Timing & trends

1. Complexity Failure Crisis & Panic

1. Complexity Failure Crisis & Panic

by Michael Campbell

Intensive Government management of our economy cannot solve the problems we have. There are too many variables involved. Massive debt problems, commodity prices, currency values, the actions of Governments at all three levels, International Government actions. They’ve all led to untenable derivative positions and banking system problems could trigger a significant liquidation panic at any time.

2. David Morgan Urges Investors to Obtain REAL Money outside the Banking System Immediately

David Morgan tells us how long he thinks the correction in the metals will last, why he believes this November’s election is less important than you might think and also talks about a key event coming up that could put a lot of pressure on the U.S. dollar

3. WHY 2017 is The Threshold to Chaos

by Martin Armstrong

I have been warning that 2017 was the Year of Political Hell with four major referendums/elections that would undermine the confidence in government – BREXIT, US Presidential Elections, French Elections, and Germany Elections. These four events hold the potential to overturn the expectations of the future.

So let me get this straight… last week the US reports weaker employment and economic data and the markets are up triple digits? Markets seem to be happy with the belief that interest rates will not go up in September. For volatility, what’s worse; weak economic data or continued record low interest rates?

So let me get this straight… last week the US reports weaker employment and economic data and the markets are up triple digits? Markets seem to be happy with the belief that interest rates will not go up in September. For volatility, what’s worse; weak economic data or continued record low interest rates?

What’s really scary is the US anemic economy is better than Europe with the Brexit contagion possibly going through Europe in next year elections. We haven’t even begun to speak about the US elections in November.

More than ever the average investor needs to find ways to reduce risk from this volatile market. It’s little wonder on our website at www.triviewcapital.com, we love John Maynard Keynes quote of “the market can stay irrational longer than you can stay solvent”.

Over the last 4 years, we have continued to be frustrated with the public markets, and more than ever believe alternative investment strategies are needed to balance the public markets irrational roller coaster cycle. When the market corrects, we believe it won’t be 100 points, it’ll probably drop 400+ points when it does. The challenge is what comes first, the big drop or increased interest rates by the US Fed? If the drop happens before the US Fed announces rate increases in the fall, it could mean a second big drop over the next 4 months.

We’re proud to launch a new program with Money Talk listeners and readers; it’s called “8 ways to 8%”. Between now and up to the World Outlook Conference 2017, we will highlight 8 different strategies to provide alternative investment strategies that target 8% or better annual yields on real cash flow businesses in multiple sectors. Of course we look forward to introducing you to these investment opportunities at the event but for those who listen to the show or subscribe on line, you’ll be able to take advantage of these strategies prior to the February event.

We plan to provide alternative strategies over coming months just in case you believe “the market can stay irrational longer than you can stay solvent”.

Craig S Burrows ICD.D

President & CEO, CCO TriView Capital Ltd.

Mortgage penalties are one of the most important aspects of choosing a lender and a mortgage term, but surprisingly one of the least asked questions from prospective clients. Although saving .1% on a $300,000 mortgage would save $300 per year, adding up to $1500 over 5 years, choosing a lender with a more favourable penalty calculation could be the difference between a $2,500 penalty and a $14,500 penalty. Pinching pennies to cost you dollars.

Mortgage penalties are one of the most important aspects of choosing a lender and a mortgage term, but surprisingly one of the least asked questions from prospective clients. Although saving .1% on a $300,000 mortgage would save $300 per year, adding up to $1500 over 5 years, choosing a lender with a more favourable penalty calculation could be the difference between a $2,500 penalty and a $14,500 penalty. Pinching pennies to cost you dollars.

So how do banks and other lenders calculate penalties?

First off, there are closed mortgages and open mortgages. Closed mortgages incur penalties when you break the mortgage and open mortgages have no penalty to break them. Generally, most mortgages are closed because the interest rate is best on closed mortgages. Lines of Credit are open (and a higher rate than a closed variable mortgage), generally fixed mortgages are not open. If the mortgage is closed, there are two primary types of penalties: 3 months interest and Interest Rate Differential (IRD).

3 months interest penalty

Most borrowers are aware of the standard penalty, which is 3 months interest. It’s also quite easy to calculate as well. $300,000 mortgage @3% is $9,000 per year, divided by 4 is $2,250. 3 months interest is the maximum penalty if you are taking a closed variable, although some banks calculate the rate at the Prime rate and some calculate it based on the net rate (most of the time, market rates are Prime minus a discount). This can make choosing a variable rate a more attractive option and in general, we are usually recommending a variable to our investor clients. However, most borrowers don’t realise that this is not the only penalty that may apply if you take a fixed rate mortgage.

Interest Rate Differential

Here’s the big one. I have had some big IRD’s in my career. One from a few years ago was about $76,000 on a $700,000 mortgage. Another was $200,000 on a $1,000,000 commercial mortgage. The whole purpose of the IRD penalty is to ensure the bank doesn’t lose money on your mortgage. An IRD is effective if the current market rates for the same term remaining is lower than your current rate. If it is, the penalty is the difference between the rates, over the remainder of the term. So if you borrow money from the bank at 6% and then a few years later rates are 4%, you would want to refinance to get the better rate, right? The problem is, you signed a contract with the bank to pay that amount. And the bank also likely has a contract in place to pay someone else a rate of return, probably around 1.5% less than what you are paying. The bank is likely paying someone else 4.5% for the money they lent to you for 6%, so they wouldn’t want to just let you get out of the contract for free. So is it fair to penalize you to get out of your contract early? Well, yes….as long as it is fair. The problem is, banks don’t have a “fair” calculation.

How the banks “get you”

First, let’s explain how a “fair” penalty calculation should look. Let’s use current interest rates, and assume rates don’t change over the term of your mortgage.

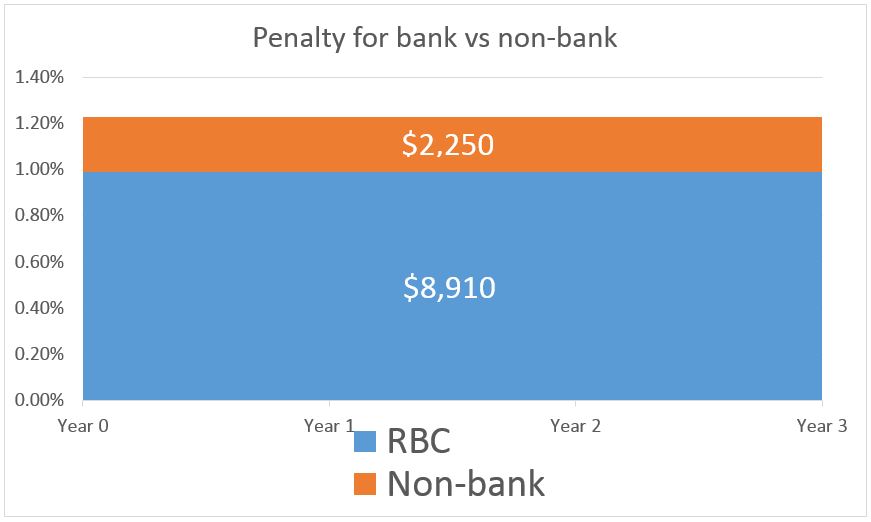

$300,000 mortgage, at 2.49% for 5 year fixed. You keep it for 2 years and break it with 3 years remaining. With a non-bank lender, their current 3 year term is 2.24% so your penalty would be .25% on $300,000 over 3 years, about $2,250 (the 3 month interest penalty would be ~$1,850 but since it is less the IRD applies here).

Let’s try this again with a major bank. How about RBC, just because…well, they’re the biggest. The big difference here is that the banks manipulate posted rates in a way that creates large, unfair penalties. Really, what purpose do posted rates have today anyways? If you pay the full price for posted rates you have probably been living under a rock for the past decade and a half or two.

$300,000 mortgage, 2.49% 5yr fixed (4.64% posted 5 year, so a discount of 2.15%). Posted 3 year rate is 3.65%.

This will probably need some visualization to understand:

So in essence, the non-bank is charging a difference of .25%, and the major bank will use the difference of .99% (2.49% vs 1.5%). This is a quick graph showing the difference in cost:

In essence, it is pure manipulation of the posted rates that cause these high penalties as they heavily discount the long term rates and offer small discounts for short term rates. As of writing this, the discount off a 3 year fixed may be around 1.4% whereas the long term rates are over 2% discounted.

What to watch out for

Keep in mind, most lenders do offer to port your mortgage if you sell but a lot of our clients have been finding it difficult to port when they sell. We have had clients who have actually improved their finances since buying their home but now aren’t able to port their mortgage. An example is when you take a 5 year fixed rate of say 2.49%, they use the actual rate to qualify you. But, if you are porting and have less than 5 years remaining, the “qualifying rate” is actually 4.74% right now. This can put you in a situation where you may be paying a large penalty to break your mortgage and simply getting a similar rate on the market, which can often be a net loss.

How to avoid the penalties

The easiest way to avoid the penalty is to generally take a variable rate or a short term fixed rate, or if taking a long time fixed rate go with a non-bank lender. Make sure you understand how lenders port as well. Credit Unions for instance can’t port outside of their lending area so if you get a mortgage with Vancity in Vancouver and want to sell and buy in another province in a few years, you may be faced with a large penalty.

Most lenders do allow for a pre-payment on your mortgage so if you have some extra cash lying around and you know you will be paying a penalty, check out how much you can pre-pay per year. It usually varies between 10% and 20% per year.

Why you may still want to use a bank

If you are just taking a cookie cuter mortgage and want the best rate and terms, non-bank lenders that are only accessible through mortgage brokers are usually your best bet. They generally have lower rates than the big banks and their penalty calculations are generally better. That said, non-bank lenders cannot offer the same products as major banks can. Some of the products banks can offer that non-banks can’t include:

– Home Equity Lines of Credit

– Best rates and terms on rental properties

– New to Canada and Non-resident mortgages

– Net worth or equity mortgages (which are nearly extinct now)

– Many other types

Just make sure you are aware of the differences and make sure you ask the right questions. IF you think you may be selling shortly and may not buy something else and port, you should probably be taking a short term rate or a variable rate.

If you would like to get a professional opinion to compare different options, contact Kyle Green at 604-229-5515 or Kyle@GreenMortgageTeam.ca.

Lehman Brothers’ bankruptcy, eight years ago, reminds us that we can rarely predict a calamity

Next week we observe not only one anniversary, but two.

The first, of course, is the 15th anniversary of the Sept. 11 terrorist attacks on the World Trade Center and the Pentagon. The second is the eighth anniversary of Lehman Brothers’ collapse.

Unsurprisingly, the former is getting the lion’s share of attention. And the latter is getting virtually no attention.

And that’s a shame, since many valuable investment lessons can be learned by reviewing it from the emotional distance of eight years.

For those of you with hazy memories, the New York-based company declared bankruptcy Sept. 15, 2008. It had been the fourth-largest investment bank in the U.S.; its bankruptcy was the biggest in U.S. history.

The aftershocks were disastrous…..continue reading HERE

….also Michael with some smiles and head scratchers:

it is my firm conviction that we will be involved in a World War that will be initiated by an Electromagnetic Pulse (EMP) weapon detonated over the continental United States.

it is my firm conviction that we will be involved in a World War that will be initiated by an Electromagnetic Pulse (EMP) weapon detonated over the continental United States.

That being said, this piece summarizes recent events that reinforce such a conclusion, a conviction that is shared by world leaders, senior military personnel, and prominent analysts, as well as being a general consensus of opinion worldwide. As of this writing, the German government has instructed its citizens to prepare for a forthcoming disaster by stockpiling at least 10 days-worth of food and 5 days of water. In Berlin, they are considering bringing back mandatory conscription (a draft) in view of the influx of Muslim aliens entering Europe.

….related:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair