up from 28 million in October 2008.

These statistics, and there are many more, show us that despite soaring financial markets fuelled by the Fed’s 0% interest rates, there is no real recovery underway. Soaring financial markets with moribund labor markets and rising prices for essential goods do not signal a healthy economy. Donald Trump knows it as do US voters.

On September 5, 2016 Trump warned that the Federal Reserve had kept rates artificially low and “It’s an artificial market. It’s a bubble.” warning that the bubble economy that the Federal Reserve has created had resulted in “very scary scenarios”. On September 6 Clinton immediately responded to Trump by saying that “presidents and candidates should not comment on Fed actions”. It was also revealed on September 6 that Goldman Sachs was banning partners from contributing to Trump’s campaign from September 1 forward.

The Rape of America (and Europe and Canada)

By (correctly) identifying the Fed as the source of economic distortions and the coming crash and impoverishment of the American people, Trump was alarming many in the financial industry by lighting fires of inquiry that cannot be put out. And the trail of evidence leads back not only to the Fed but to Goldman Sachs as well.

The rape of America has been a relatively simple process and involves a few key elements:

1) A debt-based currency system run by the central bank.

With a debt-based currency system and the ability of banks to instantly credit money into creation, the age-old formula of blowing bubbles can be effected by continually lowering interest rates and increasing the amount of currency in circulation thus driving speculation continually higher. This creates Trump’s “artificial markets”.

2) Recognize the inverse relationship between real interest rates and gold prices

Gold has historically limited the ability of central banks to blow bubbles by soaring in price. Former Clinton administration Treasury Secretary Larry Summers in his seminal 1985 paper with Barsky identified that the primary factor driving real gold prices was real interest rates (i.e. nominal interest rates minus the inflation rate). As inflation rises from loose central bank monetary policy, the real price of gold measured in constant dollars also rises and is the principal “tell” of those loose monetary policies. The principal driver of consumer goods inflation is monetary policy — as more money is created, goods prices also become more expensive. Indeed, the US dollar now buys 1% of what it could buy in 1913 when the Fed was created. But as was seen in the late 1970s, when inflation rages gold rages more. Central bankers are then forced to choose between abandonment of their paper money and bonds for real assets or to stop their money printing.

Now, Summers and Barsky were so certain of their observation that they wrote “(t)he negative correlation between real interest rates and the real price of gold that forms the basis for our theory is a dominant feature of actual gold price fluctuations.” [“Gibson’s Paradox and the Gold Standard“, Summers and Barsky, 1985 NBER working paper 1680 http://www.nber.org/papers/w1680.pdf]. The principal driver of the gold price was real interest rates — as they collapse due to inflation, the price of gold soars. The implication is that if you would like to sustain loose monetary policy for a protracted period, it is necessary to be able to control the price of gold.

And as we will see, the ability to control the bond market was almost lost in the late 1970s as both inflation and the price of gold soared forcing nominal interest rates up to the high teens before gold’s rise was arrested.

3) Convert the world’s principal gold markets from trading gold to trading paper gold thereby short-circuiting price discovery in the global gold and bond markets

The central characteristics of gold are that it is rare and of universally of value — gold has a 4,000 year history as a monetary asset as it cannot be debased or created without limit as fiat paper money can. With the 1987 creation of the London Bullion Market Association (LBMA) by the Bank of England (https://www.bullionstar.com/blogs/ronan-manly/from-bank-of-england-to-lbma-the-independent-chair-of-the-lbma-board/), gold trading was progressively thereafter converted to paper contract trading through the creation of “unallocated gold contracts” without gold backing and price discovery was thereby thwarted as these contract claims on gold can themselves be created and traded without limit (http://www.safehaven.com/article/42600/transition-of-price-discovery-in-the-global-gold-and-silver-market). By deflecting claims for gold into paper gold contracts, today there are an estimated 400 million to 600 million oz of claims for gold at the LBMA without gold backing and daily gold trading has reached 200+ million oz of gold per day (vs global annual gold mine production of ~ 100 million oz).

Price discovery of gold, and the ability of the price of gold to respond to real interest rates, has thus been greatly arrested — the knock-on and targeted effect was that the bond market was also short-circuited allowing the secular reduction of interest rates (and creation of mountains of debt in our debt-based economies). Central bankers could now defy gravity — for a while.

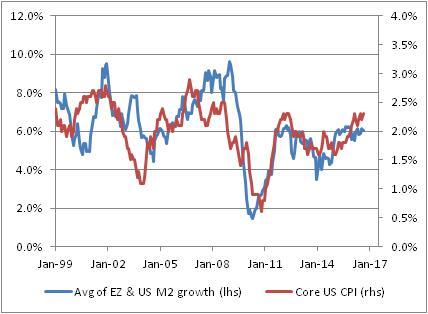

The following graph using the Bureau of Labor Statistic’s consumer price index (CPI) method of calculating inflation from 1980 held constant shows the 1987 decoupling of the price of gold’s historic inverse relationship with real interest rates with the creation of the LBMA — gold no longer responded by rising in price as real interest rates became negative and central banks were free to blow bubbles. Note also in the graph (where the inverse price of gold is plotted on the right) that in late 1982 the price of gold started to surge driving real interest rates to almost 9% higher than the rate of inflation before money started to return to bonds from gold.

Source: Reginald Howe, GoldenSextant.com. 1980 CPI computations by John Williams at shadowstats.com

Another issue given Goldman Sachs response of banning Goldman partners from donating to the Trump campaign is the key role of Goldman Sachs’ subsidiary J. Aron and Co. gold traders in advising central banks to sell and lease gold in the 1990s. Former gold banker and author Ferdinand Lips wrote at pages 123 to 124 in his book Gold Wars — The Battle Against Sound Money From a Swiss Perspective that he came to recognize in 1996 that Goldman’s J.Aron and Co. were the central advisors to central banks behind their gold policy to aggressively sell and lease gold into the market — thereby further depressing the price of gold (http://www.safehaven.com/article/35086/the-role-of-goldmans-jaron-and-co-metal-division-in-capping-gold-prices). Mr. Trump’s reference to a bubble economy driven by central banks and artificially low interest rates leads inexorably back to Goldman Sachs and the LBMA.

4. Now, continually lower interest rates over the next 30 years creating a succession of financial bubbles — when the bubbles pop, bail-out the banks and not borrowers

With gold no longer properly signalling artificially low interest rates by central banks this enabled the creation of a of a fake bubble economy as identified by Trump. When you rig the global price of gold, you rig the global bond market. Global credit market borrowing now totals $230 billion or 340% of global GDP more than double the historically sustainable level of 150% of GDP.

Central bankers have responded to the succession of bubbles and financial crises of their own creation by bailing-out the banks (lending up to $16 trillion to banks during the Great Financial Crisis) and prescribing lower interest rates and more debt compared to the needed monetary system reform and debt write-down to stabilize our economy. And Alan Greenspan who was appointed to the Fed in 1987 has retired and has been knighted as Sir Alan Greenspan by the UK establishment. A job well done.

The Bubbles are Popping but the Debt Remains

With the creation of the debt bubble and the consequent sequence of financial and economic bubbles, the US economy is now so distorted by Fed policy that even with the zero interest rates the economic output is growing at 1% and is declining. We are at the terminus point of exceptionally loose money started in 1987 by the Bank of England and the Federal Reserve.

With assets stripped from their hands and large numbers of Americans out of work and on food stamps, Mr. Trump’s words have not elicited reasoned discussion. Not only has Trump been told not to talk like that but the recriminations back and forth of sexual impropriety have stopped discussion of this core campaign issue reflecting American voter concern. And the hackneyed accusation of anti-semitism against Trump further muddies the waters (http://wallstreetonparade.com/2016/10/new-york-times-writer-suggests-donald-trump-is-an-anti-semite-for-his-reference-to-banking-conspiracy/) and with hedge fund donations to Trump totalling $19,000 vs 48.5 million for Clinton, we get some sense of the Candidate reflecting the interests of Wall Street. And this mirrors the Obama administration which executive structure was determined by Citibank (http://wallstreetonparade.com/2016/10/wikileaks-bombshell-emails-show-citigroup-had-major-role-in-shaping-and-staffing-obamas-first-term/).

The question now remains whether there will be any further discussion of this key issue broached by Trump and reform forced by the electorate or whether America will proceed with its politicians bickering about sex as the financial, economic and monetary system proceeds over the waterfall.

Notes:

1. The well documented alleged rape of nursing administrator Juanita Broaddrick in 1978 by former President Bill Clinton and Broaddrick’s subsequent intimidation into silence by Democratic candidate Hillary Clinton has revolted many long-time Democratic supporters (for a catalogue of some of Bill Clinton’s alleged crimes against women see: https://www.lewrockwell.com/2016/01/roger-stone/clintons-criminals/). And Hillary Clinton’s successful 1975 legal defence leading to the release of a rapist who raped 12 year old Kathy Shelton and audio tapes of Clinton laughing at the process as well as her using a defence that the child had a “tendency to seek out older men and engage in fantasizing.” leaves observers disgusted. The tape recording of Republican candidate Trump bragging about what women let a star like him do to them as well as the fusillade of accusations by women of unwanted groping and kissing by the Republican further leaves voters shocked — and not thinking. And more allegations are sure to follow in this political season.

We found out this week that there is pressure on the doves at the Federal Reserve, the biggest of which is Chairman Yellen, to raise interest rates. To some extent we already knew this, based on the dissents in favor of immediate hiking at the latest FOMC meeting. But the minutes this week provided evidence that the support for such a move is broadening, and even normally-dovish Fed speakers have lately been conceding the argument that it “may” soon be time to raise rates again. Notably, and critically, the Chairman is not among those turncoats. I continue to believe that Dr. Yellen will look for any and all excuses to skip a rate hike at coming meetings. Most observers don’t expect an increase to happen immediately before the US election, but the market is putting a pretty heavy weight on December. According to Bloomberg, Fed funds futures are implying a 2/3 chance of a hike at one of the next two meetings.

We found out this week that there is pressure on the doves at the Federal Reserve, the biggest of which is Chairman Yellen, to raise interest rates. To some extent we already knew this, based on the dissents in favor of immediate hiking at the latest FOMC meeting. But the minutes this week provided evidence that the support for such a move is broadening, and even normally-dovish Fed speakers have lately been conceding the argument that it “may” soon be time to raise rates again. Notably, and critically, the Chairman is not among those turncoats. I continue to believe that Dr. Yellen will look for any and all excuses to skip a rate hike at coming meetings. Most observers don’t expect an increase to happen immediately before the US election, but the market is putting a pretty heavy weight on December. According to Bloomberg, Fed funds futures are implying a 2/3 chance of a hike at one of the next two meetings.

The jobs number came in light at 156,000. This benefits the incumbent party because the number wasn’t good enough to invoke interest rate hike fears. It wasn’t bad enough for the market to tank. But all the other factors are still out there, including Deutsche Bank and now the rhetoric concerning a conflict with Russia is heating up.

So, my view has not changed. The markets are asleep and continue to sleepwalk in complacency and there are still too many possibilities for a black swan now only a month out to the election. I’ve heard different reports at this moment that are not confirmed, but we do know the Russians have instituted a no fly zone in Syria. What I can say is the rhetoric coming from both sides is nothing like I’ve ever seen and I was only two years old for the Cuban missile crisis.

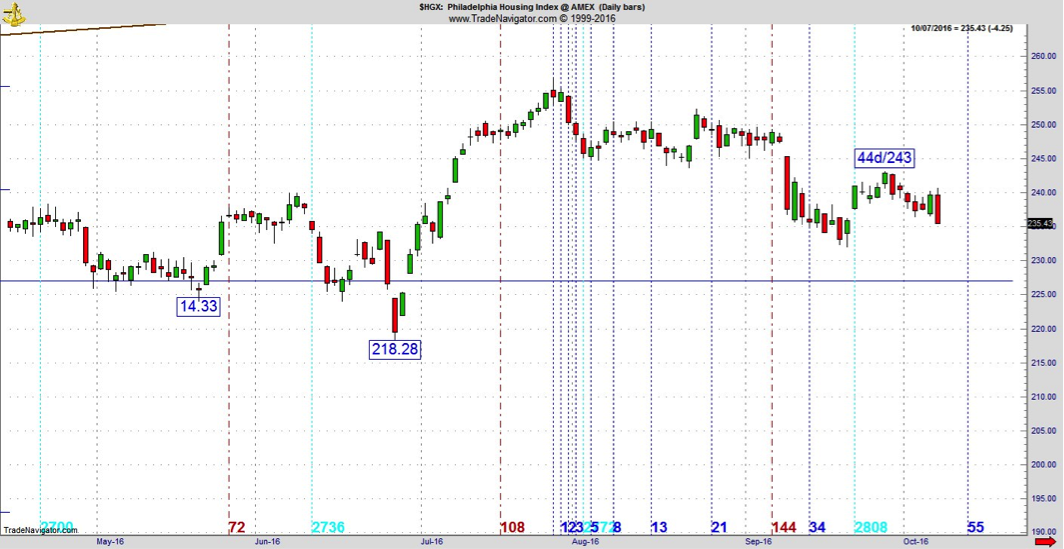

Coming into the week, there is a real shot oil could be peaking right here. Other sectors that could get into trouble are Transports and biotech, which gapped down and extended losses last week. Here’s some interesting symmetry for housing which may finally be losing it. There is a secondary high (second one off top) at 44 days off the top and a matching price at 243. This wouldn’t mean much without Friday’s candle, which was a bearish engulfing to the day before.

This one looks like it’s going to be tough to get back and if we lose housing, we are going to lose the market. It’s not a matter of “if,” but “when.” It could be right now as there will never be a better time in the entire calendar year. As you read this on Monday, note the date was right near the 2007 top and also the 2002 bottom. So this specific time of year has a history of important market turns. With everything swirling around, risk remains very high for an acceleration.

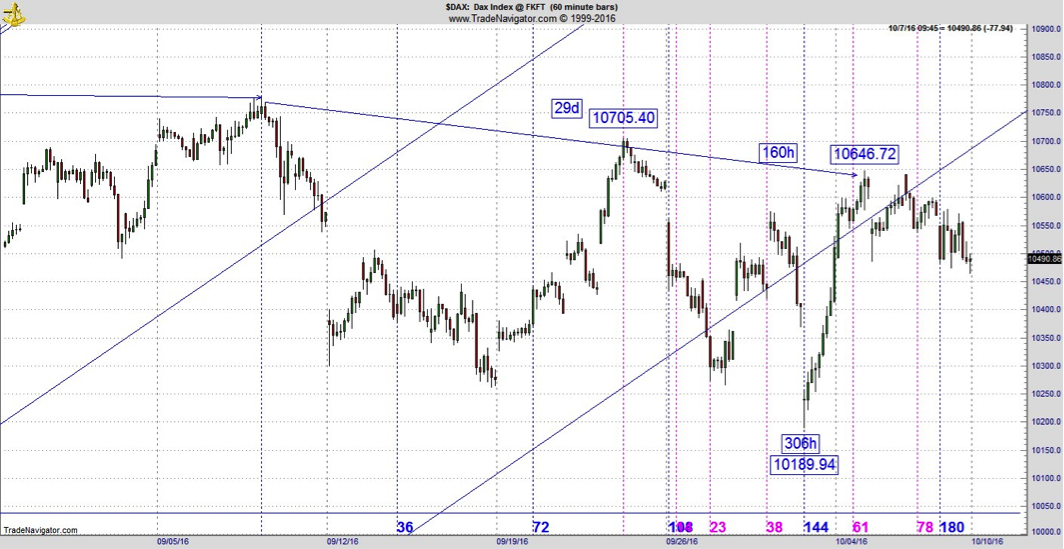

Of course, we know a lot of the trouble starts in Europe, especially Germany. The week didn’t end well there. So here’s a look at what could potentially lead down this week. First of all, the DAX turned lower on a 160 hour high to high sequence while the CAC stalled at 169 hours after a 4569 high. To start the week, the bears have an edge even as the initial Monday action in Europe was good for bulls. It might be small, but it still is an edge. But that’s only Europe, we have a divergence working.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair