Timing & trends

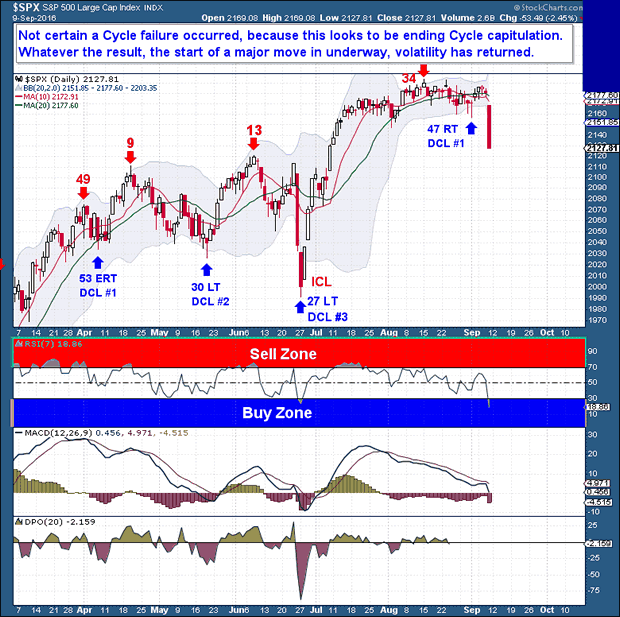

Friday’s 2% + decline in the equity markets was impressive. After a record run of low volatility and muted price action, equities suddenly awakened and exploded lower. This is exactly the sort of action I expected (although favoring upside price move) when I titled last week’s report Expecting Volatility. The market had been setting up for a big break for quite some time.

Extended periods of a lifeless, low volume trading range usually give way to volatility and significant moves in price. Going forward, at least over the short term, I expect we will see a series of 1% (plus or minus) moves in the daily indices. Although Friday’s break has significant bearish technical implications, it is too early to assume that the next extended move will be lower. What we canassume, and with a high degree of confidence, is that the next major market move has started.

The primary problem with being more definitive on direction is uncertainty around the Daily Cycle (DC). In a traditional DC (40-45 days), the low on September 1st – day 47 – could easily mark the DCL, especially with price subsequently jumping back above the 10 and 20-day moving averages. On the other hand, the September 1st low was not particularly deep, nor was the following rally of any real strength or duration. Further, a move back above the 10-dma was no big feat; the lack of a significant preceding drop and the sideways consolidation meant that the 10-dma bar was very low. Moreover, Friday’s drop appears to embody the sort of capitulation that we’d expect at the end of a DC.

For a number of weeks, I’ve maintained that a major market move was coming. Based on Friday’s action alone, I believe the move has started, so we need to be prepared for some serious volatility. The million-dollar question, of course, is whether the eventual move will be higher or lower.

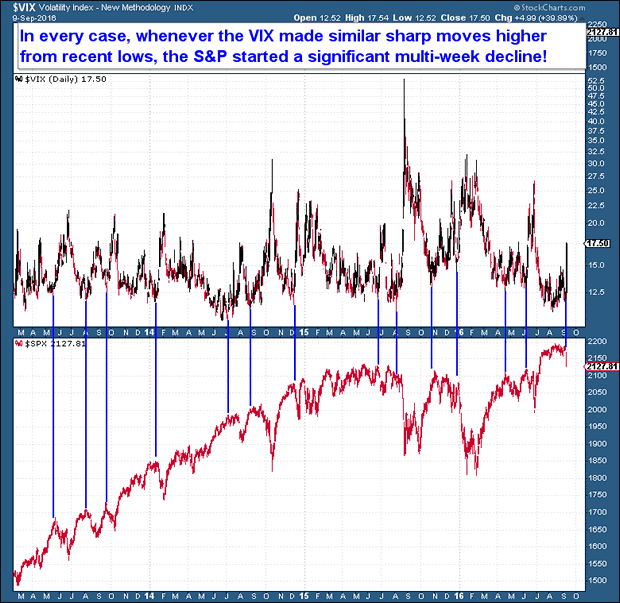

Turning to the VIX, my research uncovered an interesting, and potentially telling, relationship. Whenever the VIX reached a low and then spiked higher, it appears that a) volatility continued to expand, and b) the S&P topped and began a move lower toward a DCL or ICL.

If the above chart holds, we should probably assume that the markets have entered a corrective mode. That doesn’t mean that a major selloff is necessarily at hand, but we should expect a decline that spans more than just a single trading session.

So the Daily Cycle question becomes important. If we are seeing an extended Daily Cycle that capitulates for a few days before bottoming, the longer term move could be higher. On the weekly chart, we would likely see a back test of the breakout, with the rising 10-week moving average as the floor.

The bearish case, however, is a new Daily Cycle, one that will cascade lower out of the recent tight trading range. This would leave behind a very clear week-7 IC Top and a comfortably Left Translated IC that would have cyclical bear market implications.

An except from the Financial Tap Weekend Report – See here for more detail & a Full 14 day, no risk, money back Trial

….also:

SWOT Analysis: Are Gold and Silver Stocks the Best Area for “New Money Right Now”?

Quotable

“Surely nobody would be a charlatan, who could afford to be sincere.”

Ralph Waldo Emerson

There seems to be a lot of confusion about the US dollar reserve currency status. The biggest fallacy is the belief the US $’s reserve status bestows some great benefits on the US economy. It doesn’t. In fact it’s quite detrimental. I am penning this piece now because I noticed the snake oil salesmen (aka pundits and gurus who like to scare people using the dollar as their boogeyman) are out in force yet again.

In their never-ending series of dollar doom (DD) forecasts, predictions, confusions, hallucinations, lies, and manipulations (I will let you pick which of the words you wish to attach to your favorite double-D guru) I must say the latest incarnation they are peddling from the back of their wagon is a real whopper.

The DD punditry is now providing not only a specific reason why (“world money” will replace the dollar), but an exact date (the end of this month) to their crystal-ball-ology. I am not making this up— really. Of course the go to trade, once again, is gold. $10,000 an ounce on the way…again!

I’d like to share a few reality bites in effort to help you understand why you need not fear the Charlatan Choo-Choo of DD which seems to be racing down the tracks of gullibility…

Rationale/Fallacy #1: The dollar will be confiscated by international authoritieswho will be issuing “world money” and sending dollars back to the US in shipping containers. LOL…Now seriously, if I have to explain why this is total crap, you shouldn’t be wasting your time reading Currency Currents anyway. And don’t think this forecast is based on some miraculous issuance of International Monetary Fund Special Drawing Rights (SDR). SDRs are a claim on currency (they are not currency); and there is only a miniscule amount available anyway relative to the needs of the global monetary system. And guess what: The US dollar is the largest weight of the currency basket on which said SDRs are based. [Could one-day the SDR play a bigger role in the global monetary system? You bet. Is that one-day anytime soon? No way, as evidenced by the complete fecklessness of the G-20. Would a bigger role for the SDR be bad for the US economy—nope…in fact it would be very good for the US economy, which leads us to fallacy #2…

Rationale/Fallacy #2: The US dollar world reserve currency status will be challenged. This is one of the most consistent “go to” snake oil salesman rationales in the book. Every DD worth his weight in yuan pulls this one out of their basket of confusion when needed. But then again, most of the PhD’s in economics buy into this fallacy (no surprise there I guess).

Let’s use the US-Chinese relationship as our standard for understanding the detrimental role of the reserve currency at it relates to excess foreign reserves invested in US Treasuries:

Remember these key contentions. Foreign buying of US Treasuries…

-

Doesn’t help out the fiscal deficit in the US, but in fact makes it worse.

-

Doesn’t help push interest rates in the US down, but in fact pressures rates higher if anything.

-

Doesn’t help US employment, but in fact hurts it.

Okay, here we go with the example, I will do this in bullet point format in order to help simplify because it is confusing (balance of payments accounting is supposed be so simple):

-

China has excess savings and it shows up in its current account surplus as such. (Now we need to make a clear distinction between a country’s savings and individual savings—they are two different animals). Excess savings is another way of saying production exceeds consumption; or domestic demand cannot handle all the production therefore China has to find it elsewhere. Thus, China exports these savings in the form of purchasing US Treasuries, as said in order to grab demand from the US.

-

So let’s look at the equation….

– China buys US$’s; then buys US Treasuries with those dollars…

– $ buying by China forces up the relative value of the US$ compared to the Chinese yuan.

– An appreciating US$ (and falling Chinese yuan) tends to put downward pressure on US manufacturing, as the goods manufactured become relatively less competitive …

– Pressure on manufacturing puts downward pressure on employment, i.e. it increases unemployment and it in turn creates a feedback loop of lower relative investment from manufacturers in the US.

• Now, one of two things can happen:

- Chinese investment in Treasuries can be borrowed by businesses for investment purposes and to a degree negates impact of a lower dollar on employment; i.e. business investment creates new jobs (a positive outcome). But, as indicated above, this doesn’t usually happen because the rising US dollar makes manufacturing relatively less competitive and the feedback loop of lower employment reduces domestic demand.

- Government increases the supply of bonds to mitigate impact falling tax receipts. The US government attempts to mitigate the negative impact of China grabbing US demand, as described, through increased borrowing and spending to help alleviate impact of unemployment (falling tax receipts from workers and manufacturing sector); in short more government spending in order to replace lost local demand because of Chinese buying Treasury bonds. This is usually the case.

Now, it is precisely this additional borrowing by the US government which increases the supply of bonds which in turn pressures interest rates higher. [Additional private borrowing to support the prior standard of living also creates problems of its own as this borrowing is primarily spent on consumption and/or real estate—neither of which produce a cash flow to retire the debt.]

To simplify, remember that a rising current account deficit means lower tax receipts to government.

Summary:

Net foreign buying of US bonds

- Slows US growth

- Increases debt

- It does not lower interest rates

- Foreign buying increases fiscal deficits

- Adds to the current account deficit

So, where is the great privilege here? Why do other countries get so worked up when someone starts buying their bonds, as they buy US bonds? For example Japan makes sure it sterilizes any impact of China buying its bonds by turning around and buying a similar amount of US Treasuries to neutralize the impact. If this reserve status was so great why would Japan not embrace China’s buying of its bonds?

A French finance minister, Valéry Giscard d’Estaing, coined the phrase “exorbitant privilege” to explain the role of the US dollar in the global monetary system (even though the French, and the rest of Europe for that matter, piggybacked on artificially low exchange rates relative to the dollar after the War and never revalued—talk about no good turn goes unpunished.)

But Mr. Giscard should have known better. He would have had he read anything from economist Robert Triffin who expressed this warning about a US dollar replacing gold in the monetary system:

In 1960, Triffin testified before the United States Congress and warned of serious flaws in the Bretton Woods system. His theory was based on observing the dollar glut, or the accumulation of the United States dollar outside the US. Under the Bretton Woods system, the US had pledged to convert dollars into gold, but by the early 1960s, the glut had caused more dollars to be available outside the US than gold was in its Treasury. As a result, the US had to run deficits on the current account of the balance of payments to supply the world with dollar reserves that kept liquidity for their increased wealth.

Despite the end of Bretton Woods, the dollar’s role is still hugely dominant as the reserve currency. And guess what: the US runs a large and chronic current account deficit with the rest of world.

So, if another country took on the burden of reserve currency status, or some incarnation of Keynes idea at the Bretton Woods conference—the bancor—is reincarnated, the US economy will be much better off.

So, the next time Mr. Snakeoil tries to scare you with the usual “loss of reserve currency status” canard, tell them: That’s great! I am investing in America.

Thank you.

Jack Crooks

President, Black Swan Capital

www.blackswantrading.com

Goldman Sachs’ estimate of September rate-hike odds continue to collapse faster than Hillary Clinton as the absence of a clear signal from a series of speeches by Fed officials (concluding with Lael Brainard’s headfake). Goldman have reduced their subjective odds for a hike next week to 25% from 40% previously (still above market expectations of 13%) but remains hopeful for December. However, as Fed-whisperer WSJ’s Jon Hilsenrath warns, Yellen faces record levels of dissent as she “confronts a divided group of policy-makers.”

also:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Executive ability is deciding quickly and getting somebody else to do the work.

John G. Pollard

Many individuals sit back and look wistfully at the 1st stage of the Gold Bull Market they missed. It is interesting that people focus on what they lost but not what they might miss. Since Gold topped out in 2011, many sectors took off; one could have deployed a portion of one’s funds in any of these sectors and walked away with healthy gains. Instead, the classic Gold bug clung to Gold and let all these opportunities slide away.

Never live in regret, life is much too valuable for that. There is always another bull market, why focus on one market only. Many people fixate on the precious metals markets because many hard money experts continue to come out with gloom or doom scenarios. Never listen to anyone giving you a script that is painted with strokes of Panic. No one can function properly once he or she succumbs to panic; reason goes out the window, and nonsense takes over.

There is a way that Gold bugs and hard money experts can have their cake and their pie, but that would entail a change in perspective. If you can do this then, the process is rather simple. We will provide these details shortly; please bear with us.

Precious metals will trend higher one day but why fixate on that day only, what about today, and all the other opportunities you might be sacrificing because you have restricted your vision. If you cling to a particular outlook, you have reduced your line of sight by a significant margin. This is why Gold bugs openly state that they will not support “Fiat”, and they will rather embrace Gold and Silver than the stock market which is funded by worthless paper. To which we respond “oh really” well then what are these bugs doing when they buy Gold; are they not hoping that Gold soars in value and what will it rise in value, oh yes, worthless dollars.

If you cling to one perspective, you cannot see the full picture. How about looking at the picture from every angle. You are Gold bug or hard money fan; here is how you can have your cake and your pie

Why not embrace the equities bull, use the worthless money to get more cheap money and then use some of this paper to buy the Gold and Silver you crave; this perspective is lost to the on many because all they see is Gold and nothing else. Had they embraced this point of view, they would have been embraced the equities bull and multiplied the worthless paper (money) they had. Then, they could have used some of this worthless money to buy real money (Gold), and maybe then they would not be so obsessed with the Gold Markets. The Gold they obtained would technically be free as they used paper profits generated by embracing assets they typically would not; this extra paper was used to bankroll the purchase of new bullion. In effect, they would be pulling a page out of the central banker’s books. A perception depends on the angle of observance; alter the angle and you modify the perception.

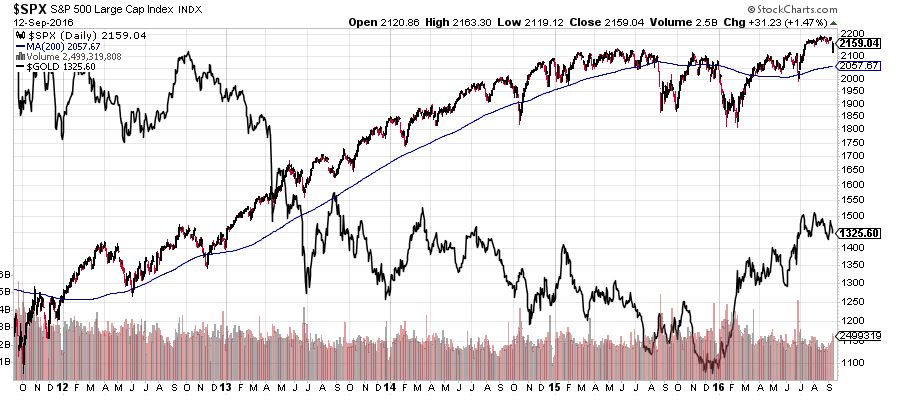

This chart illustrates how Gold performed vs. the SP500 over the past five years; in comparison, Gold has taken a beating and is now making a modest comeback. This took place in the face of the greatest money printing efforts from central bankers in the history of this planet. What happened to the hard money argument that Gold will rise as the money supply soared. Instead the opposite took place, the more money central bankers created, the more Gold fell.

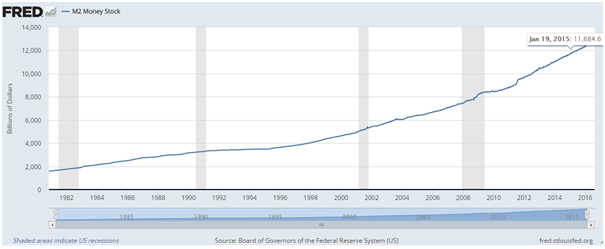

This chart clearly illustrates that since 1980, Gold has not fared as well as it should have. Look at how the money stock has increased. The price of Gold should have continued to trend upwards, and it should be north of $2500. Instead, it cannot even trade to $1400. There is a reason for this; central bankers have managed to recreate reality. By brainwashing the masses and creating new definitions for inflation, they have convinced the masses that Gold is an old relic not worth focusing on, but that is a story for another day.

This is why it is important not to be belong to any group and why it is more important to concentrate on the trend. Don’t fall in love with Gold; it is just another investment; it will trend up for some time, then pull back and correct firmly and then trend up again. Nothing trends up forever, well, stupidity being the only exception.

Once again, the point we are trying to make is that you should not live in regret; the 1stphase of the Gold bull is over, but the next phase will be even stronger. We have a high-end target of $5000 for Gold and to be honest with you, we hope it does not trade to $5000, and we are wrong. Inflation will be quite significant if Gold hits $5000, so those fools hoping for Gold $25,000 or $50,000 have no idea how terrible things would be if Gold traded to those targets. If, Gold ever trades to $50,000, the world as you know it will be over. Chaos will be the order of the day. We will be facing a situation that will be even worse than the Greate Depression. Luckily most of these guys are full of hot air, and it is more likely Central bankers will embrace Gold before Gold trades to those targets.

Conclusion

Forget the noise, focus on the trend. Experts are there to confuse and not enlighten one. We have never claimed to be experts, at most we will settle for the title of advanced students of the Market. The market is a complex beast, and there is always something new you can learn. Those that refuse to accept this are usually punished severely.

Moreover, don’t forget, you can have your cake and your pie. Use worthless paper to make more paper and then use some of this paper to buy (Real Money) Gold and or Silver bullion. In such crazy times, it would be prudent for everyone to have a portion of his or her funds in Gold and Silver bullion. If you have no position in bullion, use strong pullbacks to open new positions.

Ability is a poor man’s wealth.

M. Wren

….related: Gold and Gold Stocks Correction Continues

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair