Timing & trends

The lack of integrity among the press is becoming just in your face. The New York Times published an amazing endorsement of Hillary Clinton on Saturday in hopes that they can persuade their readers to overlook all the scandals of Hillary and make her President. I would understand not endorsing either, but to ignore the law, the corruption, and common sense, merely reveals that the New York Times cannot be trusted. This is even more astonishing from the standpoint that the New York Times was the paper to break the story on Hillary’s emails on March 2nd, 2015. It was also the New York Times that published “2008 Crisis Deepened the Ties Between Clintons and Goldman Sachs”explaining how Hillary came to help rescue their image. It was the New York Times that reported how Hillary kept changing her story on the emails. To simply ignore all of this as if it never happened leaves one speechless at the political attempt to manipulate the public. This is what the New York Times actually wrote in their endorsement:

The lack of integrity among the press is becoming just in your face. The New York Times published an amazing endorsement of Hillary Clinton on Saturday in hopes that they can persuade their readers to overlook all the scandals of Hillary and make her President. I would understand not endorsing either, but to ignore the law, the corruption, and common sense, merely reveals that the New York Times cannot be trusted. This is even more astonishing from the standpoint that the New York Times was the paper to break the story on Hillary’s emails on March 2nd, 2015. It was also the New York Times that published “2008 Crisis Deepened the Ties Between Clintons and Goldman Sachs”explaining how Hillary came to help rescue their image. It was the New York Times that reported how Hillary kept changing her story on the emails. To simply ignore all of this as if it never happened leaves one speechless at the political attempt to manipulate the public. This is what the New York Times actually wrote in their endorsement:

“In any normal election year, we’d compare the two presidential candidates side by side on the issues. But this is not a normal election year. A comparison like that would be an empty exercise in a race where one candidate — our choice, Hillary Clinton — has a record of service and a raft of pragmatic ideas, and the other, Donald Trump, discloses nothing concrete about himself or his plans while promising the moon and offering the stars on layaway. (We will explain in a subsequent editorial why we believe Mr. Trump to be the worst nominee put forward by a major party in modern American history.)”

To call Trump the “worst nominee put forward by a major party in modern American history” is just astonishing and leaves one with their mouth wide-open. Emails, corruption, Clinton Foundation taking money from foreign governments when Hillary is Secretary of State all means nothing. If this is honorable showing trustworthiness, then the old saying people judge others by themselves means this is what the New York Times also thinks is acceptable. This endorsement is clearly a desperate attempt by the ESTABLISHMENT to rig the election just as the media did in Britain to convince the people they should surrender their dignity to Brussels. There too the press predicted a major depression and collapse of Britain if they people voted to exit Europe. Nothing of the sort has unfolded and the scare tactics of mainstream media in that instance was deplorable. Goldman Sachs, Morgan Stanley and Credit Suisse have all had to revise their forecasts that called for the end of the world if BREXIT passed.

The New York Post has said it best. This election has captured in their bold headline: American journalism is collapsing before our eyes. Indeed, this is the end of mainstream media. If Trump wins, this victory may see the decline and fall of mainstream media once and for all. As the younger generation abandon such media, even Warren Buffett has said he would only invest in local community newspapers. USA Today has been offering buy-outs for employees with over 15 years on the job who are 55 or older to reduce the work force.

The New York Post has said it best. This election has captured in their bold headline: American journalism is collapsing before our eyes. Indeed, this is the end of mainstream media. If Trump wins, this victory may see the decline and fall of mainstream media once and for all. As the younger generation abandon such media, even Warren Buffett has said he would only invest in local community newspapers. USA Today has been offering buy-outs for employees with over 15 years on the job who are 55 or older to reduce the work force.

TV began to displace newspapers with their nightly news programs and coverage of political debates live. That started the process of the decline and fall of newspapers. Now the internet is here and the younger generations do not buy newspapers. The lifeblood of media has been advertising revenue. That has turned the tide. There is a growth of 15.7% in advertising revenue, but it is all on the internet with not increases appearing for TV or newspapers. This biased and foolish endorsement of Hillary by the New York Times has simply exposed that they are part of the ESTABLISHMENT and this is really what is under attack in these elections on a global basis. It is like supporting Napoleon in the Battle of Waterloo on that fateful day of June 18th, 1815.

….also Michael’s Editorial: Oh No Not Again

Dr. Faber played a game of Long & Short, where he spelled out his view on central banks, currencies and commodities, among other items. Then, he gave probabilities on a number of possible world events and explained his reasoning.

The U.S. will go into a recession by 2020

The U.S. will go into a recession by 2020

A: 100% probability. We are in a lengthy expansion already, far above the average expansion in the 20th century. We have a lot of imbalances, in my view a recession is inevitable. But unlike central banks, I do not regard a recession as negative. It’s like the human body, an economy also needs a resting period occasionally to adjust. A recession is not something that has to be avoided at all costs.

The European Union will break up by 2020

A: 80%. Economically, the EU would probably will break up. But it’s also a political issue as there may be lot of political obstacles to complete a split from the EU. Some countries like Austria or France would like to split from the EU, but if they could do it in practice is not entirely clear to me.

….also: Marc Faber Rings the Alarm Bell, Predicts a 50% Near Term Correction in Stocks

The Bank of Japan gave us a glimpse as to just how far down the rabbit hole we may have to follow global policy makers as we try to make sense of ever more complex and shall we say, innovative ‘tools’ being used in the effort to engineer individual economies and asset markets within the global financial system. BoJ announced it would conduct “JGB purchase operations” in order to “prevent the yield curve from deviating substantially from the current levels”.

The market initially interpreted this to mean BoJ stood in support of a rising yield curve, which would for example, help the banks (ref. MTU and SMFG, which exploded higher off of the support levels we had projected), but by the end of the week the Japanese Yield Curve had eased substantially and there seemed to be confusion about what the policy’s intent, or would-be effects, actually were. I wonder if the BoJ even fully knows what it is doing now. Lots of moving parts in a complex system.

As for the FOMC, it was non-business as usual. For all the pomp and bluster of the August-September Jawbone blitzkrieg we’ve been subjected to, the damn committee simply rolled over again, admonishing through hints that they really, really mean it when they imply a rate hike is still coming in 2016. But for now and to the surprise of very few, they did what they have done for the last 8 years; obfuscate and delay.

This time we even saw renowned dove Eric Rosengren rightly (in my opinion) shifting to the hawk side of the table as he observes a landscape of cranes to nowhere in Boston and extrapolates… ‘hmmm, I think we are blowing an asset bubble’. Yet still, the committee chaired by Janet Yellen – she of the hawk-tinged Jackson Hole Jawbone (with handy QE “tools” in her back pocket) went on to vote NO HIKE despite elevating CPI and soaring real estate, healthcare and services costs. Also, let’s not forget the ‘near all-time highs’ stock market, which unsurprisingly got an across the board price surge in response.

Where to now? Speaking as a lowly participant, I gave my stance in Friday’s in-day market update (profit retention). As you will see in this week’s report, weekly US stock market charts remain just fine, as we have noted for months now. But the daily charts of NDX and SPX used in the update gave some parameters to shorter-term correction potentials. What’s more, the global macro is a confusing mess. Japan took confusion to a new level last week, but the US is also a Wonderland of its own, post-2008.

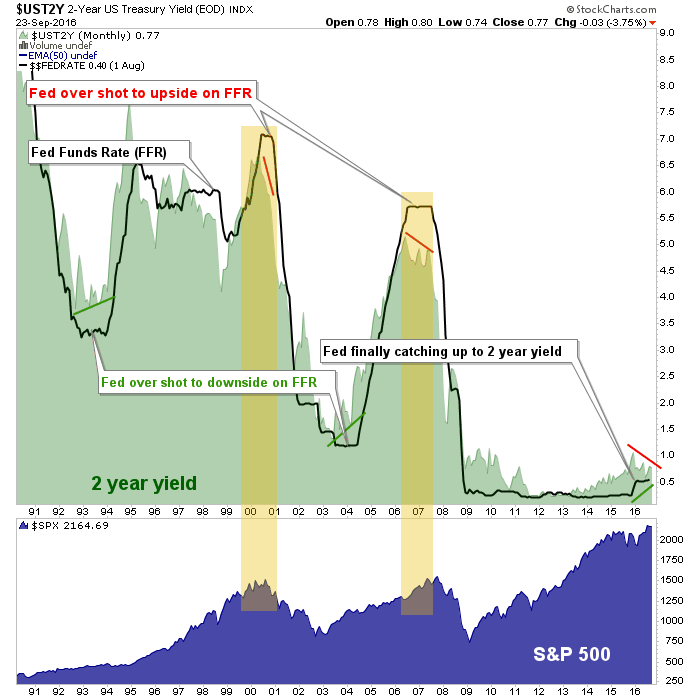

The chart above asks whether we are at a time like 1993/94 and 2003/04 or a time like 2000/01 and 2007/08. The interplay between the Fed Funds Rate (FFR) and the 2 year Treasury yield is – in my opinion, due to unprecedented bond market meddling under the Bernanke Fed – now dysfunctional.

Declining in 2016, the 2 year has been acting like it does at important economic and stock market tops, but Fed policy has not caught up to and exceeded the 2 year. We have long noted that the Fed decides nothing; the bond market makes the decisions. Yet the 2 year has been rising since 2013 and only in December of 2015 did the Fed decide to start to get in line with the message. Ever since then the 2 year yield has been declining, as it does at market tops, and this assuredly factors into the FOMC’s dovish rollovers.

Yet the starting point of this process is unlike any that came before. In 2000 the process began with yields above 6%. In 2007, above 5%. Today? 1% on the 2 year and .5% on the FFR. Those data points are lower than even the bombed out post-recession levels of 1992/93 and 2003, which preceded new cyclical bull markets.

Did someone say “confusing”? Did someone imply that even the likes of the Fed and the BoJ are confused? Did someone name a market report and associated service after the story of Alice in Wonderland during the lead-in to Q4 2008, when so many of the distortions built into the system were first introduced? I make a big deal about “playing it straight”, i.e. using the indicators and market signals for what they tell us, not what our most closely held views (biases) want them to tell us. But there is a highly technical term we can use for the chart above; it’s all screwed up.

Now there is little going on in macro markets that is conventional, and because of that it is difficult if not impossible for conventional analysts, quants and various other data miners to extrapolate forward in any accurate way. If the process noted above were coming from, say, 3.5% to 4% yield levels it would be easy to call it a ‘high risk, sell stocks’ atmosphere because all the ducks would be lined up and we would be believing the Fed when it poops rising interest rates talk out of its orifice. We could then expect the typical over shoot and ensuing bear market. I think that is what is coming, but the timing – in line with continual ‘obfuscate and delay’ of the Fed, is what is in question.

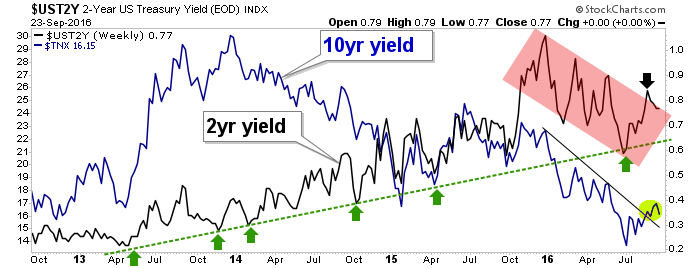

The chart above shows the ongoing 2016 downtrend in the 2 year yield. That is the plan that the Fed is following. Notice the big spike in October/November 2015? Notice the single Fed Funds Rate hike in December of 2015? Ever since then the 2 year has trended down and so the Fed has stood down. They ramp up the tough talk however when the dupes on the long end of the curve begin to get unruly. As noted recently, the 10 year yield broke its downtrend. About the only ones who would like that are the Banks, pigs that some of them are [insert Stumpf photo and time-wasting belly aching here].

A rising yield curve is not what is happening yet, however. But if it were to happen confidence in the Federal Reserve would take another hit. So for now they ‘tough talk’ the bond market, holding that massive would-be .25% rate hike over our heads.

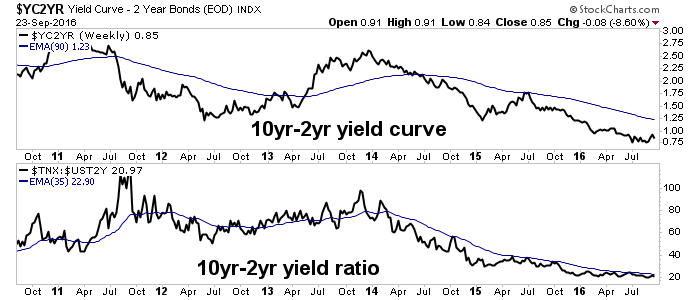

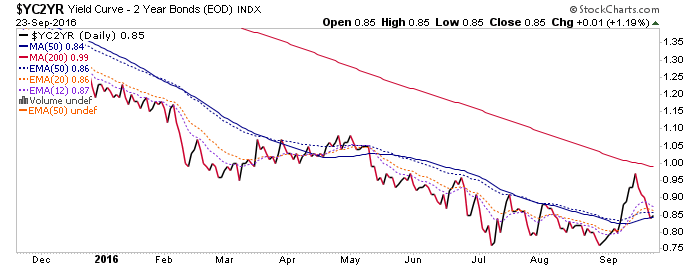

I think they’ll probably raise in December if the markets do not fall apart in the interim. They do have a bit of wiggle room before they overshoot the 2 year per the first chart above. Another hike would give them a second little nugget of credibility. But if long-term yields resume climbing at any point, the message would be inflationary and the Fed may have to chase the curve higher. If on the other hand, yields do not resume upward we’ll have seen the last rate hike in a long while. Here’s the daily yield curve; it is no wonder Fed sensitivities got stoked in September. Last week it was tamped back down.

….also: Hot Properties: Where Did Vancouver Scare Foreign Money To?

NFTRH.com and Biiwii.com

There were some hopes that a non-move by the Fed would end the current correction in precious metals and spark a move to new highs. Unfortunately, the Federal Reserve cannot override the supply and demand component of the market. Gold and gold stocks popped higher but less than two days later the sector (and specifically the miners) has given those gains back. That tells us plenty of sellers remain and this sector needs more time and perhaps lower prices before this correction ends.

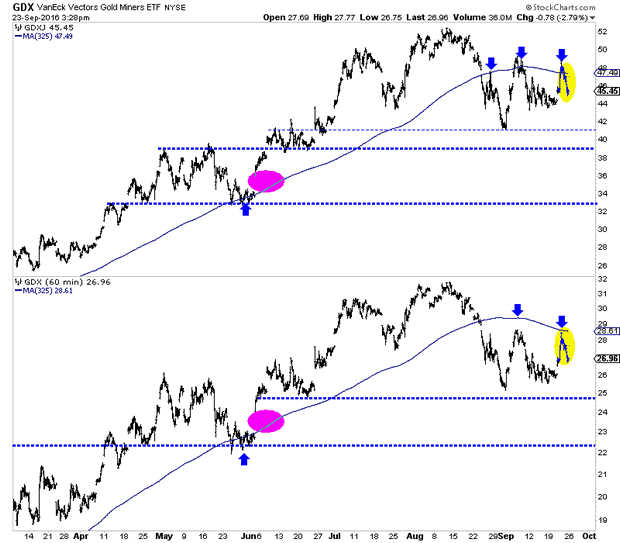

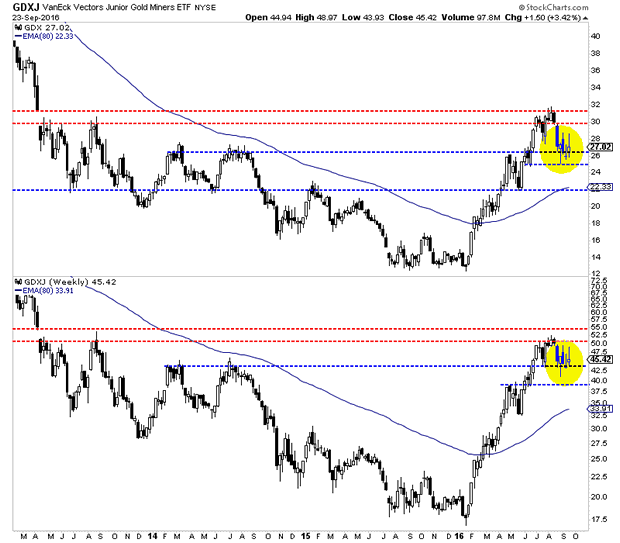

The hourly charts, seen below show the miners selling off after testing their 50-day moving averages. GDX showed a bit more strength on this pop as it reached its 50-dma before retreating. GDXJ nearly touched $49, which is within 10% of the recent high before reversing those gains quickly. The miners could test recent lows before retesting their 50-day moving averages.

The weekly charts indicate the correction can be deemed bearish consolidation. The candles from the past three weeks have not been remotely bullish. The miners had one solid down week followed by two weeks in which the market failed to hold its gains. GDX (top) has key support at $25 while GDXJ (bottom) is trying to hold above $44. Weekly closes below $26 and $44 could usher in more losses in the short-term.

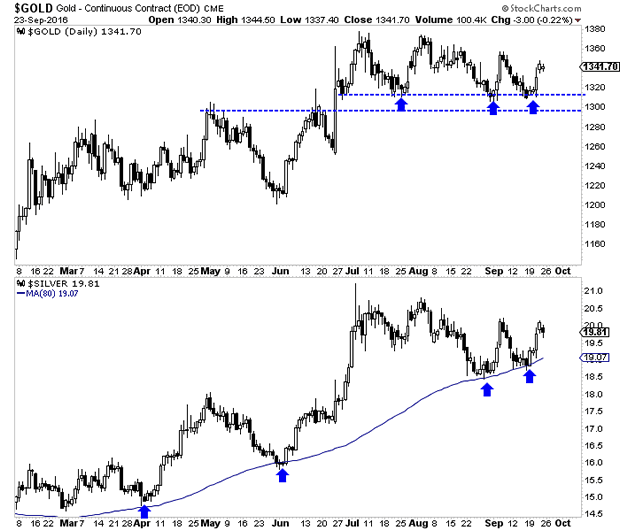

Turning to the metals, we find more encouraging signs as Gold and Silver have maintained support quite well. The daily candle charts for Gold and Silver can be seen below. For the third time in the past few months Gold was able to hold support at $1300-$1310. Meanwhile, Silver held its August low and has shown more strength than Gold recently. That is positive.

The precious metals sector remains in correction mode but the longer the sector can hold and digest recent gains without significant price deterioration then the more likely a bullish outcome becomes. The strength in the metals is a healthy sign but the relative weakness in the miners and failure to hold gains is a signal that the correction will definitely continue in terms of time. Traders and investors should wait for either this market to become oversold or the correction to mature. In the meantime, focus on the opportunities scattered amongst individual companies rather than the sector itself.

Jordan’s premium service

….related: Gold Stocks: The Money Stick Play

It looks like the foreign buyers tax has put the breaks on Chinese buying in vancouver – but the big question is where will the money go now. Ozzie on some of the actual numbers in reaction to the foreign buyers tax. Also this weeks “Hot Properties”.

Michael Campbell’s Editorial: Oh No Not Again

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair