Timing & trends

Every investor has at least one horror story to tell.

Usually they involve an event that came out of nowhere – a “black swan” – that completely crashed or changed the market in an unpredictable way.

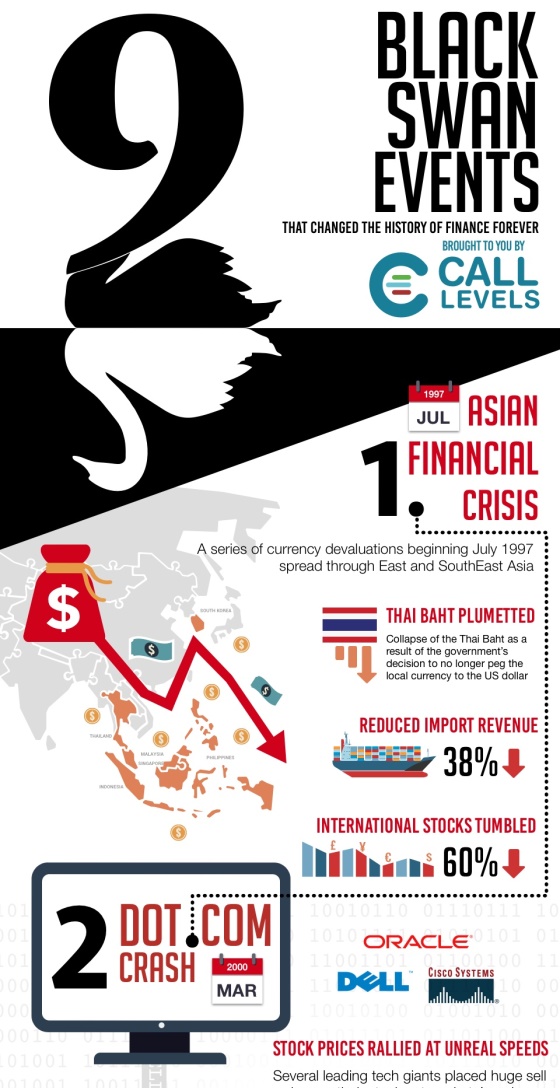

Today’s infographic covers nine of the most recent black swans and their deep impacts on markets.

Click image to view all 9 Black Swans That Changed Finance

![]()

The Department of Finance threw a major wrench into the gears on Oct 3 by making huge material changes to the way that many borrowers get qualified. Here’s a rundown of what is changing and how it impacts you and the market.

What is changing?

Effective Oct 17th, the qualification rate will apply to all insured mortgages, not just those taking terms shorter than 5 years or choosing variable terms. Currently the qualification rate is 4.64%. Many first time home buyers have been forced to choose a 5-year fixed rate as they would qualify at the actual rate itself instead of 4.64% (currently 5 year fixed rates are at or below 2.49% in most cases).

The rules kick in for any applications received by the insurer after Oct 17th, but in many cases lenders will stop taking new applications a few days in advance to give them time to prepare and submit deals to the insurers.

In order to be sent to an insurer, you must have a live deal (an accepted offer). Pre-approvals do not count.

This will not impact existing mortgages already in effect or existing mortgage applications that have already been approved (not just pre-approved).

Capital Gains for non-residents

Non-residents will no longer be able to claim the capital gains exemption for selling a principal residence if they were not a resident in Canada in the year the individual acquired the residence (a good thing)

This will impact those who attempt to flip houses and not pay the capital gains tax

Impact of the new rules (there are a lot)

Lower borrowing power for buyers, specifically those with 20% down but also those who may need to qualify on a program that banks require to be insured, even if you have over 20% down (like self employed programs, small square footage units, small towns, etc.)

Assuming the median income of $76,000 per year, the maximum borrowing power for someone who used to be able to purchase a $500,000 property with 10% down now qualifies for about a $425,000 purchase

Assuming an income of $100,000 per year, the maximum borrowing power for someone who could purchase a $700,000 property now qualifies to purchase around a $550,000 purchase.

Overall, a decrease in borrowing power of around 15% – 20%

Less competition – Non-bank lenders insure most or all of their mortgages and if they are unable to insure certain mortgages, those clients will have to deal with deposit taking institutions who can place those clients on their own balance sheet

Already the largest non-bank lender has pulled out of financing conventional (more than 20% down) rentals and business for self applications

Higher rates – If banks have to balance sheet applications, interest rates, especially for rentals, self employed, and other hard to insure business, will increase as the cost of funds is higher when they are not able to sell the mortgages in the secondary market as “MBS” (Mortgage-Backed Securities)

Renewals that are conventional (more than 20% equity) coming up that don’t fit the below criteria won’t be able to remain insured which may increase the cost, and so the best rates may not be passed on to those who don’t fit these criteria. These rules apply Nov 30, 2016.

Loan for a purchase of a property or renewal

Owner occupied (sorry, no rentals)

Maximum amortization of 25 years

Maximum purchase price of $1,000,000 at the time the loan is approved

Minimum 600 credit score at time of approval

Max Gross Debt Servicing of 39% (all housing related expenses) and Total Debt Servicing of 44% (all expenses including housing related and credit cards, loans, etc.) by applying the greater of the mortgage rate or the Bank of Canada five-year rate (4.64%)

If there are less non-bank lenders doing rentals, self employed, etc., that business will likely flow to the few remaining banks who are doing them. If this is the case, the banks will likely either tighten guidelines to stem the flow of new business or surcharge the rates for “unique” deals

Margins will shrink for non insured mortgages, which may create a larger gap between insured and uninsured mortgages (currently best rates are for owner occupied with less than 20% down, at about .1% better of a rate)

Revised B-20 guidelines are likely to include qualifying at the Bank of Canada rate even for those with over 20% down, we are being told. News have not been officially announced but seems likely at this point

Amortizations over 25 years may be surcharged or simply not available as banks won’t be able to insure those mortgages

“A-“and “B” lenders’ market share will increase as deals get tougher to do

Credit Union market share may also increase as these rules only apply to federally regulated lenders. Credit Unions are provincially regulated.

A Bank of Canada overnight lending rate (which impacts the Prime rate) drop seems more likely as:

Mortgage rules are often created to slow the housing market in an effort to curb the upward surge of real estate prices due to a low interest rate environment. This could be some foreshadowing, here

There is likely going to be a GDP hit from these new rules as oil and housing are two of the largest determinates of our GDP growth and are both on the ropes

Negative news to foreign buyers via the Capital Gains changes as well as the previous 15% foreign buyers tax in BC will deter foreign investment which Canada needs

What should you do?

If you plan to buy, make sure you know how the new rules will impact you. You may wish to pull the trigger sooner rather than later.

If you are buying a pre-sale, make sure a full application is made through your broker or bank to get an insurer’s approval now. The rate may not be guaranteed but at least the financing will be approved.

Refinance now. You are most likely to get the higher possible appraised value that we will be seeing for the short-medium term and new rules may make this more difficult to obtain

Suck up to your favourite Credit Union. They may become your best friend. I know I am (and will continue to be).

Can we please have a chat with Finance Minister Bill Morneau about the lack of government intervention in CREDIT CARD DEBT which is the main culprit to many personal bankruptcies and bury individuals in debt payments with card rates up to 29%?

Indeed, Kyle!

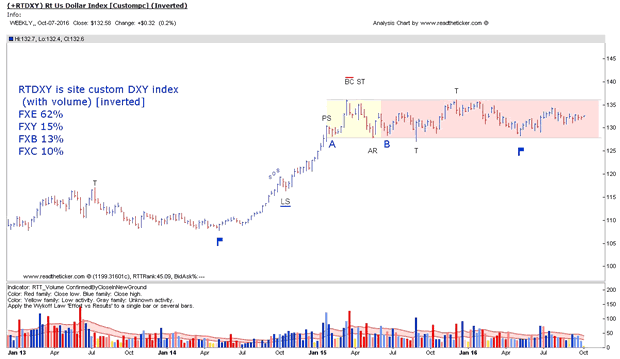

The last thing the US needs is a higher US dollar!

Higher dollar is due to:

1) Expected higher US interest rates

2) Less $USD in the world, as other pay back $USD loans

3) Demand for $USD dollar assets for safety.

4) Expected trouble in the European bank circles.

A higher is dollar is not good.

Below we have a very obvious accumulation pattern, watch this, a break out higher will be on news that wont be good for the world.

Investing Quote…

“I have yet to find a man, in or out of Wall Street, who is able to make money in (markets) continuously or uninterruptedly. Like anyone else, I have good and bad periods.” ~ Richard D Wyckoff

“I measure what’s going on, and I adapt to it. I try to get my ego out of the way. The market is smarter than I am so I bend.” ~ Martin Zweig

“It’s easier to fool people, than to convince them they have been fooled.” ~ Mark Twain

“Unless you can watch your stock holding decline by 50 per cent without becoming panic stricken, you should not be in the stock market.” ~ Warren Buffett

“By failing to prepare, you are preparing to fail.” ~ Benjamin Franklin

Please don’t take this as boasting, but for months now I’ve been using my cycle analysis and AI software to warn everyone I could that gold and silver and miners were headed lower, not higher.

And I gave a date. I stated they were headed lower into today, October 5. I made that forecast as many as seven or eight months ago.

Since then, we’ve seen gold plunge from as high as $1,377 to yesterday’s low of roughly $1,266 — a $111 drop, or just over 8.0%. The loss in silver has been similar.

I got my share of hate mail for that forecast, especially from those following the trading analysts out there who keep calling for the death of the dollar and who use every piece of news they can find to make an excuse for higher metals prices.

Unfortunately, they don’t understand the precious metals market. They can’t possibly understand it because most of them have never traded it. Most of them are unaware of the history of gold and most of them are simply fear-mongerers.

Not me. I tell it like it is, with my Artificial Intelligence Model and the waves, or cycles, I follow. My sole mission is two-fold …

- Keep you out of trouble, like I just did.

- Make you money, scientific profits and make it easy, with my very accurate forecasting models and more.

Right now, due to the severity of the selling, I cannot claim the low is in and the next leg up is about to start.

So we have to wait a few days to watch the action, which I will do for you.

Meanwhile, stay alert, the markets are really heating up.

Best,

Larry

Editor’s Note: Due to Hurricane Matthew, you may not hear from us for a brief time. We will resume our normal schedule as soon as the storm passes.

You read that right. Not only is Italy selling 50-year bonds, but people are lining up buy them.

You read that right. Not only is Italy selling 50-year bonds, but people are lining up buy them.

Italy’s first 50-year bond sale had huge demand

(Reuters) – Italy sold its first 50-year bond on Tuesday as some investors bet the European Central Bank may soon add ultra-long debt to its asset-purchase stimulus scheme.

About 16.5 billion euros of orders were placed for the bond – 5-1/2 times the expected sale amount, despite concerns over Italy’s banks and an upcoming referendum that could unseat its prime minister.

Many of the fund managers who lend to Italy – and those who have already bought 50-year bonds from France, Belgium and Spain this year – may not live to see it paid back. Those who signed up to Ireland’s 100-year bond in March almost certainly won’t.

But they could make quick gains if the ECB extends the maturity limit on its bond-buying scheme later this year, in an attempt to prolong its 1.7 trillion euro programme.

Analysts say such a move could be among tweaks expected in December to allow the central bank to continue quantitative easing beyond its scheduled end in March 2017.

“It is one of the least sensitive options from a political, technical and legal perspective,” said Frederik Ducrozet, senior European economist at Swiss wealth manager Pictet.

For those not familiar with Italy, a good place to start is the Wikipedia list of Italian prime ministers. Spoiler alert: They’ve had a million of them, and few have lasted more than a couple of years. This is the quintessential ungovernable society.

Meanwhile, its banks are pretty much zombies, loaded with fatal levels of bad debt but still shambling around thanks to repeated bailouts. The government runs consistently excessive deficits, so its debt load is growing at an unsustainable rate. And its people are more worried about protecting antiquated labor and tax regulations than competing successfully in a modern global economy.

And yet bond investors love the country’s debt. The reason, as the above article explains, is that no one thinks of these bonds as Italian. Once the ECB buys them up (at a nice premium to the initial sale price) they’ll become, in effect, German debt, guaranteed, via the ECB, by that much stronger, better managed economy.

So in the minds of bond buyers they’re not lending money for 50 years, but more like six months, until the ECB starts snapping them up. Which means the ECB is, in effect, directly funding the Italian government with newly-created Euros. Italy – and the rest of the peripheral eurozone countries – are thus handed an effectively-unlimited credit card allowing them to spend whatever they want, safe in the knowledge that it’s all covered by their friends in Brussels and Berlin.

Wonder how they’ll handle that freedom?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair