Gold & Precious Metals

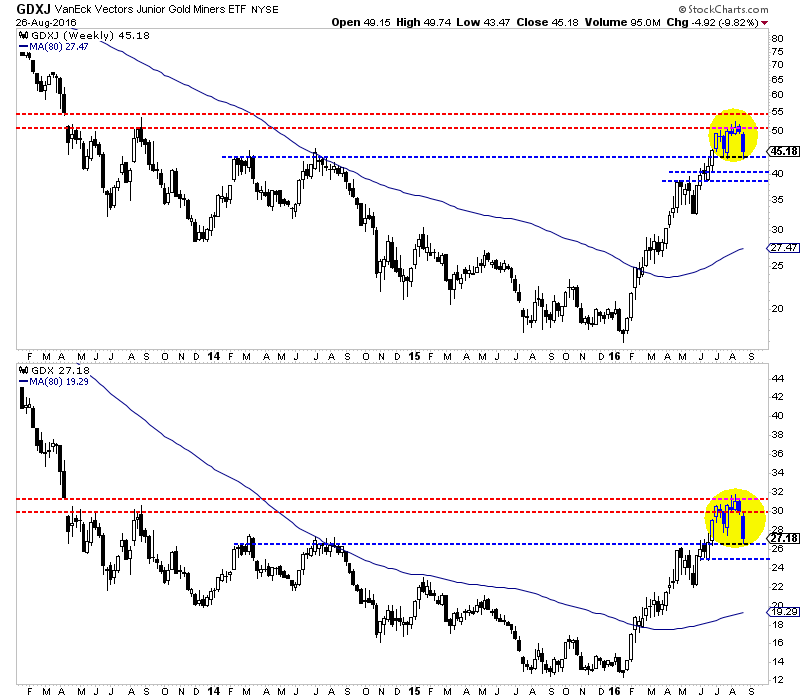

Last week we projected 5% to 10% downside in the gold stocks. Well, not to butter my own bread but GDX and GDXJ both lost 9% on the week. That being said, I believed that the weakness would be limited and miners could rebound to new highs in September. While that possibility remains, there is a chance this correction could go a bit deeper and perhaps last longer.

The weekly candle charts below show that the miners are correcting after failing to break into a “thin zone” of resistance. GDX has broken below its July lows and corrected as much as 16%. It has support at $25-$26 and that includes the Brexit gap. Also, the 38% retracement of its entire rebound is just below $25. Meanwhile, GDXJ has yet to break its July low in the $43s. It has corrected as much as 17% but could end up testing $39-$41. The 38% retracement of its entire rebound is a hair below $39.

GDXJ, GDX Weekly Candles

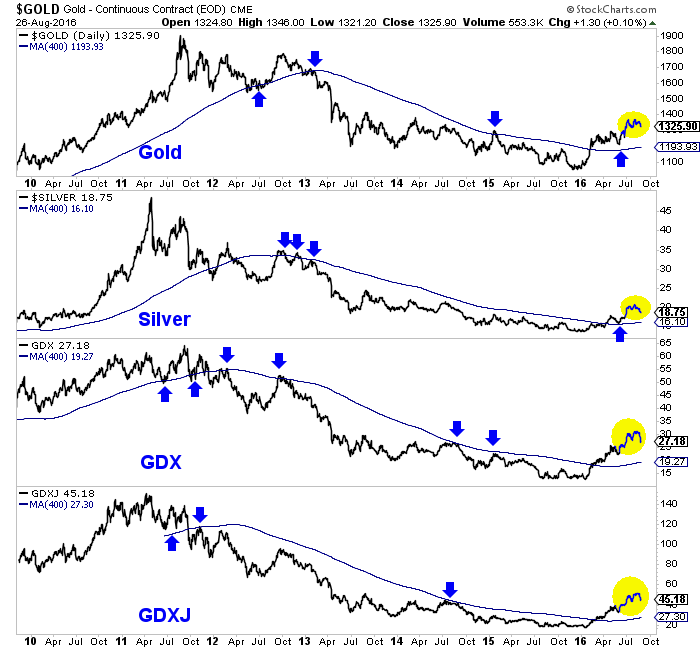

Whether the correction lasts longer or evolves into a long consolidation, precious metals will remain in a bull market. It is hard to argue against the chart below. We plot Gold, Silver, GDX and GDXJ along with the 400-day moving average which is an excellent indicator of the primary trend. The sector sits comfortably above the 400-day moving averages which are sloping upward for the first time in years.

While we expected this correction, we did not anticipate there would be a chance for a larger correction. If you believe we are in a new bull market, as I do, then the path to financial success is buying and holding and buying weakness. (Our guidance for selling, we’ll get to another time). If I were holding too much cash or missed the epic rebound, I would be taking advantage of further weakness. Buying 20% to 25% weakness in a bull market (especially one that is only months old) will likely payoff in the long run.

Jordan Roy-Byrne, CMT, MFTA

related:

Citizens of the developed world are watching Venezuela’s descent into financial and political chaos mostly, it seems, with amused detachment, safe in the assumption that we’ll never end up hunting our cats and dogs for food.

Citizens of the developed world are watching Venezuela’s descent into financial and political chaos mostly, it seems, with amused detachment, safe in the assumption that we’ll never end up hunting our cats and dogs for food.

But – since Europe, Japan and the US are making essentially the same mistakes as Venezuela’s past and present governments – we might want to question that certainty. Consider what’s happening in the third biggest US city:

Chicago’s detective force dwindles as murder rate soars

(Reuters) – Every two weeks, Cynthia Lewis contacts the detectives investigating the homicide of her brother on Chicago’s south side almost a year ago.

They have had no success finding who shot Tyjuan Lewis, a 43-year-old father of 15, near his home in the quiet Roseland neighborhood of single-family houses.

The death of Lewis, who delivered the U.S. mail for 20 years, is one of hundreds of slayings in 2015 that have gone unsolved as the number of homicides soared in Chicago, piling pressure on a shrinking detective force.

In a city with as many as 90 shootings a week, homicides this year are on track to hit their highest level since 1997.

Chicago’s murder clearance rate, a measurement of solved and closed cases, is one of the country’s lowest, another sign of problems besetting police in the third biggest city in the United States.

Detectives and policing experts interviewed this week said Chicago struggles to solve murders because of declining numbers of detectives, the high number of cases per detective and because witnesses mistrust the police and fear retaliation from gangs.

The number of detectives on the Chicago police force has dropped to 922 from 1,252 in 2008. One detective who retired two months ago said investigators are overwhelmed. “You get so many cases you could not do an honest investigation on three-quarters of them,” he said in an interview. “The guys … are trying to investigate one homicide and they are sent out the next day on a brand new homicide or a double.”

Why should a city as apparently affluent as Chicago have such a nightmarish crime situation? Because it’s not really that affluent. Like most of the rest of the formerly-rich world, Chicago ran out of money years ago and has been more-or-less secretly borrowing to cover the shortfall. Its public sector pensions, for instance, pay retired workers far more than the city can afford – but are legally uncuttable according to a recent court ruling. Here’s that story:

Pension ruling another blow to Chicago taxpayers — and Emanuel

(Chicago Tribune)- The Illinois Supreme Court ruled unconstitutional another pension reform law on Thursday, this one affecting Chicago and splashing more red ink on fragile, debt-ridden city finances.

The court’s decision to toss Chicago’s pension reform law, which the Illinois legislature approved in 2014 as an attempt to rescue pension funds for municipal workers and laborers, was not a surprise. Nor is its ripple effect: As the opinion states and unarguable math attests, those two funds remain on track to go insolvent “in about 10 and 13 years, respectively.”

The court previously had twice ruled that an Illinois Constitution pension clause protects retirement benefits promised from a worker’s start of public employment. The law the justices rejected had required certain city of Chicago workers to pay more toward their pensions, scaled back cost-of-living increases upon retirement, and raised the retirement age. The court ruled that those changes violate the constitution’s provision that membership in any pension or retirement system “shall be an enforceable contractual relationship, the benefits of which shall not be diminished or impaired.”

The decision repudiates Mayor Rahm Emanuel’s strategy for salvaging a vastly underfunded Chicago pension system that also covers public safety workers — police and fire — and Chicago teachers. Emanuel persistently has argued that because 28 of 31 unions affected by the 2014 reform law had agreed to it. Emanuel said that because the law would shore up the funds in the long run and thereby protect benefits for retirees, it would meet constitutional muster.

But the Supreme Court disagreed. In a 2015 ruling rejecting a pension reform law affecting state lawmakers, the justices faulted state lawmakers for not making adequate payments into their pension system. Thursday’s ruling similarly blamed city leaders for failing to make adequate payments into City Hall’s pension funds: “The pension code continued to set city contribution levels at a fixed multiple of employee contributions. This contribution level had no relationship to the obligations that the funds were accruing.” To rule in favor of the law would mean that the court would have to “ignore the plain language of the constitution.”

Translation: City and state politicians have known well that they were awarding pension benefits that Illinois governments cannot afford. Rather than properly fund pension systems, the politicians have spent on other priorities the tax revenues they should have set aside to fulfill all the generous retirement promises they made to their friends in public employees unions.

Now that this mess has become impossible to hide, new borrowing is getting harder and tax revenues aren’t sufficient to maintain previous levels of health, safety and livability. The result: a steady march down the affluence ladder towards a living standard that would be familiar to people in Brazil or India.

And it’s not just Chicago. Lots of other developed-world cities, states and countries are in similar predicaments, mostly because previous leaders over-promised on pensions that can’t be paid without skimping on everything else. See State pension fund gap approaching $1 trillion.

What does this mean? Over time – and not all that much time – life will get a lot harder for millions of people who are unprepared for it. Crime will metastasize, at-risk kids will go straight from school to prison, roads won’t be maintained, garbage won’t be picked up. It will, in short, become extremely unpleasant for the developed world’s former middle class. Then will come the civil unrest, and just like that your neighborhood looks like those Argentina videos.

The sad thing is that none of this is a surprise. As with so much else that’s going wrong, it traces directly back to the 1971 decision to hand the world’s governments an effectively unlimited monetary printing press. What has followed tracks perfectly with the view of human nature espoused by the Austrian school of economics, which is that we’re potentially brilliant but also corruptible. Since the ability to create money out of thin air is the ultimate temptation, of course nations, states and cities have all borrowed too much and made too many unsupportable promises.

And of course they can’t easily shed these obligations, because one of the laws of public life is that once created, a program gains beneficiaries who will defend it to their dying breath. So debt and unfunded liabilities keep expanding until the bill comes due. Then look out, cats and dogs.

related by Michael Campbell:

For Friday August 26, 2016 3:00 PST

DOW – 33 on 300 net advances

NASDAQ COMP – 5 on 150 net advances

SHORT TERM TREND Bullish

INTERMEDIATE TERM TREND Bullish

STOCKS: Today was all about the Fed. When Janet Yellen’s speech was made public, the Dow seemed somewhat satisfied and rallied to be up over 100 points.

Then Vice Chair Stanley Fischer decided he needed some publicity and came out with a more hawkish statement on interest rates and the fear of a quarter point rise in Fed Funds caused an immediate swoon.

GOLD: Gold was flat. In spite of a sharp rise in the dollar and higher rates. Actually, the yellow metal was much higher earlier in the day so it did drop somewhat.

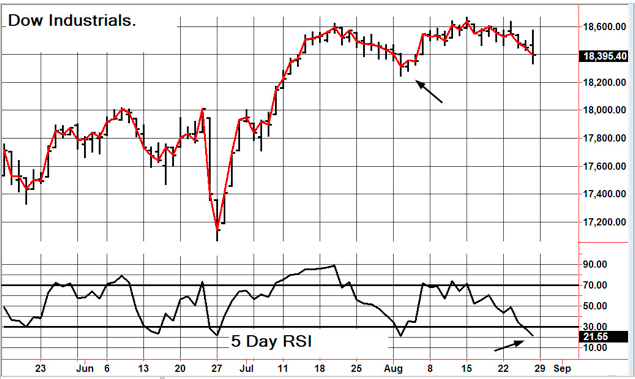

CHART: This is the same chart as yesterday. The Dow is even more oversold (bottom arrow). It is also approaching the level that stopped the last decline (top arrow). It should move higher soon. If not, it is a sign of a more significant decline.

BOTTOM LINE: (Trading)

Our intermediate term system is on a buy.

System 7 We sold the SSO at 71.17 for a loss of 1.29. Very disappointing.

System 8 We are in cash. Stay there.

News and fundamentals: The second revision of Q2 GDP came in at 1.1%. Even worse than the first estimate. The trade deficit was $59.3 million, better than the expected $63.2 billion. Consumer sentiment was 89.8, lower than last month’s 90.4. On Monday we get the Dallas Fed mfg survey and personal income.

Interesting Stuff:

Ordinary riches can be stolen; real riches cannot. In your soul are infinitely precious things that cannot be taken from you. ————Oscar Wilde

TORONTO EXCHANGE: Toronto was up 9.

BONDS: Bonds were down sharply.

THE REST: The dollar was sharply higher. Silver was mildly higher. Crude oil was flat.

Bonds –Bearish as of July 14.

U.S. dollar -Bearish as of August 16

Euro — Bullish as of August 16.

Gold —-Bearish as of August 22.

Silver—- Bearish as of August 19.

Crude oil —- Bullish as of August 3.

Toronto Stock Exchange—- Bullish from January 22.

We are on a long term buy signal for the markets of the U.S., Canada, Britain, Germany and France.

related:

Larry Edelson on: Cycles Hitting Now!

Today’s videos and charts (double click to enlarge) include Gold’s Battle for $1392 and Silver Inverse Head & Shoulders Bottom Chart:

Gold & Silver Bullion Video Analysis

Precious Metal ETFs Video Analysis

SF60 Swing Trades Video Analysis

Thanks

Morris

website: www.superforcesignals.com

related: Gold & Silver Trading Alert: Suspicious Reversal in Gold

After four grinding years of falling metal prices and vanishing market capitalizations, we have seen a stunning shift in market sentiment since mid-January, says Matt Geiger of MJG Capital. Multiple physical commodities are now in technical bull markets, and resource equities in particular have enjoyed a spectacular 2016 thus far. Geiger highlights several companies poised to take advantage of the boom.

Metal prices are again on the rise. Particular standouts include: silver, lithium, zinc, gold, platinum and palladium. All of the aforementioned metals have entered new technical bull markets in 2016 and seem to be building momentum. It took four painful years, but this proves yet again that low prices are the best cure for low prices. When the price of a particular commodity drops precipitously, two phenomenons inevitably occur: (i) higher cost suppliers of the commodity cut production and (ii) buyers of the commodity purchase more in real terms. These twinning events may take a while to play out, but they inevitably do.

M&A activity has picked up, particularly in Q2/16. This is great news for quality development projects not yet owned by a major producer. The recent bear market has a left a dearth of near-term production candidates and those still remaining are that much more valuable to a potential acquirer. Additionally, if this indeed becomes a multiyear bull market, then explorers too will receive increased attention. Shareholders of well-managed prospect generators are poised to do very well over the coming few years.

Here are a few companies that I believe are well positioned to ride the bull.

Golden Arrow Resources Corp. (GRG:TSX.V; GAC:FSE; GARWF:OTCPK) has been a strong performer in 2016. The company, founded by the experienced Joe Grosso, has been exploring and developing precious metal projects in Argentina for over two decades. Golden Arrow’s flagship asset, the Chinchillas project in Jujuy Province, looks increasingly likely to reach production by the end of 2017 thanks to a joint venture with silver heavyweight Silver Standard Resources Inc. (SSO:TSX; SSRI:NASDAQ). Once the Chinchillas joint venture begins generating cash flow (or, conversely, is bought outright by Silver Standard), the company will return to its roots as a prospect generator focused solely on Argentina.

The market has rewarded Golden Arrow so far in 2016 for the following reasons:

- Chinchillas offers near-term production potential with a very affordable initial capex (thanks to synergies with JV partner Silver Standard and its producing Pirquitas asset).

- Due to its massive size and relatively low grade, Chinchillas is a classic “optionality play” with significant leverage to the price of silver (which has been the best performing commodity so far in 2016).

- Argentina’s election of pro-business President Mauricio Macri has opportunistic mining investors streaming into the country.

Golden Arrow’s Chinchillas project is a textbook optionality play—a relatively low-grade deposit that contains over 200 million silver-equivalent ounces. One key takeaway is that this is a massive project, particularly when you consider that at least 50% of the land package has yet to be explored. An ultimate resource of 500 million silver-equivalent ounces is optimistic but not impossible.

Golden Arrow is likely to “add another horse to the stable.” This acquisition would likely be similar in geology to Antofalla, and the goal would be to discover another Chinchillas-like deposit. The company’s deep experience in Argentina will give it a leg up in any negotiations that may take place.

Golden Arrow is likely to “add another horse to the stable.” This acquisition would likely be similar in geology to Antofalla, and the goal would be to discover another Chinchillas-like deposit. The company’s deep experience in Argentina will give it a leg up in any negotiations that may take place.

Almadex Minerals Inc. (AMX:TSX.V) is another company that has taken off, with a 500% year-to-date gain. The company was formed just 12 months ago, when well-respected Almaden Minerals spun out its prospect generation business so the company could focus on Ixtaca. We started buying in Q4/15, when Almadex’s market cap was equal to its working capital position. In hindsight, this was a ludicrous proposition considering management’s multidecade exploration expertise in Mexico.

In the first half of 2016, the company was relatively quiet on the prospect generation front. Instead, the company’s share price was buoyed by positive developments surrounding Almadex’s royalty and equity holdings. There were three major developments:

- The materialization of Gold Mountain Mining Corp.’s (GUM:TSX.V) Elk Gold project into a legitimate British Columbia development play, on which Almadex owns a 2% NSR royalty

- The revitalization of the Ixtaca project, on which Almadex owns a 2% NSR royalty

- The sale of El Encuentroto to McEwen Mining Inc. (MUX:TSX; MUX:NYSE) for CA$250,000 (Almadex retained a 2% NSR royalty on the property)

However, just within the past two weeks, the company has demonstrated why the prospect generation business can be so exciting. On Aug. 8, the company announced an intersection of 163.5m at 0.68 g/t gold and 0.29% copper at its fully owned El Cobre project. These results were only for the top half of the hole and, sure enough, the company announced earlier this week that another 150.9m at 0.55 g/t gold and 0.22% copper was intersected below the initial zone of mineralization. Assays ended at 540m, with the news release stating that “Porphyry style alteration continues to the end of the hole, currently at ~890 meters depth and advancing.”

While the full results from hole EC-16-010 have yet to be received, this already looks to be a legitimate discovery of a large copper-gold deposit. Over the coming months, Almadex will bring additional drill rigs to the property to both (a) conduct stepout drilling around hole EC-16-101 and (b) test several anomalous areas on the property that have yet to be drilled. These next six months hold the potential for immense value creation at El Cobre.

Nevsun Resources Ltd. (NSU:TSX; NSU:NYSE.MKT) remains my favorite mid-tier base metal play. While Nevsun’s share price has lagged many of its peers, the company has had a sensational 2016 from a business perspective. The market will soon catch on.

There have been multiple positive developments thus far this year, but Nevsun’s most significant was the acquisition of Reservoir Minerals and its world-class Timok copper-gold project in Serbia. Timok has become one of the most significant undeveloped base metal deposits in the world due to its high grade, massive size and proximity to existing mining infrastructure.

An April 2016 PEA on Timok’s Upper Zone outlines the project’s exceptional economics, including an initial capex of $213 million; a post-tax NPV of $1 billion (at 8% discount rate and spot metal prices); a post-tax IRR of 86%; and a payback of less than one year.

For a project of this size, these economics are virtually unheard of. Additionally they don’t take into account Timok’s Lower Zone, which may have a potential production life of 15–20 years. We’ll learn more about the Lower Zone over the coming year as Nevsun has initiated an aggressive drilling program. In a best case scenario, the Lower Zone could double or triple the overall value of Timok.

Developments at the Bisha mine in Eritrea have been overshadowed by the high-profile Timok deal. However, there have been several significant developments this year worth noting, including Bisha’s zinc expansion coming in on time and underbudget and Q1/Q2 supergene copper ore production of 55.8 million pounds at a C1 cash cost of $1.04 per payable, which was above guidance of 40-50 million pounds and under the cost guidance of $1.20 to $1.40 per payable pound of copper.

Additionally, Newsun announced that it had increased its total land package of exploration licenses to 814 square kilometers in Eritrea’s Bisha VMS District. This represents a 1,891% increase from the 41 square kilometers the company had before the deal. This acquisition solidifies my belief that Nevsun will find enough ore to keep the Bisha mine producing for another three decades. This may be a VMS district on the same scale as Manitoba’s Flin Flon district, which has seen 25 producing mines in the past century. I’m thrilled to see what the company can discover elsewhere in the district over the coming years.

Matt Geiger is the general partner at MJG Capital, a limited partnership focused on long-term capital appreciation through investments in natural resources.

1) The following companies mentioned in this article are sponsors of Streetwise Reports: Golden Arrow Resources Corp. The companies mentioned in this article were not involved in any aspect of the article preparation. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Matt Geiger: I or my family own shares of the following companies mentioned in this article: Golden Arrow Resources Corp., Almadex Minerals Inc. and Nevsun Resources Ltd. I personally am or my family is paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds under my company’s control hold the following companies mentioned in this article: Golden Arrow Resources Corp., Almadex Minerals Inc. and Nevsun Resources Ltd.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) Patrice Fusillo assisted in compiling this article. Ms. Fusillo is an employee of Streetwise Reports. She owns, or her family owns, shares of the following companies mentioned in this article: None. She personally, or her family, is paid by the following companies mentioned in this article: None.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview or the time an article is accepted for publication until after it publishes.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair