Gold & Precious Metals

Briefly: In our opinion, speculative short positions are favored (with stop-loss at 2,210, and profit target at 2,050, S&P 500 index).

Our intraday outlook is bearish, and our short-term outlook is bearish. Our medium-term outlook is neutral, following S&P 500 index breakout above last year’s all-time high:

Intraday outlook (next 24 hours): bearish

Short-term outlook (next 1-2 weeks): bearish

Medium-term outlook (next 1-3 months): neutral

Long-term outlook (next year): neutral

The main U.S. stock market indexes were mixed between -0.1% and +0.1% on Wednesday, as investors hesitated following Tuesday’s decline. The S&P 500 index is the lowest since half of September. Is this a new downtrend or just more consolidation following June – July rally? The nearest important level of resistance is at around 2,140-2,150, marked by previous support level. The next resistance level is at 2,170, among others. On the other hand, support level is at around 2,120, marked by September local low. The market trades along medium-term upward trend line, as the daily chart shows:

Expectations before the opening of today’s trading session are negative, with index futures currently down 0.5-0.6%. The European stock market indexes have lost 0.7-1.3% so far. Investors will now wait for the Initial Claims number release at 8:30 a.m. The S&P 500 futures contract trades within an intraday downtrend, as it extends its recent move down. The nearest important level of support is at around 2,100-2,110. On the other hand, resistance level remains at 2,130-2,140, marked by short-term consolidation, as we can see on the 15-minute chart:

The technology Nasdaq 100 futures contract follows a similar path, as it extends its recent sell-off. The nearest important level of resistance is at around 4,800-4,820, marked by previous support level. On the other hand, support level is at 4,750-4,770, marked by some previous consolidation.

Concluding, the broad stock market fluctuated yesterday, following its recent decline. For now, it looks like a flat correction within a short-term downtrend. Therefore, we continue to maintain our speculative short position (opened on July 18th at 2,162, S&P 500 index). Stop-loss level is at 2,210 and potential profit target is at 2,050 (S&P 500 index). You can trade S&P 500 index using futures contracts (S&P 500 futures contract – SP, E-mini S&P 500 futures contract – ES) or an ETF like the SPDR S&P 500 ETF – SPY. It is always important to set some exit price level in case some events cause the price to move in the unlikely direction. Having safety measures in place helps limit potential losses while letting the gains grow.

Thank you.

….also:

Wall Street Earnings Recession is No Cause for Worry; Stock Market Bull has Been Ignoring It

I hope everyone enjoyed their Thanksgiving weekend. My weekend began by attending a memorial service for my wife’s friend who passed away from MS. It was a bit controversial as she was one of the first 200 pioneers of assisted suicide in Canada. She was only 60 years old and spent most of her adult life dedicated to raising a large family, and spending countless hours volunteering in our community. She will be greatly missed with the ripple effect far reaching.

Attending the service over the weekend reminded me once again, of the importance of planning for tomorrow but living for today. I turned 50 in June and am faced with the realization that I’m closer to 60 than I am 40. I don’t feel 50 but the fact is, I am. I have my health however, I know I’m not alone when it comes to financial planning and wondering what is enough? Is the 80% of income for retirement still relevant? Do I plan on living a long life rather than just existing at the end?

I am always interested in reading the most current financial articles that discuss the balance between living for today, but planning for tomorrow. I especially appreciated reading the weekend newspaper articles (October 8, 2016 National Post and Globe & Mail) about Canadians my age assessing their retirement readiness with financial planners. One publication discussed how to invest $700,000 while the other discussed the merits of robo advisors. The financial advisor recommended a 2% return of $14,000 after fees and taxes on $700,000. This approach makes absolutely no sense. To risk the volatility of the stock market for 2%? Why not leave your money under a mattress and pull $14,000 a year for the next 50 years without any risk?

With those options, no wonder the odds are stacked against the average investor. To add insult to injury, Portfolio Manager Martin Pelletier, of Trivest Wealth Counsel Ltd. was quoted in the Financial Post on September 27th saying that people should not invest in private equity investments, unless they have a minimum of $10 million of financial assets. So it’s ok for institutional and pension funds to invest but not the average investor?

We can offer a third option. It’s called genuine diversification that includes alternative and private equity investments into your financial portfolio. It forms a vital plan that can pay more than 2% but doesn’t expose the entire portfolio to ruin. That percentage is based on your suitability for risk and time horizon when you need your money back. The best news is you don’t have to have $10 million in the bank to invest, not even close in fact.

At TriView Capital, we want to help you if you think that your current investment strategy isn’t working. For as little as $5,000, you can invest in private equity through an OM (Offering Memorandum) with other eligible investors. As of 2016, Securities Regulators across Canada have imposed that new OMs must have audited financials which should help add greater transparency and accountability for investors. There are risks and it’s our job to take you through the pros and cons of alternative investing. Best of all, many can be added into your registered accounts.

Ahead of the 2017 World Outlook Conference, we will start highlighting these “8 ways to 8%” annual yields through MoneyTalks and our current investors. Please visit our website at www.triviewcapital.com as we start the process of showing you strategies towards “8 ways to 8%”.

Craig S Burrows ICD.D

There Is No Economic Recovery!

The FED and the Corporate World understand that there is NO economic recovery. They need to keep feeding this ‘bull market’ with plenty of accommodative easing or this ‘bull’ will die. The FED will do whatever it takes to maintain this by cutting rates to near zero and below so asto spruce up the economy. However, these conventional policies that are being applied, by the FED, will not work seeing as the ‘deflationary forces’ have gained momentum. Global economies cannot sustain rate hikes. They will continue to use ‘expansionary monetary policy’, indefinitely: (https://finance.yahoo.com/news/trump-says-fed-chief-yellen-114816250.html).

The FED will no longer remain the ‘lone wolf’ Central Bank of and by keeping interest rates from going negative. The New Zealand Central Bank went through this same cycle, last year, at which time the economy could not sustain a rate hike, thus resulting in a quick cycle of rate cuts.

The ‘herd mentality’ is now at the stage where they must accept this as the ‘new norm’. They want to keep this illusion alive and do not want to deal with the reality.

When the FED does implement negative interest rates, the stock markets are going to soar so high that it will probably even shock the ‘bulls’. Thus, this is the reasoning that the market will not currently crash, but will experience sharp corrections. In this current market environment, I now recommend putting your money into precious metals.

This is one of the most detested ‘bull markets’ in history. The FED has provided this market with the ingredients that it needs to take it to the ‘bubble level’. The masses will embrace this market in the same manner as the corporate world has done so for the past eight years.

The main trigger for the financial crisis of 2008 was the issuance of mortgages that did not require down payments. The ease at which one could get mortgages, in the past, is what drove housing prices into unsustainable levels.

Currently, Barclays has launched the “Family Springboard Mortgage” which allows homebuyers the opportunity to purchase a property with a mere 5% deposit. In order to acquire this 5% deal, one will need guarantors to put up the cash, which, in turn, will be lost if one fails to repay the mortgage.

Ones’ family/guarantor must place savings which are equal to 10% of the purchase price into a Barclays Helpful Start savings account. No withdrawals are allowed for three years. The Helpful Start savings account pays the Bank of England’s’ base rate plus 1.5%, which currently means getting 2% interest, before taxes. This is not a lot of interest considering the lengthy period of time: (http://www.barclays.co.uk/mortgages/family-springboard-mortgage).

When the FED starts purchasing private assets, this will negatively impact economic growth and consumers’ well-being. This reasoning is that the FED will use this power to keep failing companies alive and thus preventing the companies’ assets from being used to produce goods or services which are more highly valued by consumers.

The Reality:

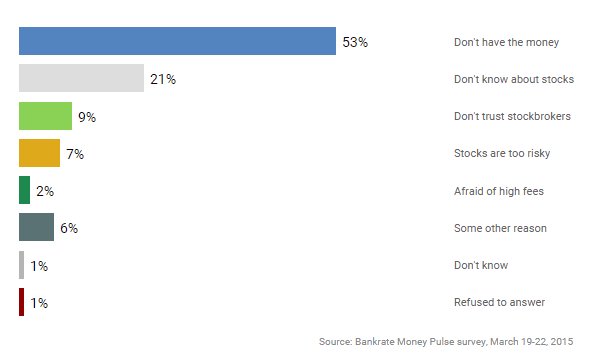

Over 50% of Americans do not have enough money to invest in stocks. The U.S., unfortunately, is currently appearing to be closer to that of a third world nation. Americans appear to be living hand to mouth thus making it more and more difficult for the average person to focus on his/her financial security. One in every seven Americans currently depend on food stamps in addition to using Food Banks, despite this ‘so-called economic recovery’.

The chart below from Banktrate.com illustrates that a total of 74% of individuals either do not have enough money to invest in the stock market or they do not know anything about stocks.

Random tests have already shown that the monkeys with darts fare better than most of these experts would.

The severe economic contractions which I have been speaking of, over the last couple of years, should now be evident to all of us, today. Productivity has now fallen to a negative rate. Investment has stalled and individuals have turned against globalization. Without productivity growth, capitalism becomes unpopular, globalization becomes unpopular and politicians, in turn, become unpopular.

Conclusion:

Gold and silver should be viewed as a form of insurance against the impending future financial disaster. We will also experience another disaster, sooner or later. I am not advocating that you should load up on bullion seeing as the precious metals sector has put in a bottom. I am referring to one obtaining insurance against another financial crisis that has the potential to be larger than the 2008 financial crisis was.

Every crisis also brings with it an opportunity, hence, one should make the best use of this opportunity before the price of gold and silver jump and value. It is better to invest now and see one’s investments multiply rather than waiting for the crisis to commence and pay a premium for insurance later.

The choice for president has never been so bad. The latest polls show 63% of voters said Clinton is overly secretive, 55% said she was corrupt, and 52% said she was “extremely liberal.” This is very interesting since the only presidents since 1900 to be elected with greater than 60% of the popular vote were Lyndon Johnson in 1964 after the Kennedy Assassination, 61.05%, Franklin Roosevelt in 1936 with 60.80%, Richard Nixon in 1972 with 60.67%, and Warren Harding in 1920 with 60.32%. Therefore, Hillary beats everyone with the highest rating of distrust.

The choice for president has never been so bad. The latest polls show 63% of voters said Clinton is overly secretive, 55% said she was corrupt, and 52% said she was “extremely liberal.” This is very interesting since the only presidents since 1900 to be elected with greater than 60% of the popular vote were Lyndon Johnson in 1964 after the Kennedy Assassination, 61.05%, Franklin Roosevelt in 1936 with 60.80%, Richard Nixon in 1972 with 60.67%, and Warren Harding in 1920 with 60.32%. Therefore, Hillary beats everyone with the highest rating of distrust.

The polls are being rigged as they were in Britain for BREXIT. But plan B is clearly being put into play already preparing the public for the accusation that should Trump win, the election will be called a fraud because of Russian hackers. The Washington Post, a big Democratic Party mouth piece, ran the story that Russian  hackers target the Arizona primary. CNBC is carrying the story that Russia will hack the elections. Obama has outright accused Russia of targeting the Democratic National Party (DNC) claiming two Russian hackers were discovered. This is the story being carried even by the BBC, yet the specialist called in was Shawn Henry, the chief security officer at company called in Crowdstrike, who is himself a former executive assistant director of the FBI. It was even bantered about in the second debate between Hillary and Trump. The New York Times is jumping in also carrying the story. Reuters is now reporting that there is no question that Russia was behind the hacker at the DNC.

hackers target the Arizona primary. CNBC is carrying the story that Russia will hack the elections. Obama has outright accused Russia of targeting the Democratic National Party (DNC) claiming two Russian hackers were discovered. This is the story being carried even by the BBC, yet the specialist called in was Shawn Henry, the chief security officer at company called in Crowdstrike, who is himself a former executive assistant director of the FBI. It was even bantered about in the second debate between Hillary and Trump. The New York Times is jumping in also carrying the story. Reuters is now reporting that there is no question that Russia was behind the hacker at the DNC.

Democrats are now warning foreign governments and hackers that cyber attacks against the U.S. will be treated like any other, even if it leads to war. DNS hijacking or DNS redirection is a common practice. This amounts to subverting the resolution of Domain Name System (DNS) queries. This can be achieved by malware that overrides a computer’s TCP/IP configuration to point at a rogue DNS server under the control of an attacker. It can even modify the behavior of a trusted DNS server so that it does not comply with internet standards. However, the hardest problem in finding the source of these attacks is really attribution. Each data packet sent over the Internet contains information about its source and its destination. Yet the source field can be changed [spoofed] by an attacker to make it appear as if it is coming from someplace it’s not. This is standard operational procedure. Consequently, I serious doubt that a professional hacker would have left a trace.

I cannot stress strong enough that there is no way they will allow Trump to enter the White House. It appears that should he win, like BREXIT against the odds and the polls, Obama will not leave and the election will be declared a fraud. Obama will most likely step down and hand it to Joe Biden. Out models are showing November as a rather important turning point and this seems unusual insofar as that it would be limited to merely an election. Something else may be in the wind.

….related from Martin: The Urgency of The Issues

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair