Asset protection

I’ve been saying for the past couple years that the next recession here in the US will probably be triggered by an external macro event or cascade of events, coming out of Europe or China. Today’s Outside the Box sharpens our focus on China, which had already got quite a lot sharper with Michael Pettis’s piece in Outside the Box on Sept. 2.

I’ve been saying for the past couple years that the next recession here in the US will probably be triggered by an external macro event or cascade of events, coming out of Europe or China. Today’s Outside the Box sharpens our focus on China, which had already got quite a lot sharper with Michael Pettis’s piece in Outside the Box on Sept. 2.

Today’s post comes from Ambrose Evans-Pritchard of the London Telegraph. He is commenting on the recently released quarterly report of the Bank for International Settlements (“the central banks’ bank”), in which the BIS repeats Pettis’s warning that China faces escalating risk of a major debt and banking crisis.

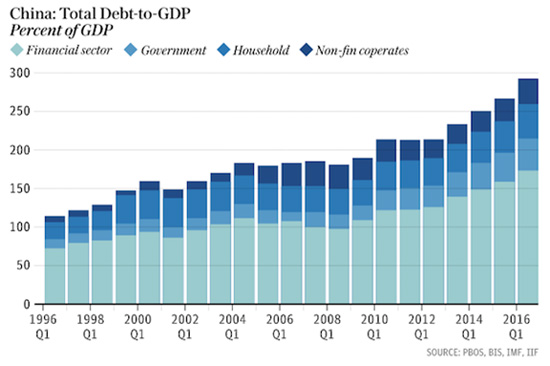

The BIS is also rightly concerned about spillover from China to the global economy. After noting that outstanding loans in China have reached $28 trillion – as much as the commercial banking loan books of the US and Japan combined – Ambrose adds, “The scale is enough to threaten a worldwide shock if China ever loses control. Corporate debt alone has reached 171pc of GDP, and it is this that is keeping global regulators awake at night.”

Total Chinese debt reached 255% of GDP at the end of 2015, a jump of 107% in the past eight years – and still rising fast. Every year, China’s leadership promises to rein in debt growth, and every year the growth just keeps accelerating. That is because China’s GDP growth is fueled by debt, and that debt is becoming increasingly inefficient in producing GDP.

Does China still have the resources to deal with this issue? The answer is a qualified yes – but then there may not be the resources to deal with the other little items on China’s shopping list. The New Silk Road that China seems to be actually in the process of building is estimated to cost $1 trillion, and that’s without cost overruns. Plus, the Chinese leadership has promised massive spending on the interior part of the country to bring up the quality of people’s lives there.

One trillion here and one trillion there, and pretty soon you have run through your reserves and are getting into monetization problems; and then you have all sorts of currency and related issues, not to mention potential inflation, unemployment, the slowing of the economy, the associated public unrest, and so on.

No, I do not think China is going to massively implode, but the world is really not ready for a China that is only growing at 2% or 3% a year. (Even though 2–3% growth would sound pretty good if it was happening in the US.) That will feel a lot like a hard landing as far as world growth is concerned. All happening when there are unsettled political agendas in a number of countries (starting with this one) with regard to globalization and trade treaties.

I am back in Dallas after spending the past few days with Shane in Denver. I got to catch up with David Rosenberg and Mark Yusko and have lunch with George Will. George, who is normally upbeat as he looks to the future, spoke after lunch at the conference and delivered one of the most depressing speeches I have heard in a long time. He was just not in a good mood. I should have tried to engage him on baseball, and the afternoon might have been more enjoyable.

Have a great week and savor the last few days of official summer.

Your seeing global risk everywhere he looks analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

Get John Mauldin’s Over My Shoulder

“Must See” Research Directly from John Mauldin to You

Be the best-informed person in the room

with your very own risk-free trial of Over My Shoulder.

Join John Mauldin’s private readers’ circle, today.

China facing full-blown banking crisis, world’s top financial watchdog warns

By Ambrose Evans-Pritchard

Originally published in the Telegraph, Sept. 19, 2016

China has failed to curb excesses in its credit system and faces mounting risks of a full-blown banking crisis, according to early warning indicators released by the world’s top financial watchdog.

A key gauge of credit vulnerability is now three times over the danger threshold and has continued to deteriorate, despite pledges by Chinese premier Li Keqiang to wean the economy off debt-driven growth before it is too late.

The Bank for International Settlements warned in its quarterly report that China’s “credit to GDP gap” has reached 30.1, the highest to date and in a different league altogether from any other major country tracked by the institution. It is also significantly higher than the scores in East Asia’s speculative boom on 1997 or in the US subprime bubble before the Lehman crisis.

Studies of earlier banking crises around the world over the last sixty years suggest that any score above ten requires careful monitoring. The credit to GDP gap measures deviations from normal patterns within any one country and therefore strips out cultural differences.

It is based on work the US economist Hyman Minsky and has proved to be the best single gauge of banking risk, although the final denouement can often take longer than assumed. Indicators for what would happen to debt service costs if interest rates rose 250 basis points are also well over the safety line.

China’s total credit reached 255pc of GDP at the end of last year, a jump of 107 percentage points over eight years. This is an extremely high level for a developing economy and is still rising fast .

Outstanding loans have reached $28 trillion, as much as the commercial banking systems of the US and Japan combined. The scale is enough to threaten a worldwide shock if China ever loses control. Corporate debt alone has reached 171pc of GDP, and it is this that is keeping global regulators awake at night.

The BIS said there are ample reasons to worry about the health of world’s financial system. Zero interest rates and bond purchases by central banks have left markets acutely sensitive to the slightest shift in monetary policy, or even a hint of a shift.

“There has been a distinctly mixed feel to the recent rally – more stick than carrot, more push than pull,” said Claudio Borio, the BIS’s chief economist. “This explains the nagging question of whether market prices fully reflect the risks ahead.”

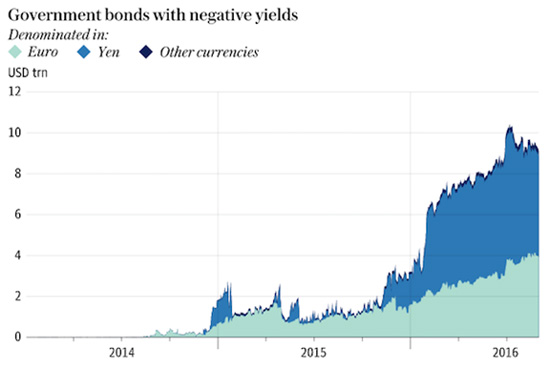

Bond yields in the major economies normally track the growth rate of nominal GDP, but they are now far lower. Roughly $10 trillion is trading at negative rates, and this has spread into corporate debt. This historical anomaly is underpinning richly-valued stock markets at time when profit growth has collapsed.

The risk is a violent spike in yields if the pattern should revert to norm, setting off a flight from global bourses. We have had a foretaste of this over recent days. The other grim possibility is that ultra-low yields are instead pricing in a slump in nominal GDP for years to come – effectively a trade depression – and that would be even worse for equities.

“It is becoming increasingly evident that central banks have been overburdened for far too long,” said Mr Borio.

The BIS said one troubling development is a breakdown in the relationship between interest rates and currencies in global markets, what it describes as a violation of the iron law of “covered interest parity”.

The concern is that banks are displaying a highly defensive reflex, and could pull back abruptly as they did during the Lehman crisis once they smell fear. “The banking sector may become an amplifier of shocks rather than an absorber of shocks,” said Hyun Song Shin, the BIS’s research chief.

This conflicts with what the Bank of England has been saying and suggests that recent assurances by Governor Mark Carney should be treated with caution.

Yet it is China that is emerging as the epicentre of risk. The International Monetary Fund warned in June that debt levels were alarming and “must be addressed immediately”, though it is far from clear how the authorities can extract themselves so late in the day.

The risks are well understood in Beijing. The state-owned People’s Daily published a front-page interview earlier this year from a “very authoritative person” warning that debt had been “growing like a tree in the air” and threatened to engulf China in a systemic financial crisis.

The mysterious figure – possibly President Xi Jinping – called for an assault on “zombie companies” and a halt to reflexive stimulus to keep the boom going every time growth slows. The article said it is time to accept that China cannot continue to “force economic growth by levering up” and that the country must take its punishment.

One bright spot is a repayment of foreign debt denominated in dollars. Cross-border bank credit to China has fallen by a third to $698bn since peaking in late 2014 as companies scramble to slash their liabilities before the US Federal Reserve raises rates. The tally for emerging markets as a whole has fallen by $137bn to $3.2 trillion.

China’s problem is internal credit. The risk is that a fresh spate of capital outflows will force the central bank to sell foreign exchange reserves to defend the yuan, automatically tightening monetary policy. In extremis, this could feed a vicious circle as credit woes set off further outflows.

The Chinese banking system is an arm of the Communist Party so any denouement will probably take the form of perpetual roll-overs, sapping the vitality of economy gradually.

The country was able to weather a banking crisis in the late 1990s but the circumstances were different. China was still in the boom phase of catch-up industrialisation and enjoying a demographic dividend.

Today it is no longer hyper-competitive and its work-force is shrinking, and time the scale is vastly greater.

For the last several months, I’ve been putting up with some hate mail, as I forecast a severe decline in the precious metals. Questions came into my mailbag like …

– “Don’t you see the negative interest rates in Europe, surely they are bullish for gold?”

– “Don’t you see that George Soros and other big hedge fund managers are loading up on gold? What’s with you, Larry?!”

– “China and India are still buying gold so that must be bullish, no?”

– “One well-known analyst says the dollar is going to crash on September 30 so we must buy gold now, Larry!”

Let me address the above, and more, so you have a handle on why I’ve been bearish gold and silver — and correct!

FIRST, negative interest rates are not necessarily bullish for gold. Or silver. Why? Because you cannot spend gold and silver as if it’s real money. Hardly a soul will take it except an informed buyer, and in a barter situation.

The fact of the matter is this: People are hoarding cash in physical and digital form far more than they are hoarding gold and silver. They are doing so because …

A. It’s easier to hoard cash.

B. With deflation still ravaging Europe, that cash’s purchasing power is constantly increasing.

C. It IS easier to spend cash.

And more. So in a very real sense, gold is no longer money. A store of value? Yes, but only when governments’ backs are up against the wall. And that time is coming. But for now, gold and silver are simply commodities.

SECOND, don’t you see that George Soros and other big hedge fund managers are loading up on gold? What’s with you, Larry?! Sure I do, and I also saw them get KILLED when gold topped in September 2011 and they held on to their gold and incurred losses of 50% and more.

Just because they manage big money doesn’t mean they can’t get a trade wrong sometimes. In fact, they get them wrong far more often than you would imagine.

THIRD, China and India are still buying gold so that must be bullish, no? Yes, they are still buying, but so what?! Neither country has any intention of implementing a gold standard. They are simply diversifying their reserves a bit, just like you should be doing with your savings.

FOURTH, one well-known analyst says the dollar is going to crash on September 30 so we must buy gold now, Larry!

This one is total, unadulterated BS. This analyst has been wrong forever on the dollar and doesn’t have a clue how the world’s monetary system works or the global economy.

His theory is that the International Monetary Fund (IMF) is going to officially add the Chinese yuan to the IMF’s composition of its Special Depository Receipts, or SDRs, on September 30 and therefore, the dollar will crash.

Give me a break!

A. The yuan was approved by the IMF for inclusion in the SDRs a year ago. That means the dollar market has already had a year to digest it. And what has the dollar done since then? Appreciated against the Chinese yuan.

B. The yuan only accounts for about 4% of all of foreign exchange (forex) transactions today, which are well over $5 trillion a day. Meanwhile, the U.S. dollar accounts for as much as 85% of daily forex turnover.

How could the yuan even make a scratch in the dollar?

C. The yuan doesn’t have the liquidity or the market depth to dethrone the dollar. There are still capital controls in China on how much yuan can leave the country and it’s still largely a closed system.

C. The yuan doesn’t have the liquidity or the market depth to dethrone the dollar. There are still capital controls in China on how much yuan can leave the country and it’s still largely a closed system.

For instance, I have about $500 worth of yuan I forgot to change back to dollars the last time I was in China. I can change them to dollars in Southeast Asia, but due to a lack of liquidity, it will cost me as much as 20%.

And in the U.S? Forget it. Try converting yuan to dollars or vice versa. If you’re lucky, you might be able to do so at JFK, LAX or Chicago — but it will cost you a fortune.

D. Did this analyst even consider the fact that there’s plenty of legal and illegal Chinese money that wants to leave China, for diversification and whatever reason?

From what I can tell, no, he hasn’t. And that’s a big, biased mistake because there’s hundreds of billions of wealthy Chinese money that also wants to go abroad to invest, and mainly in the U.S. — buying businesses and real estate.

Bottom line: The U.S. dollar is NOT headed for any type of crash. To the contrary, my models show the dollar getting much stronger going forward — regardless of who takes the White House come November.

Why? Largely because Europe and the Middle East are such a mess. Anyone with any decent money would want to put it to work in the U.S., which means demand for dollars will continue to rise, even amongst the Chinese and Southeast Asians.

There really is no alternative at this time.

However, as I have also long maintained, the U.S. dollar cannot be the largely sole global reserve currency and the world’s reserve currency must change to a basket of currencies that is far more fair to the G-20.

That change will come by 2020, and it will involve the IMF or the World Bank. The new world reserve currency will be a composition of currencies of the G-20, it will be solely in electronic form, and it will be tied to a floating basket of commodity values.

That way, it will be not only transparent and fair but also subject to free market forces.

And by the time that transition comes, there may be some turmoil in the forex markets, but even then, the dollar will not crash.

Bottom line: Don’t fall for all the fear-mongering on the dollar. It’s coming from either inept analysts or fear-mongers trying to pick your pockets.

Lastly, keep your eyes on gold and silver now. Cycles still point lower into early October, they point higher for the dollar, and lower for stocks.

October is merely two weeks away, so stay very tuned in. My Real Wealth Report subscribers and trading service members are now starting to get very active with specific buy and sell signals for terrific profit opportunities.

Stay tuned and stay safe!

Best wishes,

Larry

The energy complex are trading higher after the EIA released its latest weekly oil inventory report. The data showed Total Crude & Product stocks decreased by 6.034/mmbls to 1390.917/mmbls for week ending Sept. 16. Looking at the year-on-year for Total Crude & Product stocks we see we are now 93.2/mmbls above last year’s level for this time of the year and above the five-year average by 242.9/mmbls.

…related:

Perspective

This week’s harvest of headlines records a lot of hope in the crude oil markets as well as remarkably reckless borrowing. Matched, of course, by the equivalent in lending.

All without a regard for how the debt will be serviced. Financial history is at the point where the real power shifts from the Federal Reserve System to Mister Margin. It has many times since 1913 and since the advent of reckless central banking the roles of each side have become very distinct.

The Fed’s ambition is to get the accounts fully leveraged or “out of line”. This has been impressive. Mr. Margin’s job description is to get the accounts “in line” and that will be done.

It could take until November.

The following is part of Pivotal Events that was published for our subscribers September 14, 2016.

Stock Markets

Market dynamics have been outstanding. Outstanding in setting a series of important tops, perhaps adding up to “Peak” for the senior indexes and a big “Rounding Rebound” for the broad market.

Our case has been is that central bank equity buying had to focus upon the big stocks— the “Nifty 500”.

With so many central banks buying the popular trades, Long Term Capital Management (LTCM) comes to mind. It was in 1998 and LTCM had an outstanding reputation in theoretical pricing of options. So outstanding, that senior central banks made direct loans to the highly leveraged fund. The Bank of Italy did this and took an equity position as well.

The wager was that with the European Union, credit spreads would narrow. That was the theory. We pointed out that even with the serious discipline of a gold standard spreads did not narrow to a common level.

On a natural turn to widening that summer LTCM was suddenly and irrevocably offside. It lost $4.6 billion in less than four months.

The fund collapsed to effectively less than zero and the distress amongst the central banking community was palpable. This added to the overall panic.

Now there are many central banks that are very long, as we note, the popular trades, including equities.

“Come on in – all the lemmings are doing it!”

In 2000 and 2007, the Street stayed long because the Fed would “cut rates”. This is not an option now, so the equivalent mojo is that central banks will “buy more assets”.

Rather an interesting evolution of the “Greater Fool” theory.

As with previous market peaks, credit strains are becoming visible and are forcing stock markets down.

How far?

It will take a cyclical bear to clear the financial excesses.

The hot leading sectors accomplished speculative excesses that were noted as they occurred.

The action in Utilities (XLU) climaxed in early July. Base and Precious Metal Miners (XME and HUI) at the end of July. All three are breaking down.

Over in the financials, last week we noted that the action in XLF has registered an Upside Exhaustion as well as a Sequential Sell. Enough technical excess to call for another “Widows & Orphans Short”. The last one was in July last year and mainly based upon the action in Wells Fargo.

BKX fell from 80 to 53 in February and has rallied up to 72. The recent technical readings are more comprehensive than last year’s.

Transports did not confirm the Dow high and have slipped below the 50-Day moving average at 7854. Now at 7771, through the 200-Day at 7624 would turn the chart down.

On the broad market, the NYA did not set new highs and we have been watching the 20- Week ema. This is at 10568 and with the index at 10505 today, the break is significant.

The equity wager now is not on a “Fed cut”, but that central bank promises to buy assets will be effective.

Currencies

Once again it is time to review the theory that currency depreciation is the mojo for economic growth. And when that theory is faltering depreciation becomes the preventer of bad things.

Of course, veteran traders have never really gone along with this.

The most glaring thing out there is that the theory has never worked. Now it is becoming more apparent.

The question has always been. When do the Federales learn to doubt?

The next dollar rally may instruct.

Since the first of August, the DX has been in a trading range between 94 and 96.25. The last low was last week at 94.39. At 95.50 now, there is resistance at the 96 level which is between the 50 and 200-Day moving averages.

Technically, the DX needs to get above the 20-Week ema to start the rise. This would be similar to the “launch” in July 2014.

It got slightly above last week and the ema is at 95.61.

Bonds

- Sequential Sells were generated going into the top.

- That was on the 9 and 13-Week readings.

- The 20-Week ema governed the corrections on the way down into late 2015.

- The same ema governed on the way up.

- Taking it out will formally turn the global treasury market down.

Ampersand

Been reading an interesting diary from the late 1700s.

Hazards of country life:

September 21, 1786

A Country Parson

James Woodforde’s Diary 1759-1802

“My Brother John indifferent to day being merry last Night and very near killed last Night going home from Ansford Inn to his own House on horseback and falling off – his face is cut but little however….”

On Travel:

October 11, 1786:

“Whilst we were at Newmarket and changing Coaches and Luggage, found that a small red Trunk of my Nieces was left behind in London, in which were all her principal Matters – It vexed her at first very much – but on my assuring her that I saw it safely lodged in the Warehouse, she was more composed. I would not pay the remaining part of our fare or for our Luggage till the Trunk was forthcoming….”

BOB HOYE, INSTITUTIONAL ADVISORS E-MAIL

bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

Listen to the Bob Hoye Podcast every Friday afternoon at TalkDigitalNetwork.com

Quotable

“If you don’t know where you are going, any road will get you there.” – Lewis Carroll

Commentary & Analysis

After the Bank of Japan (BOJ) did what it did, a boatload of economics Ph.D. descended on the airwaves and internet blogs this morning to share their usual inside baseball stuff in an effort to explain the “bold” move by the Bank of Japan—targeting the yield curve. But outside the minds of economists who actually condone such tinkering will any of this matter?

Japan has blazed the trail to zero rates and beyond. Suckers in Europe have followed because it has worked so well for Japan. This action on the part of the CBs begs the question: To what good have any of your policies done, short of providing liquidity to help stabilize the banking system and credit markets in the midst of the crisis? The BOJ has been at this game of ZIRP off and on (mostly on) for the last 20+ years. Growth in Japan is still morbid. Debt to GDP is off the charts. And deflation is still the order of the day.

Some seers are saying the BOJs decision not rely on increases in the money supply, and just maintain its current level of quantitative easing, is a hint to the Japanese government that monetary policy isn’t getting the job done and structural reforms are needed in order to change the economic trajectory.

To review, Prime Minister Abe was elected in December 2012. Upon taking office he enunciated a three arrow strategy in order to break the grip of deflation in Japan and grow the economy. These three arrows were: 1. the pressuring of Bank of Japan into launching unprecedented aggressive monetary easing and setting a target of 2% inflation to support a target of 2% real GDP growth (4% nominal growth); 2. a blowout deficit-financed supplemental government budget filled with new public works spending; and 3.

a program of reforms to achieve growth through stimulating private investment. The third arrow, the most important if you aren’t a hedge fund manager, is the most important. And so far this arrow hasn’t left the quiver.

Why? Simple answer: Crony capitalism doesn’t want real reform (Brexit a perfect summary of that.) Big business doesn’t want real competition. This is why CEOs of our major corporation are joined hand-in- glove with our political leaders. Big investors love the financial asset bubble; why make changes?

I am not sure if the BOJ is implicitly sending a message to the Japanese political class. But I do know it is past time all central bankers reach back and find their spines, assuming they ever had such a thing to begin with, and explicitly tell their respective governments—we can do no more. Financial repression isn’t working for most of our citizens; save those with access to capital. Is there any wonder why hedge fund manager extraordinaire Ray Dalio, and his cronies, are constantly creating all kinds of arguments why the Fed shouldn’t raise rates—“OMG, they can’t raise rates.” Hell, I think if Ludwig von Mises were pulling down a cool $500+ million a year, as did Dalio in 2015, he’d be all for financial repression too.

Add to this shit-show the fact no one yet understands the potential unintended consequences of negative rates. The prospect of an estimated $12 trillion in paper issued at negative rates is an anathema to a market system that allocates finite resources through proper price signals, and should terrify anyone with a logical brain cell left in their head.

Time for real structural reform, or to put it another way, time for Mr. Market to start clearing away the dead wood so fresh entrepreneurial growth can resume is way past due. That signal for the entrepreneur is sent first and foremost through the rate of interest (the signal now being sent to the market will be responsible, at some point, for the trillions of dollars in capital flowing straight down the rabbit hole). But instead of CBs doing what we know works (does anyone remember a man named Paul Volcker), let’s just keep stumbling along in monetary and fiscal wonderland, keeping those political contributors happy, and expecting everything to work out for the best. It’s such a grand idea it requires a Ph.D. in economics to understand it.

Thank you.

Jack Crooks

President, Black Swan Capital

www.blackswantrading.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair